Executive Summary

The requirement that a financial advisor must “Know Your Client”, including his/her tolerance for taking risks, is a universal requirement amongst investment regulators around the world.

Yet a recent survey of the global landscape for best practices in risk profiling by Canadian financial planning software provider PlanPlus reveals a disturbing lack of quality risk tolerance questionnaires (RTQ) and support tools for financial advisors. In part, this appears to be driven by the fact that regulators articulate the principle of “know your client’s risk tolerance” but provide little guidance on how it should be done to ensure that it’s right. And to a large extent, the problem stems from the reality that neither regulators, academics, nor advisors themselves, even have agreement on exactly what key factors of a client’s “risk profile” should be evaluated in the first place.

Nonetheless, a growing base of academic research is beginning to articulate a clear risk profiling framework, from recognizing the separation of risk tolerance from risk capacity, the role of risk perception (and misperceptions) on client behavior, and how “risk composure” (the stability of a client’s perceptions of risk) itself can vary from one cline to the next. Of course, just because these factors can be identified doesn’t make them easy to measure with a questionnaire, especially when it comes to “subjective” abstract traits like risk tolerance. On the other hand, the research suggests that financial advisors just trying to interview clients about risk may not be doing a better job, either.

In the end, the optimal approach may eventually be a combination of both, where psychometrically designed risk tolerance questionnaires assess a client’s willingness to pursue risky trade-offs, and the financial advisor can then assess the client’s risk capacity, financial goals, and ability to achieve their objectives given the constraint of their tolerance. And ultimately, an effective risk tolerance questionnaire may not only make it easier to properly match investment solutions to a client’s needs, but also make it easier to manage client risk perceptions and investment expectations on an ongoing basis. Or at least identify which clients are most likely to be challenged when the next bear market comes along!

PlanPlus Searches For Global Best Practices In Investment Risk Profiling

Assessing a client’s risk tolerance, as a part of providing investment management advice or investment product recommendations, is universally recognized as essential by regulators around the globe.

Notably, though, there’s a wide range of perspectives amongst regulators about what, exactly, “risk tolerance” actually is, how it should be measured, what factors are and are not relevant, and how those factors should be weighted when evaluating if an investment recommendation was appropriate or not.

To understand the landscape, the Ontario Securities Commission of Canada engaged PlanPlus (a leading financial planning software provider in Canada that has a global footprint, albeit little presence in the US) to assemble a research team that would compare Canadian practices on risk tolerance assessments to the best practices globally.

Unfortunately, though, what the researchers found was that most regulators around the world are “principles-based” in requiring that advisors understand and assess the client’s risk profile – an essential step fulfill any advisor’s “Know Your Client” (KYC) obligations – yet provide little guidance about how, exactly, that should be done.

Of course, if there was a clear and universally accepted academic framework for evaluating risk tolerance, this might not necessarily be an issue. For instance, in the U.S., an investment fiduciary has an obligation to provide the advice that a prudent expert would have given a similar client in similar circumstances. And although this principles-based “prudent expert” standard isn’t explicitly defined, the courts have recognized it to mean that the expert should have followed the principles of the academic Modern Portfolio Theory framework. Yet when it comes to risk tolerance, regulators have provided a principles-based expectation and obligation on advisors to make an assessment, but without any acknowledgement of the missing academic framework that would/should clarify how advisors actually do it.

In fact, the researchers found that there’s a surprising paucity of any academically research to validate most key concepts associated with a client risk profile. The situation is further complicated by the fact that there isn’t even clear agreement about what all the relevant factors are that should be considered, not to mention how they should be incorporated together to make a recommendation. And what little research has been done is difficult to bring together, because there isn’t even a consistent usage of terms regarding risk tolerance and a client’s overall risk profile!

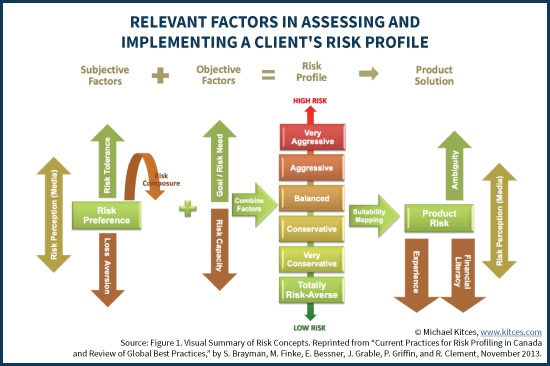

Breaking Apart The Risk Profile – Tolerance, Capacity, and Risk Perception

From the academic perspective, those who study consumer behaviors around risk and how it influences investment decisions are converging on three core constructs.

