Executive Summary

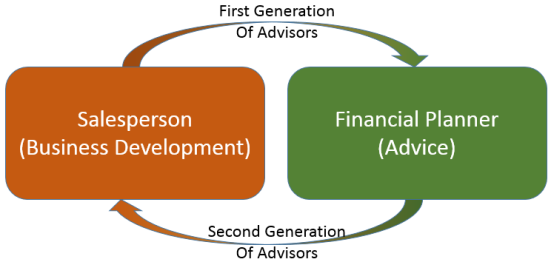

In the early days of financial planning, most "advisors" were ultimately insurance or investment salespeople, who evolved their skillsets and their practices over time to become financial planners. Accordingly, the education of financial planners was focused in adult education certificate programs, "learning" financial planning was about how to transition clients - and potentially the business model itself - from being focused on products, to advice instead.

As financial planning education began to shift to colleges and universities in the 1980s and 1990s, culminating in an explosion of degree-based financial planning programs in the early 2000s, this process of how a financial planner is trained as such began to change. While the first generation of financial planners were ultimately salespeople who became financial planners later, this next generation of financial planners will actually be the first seeking to enter the workplace and be trained as such from the start.

In turn, this transition is presenting new challenges for firms aiming to train and develop financial planners. While the historical process was to train experienced salespeople with existing clients to become financial planners, the new model looks more like the traditional one for professionals, starting with formal education, then transitioning to an "apprenticeship"-style period of gaining experience and honing skills, and only then - for the subset who wish to do so - going out to start a practice, and cultivate a skillset as a "salesperson" doing business development.

In other words, we used to train salespeople to be financial planners, and now the challenge is how to train financial planners to be effective salespeople! Ultimately, this will require new models of developing financial planners, as the required investment to train them are more significant than ever, in terms of both time and resources, forcing firms to figure out along the way how best to make the process of creating new financial planners successful for both the new advisor, and the firm as well!

Training Salespeople Into Financial Advisors

The emergence of financial planning is still a relatively new phenomenon. The first graduating class of CFP certificants was just over 40 years ago, and many of the early graduates have only recently begun to retire.

Yet through much of the early decades of financial planning, the reality was that financial planning was rarely sold as financial planning, or at best was only sold for a nominal fee. For the most part, financial planning was a means of doing needs-based analyses to determine what products should be implemented, and was compensated by commissions for the sales of those products.

Accordingly, the reality through most of the early years of financial planning was that it served as an enhancement to the sale of products that were needed at the end of the financial plan. In turn, CFP certification programs were primarily adult education certificate programs, designed to train experienced salespeople with an existing client base to be comprehensive financial planners, able to better understand and identify client needs, more effectively implement financial services products, and perhaps find opportunities for additional products that clients didn’t already have.

Over time, many advisors who trained in financial planning ultimately evolved their practice fully towards ongoing, relationship-based financial planning, includes adjusting their business model to align with a relationship-based service (i.e., transitioning from commission-based product sales to an ongoing AUM or retainer model).

Nonetheless, the reality is that for most of its first few decades, the primary focus of training financial planners was about taking experienced salespeople, with existing client bases, and advancing their knowledge base, skillset, and perhaps ultimately business model, into one that delivers ongoing financial planning. In turn, much of the focus in “training” financial planners was about how to convert existing product sales clients into becoming financial planning clients, and how to eventually convert the business model itself (from commissions to AUM/retainers).

Training Financial Advisors To Be Advisors From The Start

In the mid-1980s, the CFP Board was spun out from the College for Financial Planning (which was originally both the ‘keeper of the marks’ and the primary educational institution for the CFP certification), and in 1987 the first 20 universities teaching financial planning were recognized by the CFP Board. However, it was only in the past 15 years that financial planning truly saw a significant adoption in undergraduate- and graduate-degree-based college and university programs and the rise of financial planning academia.

The distinction of this emergence of college-degree-based financial planning is that for the first time, people began to enter the financial services world already trained in the knowledge of financial planning and now looking to become financial planners. By contrast, for most of the history of financial planning, “new” financial planners were not actually new to financial services; they were existing, experienced practitioners (generally, financial services product salespeople in insurance or investments) who were transitioning themselves and their businesses to financial planning. As a result, even though the first CFP certificants have been around for more than 40 years, the potential of graduating a significant number of people with a financial planning degree to immediately enter as a new financial planner is actually a relatively new phenomenon of the past decade or so.

In turn, this has put unique new challenges on financial advisory firms. It requires firms to create a path – and be able to derive value – from “trainee” financial planners, who do not have an existing client base on which to practice and train themselves as occurred in the past. Instead, the firm itself must provide clients for “practice” and a training ground with resources for advisors, developing them into financial planning professionals while still attempting to derive enough value from them to be viable as a business model in the first place.

