Executive Summary

A popular feature of permanent life insurance is that it accumulates cash value that can grow over time – ensuring that if the policy is surrendered, the policyowner will still have something to show for it that cannot be forfeited. However, this “non-forfeiture value” of a life insurance policy has an important secondary benefit as well – it gives an insurance company the means to provide policyowners a personal loan at favorable interest rates, because the cash value provides collateral for the loan.

Yet even as cash value life insurance operates as collateral for a life insurance policy loan, it also remains invested, earning a rate of return that slows the erosion of the net equity in the policy and allows a policy loan to remain in place for an extended period of time. And with some insurance policy loan strategies – such as the popular “Bank On Yourself” approach, there’s even a possibility that the cash value can out-earn the stated interest rate of the loan, allowing the loan to compound ‘indefinitely’.

The caveat, however, is that in the end a life insurance policy loan is still really nothing more than a personal loan from an insurance company, using the life insurance cash value as collateral. Which means even if the net borrowing cost is low because the cash value continues to appreciate, that’s still growth that the investor might have enjoyed for personal use, if the loan was never taken out in the first place. Or viewed another way, trying to bank on yourself doesn’t work very well when ultimately the loan interest isn’t actually something you pay back to yourself, it simply repays the life insurance company instead!

Life Insurance Cash Value: A Non-Forfeiture Benefit

When an individual simply pays for annual term insurance, the consequences of cancelling a policy are rather straightforward: the policyowner stops paying the premium, and the insurance company is relieved of its commitment to pay a death benefit if the insured passes away. The relationship is akin to a renter and a landlord – as long as the rent is paid, the renter lives in the property, and if the renter decides to move out, he/she simply stops paying the rent, and the two part ways.

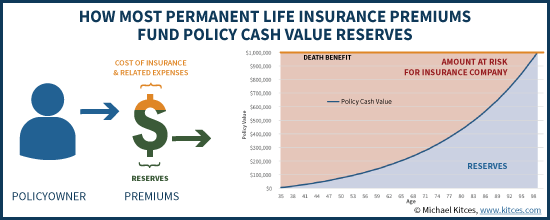

In the case of permanent insurance, however, the situation is more complicated. The insurance company offering permanent insurance is collecting far more in annual premiums than is necessary to “just” cover the annual cost of death benefit coverage, because the policy is designed to endow at its face value (i.e., have the cash value compound to the policy’s face value) at age 100. In turn, this means the insurance company holds an increasing amount of reserves, necessary to pay that fully endowed face value at the policy’s maturity date, should the insured actually “outlive” the policy. (Notably, policies issued for the past 10 years use more recent 2001 CSO mortality tables that extend the maximum life span of the policy to age 121.)

The significance of these reserves is that while with term insurance, if the policyowner stops paying the premiums the coverage is simply forfeited, with permanent insurance state regulators require insurance companies to provide some kind of benefits that cannot be forfeited even if the policyowner allows the policy to lapse. This non-forfeiture benefit, to return a (large) portion of the reserves associated with the insurance policy, is what we typically call the “cash value” of permanent life insurance.

The Life Insurance Policy Loan – A Cash-Value-Backed Personal Loan

While the origin of the “cash value” of permanent life insurance was as a non-forfeiture value for the policyowner – a share of the insurance company reserves associated with the policy that couldn’t be forfeited even if the policy lapsed – the existence of this “asset” is also what makes it possible to obtain a life insurance policy loan.

In fact, the reality is that a life insurance policy loan is really nothing more than a personal loan from the insurance company to the policyowner… for which the cash value of the life insurance policy serves as collateral. And the insurance company can confidently make the loan to the policyowner, at a relatively ‘favorable’ rate of interest, because it knows that if the loan is unpaid the collateral can be foreclosed upon and liquidated to repay the loan. Because the life insurance company controls the cash value that is serving as collateral to the loan in the first place!

In turn, the reality that the cash value of life insurance serves as collateral for the (personal) loan also explains why a growing loan can cause a life insurance policy to lapse – because ultimately, the insurance company doesn’t want to take any risk that the loan could ever be “underwater” (where the balance of the loan is greater than the collateral backing the loan). Thus, as the value of the loan approaches the cash value of the life insurance policy, the insurance company does in fact compel the liquidation of the collateral to repay the loan… even if that unfortunately causes the life insurance policy to lapse in the process!

