Executive Summary

In recent years, there has been a growing debate about the relevance of P/E ratios, especially the Cyclically-Adjusted Price-Earnings (CAPE) ratio popularized by Nobel Prize winner Robert Shiller. Are stock P/E ratios really elevated in today's environment? And what does that really mean anyway? Could P/E ratios simply have reached a new permanently high plateau?

Yet when the standard P/E ratio is flipped upside down, a different conclusion quickly emerges: stocks with a high P/E ratio have a low E/P ratio. And a low E/P ratio means the markets in the aggregate (or some stock in particular) simply are not producing very much in earnings relative to their current price. Which means regardless of whether the earnings are ultimately paid as dividends or reinvested for future growth for price appreciation, there just isn’t as much return available on the table.

Viewed from this perspective, perhaps the oft-maligned P/E ratio deserves more credit after all. No one would debate that bonds with a yield of 4% will likely have a lower return than bonds yielding 8%, or that rising bond yields can further dampen a bond’s total return. So if we examine equities based on their E/P ratios, and look to their earnings yield as well, is it really so controversial to expect that below-average earnings yields (and correspondingly high P/E ratios) may well lead to below-average returns in the future?

Understanding the P/E Ratio

The basic concept of a P/E ratio is relatively straightforward: it's the price that investors are willing to pay to get access to (i.e., to own a share of) the current/future earnings of a company. Ultimately, the value of a company should be the discounted present value of its future cash flows, but since future cash flows themselves are uncertain, we can look at what investors are paying for a slice of current earnings as a benchmark.

If investors are optimistic that earnings will grow for a particular company, they'll likely be willing to pay more to own a slice of those earnings than another company with less appealing growth prospects. Simply put, you'd likely be willing to pay far more for $1 of company’s earnings that's going to grow at 20%/year (a strong growth company) than one that's only expected to grow its earnings at 3%/year (a mature company in a competitive industry). Thus, higher growth companies generally have higher P/E ratios than lower growth companies, and investors tend to pay higher P/Es in the aggregate in more optimistic economic environments that are anticipated to produce more growth.

The caveat, however, is that ultimately a P/E ratio changes both by investors buying up or selling down the Price, but also because of changes in the Earnings of the company itself. And although there is general agreement about what the P/E ratio means/implies, there is less agreement about exactly what estimate of earnings is best to use to calculate it in the first place.

To smooth out this volatility of earnings, Nobel Prize winner Robert Shiller has popularized the “Cyclically-Adjusted Price-Earnings” ratio (or CAPE for short) which uses as the denominator of the P/E ratio a 10-year inflation-adjusted average of trailing earnings (the Price is still the current price of the market). Shiller’s research suggests that this ratio has some predictive value for long-term returns.

Notwithstanding its apparent predictive value, though, much criticism has been levied at the Shiller P/E ratio (and P/E ratios in general) as lacking usefulness or relevance for investors. To some extent, this may really be valid in the short term, as there are a lot of factors besides just valuation that can impact a stock's return in the short term.

Yet it appears that to some extent, criticism towards the P/E ratio may simply be due to its lack of intuitiveness – it’s hard for us to wrap our heads around what a P/E of 12 or 15 or 20 or 25 really “means”. Yet in practice, the apparent relevance of the P/E ratio may be far clearer if it’s simply turned upside down.

Flipping The P/E Ratio To An E/P Ratio

To the extent that a P/E ratio measures price relative to earnings, its reciprocal – if you flip the fraction – is simply a measure of earnings relative to price. In other words, given the stock has a certain price, what percentage of its value is created every year in the form of earnings. In essence, the E/P ratio is simply a measure of “earnings yield”.

Of course, in the case of earnings, we don’t necessarily know in the near term whether the stock will pay out its earnings in dividends, or take its earnings and reinvest them for future growth (resulting in theory in higher dividends in the future). Nonetheless, if we ultimately care about a company’s (future) cash flows, the earnings yield is the simplest way to evaluate how much is being generated relative to the current price.

From this perspective, knowing a stock’s earnings yield and its E/P ratio should be highly appealing. As with any investment, stocks with a high earnings yield should probably generate a decent return, and stocks with a low yield are probably less likely to do so. While there is an astonishing amount of debate about whether a stock with a P/E ratio of 25 is riskier than a stock with a P/E ratio of 12.5, is there really any debate that a stock yielding 4% (whether those earnings are ultimately being distributed as dividends or reinvested for growth) is probably not as good of a deal as a stock yielding 8% (to be distributed or reinvested as well)? Because mathematically, a P/E ratio of 12.5 vs 25 and an earnings yield of 8% vs 4% (respectively) are the exact same thing!

