Executive Summary

Saving up a "traditional" 20% down payment can be difficult for many individuals. As a result, many borrowers end up paying private mortgage insurance (PMI), in order to cover the lender's risk that the proceeds from foreclosing on a property would not be sufficient to cover the outstanding liability of a mortgage. On the one hand, PMI is therefore valuable to borrowers as it creates opportunities for homeownership for those that don't have enough cash saved up to put 20% down (it is effectively the "cost" of buying a home without a traditional down payment), but, at the same time, PMI can seem like an expensive drain on a borrower's cash flow, making it enticing to pay down the debt to eliminate the need to pay PMI.

In this guest post, Dr. Derek Tharp – a Kitces.com Researcher, and a recent Ph.D. graduate from the financial planning program at Kansas State University – examines how to determine the ROI from prepaying a mortgage to eliminate PMI, and finds that although the ROI can be high over short time horizons, the ROI from eliminating PMI over longer time horizons is often much lower.

PMI is generally required on a mortgage with a long-to-value (LTV) ratio of less than 80% (i.e., less than a 20% down payment). Because PMI is actually a form of insurance for the lender rather than the borrower, the reality is that PMI is functionally the same as a higher interest loan taken out on whatever amount would be needed to be prepaid in order to reduce the LTV ratio to less than 80%. For instance, if a borrower pays $1,200 per year in PMI premiums for a $200,000 home with a 5% down payment, then the borrower is initially paying an effective $1,200 of interest on a loan equal to the additional 15% ($30k) that would be needed to be prepaid in order to avoid PMI. Which is not an insignificant amount of interest, as $1,200 of annual interest on a $30,000 loan is effectively 4% loan on top off whatever the underlying interest rate is. So, if a borrower is paying 4.5% on a mortgage, then the total cost of the additional "loan" (PMI) is roughly 8.5%. Further, since this assumed $1,200 premium does not reduce as the balance needed to get below 80% LTV declines, the cost of keeping this "loan" in place increases with time. For instance, a borrower paying $1,200 per year in PMI on a mortgage that is only $5,000 away from eliminating PMI is effectively paying a rate of 24% on top off whatever their underlying mortgage rate is!

However, this 8.5% only represents a short-term ROI over a single year time period, and a key consideration in determining the long-term ROI of an investment is the rate at which it can be reinvested. Since pre-payment of a mortgage is effectively "reinvested" in a stable investment that "only" earns an ROI equivalent to the mortgage rate itself, this creates a long-term drag on the ROI from prepaying a mortgage (as funds are then tied up in debt repayment rather than investments which may have a higher long-term expected returns). And over long enough ROI time horizons (e.g., 30-years), the ROI of eliminating PMI effectively approaches the same ROI as prepaying the mortgage itself (albeit slightly higher due to some benefit that remains from the initially higher ROI). Which is important to acknowledge because while PMI elimination can look highly attractive based off of a single year ROI, failure to appreciate the differing short-term and long-term ROIs can lead investors to make pre-payment decisions which may not align with their long-term goals.

Of course, pre-payment of a mortgage to eliminate PMI may still be an attractive investment (particularly on a risk-adjusted basis), but the reality is that the time horizon used to evaluate the decision has a substantial impact on the long-term ROI. And given that it is the long-term impact that is most important for investors to consider, deciding whether to eliminate PMI may not be as much of a "no-brainer" as simply calculating the single year ROI may lead us to believe!

What is Private Mortgage Insurance?

Most buyers who have purchased a home with less than 20% down are familiar with private mortgage insurance (PMI). PMI is actually insurance for the lender rather than the borrower (despite the fact that borrowers typically pay PMI). PMI protects the lender in the event that the borrower stops making mortgage payments, and the proceeds from the foreclosure and sale of a property are insufficient to cover the outstanding loan.

This is why PMI is not needed on mortgages with a loan-to-value (LTV) ratio of less than 80% (i.e., with a down payment of 20% or larger). When the borrower’s equity in a home is sufficiently large, lenders can be more confident that they will be able to recoup their loan, even if the borrower defaults and they need to foreclose on the property to do so.

And although many buyers seem to resent PMI, the reality is that it is PMI which allows individuals to buy a home with less than 20% down in the first place. Simply put, PMI is the cost one must pay for the flexibility to buy a home without a traditional down payment, which is increasingly valuable as even fairly modest homes in some of America’s most expensive housing markets can come with high six-figure and even seven-figure price tags.