Understanding Net Borrowing Rates And Insurance Policy Loan Spread

An important caveat to the dynamics of life insurance policy loans – and the fact that if the value of the loan reaches the total cash value of a policy it can cause the life insurance to lapse – is that even if no payments are being made on the loan and its balance compounds (or technically, negatively amortizes), the cash value as the underlying collateral of the loan continues to grow as well.

After all, the life insurance policy loan is still nothing more than a personal loan from the insurance company, using the asset value of the life insurance as collateral. Which means the cash value itself is still an asset of the policyowner, and remains invested with the potential to grow – just as the value of the underlying real estate can continue to grow, even though there’s a mortgage against the property.

But in the context of life insurance – where the value of the asset can grow almost in line with the balance of the loan, even when no payments are made on a life insurance policy loan – it can take a significant amount of time for the compounding loan balance to erode the net equity of the policy and ever trigger a lapse of the coverage. Or viewed another way, determining how long it will be until a life insurance loan causes the policy to lapse is based on the net borrowing cost (how quickly the loan is outcompounding the cash value asset), not just the stated borrowing rate on the loan.

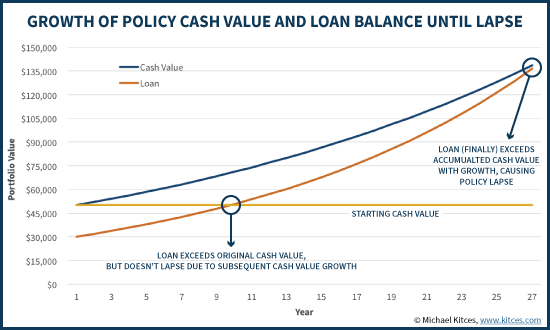

For example, imagine a situation where a life insurance policyowner has a whole life policy with a $50,000 cash value, and takes out a $30,000 loan at a 6% interest rate, which means the policy has a net equity value of $20,000. With 6% compounding loan interest, the policy would lapse within nine years as the loan compounds to $50,684, eroding the net equity down to $0. However, if the underlying cash value continues to earn a 4% crediting rate, then the policy won’t actually lapse after nine years. Because by then, the loan balance may be up to $50,684, but the cash value itself would be up to $71,116 (which means the net equity has actually grown to $20,432!)!

In fact, at these rates – where the loan compounds at 6% but the cash value (as collateral) compounds at 4% as well – even with no payments on the loan, it would actually take 27 years for the original $20,000 of equity in the policy to be eroded down to $0, causing the policy to lapse! (And in reality, it would take even longer, because subsequent premium payments into the life insurance would add even more cash value, increasing the size of the collateral and reducing the danger of policy lapse).

Notably, though, if the policy were to actually lapse at the end of this time period, the policyowner will be required to report gains and pay taxes based on the gross value of the policy ($144,000)! While the net value of the policy may be zero, as far as the IRS is concerned, the lapse of the policy is still the surrender of a policy worth $144,000 – even if the policyowner is required to use all $144,000 to repay the outstanding personal loan!

The Problem With Trying To Bank On Yourself With Life Insurance Policy Loans

Recently popular life insurance loan strategies like “Bank On Yourself” and “Infinite Banking” rely heavily on the idea that when an insurance policyowner borrows from a life insurance policy, they are “borrowing from themselves”, often at a very low net loan spread. Some even have the potential that the underlying cash value may outearn the borrowing cost anyway (between the growth in cash value and potential dividends from a non-direct recognition whole life policies, or the upside potential from the crediting methods of equity-indexed universal life policies).

And while Bank On Yourself is "legit" in that borrowing and repaying life insurance loans is a way to tap the cash value of a life insurance policy without surrendering it, the big caveat to these scenarios, as discussed earlier, is that ultimately someone who takes out a life insurance policy loan isn’t actually “banking on yourself” at all. The reality is that it’s just simply taking out a personal loan, not unlike a credit card loan, a mortgage, or a P2P loan, for which loan interest will be paid. The difference is simply that the loan happens to come from a life insurance company, and can be done at a relatively appealing rate of interest thanks to the cash value of the life insurance serving as collateral for the loan. Still, the borrower is really doing nothing more than taking out a personal loan and racking up loan interest while using their cash value life insurance as loan collateral! In other words, a life insurance policy loan isn't "banking on yourself" any more than taking out a home equity line of credit is "banking on your house".