Of course, there are times that an investor might still want to buy a stock with a current earnings yield of 4% instead of one with a yield of 8% - for instance, where the investor has a strong belief that earnings will rise significantly with growth in the near future, such that what appears to be a “low” earnings yield today will end out being more favorable in the future. And that’s a valid viewpoint to have, with the caveat that it becomes intuitively obvious that you really should only ever buy a stock with a yield of 4% instead of one with 8% because you expect that company’s earnings and fortunes to grow significantly (or because you expect the company yielding 8% to be poised for an earnings tumble). Otherwise, you’re just buying a stock generating less cash and having a lower yield. It shouldn’t be any great surprise that it will have a lower expected return!

The Predictive Value Of E/P Ratios

While it seems intuitively obvious that all else being equal stocks yielding 8% will have a better long-term return than stocks yielding only 4%, the question arises: given how volatile earnings really are, is the predictive value really any good? As it turns out, yes.

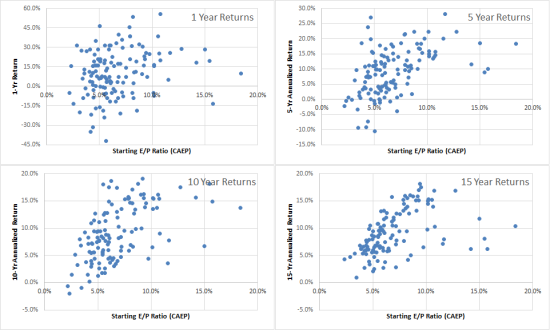

The charts below show the E/P ratios of stocks over time, and their subsequent 1, 5, 10, and 15 year returns. The E/P ratios are calculated in the same manner as Shiller CAPE – literally, they’re simply the reciprocal E/P fraction, and the graph simply looks at the relationship between the then-current earnings yield (based on trailing earnings) and what the average annual growth rate of stocks turned out to be 1/5/10/15 years later.

As the results show, E/P ratios don’t have a very strong relationship to returns in the short term, but the relationship improves significantly over longer time periods, and especially at yield extremes. Over a 10-year period, the negative returns consistently occurred when the earnings yield on stocks was below 5%, and similarly none of the strong return scenarios (15%+) occurred until the earnings yield was over 5%. An earnings yield of 5% corresponds to an environment where the P/E ratio is over 20; in other words, just as the P/E ratio implies as well, buying stocks with a P/E over 20 (or an earnings yield below 5%) has a higher likelihood of loses a decade later, and a greatly diminished probability of outsized returns.

Of course, in the ideal world, we would simply predict the value of a stock based on the actual value of anticipated cash flows (i.e., forward earnings) it will generate in the coming years. Unfortunately, there’s a problem with forward P/Es: the reality is that analysts aren’t very good at actually estimating this, as shown in the chart below from Yardeni which finds that on average analysts overestimate earnings to the tune of about 30% (and they tend to be off the most at turning points in the markets where they matter the most!).

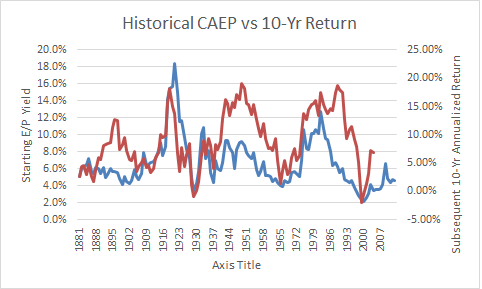

This lack of predictive value for forward earnings is ultimately what leads to the use of trailing earnings (eliminating the optimism bias of forward earnings), and in particular the Shiller CAPE, as trailing 12-month earnings are similarly problematic For instance, through the end of the second quarter of 2007, the trailing 12 months of as-reported earnings were $84.92/share and the S&P 500 was at 1,503 on September 29th of that year, resulting in a P/E ratio of 17.7. One year later, in the summer of 2008 (after the market had already peaked in October 2007 but before the market crash), earnings were at $51.37 and the market had come down to 1,280, resulting in a P/E ratio of 24.9. Another year later, in the summer of 2009, not long after the market had troughed (along with earnings), the trailing 12-month as-reported earnings were only $7.51 (due in part to the huge write-offs from financials as they gave back what turned out to be very overstated profits from the prior years) and the market was at 919, resulting in a P/E ratio of 122.4! In other words, because of the significant volatility of immediately trailing earnings in the midst of a turn in the market cycle, the trailing P/E ratio showed the market as cheapest in 2007 at its peak before the crash and astronomically expensive in 2009 after the crash happened and stock prices were down 40%!

