Executive Summary

The traditional approach to evaluating risk tolerance - which has been enshrined into our standard regulatory process for determining the "suitability" of a recommendation - involves gauging a client's attitudes about risk, their financial capabilities to take risk (e.g., time horizon, need for income, and availability of other assets), and mixing them together into a composite score that can be assigned to a portfolio. A strong attitude and financial ability to take risk gets a high score and an aggressive portfolio, a poor attitude for risk and significant portfolio needs result in a conservative portfolio, and a mixture of the result leads to a moderate growth portfolio in the middle.

Yet the fundamental problem with this traditional approach is that it confuses someone's capacity to take risk with their actual need or desire to do so. The end result is that wealthy clients who don't want or need risk end out being given moderate growth portfolios anyway, young clients who have a long time horizon but no desire for risk end out with equity-centric portfolios that may scar them for life, and clients who have unrealistic spending goals end out with impossibly conservative portfolios doomed to fail.

The solution to this challenge is a fundamental change to how we view risk tolerance and financial risk capacity in the first place. The optimal portfolio solution is not a combination of risk tolerance and risk capacity; it's the portfolio that can best achieve the client's goals, constrained by risk tolerance to ensure that neither the portfolio, nor the goal, exceeds the client's tolerance in the first place. In other words, it's absolutely crucial to separate out our evaluation of whether someone needs risk, whether they can afford risk, and whether they want to take risk, so that the ultimate portfolio recommendation can properly align all three.

Defining Risk Tolerance And Risk Capacity

In the standard process of evaluating "risk tolerance" there are usually a wide range of questions regarding both someone's financial and their mental ability to manage risk and withstand risky events.

The financial questions - which might related to their need to tap the assets for income/withdrawals, the time horizon of the goal, and the availability of other assets - speak to the person's risk capacity. In other words, to what extent could a "risky event" happen (e.g., a market crash) without damaging the underlying financial goals. If you don't need money for decades (i.e., long time horizon) a near-term disaster won't impact goals. If you aren't withdrawing anything from the portfolio and it's just a small slice of overall net worth, again a near-term disaster won't impact goal. These would be clients who have a high capacity for risk. By contrast, if the goal is to take significant ongoing withdrawals, starting immediately, there is a far lower capacity for risk; if "something bad" happened, the goals would be in serious danger.

Once separating out the purely financial matters, true risk tolerance becomes purely focused on a client's actual attitudes about risk. In other words, does the client actually have the mental inclination and desire to pursue a more favorable outcome at the risk of a less favorable result. Notably, these mental attitudes about risk have nothing to do with the ability to afford the risk - it's simply about the desire to pursue actions or goals that entail risky trade-offs (or not).

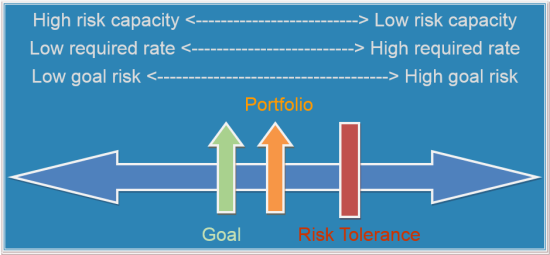

From this perspective, risk capacity actually becomes a measure of how risky the client's goals actually are; i.e., do the goals require a high rate of return just to have a chance of success, or is the goal so low risk that even a bad market outcome can't derail it. Risk tolerance measures how much of a risky trade-off the client is willing to pursue, whether that be expressed in the portfolio the client invests in, or the goals that the client aims to achieve in the first place. The simple key: it's crucial to be certain that neither the portfolio, nor the goal, is riskier than what the client can actually tolerate.

As the illustration shows, the client has a relatively conservative goal on the spectrum, a portfolio that should be able to achieve a return slightly in excess of that necessary to achieve the goal, and both the portfolio and the goal are more conservative than (i.e., to the left of) the client's maximum level of risk as indicated by their risk tolerance.

Why Separating Risk Tolerance And Risk Capacity Matters

To understand why this distinction between risk tolerance and risk capacity is so important, imagine two hypothetical clients: John Smith, and Betty Burton. Both clients are highly adverse to risk; if you gave them a questionnaire that just asking about their attitudes and willingness to take risk, both would earn the lowest possible scores. If you asked them "In a bear market, would you: A) Buy more; B) Just hold tight and stay invested; or C) Sell some of your portfolio" they'd answer "D) SELL EVERYTHING IMMEDIATELY!"

From the goal perspective, John's plan is to retire in about 15 years. His income goal is about $15,000/year, from a portfolio projected to be at $1,500,000 by then. Accordingly, John has what we'd call a "high capacity for risk"; if someone horrible happens in the market, his future withdrawal rate will go from 1% to 2%, which is still extremely conservative and safe. In other words, even if something bad happens to John's portfolio, his goals will be fine, and he has a high capacity for risk.