The first is risk tolerance itself. In the academic context, risk tolerance very narrowly and specifically refers to a client’s willingness to take on risk – i.e., to pursue an uncertain positive outcome, with the potential that a negative outcome could result instead. Those who have greater risk tolerance are more willing to engage in larger “risky trade-off” scenarios, while those with less risk tolerance tend to avoid them. Notably, some research in this regard focuses on risk aversion, or the dislike a client has towards risk or falling below a certain income/wealth threshold. Ultimately, though, risk aversion can be viewed as the opposite side of the same coin (e.g., an unwillingness to take risks – low risk tolerance – is akin to having a high risk aversion).

The second construct is risk capacity, or the client’s financial ability (in dollars and cents terms) to endure a potential financial loss, and still be able to achieve his/her goals. Of course, whether goals can be achieved in the event of a risky/bad outcome depends on what the goal is in the first place. And some goals are so aggressive that they may actually necessitate taking greater risk just to be achievable (which means the goal itself is risky, and has a higher “risk need” associated with it). Notably, though, risk capacity and the associated risk need to achieve a goal exist independently of the client’s risk tolerance. The mere fact that a client can afford to take risk, or needs to take risk, doesn’t mean he/she wants to or is willing to take risk (though of course, a risky goal for a low-risk-tolerance client implies that it might be time to find a new goal!).

The third construct is to recognize that different clients have different risk perceptions – how risky they think markets (or rather, their investments) are in the first place. The key point is that if perceptions are (or become) misaligned with reality, investors may engage in “surprising” behavior that seems inconsistent with their risk tolerance. For instance, an individual who is highly risk tolerant, but has the (mis-)perception that a calamitous economic event will cause the market to crash to zero, might still want to sell everything and go to cash. Even though he/she is tolerant of risk, no one wants to own an investment going to zero! In addition, the research suggests that some people may have better risk composure than others; in other words, some investors can keep their composure and maintain a consistent perception of the potential risks around them, while others have risk perceptions that are more likely to move wildly. And of course, perceptions of risk themselves also vary by the information that the individual has available to them – poor financial literacy and education can increase the likelihood of risk misperception, as can media coverage of scary/risky events (triggering the availability bias).

Notably, in this context, risk capacity is an objective measure (the dollars-and-cents mathematical analysis of the consequences of risky events), while risk tolerance (and risk perception) remains more subjective (an assessment of an abstract psychological trait). And it’s the combination of all of those subjection and objective factors that characterize the client’s entire “risk profile”, which in turn will lead to investment recommendations that may vary from very-aggressive to very-conservative.

Of course, even after evaluating the objective and subjective domains of the risk profile, it’s still necessary to actually map the results of the risk assessment to actual investment solutions… which again entails understanding both the objective risk of the investment product, how it fits into the client’s risk capacity and needs and goals, and also the subjective perceived riskiness of the investment (as even an objectively appropriate investment may subjectively seem overly risky if the client misperceives/misjudges the risk of the solution).

The Challenge Of Designing Good Risk Profiling Tools And Assessments

The good news of our increasingly robust understanding of all the different dimensions of a client’s risk profile is that it allows us to better match investment solutions to client goals while also being consistent with their tolerance for risk. The bad news, however, is that when there are so many factors involved – and “sub-factors” that are relevant as well (e.g., tolerance for risk based on upside potential may not be a mirror image of downside risk aversion, as prospect theory has shown) – it’s difficult to figure out how to blend them all together for an appropriate recommended solution.

In addition, the reality is that it’s difficult to measure the subjective aspects of risk tolerance itself, simply because it’s the representation of an abstract psychological trait in the first place. In other words, we can’t just objectively look into someone’s brain and figure out what their risk tolerance is. Instead, we have to ask questions, evaluate the responses, and try to figure out how clients feel about their willingness to take risky trade-offs, and how they perceive the risks around them.

Unfortunately, though, many risk tolerance questionnaires (RTQs) don’t actually do a very good job of helping to predict a client’s actual investment behavior during volatile markets, particularly when they ask about how the investor believes he/she would behave in the event of a significant financial loss. In part, this appears to be due to differences from one investor to the next as to what constitutes a “risky” and undesirable loss in the first place, which can be based on sometimes-arbitrary reference points. An investor whose portfolio recently ran up from $1M to $1.2M may not stress about a subsequent $200,000 loss (because they’ve still got their $1M, and the lost gains were just “house money” to them), while someone who just inherited $2M (and uses the full $2M as a reference point) may be far more stressed about the same dollar amount decline (even though it’s actually a smaller percentage loss). So an RTQ that asks about the consequences of a $200,000 loss would get somewhat counterintuitive responses (where the wealthier client is more averse simply because of a different reference point for “losses”).