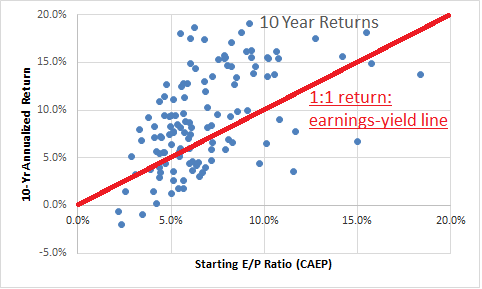

This, ultimately, is the point of the Shiller CAPE ratio; on a 10-year cyclically adjusted basis, the CAPE ratio showed the markets as expensive in late 2007 and cheap after the crash, while short-term 12-month trailing earnings showed the opposite! Of course, a long-term trailing E/P ratio (e.g., CAPE, based on 10 years of smoothed trailing earnings) will inevitably “understate” earnings going forward – at least, to the extent that there is any future growth rate anticipated. Nonetheless, this is not necessarily problematic; it simply means that the predictive value of earnings yields is not a direct 1:1 ratio. In other words, an earnings yield of 4% doesn’t mean the stock solely has an expected return of 4%, or that an 8% yield has an expected return of 8%. Given that earnings and the economy do tend to grow over time, 10-year annualized returns are typically higher than the earnings yield at the beginning of the time horizon (as shown below, most returns are above the 1:1 return:earnings yield diagonal line); a 4% earnings yield is expected to produce some return greater than 4% as earnings grow (and likewise for an 8% earnings yield). Nonetheless, the correlation remains strong; while a low earnings yield doesn’t unequivocally predict a precisely similar long-term return, it still reveals and elevated risk of a bad return and a reduced likelihood of a good one.

Viewed another way, when earnings yields start out weak, with some future growth returns may be a little higher, but there’s just only so much potential earnings growth on the table to make up for the low starting point. While individual growth stocks can potentially overcome a low earnings yield, for the market in the aggregate the economy and total earnings can only grow so fast, as earnings growth and profit margins themselves tend to be mean-reverting as competitive capitalism takes hold!

This can be viewed not only in comparing investments directly – a stock with an earnings yield of 4% versus one at 8% - and looking at markets in the aggregate, but also in looking at the absolute level of the earnings yield for markets relative to history. Stocks with an earnings yield well below the historical average (i.e., a high P/E ratio) have an elevated risk of delivering below-average returns, and conversely stocks with an above-average earnings yield (low P/E ratios) are likely to deliver above-average returns in the future. And if earnings yields are going to rise, then just as a bond, prices must fall, further exacerbating the low expected returns of a low earnings yield environment. As the chart below shows, there is a strong relationship between starting E/P yield (based on CAEP) and subsequent 10-year returns, especially when the E/P yield is low to begin with (overall correlation is a solid 0.529).

The bottom line, though, is simply this: while there has been a great deal of controversy about P/E ratios, it’s hard to see why there is such debate at all when viewed as an E/P ratio instead. No one would debate that a bond fixed to a yield of 4% has a lower return than a bond with a yield of 8%, or that a bond with a low yield that must rise to historical averages is going to lose more value in the process.

In the case of equities, the cash flows are less certain than a bond – they can, and generally will (at least for the aggregate market) grow over time, and there is some valid debate about the best way to evaluate earnings. Nonetheless, the simple conclusion remains that buying stocks with an earnings yield significantly below historical levels should have an elevated risk/likelihood of delivering below-average returns. Even if stock P/E ratios have reached a new “permanently high plateau”, the corresponding earnings yield valley should make it clear that returns must inevitably be lower in the future, even if such P/E or E/P ratios are sustained. Or in the bond context - when bond yields fall to 3% from historical levels and stay there, avoiding the bond price losses that would occur if rates rise, the good news is that bonds won't lose value from rising rates, but the bad news is still that as long as they're priced for a 3% yield in the first place, there's not much room for a better return that reaches the long-term historical average, either! So is it really that different if we're talking about stocks with an earnings yield of 3% instead of bonds with a yield of 3%?

