Executive Summary

As the pressures of commoditization on investment advice continue to increase, more and more advisors adopting financial planning and wealth management services for their clients. Yet compared to the world of investing – where an advisor’s value proposition can be clearly articulated and measured in dollars and cents – it’s far more difficult to convey the value proposition of an intangible long-term service like financial planning. Determining whether an advisor provided a good Return On Investment in the portfolio is one thing, but how do you describe the ways an advisor tries to help a client get a better “Return On Life”?

In what may be one of the best clear descriptions of the key value propositions that financial planners provide, financial life planning pioneer Mitch Anthony boils it down to 6 key phrases: we provide Organization, Accountability, Objectivity, Proactivity, Education, and Partnership. While the words themselves aren’t necessarily new and unique, Anthony’s way of weaving them together into a Return-On-Life value proposition for clients certainly is.

Of course, the caveat is that just saying you can deliver on these value propositions to clients is one thing; actually doing so is another. Yet accordingly, this means that Mitch Anthony’s framework for a financial planner’s value arguably provides not only a good description for clients, but also a guidepost for advisors about where they should focus their own energies. Do you think these 6 key value propositions are a good way to describe the benefits of financial planning to clients? And can you really deliver them?

The Varying [Not Always Unique] Value Propositions Of Financial Advisors

In the world of investment advice, defining a value proposition is relatively straightforward. Advisors can offer superior investment selection, better investment analysis, effective diversification and risk management, built on the foundation of a quality investment process, all in pursuit of the investment holy grail: alpha. Generating alpha by definition means the client’s risk-adjusted returns have been improved, and in the process also means the client who pays the advisor’s fee is generating a “Return On Investment” (ROI) in the form of higher returns over and above what was paid in fees.

While generating alpha is certainly difficult, the process of evaluating an advisor and whether he/she is delivering the desired ROI is rather straightforward. Investment results can be measured, quantified, benchmarked, and evaluated. A track record of prior performance can substantiate that results have at least been delivered in the past.

When it comes to financial planning, though, defining a value proposition becomes far more difficult. After all, trying to sell an intangible service is difficult, when prospective clients can’t see or feel it (as they could a tangible product). And it becomes exceptionally difficult to differentiate an “invisible” service that the prospective client has never experienced in the first place. While some focus on traits like the expertise and experience of the advisor as the “value” of working with him/her, that’s really more about the traits of the advisor than the actual value to the client. For others, the value proposition may be defined in more client-centric terms – benefits like “we provide you [financial] peace of mind” – but it still leaves something to be desired. How much peace of mind can an advisor give, really? And how exactly do you measure that to substantiate a track record of success?

The 6 Key Value Propositions A Financial Planner Provides

At this year’s AICPA Personal Financial Planning conference, one of the general sessions was led by financial life planning pioneer Mitch Anthony, who put forth what may be the best set of terminology I’ve ever heard for articulating the true client-centric value proposition of financial planning. Framing it in the context of an (admittedly still unmeasurable) goal of improving a client’s “Return On Life” (ROL, as opposed to the traditional approach of trying to improve the client’s portfolio ROI), Anthony suggested that the six key value propositions of financial planning are that we provide:

At this year’s AICPA Personal Financial Planning conference, one of the general sessions was led by financial life planning pioneer Mitch Anthony, who put forth what may be the best set of terminology I’ve ever heard for articulating the true client-centric value proposition of financial planning. Framing it in the context of an (admittedly still unmeasurable) goal of improving a client’s “Return On Life” (ROL, as opposed to the traditional approach of trying to improve the client’s portfolio ROI), Anthony suggested that the six key value propositions of financial planning are that we provide:

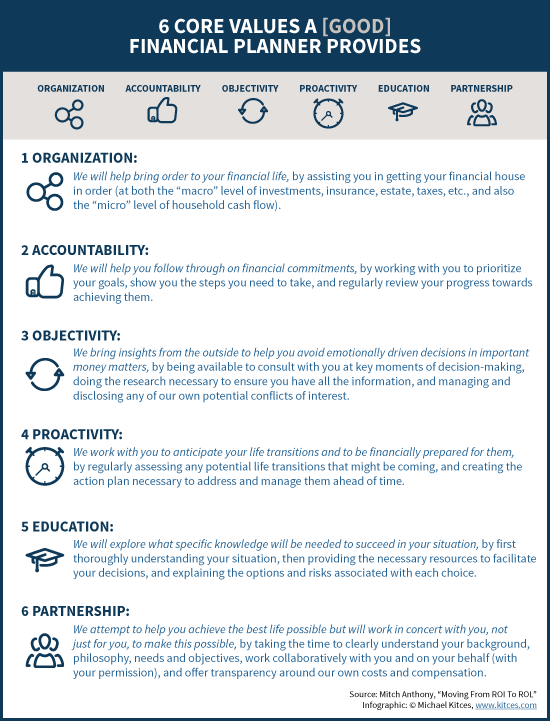

Organization. We will help bring order to your financial life, by assisting you in getting your financial house in order (at both the “macro” level of investments, insurance, estate, taxes, etc., and also the “micro” level of household cash flow).

