Executive Summary

For “lower income” individuals whose income falls within the bottom two ordinary income tax brackets, the Internal Revenue Code applies a 0% long-term capital gains rate to the extent their gains also fall within the lower two brackets. However, the 0% rate only applies as long as the income actually does fall within those lower brackets – which means “too much” in capital gains will eventually cross out of the 0% rate and into the higher tax brackets.

Nonetheless, the potential for 0% long-term capital gains rates means that for those who are eligible, the best thing they can do every year is not harvest capital losses – the “typical” capital gains strategy – but instead to harvest gains! By selling investments that are up, and buying them back again immediately (without any wash sale rules to navigate!), the taxpayer can effectively get a step-up in basis on current investments without any (Federal) tax liability!

Of course, the caveat to this strategy is that while long-term capital gains may be eligible for 0% rates for lower income individuals, it is still income itself, potentially impacting certain deductions and tax credits, and the taxation of Social Security. In addition, harvesting capital gains must be coordinated with other strategies, like partial Roth conversions, which can potentially drive up long-term capital gains rates and make capital gains harvesting less effective. Still, though, the potential to claim a free step-up in basis is not one to be missed, for any years where income is low enough to take advantage of the rules, whether due to just having income low enough to qualify, having a “temporarily” low income year due to a job loss or change, or simply looking to harvest capital gains once retired when wage income is gone and required minimum distributions have not yet begun!

Mechanics Of The 0% Long-Term Capital Gains Tax Rate – The 0% Rate Is Not Unlimited!

The 0% long-term capital gains rate was created under the Jobs Growth and Tax Relief Reconciliation Act of 2003 (also known as President Bush’s second major piece of tax legislation), with a delayed implementation of 2008. The rule was scheduled to expire with the rest of the “sunset” provisions at the end of 2010, but was extended two more years under the first “fiscal cliff” legislation (the Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010), and then was ultimately made permanent under current law as a part of the second fiscal cliff legislation, the American Taxpayer Relief Act of 2012.

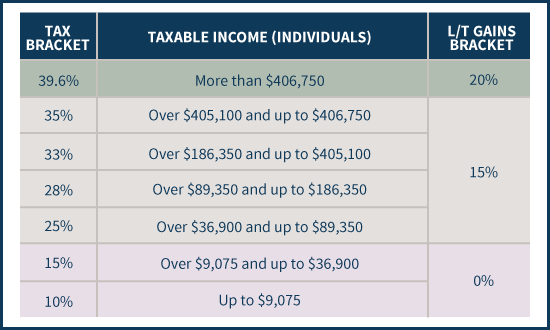

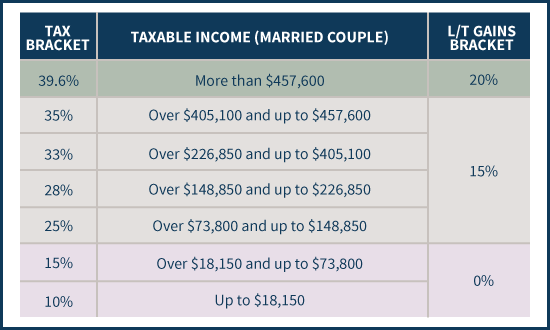

Technically, the 0% long-term capital gains tax rate is just one of three tax brackets that can apply to long-term capital gains. The thresholds for determining which bracket applies to a long-term capital gain are drawn from the tax bracket thresholds for ordinary income brackets, as shown below (for married couples).

As with the ordinary income brackets, the long-term capital gains brackets are graduated, and income that crosses out of one bracket falls into the next. Thus, for instance, just as a married couple having $500,000 of ordinary income would cross the 10%, 15%, 25%, 28%, 33%, 35%, and 39.6% ordinary income brackets, so too would that married couple having $500,000 of long-term capital gains span all three capital gains rates, with the first $73,800 in the 0% bracket, the next $383,800 taxed at 15% (up to $457,600 of total income), and only the last $42,400 would be taxed at the top 20% rate. (Michael’s Note: In this situation, the separate 3.8% Medicare surtax would also kick in for the upper capital gains income levels, effectively resulting in four capital gains tax brackets.)