Fortunately, such tracks and opportunities have continued to grow as advisory firms continue to transition into more relationship-based models – e.g., the AUM model – that are growing larger and larger, which in turn allows the financial advisory firm to separate out the expensive process of finding potential clients (prospecting) and “binding” them (getting them to sing up for services), from the relatively less expensive tasks of grinding financial plans and minding client relationships (as there is a significant premium to the “cost” of a financial planner with strong business development skills). This has led to “team” models emerging, as the tasks of finding and binding (i.e., business development) have been separated from minding and grinding (i.e., delivering ongoing financial planning services to existing clients).

Nonetheless, as firms are discovering, the process of training and developing a financial planning professional is significantly more difficult and complex than training and developing a financial services salesperson (who may or may not become a financial planner later). While developing successful salespeople is difficult for the simple reason that most of us are just not naturally inclined towards the ongoing rejection inherent in a sales career, it is at least relatively straightforward from the training perspective. “Advisors” could be trained in a limited number of products and how to sell them, and then sent forth to sell; those who failed would move on, and those who succeeded (and generated revenue and profits for the firm) could be reinvested into with additional training and development (culminating in becoming a financial planner).

By contrast, training a financial planning professional from the start requires an understanding of not only the wide base of technical knowledge in which the advisor must be competent, but also the client communication skills to build a planning relationship, establish rapport, and eventually deliver planning recommendations that clients will actually act upon. This requires significantly more time, more training support, and a client base upon which these skills can be “practiced” and cultivated through experience.

The need for a longer and deeper training process also raises the stakes for the firm doing the training; if a salesperson doesn’t work out, the firm invests relatively little up front, and has the ‘luxury’ of seeing who succeeds and deciding after the fact who should be receive the investment of additional training. By contrast, when a new financial planner is being trained, there is far more investment of time and dollars and firm resources, with what often is little indication in the early years of who will ultimately be successful in the end. There isn’t much evidence yet that those who enter to be trained as financial planners will have a better survival rate than those who enter as salespeople (though many studies suggest that CFP certificants who do survive generate more income than non-CFPs), yet the cost of turnover for planners who don’t make it is dramatically higher for the firm because of the training investment in the first place.

Turning Financial Advisors Into Salespeople?

Of course, even for financial planners who train as financial planners from the start, for many of them the end point is eventually to learn to become “salespeople” – not necessarily to sell financial services products, but simply to sell themselves and their ongoing financial planning services. Arguably, all financial planning includes at least some aspect of sales!

This means that in the long run, the training of a financial planner has essentially been turned around 180 degrees. What was once a process of training salespeople who later learn to become financial planners has now become a process of training financial planners who later learn to become salespeople!

In fact, this squeeze is already being seen in many firms. In the early stages of financial planning – where most financial planners were established salespeople-turned-planners – most firms grew by leveraging the skillset of the founder (a salesperson) and involved hiring “grinders and minders” to do the financial planning work and maintain relationships, freeing up the time of the founder to “find and bind” more new clients and grow the firm. However, as founding financial planners are retiring or developing succession plans, a severe shortage of financial planners with sales and business development skillsets is emerging. Now, one of the greatest challenges for many firms really is figuring out how to turn their existing financial planners – trained as such from the start – to become salespeople who can help grow and develop the business!

Accordingly, it seems the emerging next frontier is about how to convert the process of training salespeople into financial planners, to instead figure out how to train financial planners into salespeople (especially in a world where so many of today’s new financial planners really do not want “sales jobs”). To some extent, the solution to this emerges in the “career track” of the firm, which start in grinder positions, then minder positions, and for those who aspire to continue to climb the career track ladder, can develop their finder/binder business development skillsets. Nonetheless, given that many firms are too small to sustain such career tracks in the first place, this challenge is significant; and even for firms that are large enough, the relative cost of turnover of financial planning trainees is still significantly greater (than it was for financial services salespeople), due to the higher investment into those people in the first place.

While this kind of track has emerged in other professions – for doctors, it’s a standard that professionals learn their technical knowledge first (in school), then practice and hone the application of their skills (residency), and only then emerge as full professionals and decide where to direct their career. A similar path exists for lawyers and accountants, and many other professionals, where there is a career path of education, then “apprenticeship”, and then finally become a practicing professional that may have to go out and “get” clients. Even in most of those professions, though, the fact that their services are generally “bought” (i.e., people come find them) and not “sold” (people have to be convinced to purchase the service) mean the stakes remain higher for training financial planning professionals than others, though the "apprenticeship" track is slowly emerging in financial planning as well.

The bottom line, though, is that we are now in the midst of creating a new path for training and developing financial planners, and the experience of this generation of planners – who increasingly are entering financial services already having started their education and training as planners – will be substantively different than the generation that preceded them. This may be the second generation of financial planners, but it will be the first generation trained as such from the start. This will ultimately require us to develop new training models, and even new business models, to accommodate a training/career track, and the firms who figure out how to do this effectively – and garner value from their “financial planning apprentices” as they learn their craft – will be best positioned for long-term success!