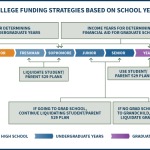

A longstanding challenge for independent RIAs has been finding a way to effectively and efficiently help their clients with 529 college savings plans - due primarily to the fact that "advisor-sold" 529 plans are actually built primarily for broker-dealers, while "direct-sold" plans aren't meant to have any advisor involvement at all... and leaving advisors at RIAs stuck in between. As a result, there has been little growth of 529 plans in the RIA channel, and fiduciary advisors who would like to help their clients comprehensively manage their wealth have had few options to facilitate the implementation of 529 plans and manage them thereafter.

In this week’s #OfficeHours with @MichaelKitces, my Tuesday 1PM EST broadcast via Periscope, we discuss the traditional broker-sold and direct-sold channels for 529 college savings plans, the blocking points of why more RIAs don't get involved with 529 college savings plans, and why a third option - the "advisor-supported" 529 plan - is needed to better facilitate RIAs helping clients invest in 529 college savings plans.

From their start, there have been two distribution channels for 529 college savings plans: advisor-sold, and direct-sold plans. Direct-sold plans were simply sold (marketed) directly to do-it-yourself consumers, who could open and invest the accounts themselves. Yet because not every consumer wants to do it themselves, many state 529 plans also created an “advisor-sold” option (and/or mutual fund companies that had long-standing relationships with advisors – like American Funds – established advisor-sold plans that they hoped would become appealing to advisors regardless of their state location). Yet the caveat is that because advisor-sold plans can only compensate advisors via the mutual fund commission structure, they would more aptly be described as "broker-sold" plans and can only be used by those who work under a broker-dealer. Since RIAs can't receive a commission, RIAs can’t even access and use “advisor-sold” (broker-sold) 529 college savings plans at all!

Instead, advisors in RIAs generally have to work with clients through the “direct-sold” plans for do-it-yourselfers. But this is a problem for most RIAs, since direct-sold plans aren't built for an advisor to be involved at all, leaving RIAs with no way to track performance, manage the account, nor to bill the account for services rendered! At best, advisors can try and work around this by using account aggregation tools like eMoney Advisor or ByAllAccounts to access the client's account directly, and some plans (such as the Utah Education Savings Plan) have provided solutions to pipe client account data directly into portfolio reporting tools from the UESP website. But Utah's plan seems to be the exception to the general rule for direct-sold 529 plans right now: that they are not practical, and certainly not scalable, for independent RIAs to use with their clients.

Which means if (direct-sold) 529 plan providers really want to better engage the rapidly-growing RIA community to help their clients with 529 plans, then we need a third type of 529 plan: the "advisor-supported" plan, where the advisor isn't a broker who sells the plan, but an independent advisor who supports and advises on the plan. And a successful advisor-supported 529 college savings plan is going to have to get good in 4 core areas: 1) reporting (which means providing transaction-level data feeds to popular performance reporting tools), 2) trading (by integrating to existing rebalancing and model management trading software for RIAs), 3) billing (to make it feasible for RIAs to include the 529 plan as part of their billing process on their expanded assets under advisement, ideally with an option to bill the fee from the 529 plan directly); and 4) educational and planning tools to help RIAs understand when an out-of-state advisor-supported 529 plan is appropriate and when an in-state plan might be better (e.g., for in-state tax benefits).

But the bottom line is simply to recognize that, while 529 plan adoption has not been significant in the RIA channel, and the few who do use them tend to just choose simple age-based glidepath portfolios in direct-sold plans… it’s not necessarily because that’s the only thing that RIAs want from a 529 plan. It’s because, with the lack of advisor-supported 529 plan options, that has been the only option that was feasible in the first place, given that RIAs fall into the crack between direct-sold and broker-sold plans. And with better advisor-supported 529 plan options (particularly in light of the House GOP tax plan that may expand their use for private elementary and high school savings as well), there’s potential for a lot of growth of 529 plans in the RIA channel... if we can get a true advisor-supported plan!