Executive Summary

Almost by definition for many, the essence of financial planning is that it's comprehensive. Financial planners don't just look at a particular problem or product; they account for everything holistically to arrive at a recommendation and solution that fits in with the big picture. In other words, they don't just plan for a slice of the pie; they plan for the whole pie. Yet it seems that for many planners, the "whole pie" is the client's balance sheet; we plan for all the different assets (and liabilities?) that the client has, not just a particular account. What about the OTHER pie, though? Not the asset one; the INCOME pie.

The inspiration for today's blog post comes from a conversation I had recently with financial planner Don St. Clair, and some discussion we've had about just how "holistic" most planners are, given how little time many planners spend in dealing with the liability side of the client's balance sheet (i.e., do you give as much time to planning for your client's big debts, like a mortgage, as you do their big assets, like the 401(k) or brokerage accounts?). But this conversation in turn morphed into another discussion: how managing liabilities also consumes so much of a client's income, and comprises such a huge part of the client's cash flows.

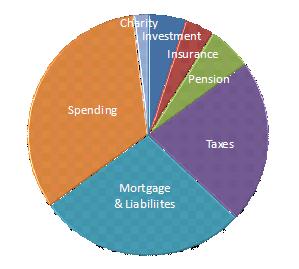

Don, not surprisingly, believes it's important to have a strong focus on the entirety of a client's cash flows, not just the ones that translate to the balance sheet, but I was really struck by a comment he once made to me, in reference to the "typical" client cash flow pie as shown here:

As Don stated it so simply: "My clients like working with me because I deal with more than just the things between 12 and 2 [o'clock, when you look at the pie chart as a clock]."

As Don stated it so simply: "My clients like working with me because I deal with more than just the things between 12 and 2 [o'clock, when you look at the pie chart as a clock]."

How right Don is; so many planners spend an inordinate amount of time focused on everything between 12 and 2, which is entirely about the cash flows that will contribute to assets on the balance sheet, and so little time elsewhere. Yes, some planners spend a reasonable amount of time on tax issues (although many defer entirely to the client's accountant), which at least gets them planning from 12 to 4. But so few planners spend more than just a few minutes of time focusing on the mortgage and liabilities, one of the biggest slices of the pie, and in my experience even more planners eschew spending any time on the other huge part of the pie: from 8 to 12, the spending portion.

Yes, many planners do look at FUTURE spending as it relates to setting a spending goal in retirement (and in turn determining the amount of assets needed to support spending), but how many planners really have conversations about a client's current spending habits? Most of us seem to view it as forbidden territory, with comments ranging from "you can't tell a client how to spend their own money, and they won't listen to you anyway" to "clients will just shut down if you try to talk about budgets with them."

Yet the reality is that for virtually all clients, the majority of their wealth is their human capital, which is converted to income over time, and that channel from human capital to financial capital is their cash flow statement. Or viewed more directly, for most clients, their cash flows are their daily experience with their money, and the aspect of money that is most tangible to them. Yet again, we as planners tend to spend FAR more time talking about assets that are only used for distant future goals, than we do about cash flows that clients can relate to every day.

Personally, I have to admit that I think Don has a good point here. A lot of planners really do spend nearly all of their time doing planning between just 12 and 2 o'clock on the cash flow pie/clock, even amongst those who try to have a holistic and comprehensive focus. Even if there is some time spent on other parts of the cash flow pie, it still pales in comparison to how much time we spend between 12 and 2 o'clock, and how much we focus on the balance sheet instead. Why are we so averse to spending more time on spending? Is it because that's not "where" we get paid for our services? Is it because we're uncomfortable talking about spending issues with clients? Is it something else?

So what do you think? Are planners overly fixated between 12 and 2 o'clock on the cash flow pie/clock? Why don't planners spend more time on the rest of the pie? Should we be more oriented towards the client's cash flow and income pie, and less focused on the balance sheet? Do we need to be?

IMO, if a planner does not look at taxes, liabilities, and spending, then they are NOT offering comprehensive/holistic advice, despite what their marketing materials might say.

I’d say the focus on 12-2 o’clock is mainly due to advisor fee structures – i.e., commissions, AUM – where the advisor doesn’t get paid (or doesn’t think he’s getting paid) to review the other important areas of a client’s financial life.

I think excluding/minimizing the time spent on the 2-12 o’clock items it’s also a missed opportunity for many planners, particularly those that serve a more ‘middle-income’ client (which I define as someone with < $1MM net worth and < $150k annual household income). There can be a relatively large value-add to a client by helping them minimize taxes, balance current spending needs with saving needs, and managing liabilities (managing a mortgage properly can have a big affect on wealth-building). Finally, I'll put in a shameless plug for the Alliance of Cambridge Advisors (http://www.acaplanners.org/index.aspx), of which I’m a member. ACA members DO look extensively at client’s spending, taxes, and liabilities.

This is a great post Michael and a subject I thought about extensivly when I searched for and created my business model.

I don’t really have much to add because I was going to write almost exactly what Brent wrote.

I think it has to do with fee structures and I will second the plug for ACA or a similar retainer model that allows the advisor to get paid beyond the assets under management or by the hour.

To say that clients won’t create budgets is false. It is the job of the financial planner to get them excited about budgets.

I did not use a budget (or save any money) for many years. Then I read “Your Money or Your Life” and learned that it was possible to retire early by saving effectively (the possibility had not occurred to me previously). Once I was motivated to save and budget, I saved and budgeted like a madman. It is the financial planner’s job to find what motivates each client to save and budget and to make the pitch for saving and budgeting that will work for that particular client.

You cannot win them all, of course. But you certainly should be trying. As you note, the saving/budgeting question is far more important than most of the stuff between 12 and 2 on the clock. I think planners focus on that stuff because it can be easily reduced to numbers and because there is a sense that there are right and wrong answers for that stuff; it makes the planners feel that they are being useful to give answers known to be right but the more important work is in the areas where what is right is less immediately clear.

Rob

Who is the author of the book you mention, there are 3 listed by that title when I searched it. Any other must-reads?

One problem with focusing on spending is that it takes a great deal of time and involves helping clients change behavior. This is the biggest challenge. I have a group of clients that hire me to focus on spending. It takes monthly meetings and regular interventions. In one case i do not manage any money for these clients. Can we afford to spend so much time with not being adequately compensated. Those with spending problems, not surprisingly, have little in savings.

Ira Fateman

Michael–Great insights. From where did you get the categories and percentages to draw your pie chart above. I’d like to know what those actual averages are.

Thank you.

Mike,

I believe Don created this chart for himself with his clients.

But there are similar charts around – for instance, “Where Does The Money Go” by the Department of Labor at http://www.psfk.com/wp-content/uploads/2010/11/Where-Does-The-Average-Consumer-Spend-Their-Paycheck.jpg which I cited back in another Nerd’s Eye View blog post at https://www.kitces.com/blog/worried-about-spending-focus-on-what-really-matters-and-its-not-the-small-stuff/

I hope that helps a little!