Notably, because the 0% long-term capital gains rate only applies until crossing the threshold of $73,800 taxable income (for married couples), the reality is that the opportunity for 0% capital gains is inherently limited – as with other low tax brackets, it only applies until there’s enough income to cross out of that bracket, and any additional income falls in the next higher bracket. It’s not an unlimited opportunity to recognize capital gains at a 0% rate just because the taxpayer is initially in a low bracket! Similarly, this means it’s also important to recognize that while long-term capital gains falling at the lower income levels may be eligible for a 0% tax rate, it is still income for tax purposes, not only for determining which bracket to apply, but also for state income taxes (which may not be a 0% rate!), as well as determining Adjusted Gross Income (AGI) and any tax-related adjustments or thresholds based on AGI.

Coordinating 0% Long-Term Capital Gains Rates With Ordinary Income Tax Brackets

While the three long-term capital gains tax brackets of 0%, 15%, and 20% are relatively straightforward to apply – with 0% on the first $73,800, 15% on the next $383,800, and 20% on the rest (plus a potential 3.8% Medicare surtax on top of the 20% rate and some of the 15% bracket!) – the rules are more complex when an individual also has ordinary income as well. At that point, there are multiple types of income, all mixing together to increase total income, but each with their own tax brackets!

Under the Internal Revenue Code, this is resolved by applying ordinary income (to fill the bottom tax brackets) first, and then adding the long-term capital gains on top. To the extent there are any tax deductions, those deductions are applied to the ordinary income first, and only apply against long-term capital gains directly once ordinary income has been reduced to zero.

Notably, this is actually the most favorable sequence possible, as it ensures ordinary income (which is otherwise taxed at the highest rates) gets the lowest brackets; while the long-term capital gains do get pushed into the “higher” brackets, since long-term capital gains are already eligible for preferential tax rates, this still comes out with the greatest tax savings.

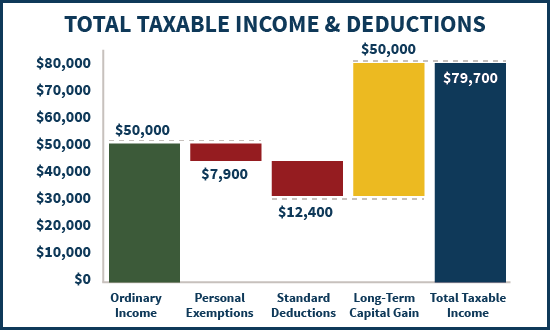

Example 1. Imagine a married couple who have $50,000 of ordinary income, and then recognize a $50,000 long-term capital gain. They will each be eligible for a $3,950 personal exemption (a total of $7,900 for the two of them), and the $12,400 standard deduction. Thus, their total deductions will be $3,950 x 2 + $12,400 = $20,300, which means their ordinary income will be $50,000 - $20,300 = $29,700 and their $50,000 of long-term capital gains go on top.

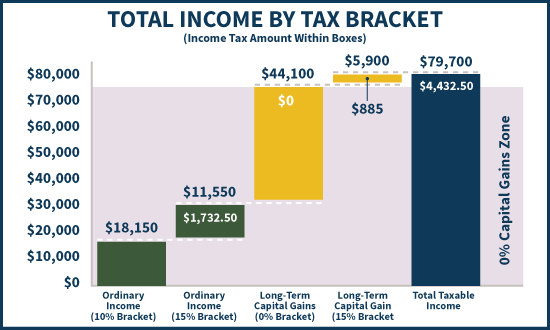

From there, the ordinary income fills up the tax brackets first, which means the first $18,150 falls in the 10% ordinary bracket, and the next $11,550 is in the 15% bracket. From there, the long-term capital gains kick in, which means the next $44,100 are eligible for the 0% long-term capital gains rate (up to the $73,800 threshold that forms the top of the "0% capital gains zone" shown below) and then the last $5,900 are taxed at the 15% long-term capital gains rate.