The situation is further complicated by the fact that when we take RTQs, we tend to answer the questions calmly and rationally, but when risky events occur, we may respond emotionally (literally using a different part of our brain). Known as the “dual self” or “dual process” theory, this disconnect between how we react to risky events in real time, and our (rational) expectation of how we will react, makes it challenging to simply ask consumers (in the hopes of getting a good answer) about their tolerance for taking future risks.

Fortunately, though, while questions like “how would you react if the markets declined by X%” aren’t very effective at evaluating our likely tolerance for risk in real time, it does appear feasible to get at least some understanding of how a particular investor will likely behave in the face of a risky event. The challenge is greater for younger investors, along with those who have poor financial literacy, because they’re even less capable of making financial self-assessments (due to the lack of experience, knowledge, or both). Nonetheless, one study found that when we’re simply asked whether we’re more concerned about possible losses or potential gains, we can reasonably self-assess our preference (which at least partially reflects risk tolerance). For instance, an investor’s risk tolerance (and their likelihood of going to cash in a financial crisis) can be at least partially predicted by their willingness to engage in risky income trade-offs (e.g., “would you prefer a job with smaller pay increases and more job security, or one with bigger pay increases but less job security?”).

In combination, the research suggests that it really is feasible to get some good perspective on an investor’s risk tolerance, and how it may vary from one person to the next. In fact, there is an entire science of “psychometrics” – the process for making good tools to measure abstract psychological traits – that can be applied to formulate an effective risk tolerance questionnaire.

Finding a balance is still challenging, though, as neither clients nor advisors seem willing to use questionnaires that have “too many” questions (although Guillemette, Finke, and Gilliam found that a small number of high quality subjective risk tolerance questions can still be reliable). Still, though, the impact of a good risk tolerance questionnaire is striking – one study found that advisors trying to assess client risk tolerance with a conversational interview had only a 0.4 correlation to the client’s actual psychometrically-measured risk tolerance. In other words, a well-designed RTQ is actually far more effective than an advisor’s professional (but highly subjective and potentially-business-model-biased) judgment.

The Sorry State Of Current Risk Tolerance Questionnaires (RTQs) And Risk Profiling Tools

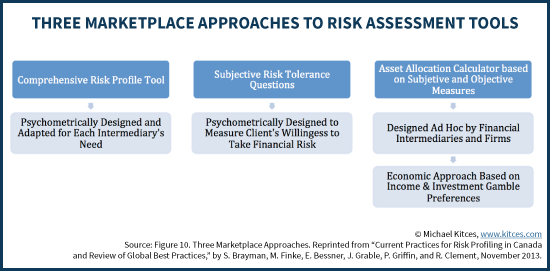

When looking across the globe, the PlanPlus research team found that there are still surprisingly few risk tolerance and risk profiling solutions available for advisors, with only about 10 solution providers of any broad reach. And amongst those providers, only 30% were able to document any form of psychometric validity to their risk tolerance questions and process itself, and few were even clear about defining their terminology and focus on what exactly they purported to measure (or not) in the first place (e.g., just tolerance, or also capacity, or also perception, etc.).

Amongst the available providers, the researchers characterized them into one of three categories: a) Comprehensive Risk Profiling tools, which used psychometrically designed questions that were adapted for (and mapped to) the company’s specific products and services; b) Risk-Tolerance-Only questionnaires, which focused solely on effectively measuring subjective risk tolerance (with the idea that it was the advisor’s job to fit the risk tolerance results into the rest of the picture, including risk capacity and financial goals, to make appropriate recommendations; and c) Asset Allocation Calculators that tended to combine the subjective aspects (risk tolerance) and the objective ones (risk capacity and time horizon) to formulate an asset allocation recommendation.

While arguably any of these can be reasonable approaches, when used appropriately, unfortunately few of the solutions were clear to even distinguish their limitations. All three types held themselves out similarly as “risk tolerance” or “risk profiling” solutions, despite their substantively different approaches, varying degrees of actual psychometric validation of the methodology, and thoroughness of their solution (e.g., “just” for asset allocation, or a more holistic risk tolerance analysis). For instance, here in the U.S., FinaMetrica would fit into the "Subjective Risk Tolerance Questions" category, while Riskalyze better fits as a tool to determine asset allocation based on gamble preferences; yet both frame themselves as "risk tolerance" or "risk profiling" tools without a clear distinction between them.