How PMI Is Determined

When taking out a mortgage with less than 20% down, the three primary ways that borrowers may pay for PMI are: (1) a borrower-paid monthly payment tacked onto the normal mortgage payment; (2) a borrower-paid lump-sum premium up front at closing; and (3) lender-paid PMI with a higher mortgage interest rate paid by the borrower to cover the lender's premium. In the third case, borrowers may not even realize they are paying PMI, as technically they are not, but the reality is that the lender is taking the extra cash they will receive through a higher interest payment and using that to purchase PMI (which means the net cost of PMI is indirectly still being passed through to borrower).

Notably, there are some potential advantages to lender-paid PMI for itemizing taxpayers, as while mortgage interest is deductible, PMI is currently not deductible in 2018 and beyond (the PMI deduction was last extended retroactively for the 2017 tax year under the Bipartisan Budget Act of 2018, but lapsed again as of December 31st of 2017, and it’s not yet clear whether another Tax Extenders bill will reinstate it again). However, given that few taxpayers will even be itemizing going forward (and therefore are not deducting mortgage interest or PMI), this tax difference may only affect a small number of homebuyers anyway.

So, while lender-paid PMI may be something to think about for some taxpayers, what most homebuyers think of when they pay PMI is either a monthly or lump-sum PMI payment. For ongoing PMI payments, annual payment amounts might range from 0.3% to 1.2% of the mortgage amount depending on many factors including the property location, size of the down payment, and how the property will be used.

Terminology note: Mortgage insurance premium (MIP) and private mortgage insurance (PMI) are effectively the same from a borrower’s perspective, but MIP is used in reference to FHA and other governmental loans (including reverse mortgages), whereas PMI (private mortgage insurance) is used for conventional loans. However, despite serving effectively the same function, the rules for eliminating MIP can be substantially different than the rules for eliminating PMI (e.g., MIP cannot be eliminated on FHA loans issued since 2013).

Ongoing PMI Payments

With ongoing PMI, the premiums are paid until the loan-to-value (LTV) ratio reaches a certain threshold. This threshold can vary depending on a specific loan, but PMI can be eliminated on most conventional loans when the LTV ratio falls below 80%.

However, it is important to note that PMI is not automatically eliminated until the LTV ratio reaches 78%. While the LTV ratio is between 80% and 78%, it is the borrower's responsibility to request that PMI is ended.

In addition, merely reaching the 80% LTV threshold based on the original value of the home does not guarantee elimination of PMI either, as the lender will likely require the borrower to obtain an appraisal, and the property may or may not then appraise at a value needed to actually eliminate PMI (i.e., if a house subsequently appraises at a lower valuation).

Further, whether appreciation can count towards improving a borrower’s LTV depends on their situation as well. In most cases, short-term appreciation (e.g., less than two years) will not be allowed to count towards eliminating PMI, and the borrower will need to reach a less-than-80% LTV ratio based on the lesser of the appraised value or original purchase price.

Note: For simplicity, several illustrations are shown in this post with 0% down. However, in practice, most conventional loans require at least 3% down, such as the 3% down (97% LTV ratio) programs now offered by both Fannie Mae and Freddie Mac).

Example 1. Jim takes out a $200,000 mortgage and on a $200,000 home. Given his credit score and other factors, he will pay an annual mortgage insurance premium of 0.6%, which amounts to an additional monthly payment of $100 ($200,000 * 0.006 / 12 = $100). Jim will pay this same $1,200/year premium amount until his LTV ratio is less than 80% (a mortgage balance of $160,000 based on the original purchase price of the home), despite the fact that his outstanding loan balance is declining from year-to-year.

Up-Front PMI Payment

With an up-front or single-premium PMI payment, a rough rule of thumb is that it will cost 2.5 to 3.5 times the annual mortgage insurance premium that would otherwise be paid on an ongoing basis. Effectively, this can be thought of as front-loading two-and-a-half to three-and-a-half years’ worth of mortgage insurance premiums. For instance, instead of paying $100/month ($1,200/year) until the LTV ratio is less than 80%, a borrower may instead pay an upfront premium of $3,000 to $4,200 at closing to cover PMI for the life of their loan.

Given that it may take a borrower who puts 5% down roughly 9 years to reach LTV ratio of less than 80% (or roughly 4 years with 3% annual appreciation), an up-front PMI payment can be a good option. Additionally, in the event that the home appraises at a higher value than the purchase price, the borrower may be able to finance the cost of the up-front premium (which may be helpful if available upfront cash is otherwise a concern).