Accountability. We will help you follow through on financial commitments, by working with you to prioritize your goals, show you the steps you need to take, and regularly review your progress towards achieving them.

Objectivity. We bring insight from the outside to help you avoid emotionally driven decisions in important money matters, by being available to consult with you at key moments of decision-making, doing the research necessary to ensure you have all the information, and managing and disclosing any of our own potential conflicts of interest.

Proactivity. We work with you to anticipate your life transitions and to be financially prepared for them, by regularly assessing any potential life transitions that might be coming, and creating the action plan necessary to address and manage them ahead of time.

Education. We will explore what specific knowledge will be needed to succeed in your situation, by first thoroughly understanding your situation, then providing the necessary resources to facilitate your decisions, and explaining the options and risks associated with each choice.

Partnership. We attempt to help you achieve the best life possible but will work in concert with you, not just for you, to make this possible, by taking the time to clearly understand your background, philosophy, needs and objectives, work collaboratively with you and on your behalf (with your permission), and offer transparency around our own costs and compensation.

While the words themselves are not necessarily new and unique, Anthony’s use of them, along with explanations of exactly what the advisor provides, and how (including some additions to the wording by yours truly), paint a remarkably clear picture of what the intangible service of financial planning is meant to provide, and why it’s worthwhile for consumers to pay for a financial planner.

In fact, it’s not hard to imagine an advisor’s website literally just using these 6 terms, and the associated explanations, as their exact explanation of “What We Do For You, The Client”! While still abstract terms, “we provide Organization, Accountability, Objectivity, Proactivity, Education, and Partnership” is still much clearer and more specific than “we provide a customized, individualized, personal financial plan!”

Living Up To The Financial Planning Value Proposition

Of course, while it’s not all that difficult to state Anthony’s core value propositions that a financial planner can offer, actually executing them still takes focus and effort, and not all financial planners today are necessarily really living up to these values in the first place.

For instance, while many financial planners will state that they help their clients get financially organized, in practice many advisors actually require and “force” their clients to get organized by gathering all their financial information together and completing a data gathering form and only then actually provide services. Actually turning the data gathering meeting itself into a client-centric “get organized” meeting is a very different experience than what most of us really provide to our clients.

Similarly, really being an effective accountability partner for clients requires helping them to prioritize what can sometimes be an overwhelming list of financial planning recommendations, and then actually coming into every financial planning meeting with a clear agenda that includes tracking what was supposed to be done by that meeting to ensure nothing slips through the cracks. And committing to being proactive means the advisory firm needs to run efficiently enough to actually have the time and opportunity to be proactive with clients. And saying you’ll work in partnership with your clients means you actually need to be prepared to do the financial planning interactively and work collaboratively in real time with them, not just assemble a financial plan behind the scenes and then tell them what they need to do next.

In point of fact, Anthony’s list of the core value propositions of financial planning are arguably not only good information to share with clients, but actually provide a good guidepost for financial planners themselves about how to improve upon their services to clients. As noted earlier, while it’s easy to say the words, it’s much harder to truly live them and execute them with clients. If you take a hard look at how you work with clients, are there ways that you could improve upon how you deliver your value to clients?

Of course, at the core of all of this is the commitment to really do financial planning in the first place – increasingly a necessity for financial advisors as the world of investment advice becomes more and more commoditized – and Mitch Anthony’s value propositions for helping clients generate a better “Return On Life” requires going deeper with them than what many advisors are accustomed to. For those who are interested, Anthony does provide a series of tools for advisors who are trying to figure out how to effectively deepen the relationship with their clients, called “MyFLPTools” (as in, My Financial Life Planning Tools), and also a coaching program for those who need help transitioning their business to become a “Return On Life” practice.

The bottom line, though, is simply this: in an era where many of the services financial advisors offer are becoming commoditized, and financial planning has become the “uncommoditizer” but only at a cost of being difficult to explain and communicate in the first place, it’s crucial to come up with an effective means of describing the value that financial planners really provide. And Mitch Anthony may have come up with the best, clearest list I’ve seen yet!

So what do you think? Does Mitch Anthony provide an effective description of the core values that financial planners provide to their clients? Do you think there’s anything missing? Is this a better or worse way to describe financial planning than how we traditionally have done? Would you use this language on your website and in your marketing materials to describe your value proposition to clients?