Ultimately, thanks to the favorable stacking sequence, the couple’s total tax bill will be only $18,150 x 10% + $11,550 x 15% + $5,900 x 15% = $4,432.50, or an effective tax rate of only about 4.4% on $100,000 of total income!

Harvesting Capital Gains At 0% Long-Term Rates

While the scope of the 0% long-term capital gains tax bracket is limited – it only applies for married couples up to $73,800 of income (after deductions) and $36,900 for individuals – the availability of the 0% rate still presents significant tax planning opportunities.

One of the most immediate is the opportunity to harvest capital gains – not losses – to the extent that those long-term capital gains will fall in the lowest bracket eligible for the 0% rate. While harvesting losses is messy – due to the requirements to navigate the “wash sale” rules, which can be especially harsh if done across a taxable investment account and an IRA – the reality is that harvesting capital gains is easy: sell the investment, and buy it back again immediately. If it’s a stock or ETF that is easily market traded, the investor may be out for no more than literally mere seconds; for a mutual fund, the investor will generally be out for 1 day (as mutual fund companies may not know how to handle a buy and sell order that both arrive at the mutual fund on the same day at the close of business!). Congress does not have a rule that says the taxpayer can avoid reporting income on their gains when they buy the position back again – in fact, the Internal Revenue Code has very specific requirements on what circumstances can avoid recognition of income because the proceeds are reinvested (e.g., Section 1031 or 1035 exchanges). Yet in the context of a 0% capital gains tax rate, selling the investment and recognizing the gain and buying it back again can be great tax planning!

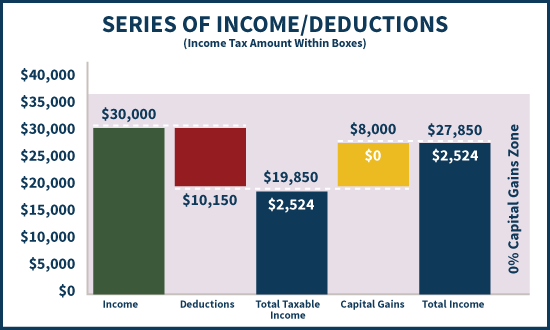

Example 2. Imagine an individual who has only $30,000 of income; this will be reduced to only $19,850 after the standard deduction and a personal exemption, and subject to $2,524 in taxes at a combination of 10% and 15% ordinary brackets. If this individual also has an investment portfolio that includes an S&P 500 index fund with a cost basis of $10,000 and a current value of $18,000, the opportunity is to sell the fund, and buy it back immediately! Without otherwise changing her investment position, the individual will now have an $8,000 long-term capital gain, pushing her income up to $27,850. However, since the gain is eligible for a 0% rate (as the 0% capital gains zone goes all the way up to $36,900 of ordinary income for individuals!), there will be no additional taxes due; the total tax liability will be the same $2,524, and what might have been $1,200 of long-term capital gains taxes (at a 15% rate in the future) just vanish altogether!

In the meantime, the act of selling the investment and buying it back again steps up the cost basis to the new current $18,000 value, reducing any future gains (or creating a higher basis to harvest future losses). The end result: the individual receives the equivalent of a step-up in basis at death, but without dying, and without facing any taxes along the way! (Michael’s note: A small state income tax liability may be due, although the Federal tax rate will remain at 0%!)

While the opportunity to harvest long-term capital gains at the 0% remains limited – only up to the tax bracket threshold – it arguably is an opportunity that investors should look to take advantage of every year, right up to that threshold! In other words, in any and every year that investors are in the 0% long-term capital gains tax bracket, they can aim to create enough capital gains to fill that 0% bracket every year – and keeping the rest deferred to the future. Notably, this 0% rate would also apply to any qualified dividends paid out in the year (which are eligible for long-term capital gains rates!).