Of course, in contrast to the requirement when making monthly PMI payments, the borrower has no obligation to notify the lender when their PMI reaches a certain value if the premium is already fully paid upfront. However, the downside to this approach is that the borrower is guaranteed to pay several years’ worth of PMI, regardless of how long it takes them to pay their mortgage down to an LTV ratio of less than 80%, or whether they even stay in the home for several years in the first place. Nor is there any way to recover the pre-paid portion of PMI in the event that the house ends up being sold in just the first few years.

Determining the ROI of Eliminating PMI

From a buyer's perspective, another way of thinking about PMI is not as a form of insurance, but rather as an interest payment on a loan equivalent to the amount needed to eliminate PMI. In turn, this amount can then be compared to available financing alternatives, such as taking a smaller initial mortgage (under the 80% LTV threshold), taking out a higher-rate second mortgage for the excess that would otherwise trigger PMI (i.e., a "piggyback loan"), or simply evaluating whether it’s worthwhile to make mortgage prepayments in order to eliminate PMI and “save” on the implied interest cost (instead of saving those dollars towards other investment or retirement accounts).

Example 2. Continuing the prior example, Jim just took out a $200,000 mortgage at 4.5% and needs to pay that mortgage down another $40,000 (to reach $160,000 and a LTV ratio of 80%) before he can eliminate PMI. Jim is paying $1,200 per year in PMI payments. Effectively, this means Jim is paying $1,200 in annual “interest” for a $40,000 loan, which amounts to an interest rate of 3%. However, Jim is paying this amount on top of his 4.5% mortgage rate, which really means he’s paying roughly 7.5% in the first year of his mortgage on the last $24,000 of his mortgage loan!

What these numbers suggest is that, from an ROI perspective, it looks like it may be appealing to pay down this mortgage as quickly as possible to reduce it below the 80% LTV threshold, even if it means foregoing other types of savings in order to eliminate the PMI and its implied interest cost (at least if the loan was structured with the monthly-payment version of PMI that can be eliminated, and not the single premium or lender-paid versions). After all, there aren’t very many other investment options available that provide the equivalent of a 7.5% “risk-free” fixed rate of return (which is still a 6.5% implied return even if the base mortgage interest is deductible in the 22% tax bracket).

Another unique characteristic of the ROI potential from paying down PMI is that the ROI increases as the 80% LTV threshold is approached, due to the fact that the PMI payment remains constant, despite the declining balance needed to eliminate PMI.

Example 3. Four years into his mortgage, Jim will have a principal balance of roughly $186,000 after making normal principal and interest payments. As a result, the amount he needs to pay in order to reach an LTV ratio of $160,000 is now only $26,000. However, his annual PMI payment of $1,200 remains the same, meaning that Jim is now effectively paying a 4.6% rate on top of his 4.5% mortgage, or roughly 9.1% in total interest for a $26,000 loan.

In essence, not only does it look compelling to accelerate mortgage prepayments (in lieu of other savings alternatives) in order to eliminate PMI, but the benefit becomes even better as the PMI threshold itself approaches. Of course, one thing to keep in mind is that PMI is only eliminated once the entire balance needed to get below the threshold has been paid. In other words, unlike most investments where each marginal dollar saved can provide the same ROI, the higher ROI from eliminating PMI is only achieved once a certain threshold has been passed.

An even more important caveat, however, is that this relatively simplistic ROI analysis does not fully consider the long-term ROI from eliminating PMI, as mortgage principal, once prepaid and assuming it is not cashed out, remains prepaid for the remainder of the lifetime of the mortgage loan.

Calculating The Long-Term Rate Of Return From Eliminating PMI

It is relatively easy to determine the true long-term ROI of eliminating PMI using the internal rate of return (IRR) function in Excel (or on any financial calculator).