Furthermore, in Canada (where the analysis was based), only 10% of the risk tolerance solution providers have been validated in any way, and only 16% were even “fit for purpose” (with the rest either using poorly constructed questions, hopelessly conflated different factors, grossly overweighting a particular factor, or simply had no mechanism to actually identify highly risk averse consumers). And it’s not clear that an evaluation of most risk tolerance questionnaires would fare any better here in the U.S., either.

The Future Of (Better) Assessments Of Risk Tolerance

The poor state of affairs in risk tolerance questionnaires – both in Canada, and around the world – suggests that there is ample room for improvement.

However, the PlanPlus researchers suggest that there will be little progress until we first get agreement on a common set of terminology and the associated definitions for key terms pertaining to risk profiling (e.g., for risk tolerance and risk capacity, the difference between those and risk perception, etc.). And realistically, this change may have to be driven by regulators, given that regulators universally seem to require some kind of risk tolerance assessment process as a part of the advisor’s Know Your Client obligations, and if regulators aren’t clear about the terminology when writing the KYC requirements, advisors (and the solutions for them) aren’t likely to fill the void.

And ironically, the challenge of getting clearer about the nuances of risk profiling is that as more factors are introduced, it becomes both more difficult to measure them, and more complex to figure out how to fit them back together in order to craft an appropriate recommendation. Even relatively “simple” conceptual adjustments – like separating risk capacity from risk tolerance – have profound consequences relative to the ‘traditional’ approach in risk profiling. For instance, when analyzed separately, younger clients with long time horizons would not always have aggressive portfolios (because even if they have the risk capacity for it, they may not have the tolerance).

Perhaps the greatest challenge in improving the assessment of risk tolerance, though, is simply figuring out what the role of a questionnaire should or should not be in the first place. Ironically, many of today’s risk tolerance questionnaires are so badly designed, they may actually be worse than using no questionnaire at all, and/or simply allowing financial advisors to make their own professional-albeit-subjective assessment. Yet the potential remains that if advisors begin to actually insist on risk tolerance questionnaires that are actually psychometrically validated as such – and/or regulators require it on their behalf – that there may be a breakthrough in the adoption (and actual usefulness) of risk tolerance questionnaires.

Fortunately, finally getting a “good” risk tolerance questionnaire doesn’t obviate the need for a good financial advisor. The PlanPlus authors suggest that the best balance may be to have RTQs focus on just risk tolerance, and allow the financial advisor as a professional to determine the optimal investment/portfolio solution that incorporates that risk tolerance, along with the client’s risk capacity and financial goals. And because at least some clients may have unusual personal circumstances that don’t fit the “normal” risk tolerance questionnaire, there can always be a role for the professional advisor to identify situations where it’s necessary to ‘override’ the risk tolerance questionnaire based on additional factors or nuances. In fact, regulators around the world – including here in the US – have raised concerns that a purely automated (e.g., “robo”) risk tolerance questionnaire process could miss out on key client information (that the questionnaire didn’t know to ask in advance), and that a financial advisor should be involved at least to affirm the appropriateness of the questionnaire’s results.

In the long run, though, the greatest opportunity of improving risk tolerance questionnaires and overall risk profiling may be the way it helps financial advisors to better manage ongoing client relationships. After all, the clearer we are about a client’s ‘true’ risk tolerance, the easier it is to identify clients who may have risk misperceptions (e.g., the client who really is risk tolerance, but is acting risk averse, and therefore may be over-estimating their actual risk). And the potential to someday determine how to measure risk composure introduces the possibility of actual knowing, in advance, which clients are most likely to panic during turbulent markets, and therefore who might need extra education, guidance, or hand-holding when the next bear market comes.

But at a minimum, the PlanPlus study reveals that while many advisors may be frustrated that traditional risk tolerance questionnaires seem to do a poor job of predicting actual client investor behavior in times of risk, that may not be a failure of the approach of trying to assess risk tolerance, but simply a recognition that there’s still a lot of room for improvement to do it better in the first place.

So what do you think? Do you find risk tolerance questionnaires to be helpful with clients? If so, what tool do you use? If not, do you think it’s because questionnaires “don’t work”, or because you haven’t had access to a properly designed one? Please share your thoughts in the comments below!