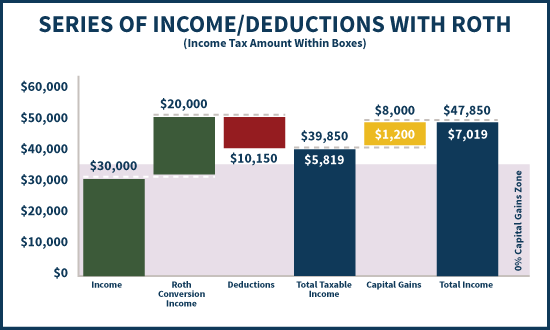

One important caveat to the strategy, though, is that investors should be cautious about simultaneously trying to do multiple harvesting strategies, such as harvesting capital gains and also doing a partial Roth conversion at the end of the year. The reason is that, as noted earlier, ordinary income always fills the lower brackets first, and capital gains stack on top.

Example 3. Continuing the prior example, if the individual also did a $20,000 Roth conversion, ordinary income would be driven up to $39,850 after deductions. This would fill the remainder of the 15% ordinary income bracket, with a small amount of income falling into the 25% bracket. Now, the $8,000 long-term capital gain will stack on top, but be subject to the 15% long-term capital gains tax bracket. Which means by adding “just” $20,000 of ordinary income (from the Roth conversion), the individual’s tax bill will jump up to a whopping $7,019, or a $4,495 increase equivalent to a 22.5% tax rate on the $20,000 of income!

In this last example, the reason for such a high tax rate is because the additional income was not only itself subject to a (mostly) 15% tax bracket, but also caused 15% tax rates to apply to the long-term capital gains, too! The additional ordinary income in the bottom ordinary brackets actually drive up the capital gains taxes, too, by pushing them into a higher bracket as well (driving the marginal tax rate as high as 15% + 15% = 30%!)!

Ultimately, the fact that “other” ordinary income can drive up long-term capital gains rates doesn't necessarily mean it’s bad to harvest long-term capital gains. It simply means that such strategies must be coordinated with other income-creation strategies as well; for instance, just converting enough of a Roth conversion to absorb deductions (if deductions exceed income altogether!), and then harvesting capital gains on top up to the maximum amount at the 0% rate!

On the other hand, it’s also important to recognize that when taxpayers are eligible for 0% capital gains rates, they should be cautious not to harvest capital losses, either, as there’s no reason to harvest a loss, and step the cost basis down, when there’s no tax savings anyway!

Other Planning Implications And Caveats Of The 0% Long-Term Capital Gains Tax Rate

The opportunity to harvest long-term capital gains at 0% rates can be highly appealing, even if it must be done opportunistically when a low-income situation presents itself – which might be a year of low income between jobs, or simply for those who haven’t grown their income enough to exceed the threshold, or perhaps after retirement when other wage income goes away (but before required minimum distributions begin).

On the other hand, the caveat is that even at a 0% rate, harvesting long-term capital gains does still count as income. This means it counts as income for state income tax purposes – which may prevent it from being a “true” 0% rate. It is also income for all other purposes as well – which means it increases Adjusted Gross Income (AGI) and can impact tax deductions (e.g., the medical expense or miscellaneous itemized deductions) or the phaseout of tax credits (from the American Opportunity Tax Credit, to the phaseout of premium assistance tax credits for health insurance). Because 0% long-term capital gains still increase income, they can also trigger the indirect taxation of Social Security benefits by causing them to be included in income, which can turn a 0% capital gains rate into 7.5%, 12.75%, or even 21.25% marginal rate! And for those qualifying for the Earned Income Tax Credit (EITC), be cognizant that your investment income must be $3,350 or less to remain eligible.

Given all of these caveats, the reality is that the opportunity to harvest 0% long-term capital gains rates will not present itself every year, and/or it may not actually be worthwhile to take advantage of. Nonetheless, since 0% long-term capital gains still amount to a free step-up in basis just by taking advantage of the rules that are there, it’s an important opportunity not to miss, as it can still result in thousands of dollars of tax savings in capital gains every year it can be done!