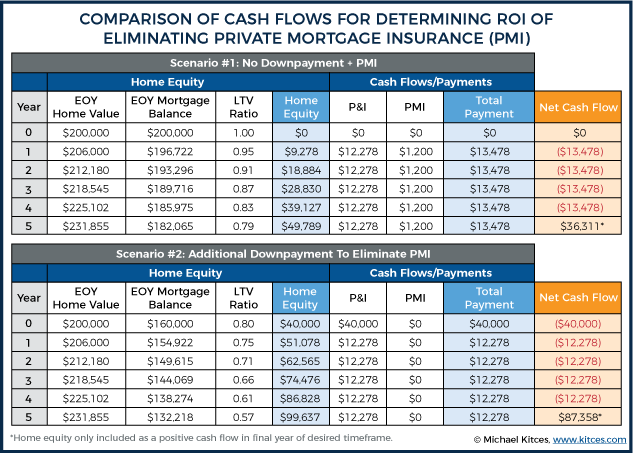

The first step is to set up two series of cash flows comparing a prepayment scenario to a non-prepayment scenario. In Jim’s case above, these would be (note: annual numbers are used for simplicity):

- An initial cash flow of -$40,000 to eliminate PMI (or $0 for the scenario in which PMI is not being eliminated).

- Annual cash flows capturing both principal and interest (P&I) payments ($12,278 per year) and PMI payments ($1,200) for each scenario.

- A positive cash flow in the final year of the time period under consideration equal to the equity a homeowner has in a property in each scenario (which differs due to different principal repayment rates assuming the payment amount is fixed). This step is probably the least intuitive, but it is essential for capturing the full effects of pre-payment on one’s wealth, since a homeowner who prepays and homeowner who does not will have different levels of home equity driven by different levels of loan repayment until the loan is fully repaid (at which point each would have 100% equity).

Example 4. Continuing Jim’s example above, assume that Jim expects 3% annual appreciation of his home. Based on this rate of appreciation and only making the minimum required mortgage payment, Jim’s home will be worth roughly $232,000 in five years and the principal reduction due to Jim’s mortgage payments will mean he owes roughly only $182,000 (i.e., he has $50,000 in equity). As a result, his LTV is less than 80% and he can then eliminate his $1,200 per year in PMI payments after five years. However, if Jim makes an extra initial payment of $40,000 to eliminate his PMI, his loan balance would then be roughly $132,000 in 3 years (giving him $100,000 in equity) and he would avoid $1,200 in PMI payments for each of these 3 years.

Based on the scenario above, we get cash flows that look like this:

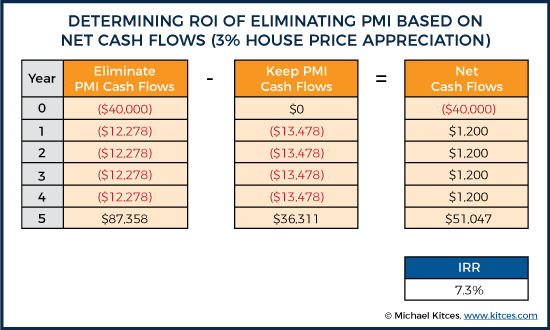

At this point, it could be tempting to put the IRR Excel function to the right of the chart and solve for a rate of return. However, that’s not quite what we want to do. What we actually want to do is find the marginal differences between the two scenarios, because what we’re really trying to solve for here is the IRR as a crossover rate between the two scenarios, which will tell us, given the impacts of eliminating PMI versus keeping it in place, what the hurdle rate is that an investment portfolio must be able to earn in order to choose to keep the PMI in place over eliminating PMI.

We would set that up by subtracting the keep PMI scenario from the eliminate PMI scenario as follows:

As you can see based on the cash flows above, once we net the two cash flow streams, we can use the IRR function to solve for a crossover rate (7.3%) which tells us how much we would need to earn on an investment portfolio to prefer the investment portfolio over eliminating PMI over a given timeframe. As you can see, this number is actually quite close to the rough estimate (7.5%) generated in Example 2. Notably, we do get this same result no matter what we assume for housing inflation. For instance, had we assumed housing prices remained flat, we would get the following:

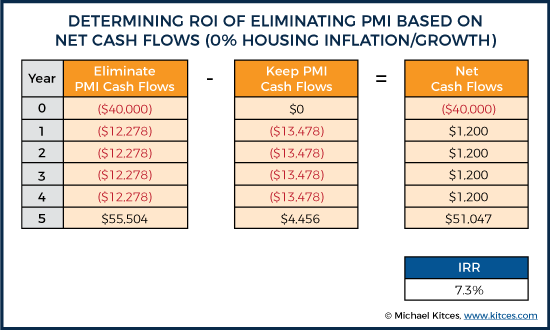

Example 5. Assume the same as Example 4, except this time annual appreciation is 0% instead of 3%.

