Executive Summary

Planners are accustomed to dealing with most types of capital that clients may have, whether it is stocks, bonds, real estate, cash, bank accounts, or other investments. Yet the reality is that for many clients, the biggest piece of capital on their balance sheet is not the stuff that they own; it's themselves, and their ability to earn income in the future. However, as planners we rarely track and account for a client's human capital; and as a result, we may overlook the financial advice that can truly have the greatest long-term impact for a client's success.

The concept of human capital is relatively straightforward. Clients earn income over time based on their labor and personal efforts, and those amounts that will be accumulated over the years can be quantified. In the typical approach, the current value of a client's human capital is simply the net present value of all the earnings they're expected to receive over their lifetime.

Viewed from this perspective, the accumulation of financial capital over time represents not so much the "creation" of financial capital by saving, but simply the conversion of human capital to financial capital. When an individual starts his/her career, there is a certain amount of income that will be earned during life; as that income actually is earned the client slowly converts potential future income into current income, and in the process either spends that income or saves it. If it is spent, it's consumed; if it is not, it is saved and contributes to financial capital. Financial capital in turn is invested to earn and grow so that it will be available for consumption in the future (i.e., in retirement). Thus, in the end, one might say that everything flows from your human capital; it is either income you consume, or income you convert into financial capital so that it can be consumed later.

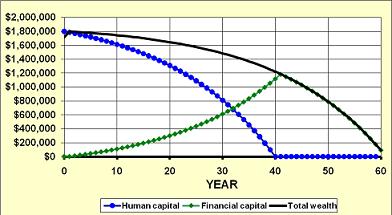

The graph below (calculated on an inflation-adjusted real-dollar basis) shows how a portion of an individual's human capital (the blue line) is steadily converted into financial capital (the green line), which rises due both to additional contributions and from investment growth. The black line represents the client's total wealth - a combination of human and financial capital - and declines over time as the client consumes his/her wealth.

So why does all of this matter? It matters because, as the graph shows, human capital is actually the greater asset on the client's balance sheet for most of his/her working career. Assuming 40 working years and 20 retired years (per the graph above), it's only after approximately 32 of the 40 working years that financial capital even grows to the point where it equals human capital (and it's only in those 8 years where financial capital has the onus to make a big push for growth before it begins to immediately turn around to begin depletion).

Accordingly, this actually means that for most of a client's working career, advice which helps to increase human capital has far more impact than adjustments to financial capital. For a client in their 20s and 30s, increasing the growth rate on your human capital by 1% (how quickly your earnings grow over time) has a radically greater impact than increasing the returns on your investments by 1%. In fact, allocating income towards "investments" that can increase your human capital (i.e., training and personal development) can have a far greater impact than saving towards financial capital! (Not to mention the impact of having a good career on overall well-being, too!)

Yet when we only look at a person's net worth as their financial assets, we tend to miss many of these insights. Clearly, we as planners have some acknowledgement that human capital exists: it's why we recommend disability insurance policies, and why we also buy life insurance against the risk that a premature death cuts human capital short. But given the relative size of human capital to financial capital for most of a client's life - and especially for the overwhelming majority of their working life - the average client conversation seems to grossly underweight human capital, and I believe that in large part is simply because we never quantify it and show it in the first place.

So what do you think? Do you talk to clients about their human capital, in addition to their financial capital? How much time do you spend on each? Have you ever shown your client's human capital on their balance sheet? If you did, do you think it would change any of the conversations?

I do not show human capital on the balance sheet. And I’m sure to discuss financial net worth as distinct from personal worth. This is a way to bring up that topic. Even if only a line item with no value. Interesting. Thank you,

I 100 % accept that Human capital becomes more important vis-a-vis financial capital, The real question is how do one develop this human capital , every individual will have different wave length to develop its own human capital. one cannot generalize this development of Human capital.

Michael..can’t agree more on this. My recent experiments focused on the youth in their 20s indicate that we as financial planners can add immense value by ‘nudging’ the youth to increase their human capital through conversations and workshops. The topic of human capital is so relevant in emerging markets like India, where over 50% of the youth, 500 million is below 30 years! I still re-call the conversations we had the FPA Retreat in May 2013 when one of the young planners asked your advice on what can be done to add value to the millennials and you had suggested to focus on helping them with increasing their human capital! This really validated what we do for the youth in the country. Thanks a lot for re-tweeting this piece few days ago which made me read up this piece again!!