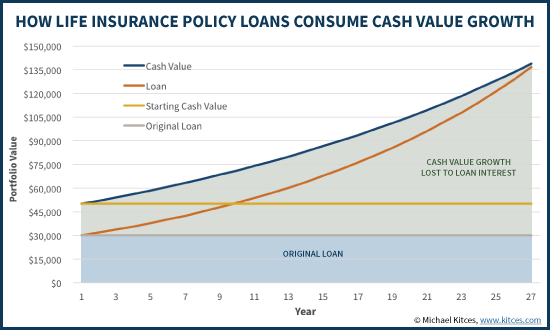

Similarly, while it might be appealing to have a low net borrowing rate like 2% (and for some policies, the net borrowing rate can be as low as a 0.25% loan spread!) the reality is that the key driver of borrowing from a life insurance policy is not actually the “net” borrowing cost (the difference between the loan interest rate and the crediting rate), but simply the loan interest rate itself! A small net borrowing cost may ensure that a loan can remain in force and negatively compound for a longer period of time before the equity is eroded… but that simply means more money is “lost” to the insurance company in the form of cumulative loan interest paid over time! Because the policyowner is still ultimately paying the entire cost of the loan interest rate!

For instance, continuing the earlier example, where a 2% net borrowing rate meant a $30,000 loan against a $50,000 policy wouldn’t actually lapse for a whopping 27 years… when the policy does lapse, it terminates with a $144,000 loan (and a $144,000 cash value to repay that loan). However, in the long run, this means the policyowner only got to use $30,000 of the cash value (via the loan), and never got the benefit of the $114,000 of growth over the subsequent 29 years! Because all of that growth was consumed by compounding loan interest! (Which the IRS recognizes in taxing the policy surrender based on the $144,000 of gross cash value – even if it’s all used to repay the loan, the policy itself was still worth $144,000 when it lapsed, producing a significant taxable gain!)

Notably, even if the growth rate of the cash value is better, and manages to exceed the borrowing rate, this may allow the life insurance policy to remain in force for a longer period of time, but it still means when the policy lapses that the policyowner pays the tax bill for all the upside growth of the cash value even though he/she never got to use it (beyond having it be consumed in covering the interest on the policy loan)! Again, the policyowner “uses” only $30,000, and never sees the $114,000 of growth (beyond the tax bill that’s due on it!).

As noted earlier, the appeal of some “Bank On Yourself” strategies is that the policy may actually earn a positive loan spread, where the growth of the cash value actually exceeds the loan interest rate. However, the challenge in today’s environment is that arguably the risks are far greater that a policy will underperform its borrowing cost, rather than outperform. In fact, the concerns about “excessive” and overstated return assumptions in equity-indexed UL policies (and the unrealistically favorable loan projections that result) has become so problematic, the National Association of Insurance Commissioners (NAIC) recently enacted Actuarial Guideline 49, specifically to crack down on the return assumptions in EIUL policies. The new rules are expected to result in a maximum projected crediting rate for loan illustrations of only about 7%, and some commentators have suggested that even 7% is still unrealistically high in today’s environment. (To put it in context, restrictions on variable universal life illustrations first adopted by FINRA in 1994 required that VUL policies “only” illustrated a 12% average annual growth rate for equities, which as we now know in retrospect was still far too aggressive as well, because regulators still tend to err to the high side!)

The bottom line, though, is simply this: in the end, a life insurance policy loan is really nothing more than a personal loan from a life insurance company, for which the cash value of the life insurance serves as collateral for the loan. This may allow for relatively favorable loan interest rates (thanks to the collateral), and the loan may be able to negatively amortize and still sustain for a long time (as the small net loan spread means it can take a very long time for the long to be underwater). Nonetheless, even if the policy loan takes decades to eventually compound and trigger a lapse – or be repaid from the death benefit if the insured passes away – the fact remains that a life insurance policy loan is not really a way to “Bank On Yourself” at all, it’s simply a strategy for taking out a loan and paying loan interest, which as with any borrowing should be used prudently to avoid accumulating significant loan interest over time!

So what do you think? Do you view life insurance loans as a viable cash flow strategy? Are you thinking about life insurance loans differently by recognizing they're simply a personal interest-bearing loan using life insurance cash value as collateral?