As you can see above, the only thing that differs between the 0% housing appreciation (above) and 3% housing appreciation (Example 4) scenarios is the year five cash flow equal to home equity minus total payments (either just P&I or P&I + PMI). Intuitively, this makes sense, since neither P&I nor PMI payments are at all affected by inflation. The only variable actually influenced is home equity value itself, but since any changes to home equity will be identical between both the keep PMI and eliminate PMI scenarios, the result will always net out to a similar marginal difference driven by differing loan repayment levels between the scenarios. In other words, it’s not about the amount of equity per se, but the differences in home equity driven by early principal repayment.

So the key point here is the marginal differences from eliminating PMI (eliminated annual payments and greater principal balance paid down) results in the same crossover rate regardless of how the underlying asset value is moving. However, that does not mean inflation is irrelevant, as inflation can influence how long a homebuyer has to pay PMI, which in turn influences the marginal differences between the two strategies. For instance, as inflation increases, the time needed to eliminate PMI without any prepayment decreases, which in turn reduces the rate of return from prepayment.

For instance, in the 0% inflation scenario above, the time needed to eliminate PMI from making P&I payments alone (i.e., reach an 80% LTV based solely on principal repayment) increases from 5-years with 3% inflation to 10-years with 0% inflation. Which means, in order to see how inflation influences the ROI from eliminating PMI, we also need to look at how the ROI from eliminating PMI changes over time.

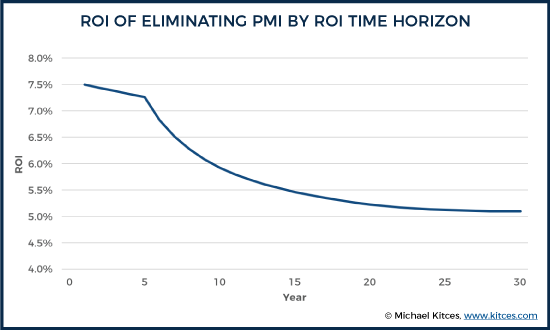

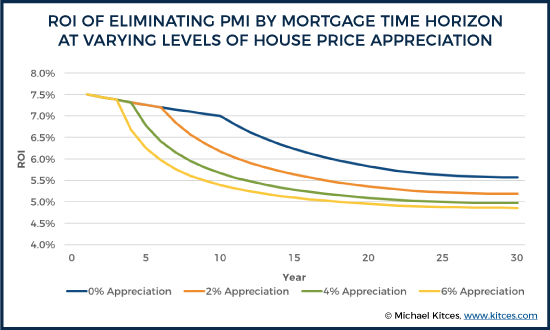

The Varying ROI Of Eliminating PMI By ROI Time Horizon

As illustrated in the prior examples, one key factor in determining the ROI from prepaying PMI is choosing an end year of the cash flow analysis in which the value of the difference in mortgage principal prepayments (additional net home equity) will be pulled back in as a positive cash flow. Of course, in practice transaction costs and other factors will influence this home equity value that is truly available to a homeowner, but ignoring that for the moment, we can analyze the ROI from eliminating PMI over various time horizons.

If we assume an inflation rate of 3%, we find the following ROIs from eliminating PMI over the life of the loan:

As you can see, the ending year chosen for analyzing the ROI of eliminating PMI can have a significant impact on the IRR calculated. Consistent with the simple estimate generated in Example 2, the ROI is exactly 7.5% over a one-year timeframe (4.5% ROI from mortgage prepayment + 3% ROI from PMI elimination). However, past the point at which PMI would have been eliminated regardless of prepayment, the marginal benefits of earlier prepayment decline. The reason for this is the reinvestment rate. Over short time horizons the impact of eliminating PMI is larger, but as we account for the fact that prepaying the mortgage effectively locks in a lower, longer-term ROI equal to the interest rate of the mortgage (4.5% in this example for time horizons up to the 30-year term of the mortgage), then effectively what we are looking at is a higher "teaser" rate in the short-term and a subsequent lower rate in later years of the loan.

Which is considerably different than how we typically think about expected rates of return on investor portfolios. For long-term investment portfolios, we often assume a constant reinvestment rate. For instance, if we assume a 60/40 portfolio will provide a long-term nominal return of 7%, then we assume that rate of return this year, and next year, and 10 years from now, etc. Of course, we may use Monte Carlo analysis or other strategies to introduce some variability, but we generally don’t say that we expect a 60/40 portfolio to generate nominal returns of 10% for the next three years and then 5% thereafter.

