Financial advisors have many ways to add value to clients’ investment portfolios, from selecting an appropriate asset allocation to rebalancing when appropriate. However, because the investor ultimately only gets to spend what they can keep after taxes, another important way advisors can add value to a portfolio is to improve its tax efficiency; after all, if the same returns can be generated in a more tax-efficient manner, in the end, investors will generate more spendable wealth (a form of ‘tax alpha’). And when it comes to individual investors and their typical mix of investment accounts and retirement accounts, one of the best ways to enhance portfolio tax efficiency is through strategic asset location, where the advisor places assets into taxable or tax-advantaged accounts depending on the assets’ specific characteristics.

Implementing an asset location strategy begins with identifying the yield, tax rate, and potential tax drag of each investment in an individual’s portfolio. The investments are then sorted into an asset location priority list based largely on tax efficiency, which can be used to help identify where to house each type of investment, with the least tax-efficient holdings being placed into the most tax-advantaged account. Which means a stock fund with a low yield (and low tax drag) might be placed in a taxable account, whereas a high-yield bond fund (with high tax drag) might be placed in a tax-deferred account, thereby reducing the amount of taxable investment income in the current year.

In addition to using asset location to strategically place investments, advisors can further enhance tax efficiency by replacing the use of broad-based index funds with a corresponding pair of funds – one low-yield tax-efficient fund and another higher-yield, tax-inefficient fund. This process, called “yield splitting”, emulates broad-based index funds in such a way that allows for their component (low- and high-yielding) parts to be invested into separate accounts by tax efficiency.

For example, with a yield-split asset location strategy, rather than investing in a single total-stock-market index fund, an advisor would instead invest in both a low-yield growth index fund and a higher-yield value index fund. The intent would be to maintain a similar return overall, but also to allow the advisor to invest the funds separately, placing the higher-yield value fund in a tax-advantaged account and the low-yield growth fund into a taxable account. Similarly, replacing a total-bond-market fund with a high-yield corporate bond fund invested in a tax-deferred or tax-exempt account and a lower-yielding Treasury bond fund invested in a taxable account would potentially reduce the tax drag while maintaining comparable expected returns.

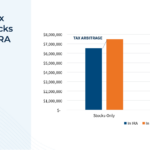

Over time, asset location can reduce the ongoing tax drag of the portfolio by nearly 10 basis points per year (of hard-dollar tax savings!), and layering the yield split methodology on top can double the asset location tax alpha by another 10 basis points (to a total of 20 bps). Cumulatively, this can add up to a 6% increase in long-term wealth accumulation over an investor’s multi-decade time horizon, simply by restructuring (i.e., yield-splitting) their core index holdings into the component parts for better asset location.

Ultimately, the key point is that while asset location is already a beneficial strategy to create tax alpha, the tax efficiency of a portfolio can be further improved upon with a yield-splitting approach to allow for even more-finely-tuned asset location implementation… all while maintaining a substantively identical overall risk/return profile for the portfolio as a whole. This not only leads to potentially significant tax savings for clients – particularly those who have the capacity for both tax-advantaged and taxable account holdings, and who pay a high Federal tax rate (and/or who live in states with high tax rates) – but also provides a tangible way for the advisor to demonstrate their own value!