Betty's plan, on the other hand, is to start tapping her portfolio immediately, and she needs about $65,000/year (inflation-adjusted) from her $1,000,000 portfolio to achieve her goals. As a result, Betty actually has a rather low capacity for risk; if something bad happens to her portfolio, her goals are in serious jeopardy, as a 6.5% withdrawal rate is a dangerous proposition. Or viewed another way, Betty's goals themselves are very risky to pursue.

Using a "traditional" risk tolerance questionnaire approach, John would answer a long series of questions about both his financial capacity for and mental views about risk. His long time horizon and low need for income would give "high" scores, while his poor attitude about portfolio risk ("SELL EVERYTHING IMMEDIATELY!" in a bear market!) would get a low score. The likely end result: John would get a score around the middle on the overall questionnaire, and end out with a moderate growth portfolio.

Using a similar traditional risk tolerance questionnaire approach with Betty, the responses regarding financial capacity would indicate a limited time horizon and a high need for income, while Betty too would show a low tolerance for actual portfolio risk. The end result is that Betty would likely get one of the lowest scores possible on the risk tolerance questionnaire, and accordingly would receive an ultra-conservative bond portfolio.

It's crucial to note the outcomes achieved with the traditional approach. John has received a portfolio that virtually ensures he will someday have a personal financial crisis, because we've given a client with no actual tolerance for market declines a moderate growth portfolio! And the problem is not unique to John; in fact, we've also given Betty a portfolio that virtually ensures she will also someday have a personal financial crisis, because we've given an all-bonds-and-cash portfolio to a client who's targeting a 6.5% withdrawal rate!

The end result of the traditional approach: two clients on the road to personal crisis and potential disaster! For John, it's because he received a portfolio that will give him far more risk than he can tolerate - just because he can afford it doesn't mean he should, nor did he even need that risk in the first place (remember, he just wants to spend 1%/year starting in 15 years!). With Betty, the problem is that she has a set of goals that are inconsistent with her risk tolerance, for which there is no portfolio solution; the real conversation with Betty should not be about whether to have an aggressive portfolio or a conservative portfolio to achieve her goals, but that she needs to adopt some more realistic goals that better align with her risk tolerance in the first place!

Practical Implications Of Separating Risk Tolerance And Risk Capacity

The sad reality is that the combination of risk tolerance and risk capacity into a single measure has been so enshrined into today's regulatory environment, that the aforementioned disasters for John and Betty would probably be entirely defensible to most regulators, as those portfolios were the ones indicated by the traditional (albeit very flawed) approach to risk tolerance.

Nonetheless, in doing financial planning for the best interest of the client, it seems clear that it's time to separate out risk tolerance from risk capacity. Just because clients can afford to lose money doesn't mean they should be invested to do so, whether it's a retiree with conservative spending goals (like John in the example above), or a 25-year-old young investor with a long multi-decade time horizon. This has ramifications for both the traditional advice we give young people ("you should have a mostly stock portfolio because you have a long time horizon and can afford to take the volatility" - ignoring whether they have the tolerance for it in the first place!?), and the process used with retirees (measure risk tolerance on a standalone basis, and only then compare it to their needs, goals, and time horizon). Otherwise, we risk "over-risking" young clients and giving them an early bad market experience that scars them so much they walk away from being equity investors for good, and for wealthier clients we may unwittingly put at risk capital they never wanted, needed, or intended to risk in the first place!

Of course, this doesn't excuse the importance of the other key aspect of managing risk for clients - providing the ongoing education and expectations management that's necessary to keep their perceptions of risk in line with what's actually happening in their portfolio. And it's important to recognize that there are still better and worse ways to measure risk tolerance in the first place; while many seem to prefer a "conversational" approach, advisors may unwittingly bias client responses in the manner that they ask the questions, and research has shown that even just the gender of the voice asking the question can influence the client response! Consequently, best practices should probably include some form of (psychometrically designed) risk tolerance questionnaire (that really just measures risk tolerance, not mixed with the other factors!) which can then be explored and validated with a follow-up conversation to clients.

In the end, the point of this discussion is not to say that risk tolerance questionnaires themselves are "broken" and unusable, but simply that our industry-standard process of mixing together risk tolerance and risk capacity questions on a questionnaire together is what's broken. As long as we mix together questions about whether someone can afford risk with whether they wish to take the risk, we will have outcomes where clients end out with portfolios that give them risk they cannot tolerate just because they can afford it. Once pure risk tolerance is viewed for what it should be - a constraint on portfolio (and goal) risk, regardless of time horizon and financial capacity - it becomes far easier to align tolerance, portfolios, and goals.