The requirement that a financial advisor must “Know Your Client”, including his/her tolerance for taking risks, is a universal requirement amongst investment regulators around the world.

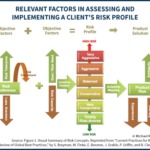

Yet a recent survey of the global landscape for best practices in risk profiling by Canadian financial planning software provider PlanPlus reveals a disturbing lack of quality risk tolerance questionnaires (RTQ) and support tools for financial advisors. In part, this appears to be driven by the fact that regulators articulate the principle of “know your client’s risk tolerance” but provide little guidance on how it should be done to ensure that it’s right. And to a large extent, the problem stems from the reality that neither regulators, academics, nor advisors themselves, even have agreement on exactly what key factors of a client’s “risk profile” should be evaluated in the first place.

Nonetheless, a growing base of academic research is beginning to articulate a clear risk profiling framework, from recognizing the separation of risk tolerance from risk capacity, the role of risk perception (and misperceptions) on client behavior, and how “risk composure” (the stability of a client’s perceptions of risk) itself can vary from one cline to the next. Of course, just because these factors can be identified doesn’t make them easy to measure with a questionnaire, especially when it comes to “subjective” abstract traits like risk tolerance. On the other hand, the research suggests that financial advisors just trying to interview clients about risk may not be doing a better job, either.

In the end, the optimal approach may eventually be a combination of both, where psychometrically designed risk tolerance questionnaires assess a client’s willingness to pursue risky trade-offs, and the financial advisor can then assess the client’s risk capacity, financial goals, and ability to achieve their objectives given the constraint of their tolerance. And ultimately, an effective risk tolerance questionnaire may not only make it easier to properly match investment solutions to a client’s needs, but also make it easier to manage client risk perceptions and investment expectations on an ongoing basis. Or at least identify which clients are most likely to be challenged when the next bear market comes along!