Yet this is precisely the dynamics that exist when looking at the ROI of eliminating PMI. Even if the rate of return is highly attractive based on short-term calculations (driven by eliminating PMI during the early years of the mortgage), the ROI in subsequent years over the life of the mortgage is simply the (much lower) mortgage rate itself. Which means, the longer-term marginal benefit from eliminating PMI ends up being a blended rate of a few years of higher rates (when PMI was in effect) and subsequent lower-rate years (when PMI was eliminated).

As you can see in the chart above, regardless of the rate of appreciation, all scenarios start out with a single-year ROI in the first year of 7.5%. Each appreciation scenario then continues to follow the same slow downward trajectory as additional years are considered until the appreciation rate is high enough that it triggers the elimination of PMI. At that point, the ROIs over longer time horizons begin to fall considerably faster, and approach (but never reach) the original mortgage rate of 4.5%, with lower appreciation scenarios leveling out at a higher ROI (due to having more years of higher PMI included early on).

The key point is that when we consider the ROI of paying down PMI over a longer time horizon (as we should, when the alternative is to invest assets in a long-term investment portfolio), the longer the time horizon, the less appealing it is to prepay PMI, as the hurdle rate (at which investing to a portfolio instead of prepaying the mortgage becomes more attractive) declines and becomes easier to clear.

Which is important, because if an investor is confident they can earn 7% nominal growth on a long-term balanced investment portfolio, then whether it’s a good ROI to prepay the mortgage to eliminate PMI depends heavily on the time horizon used to calculate the ROI in the first place. For instance, using the single-year ROI of 7.5% would lead an investor to decide they should eliminate their PMI, whereas the a 30-year ROI would suggest that using they should pay PMI so that they can keep more assets in their investment portfolio.

Of course, there are risk considerations as well, as the ROI from paying down debt is guaranteed whereas the ROI from investing in the market is not, but the key point remains that the time horizon over which ROI is determined heavily influences the true hurdle rate.

The Rising (Short-Term) ROI As PMI Elimination Approaches

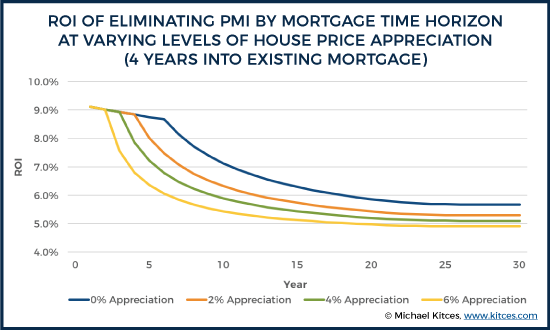

The examples above were all based on ROIs from eliminating PMI at the very beginning of the loan. While this comparison may make sense for those who have some choice or flexibility about whether to maintain a higher-than-80% LTV ratio or not (e.g., because they have a portfolio they could liquidate, or other assets that might be tapped), most individuals have PMI because they couldn’t afford a higher downpayment. As a result, many won’t be able to contemplate eliminating PMI until a few years into their mortgage – once they have made it far enough to save up some assets they couldn’t put towards their home at the time of purchase (but not so far into the loan that PMI has already ended due to appreciation).

And as was noted in Example 3 above, the (single-year) ROI actually increases as an individual is moving closer towards having PMI paid off. So, one might wonder, does that mean an individual is actually better off by waiting and then paying off PMI in a later year?

Not necessarily. This is actually a limitation of trying to use IRR to compare different investments, and an example of why NPV is a much better measure for comparing mutually exclusive investment options.

Example 6. Recall from Example 2 that if Jim’s ROI from paying down PMI increased from 7.5% initially (when he was effectively paying $1,200/year on a $40,000 loan) to 9.1% after four years (when he was effectively paying $1,200/year on a $26,000 loan), assuming 0% inflation. Jim currently has a mortgage balance of roughly $186,000 with a home valued at $200,000, and is contemplating putting $26,000 towards his mortgage balance to eliminate PMI. Jim is now wondering whether this 9.1% (single-year) ROI significantly increases his long-term ROI?