Perhaps it really is time that we stop talking about P/E ratios, and start thinking more about E/P ratios instead, as predicting that returns may be higher or lower with a low (or high) earnings yield (and a corresponding P/E ratio) really shouldn’t be so controversial after all?

Michael,

Very good points, but I am left scratching my head as to how you handled inflation in this analysis.

As you know, real returns are the only type of returns that matter (after all expenses including taxes, to be complete), and any analysis that includes the 70s is based on a time when inflation was as high as 15% annually. Could you be so kind to share how this was handled?

The 10 year earnings portion of Shiller’s CAPE’s is descibed as inflation adjusted. Shiller has a web page with data and spread sheets if you want to make your own or change the inflation adjustment method.

One would need to adjust over 10 years for loss of purchasing power of currency.

For the 1 year P/E one might hope it is an aproximation to the real P/E unless inflation is really high. It might be relevant because one might expect monitary dillution to effect both the umerator and the denominator in the same direction.

Juan,

Thanks. I did not question CAPE, which is methodologically correct as you mention and is based on real (inflation-adjusted) earnings.

For every given year’s CAPE Michael plots the subsequent 10 year returns. Does he use real or nominal returns? If he uses nominal returns, the whole analysis is methodologically flawed and needs to go to the dustbin: you simply can’t compare nominal returns from the 70s (4-15% inflation) and the 00s (2-4% inflation)!!!

Sorry about misunderstanding. You had an even better question about the 10 year returns.

I do not know, but I can point you to a way to figure it out . Did the author adjust for loss of purchasing power and what would be the answer with that adjustment? I can’t do it for youbecause right now I can only read spreadsheets on this machine.

I think Kitche’s graphs were produced easily using Shiller’s data linked below. If not simmiler graphs can be made with Shiller’s data.

http://www.econ.yale.edu/~shiller/data.htm (choos the “U.S. Stock Markets 1871-Present and Cape Ratio” link)

Looking at Shillers’s spread sheet from right to left we go from computed columns to data.

The last column where CARPE is computed at cell K194 the formula is “=H194/AVERAGE(J74:J193)”. That is a 10 year lagging average of the “Real Earnings Column”.

Now all you need, is to compute the 10 year return as a column. And make scatter plots of the two columns and line plots of the two colums with the date. I think it would be computed with the same formula except you would use an average of the _future_ 10 years Real Earnings!

That would give you the data and graphs you want.

Those can be compared with Kitce’s. If it is not the same then one could compute using the (unreal) earnings column and see if the graphs are close to kitche’s.

Corrections: Kitce’s should be Kitces’

“10 year lagging average” should be “previous 10 years average” …

Please let us know what the answer is if you find out?

I suspect because the points slope is above 1 that he might have used unadjusted earnings. On the other had he might have made the adjustmen because it would have been so easy.

I’m such a stickler I would have computed with dividends and real dividends.

Juan,

Correct, these graphs were all produced with the Shiller data.

Note that you can’t do it just with the price return data from Shiller’s spreadsheet, you have to add in the dividend payments as well to get to a total return. But yes, it’s all from his data set.

– Michael

Thank you.

Mike,

Sorry I had missed your earlier comments here, and am just catching up now.

For this particular article, the returns were nominal. I’ve subsequently done some follow-up pieces looking at the relationship between CAPE/CAEP and real returns as well – see https://www.kitces.com/blog/shiller-cape-market-valuation-terrible-for-market-timing-but-valuable-for-long-term-retirement-planning/

What you’ll find from that subsequent article is that over time horizons as “short” as 10 years, the predictive value of CAPE is pretty similar for both nominal and real returns (at least in part because the higher inflation and interest rates is theoretically reflected in how high valuations get – thus why P/Es peaked at “just” the high-20s in 1966 but went to the mid-40s in 1999).

Beyond a 10-year time horizon, though, the relationship between CAPE and NOMINAL returns really starts to break down, while the relationship between CAPE and REAL returns actually STRENGTHENS. Again, see the charts in that follow-up article.

– Michael

Michael,

John Hussman has shown that when you add a third factor to the CAPE mix, specifically, the implied profit margin in the Shiller CAPE, the predictive value of the CAPE goes up to 90% for future returns in the 10 year window. See his recent commentaries, especially, http://www.hussmanfunds.com/wmc/wmc140414.htm. this effectively ends all debate on the topic as far as I’m concerned.

BTW, I will be adding this blog post to the CAPE Catalog at http://www.pe10ratio.com.

Cheers,

Kay Conheady, CFP(R)

You have written an exellent article, and you brought data!

Thank you.