Consistent with the approach above, we can determine Jim’s net cash flows from both keeping and eliminating PMI. At various levels of annual housing appreciation, Jim’s ROI would be:

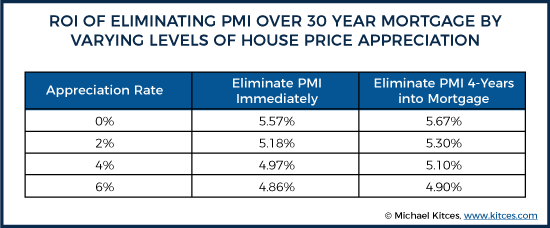

As you can see, there is a slight boost in 30-year ROI, but based on the scenario examined here, the increase in the hurdle rate is only somewhere between 0.1% and 0.04%, which is not likely to be a deciding factor in determining whether to eliminate PMI or put funds towards a long-term portfolio, despite the fact that a guaranteed 9.1% rate of return likely sounds like a no-brainer!

However, this analysis does assume that Jim does not extract equity at a later date. If Jim’s time horizon locked into the mortgage prepayment is shortened by the fact that he’s willing to extract some equity to invest elsewhere in the near-term (e.g., perhaps Jim currently owns a home in the Midwest but knows he’ll be relocated to San Francisco in two years and plans to sell his home and rent in San Francisco, meaning his home equity can be invested elsewhere... or perhaps Jim intends to do a cash-out refinance in the near term which would retain an LTV ratio of at least 80%) then making a prepayment to save on PMI for the few intervening years does become more attractive, effectively allowing Jim to capture the higher short-term ROI without being fully bound to reinvest in an asset “only” generating returns equal to the nominal mortgage rate over longer time periods!

Ultimately, the PMI elimination consideration for investors varies a lot from one individual to another. PMI rates themselves can vary substantially based on a wide range of factors (credit score, home location, down payment size, etc.), and therefore eliminating PMI could look considerably more or less attractive for a particular individual than the scenarios considered here. For instance, relative to the 30-year ROIs of 4.9% to 5.7% calculated above, a homeowner facing a PMI premium twice as large (1.2% vs. 0.6%) would experience 30-year ROIs ranging from 5.3% to 7.1%. By contrast, borrowers facing PMI premiums of only 0.3% would experience 30-year ROIs of only 4.7% to 5.1%.

So it truly is important to consider PMI elimination on a case-by-case basis, but more fundamentally, the key point is to acknowledge that prepaying PMI may not necessarily be as good of an investment as it may look at first glance. The ROI can be very attractive based on short-term ROI calculations, but the longer-term returns that result from locking up funds in an “asset” that has a yield of just the rate of the mortgage itself are going to be lower. In fact, the longer-term ROI on pre-paying a mortgage to eliminate PMI may often be only slightly better than the standard ROI an individual would receive from pre-paying their mortgage in the first place! And while this rate may still be appealing on a risk-adjusted basis, the reality is that ROI is less attractive over long time horizons!

So what do you think? Do you help clients determine the ROI from prepaying a mortgage balance to eliminate PMI? What else should borrowers consider when contemplating whether to eliminate PMI? Please share your thoughts in the comments below!

I don’t see the link to download the excel template for this?

Example 2 is wrong. He would not be paying 7.5%. He’d be paying $1,200 / 200,000 = 0.006 or 0.6%. So 4.5% + 0.6% = 5.1%. I’m curious what other basic math mistakes there are.

Example 2 is wrong. He would not be paying 7.5%. He’d be paying $1,200 / 200,000 = 0.006 or 0.6%. So 4.5% + 0.6% = 5.1%. I’m curious what other basic math mistakes there are.

$200,000 is not the correct denominator in this example. He would need to pay $40,000 to eliminate PMI, so $40,000 is the correct denominator (effectively, he’s paying $1,200 in interest on a $40,000 loan). $1,200 / $40,000 = 0.03 or 3.0%. You then add that to the 4.5% paid on the mortgage to arrive at 7.5%.

You cannot combine them if they have different denominators. I stand by my comments.

You pay 4.5% interest on the marginal $40,000 borrowed via the mortgage interest. You pay an effective 3.0% via the $1,200 in PMI on the marginal $40,000 borrowed. It is correct to add these both together to determine the cost of the marginal $40,000 borrowed.

This is incorrect. You don’t have two credit cards, one charging you 10% and another charging you 30% then combine them to say you pay 40% interest. This is basic stuff.

There aren’t two credit cards here. An analogous situation would be that you have a $40k balance on a single credit card that charges 4.5% interest plus a flat annual fee of $1,200. You have to add those amounts together to figure out your total cost of maintaining the $40k balance.

No… You don’t add interest rates together….