Executive Summary

In today's low-return environment, retirees have become increasingly stressed about the potential risk of outliving their retirement assets, which in turn has led to an increasing call for strategies that at least partially annuitize a portion of the portfolio. After all, a single premium immediate annuity (SPIA) provides a lifetime stream of income that by definition cannot be outlived, and the potential for long-lived retirees to earn mortality credits creates the potential to earn significantly more cumulative return than what bonds alone can pay. In fact, a great deal of research over the past decade has shown that partial annuitization of a portfolio can improve retirement income sustainability over portfolio-based strategies alone.

Yet in new research produced by yours truly, along with retirement researcher Wade Pfau, it appears that the prior research may not be entirely correct. While it's true that for extreme longevity scenarios, SPIAs provide an unparalleled return and enhance retirement outcomes, the strategy as commonly implemented is also an indirect form of a bucket strategy that disproportionately liquidates fixed-income assets in the early years and lets the rest of the (risky) portfolio run. By reducing withdrawals from risky assets in the early years, the exposure to potentially unfavorable return sequences is diminished, even as the total allocation to equities rises throughout retirement.

In fact, as the results show, the majority of the benefits commonly attributed to partial annuitization are actually just the indirect result of a bucket strategy that produces a rising equity glidepath. While SPIAs do still provide superior results for very long-lived retirees, it truly takes extreme longevity - i.e., married couples living beyond age 100 - before the contribution from mortality credits actually outweighs the benefits of just using a strategy that liquidates more fixed income in the early years and allows equity exposure to rise. Accordingly, the bottom line is that for retirees who truly want to hedge extreme longevity, the benefits of SPIAs remain unmatched, but for most retirees who will not live that long the reality is that SPIAs not only fail to provide benefits, but they can actually produce results inferior to just replicating the rising equity glidepath without annuitizing at all!

The Benefits Of Partial Annuitization Using A Single Premium Immediate Annuity (SPIA)

The seminal paper demonstrating the benefits of annuitizing a portion of a retiree's portfolio was "Making Retirement Income Last A Lifetime" by Ameriks, Veres, and Warshawsky in the Journal of Financial Planning in 2001. Building from the roots of Bill Bengen's "safe withdrawal rate" approach, the researchers examined the benefits of partially annuitizing 25% or 50% of the client's portfolio into a single premium immediate annuity SPIA), versus just holding a stock/bond allocation, assuming a 4.5% withdrawal rate (deliberately selecting a withdrawal rate that would have at least some risk of failure, to see if annuitization enhanced the results).

The approach in the research was fairly straightforward - retirees would rely on the annuitized funds for spending cash flows in the early years, and only increase withdrawals from the portfolio as necessary in later years to keep up with inflation. Accordingly, the portfolio would not need to be tapped as much for distributions in the early years, which would allow the retiree to defend against liquidating during a potentially unfavorable sequence of returns in the early years (as an extended period of mediocre returns in the first half of retirement while ongoing withdrawals are occurring is the primary risk for a retiree).

The results were rather striking; on a Monte Carlo basis, the 4.5% withdrawal rate for a moderate growth portfolio had a 12.6% risk of depletion, while annuitizing 25% of the assets dropped the risk of failure to 7.8% and annuitizing half the portfolio dropped it down to only 3.3%. Similar results were seen whether the time period was shorter or longer (though obviously, the longer overall time period, the greater the probability of failure across all approaches). In fact, over long time horizons, the results were so favorable that not only were the probabilities of success higher, but for conservative portfolios the median wealth was actually slightly higher in the annuitization scenarios than the non-annuitization scenarios; in other words, even though the retirees surrendered the liquidity of their annuities up front, if their retirement lasted long enough the non-annuitized half of the conservative portfolio actually grew larger than if the retiree just kept the entire conservative portfolio invested and taking withdrawals in the first place! (Though for the aggressive growth portfolios, median wealth was higher by just investing it all.)

The results of Ameriks et. al. were hailed as a major breakthrough supporting the value of partial annuitization; Google Scholar notes that the paper has been cited at least 68 times since it was published. On the one hand, the conclusions seemed almost intuitively obvious: supporting retirement with annuitization in the early years so that the portfolio only had to support material withdrawals in later years was essentially a bucketing approach that reduced exposure to sequence risk for the portfolio investments, while racking up mortality credits from the SPIA along the way. On the other hand, though, the reality is that relying on the fixed portion of the portfolio in the early years doesn't necessarily require using a SPIA in the first place, and it wasn't entirely clear how much was due to SPIA mortality credits, and how much was just a creative liquidation strategy!

The Flaws Of SPIA Partial Annuitization Research

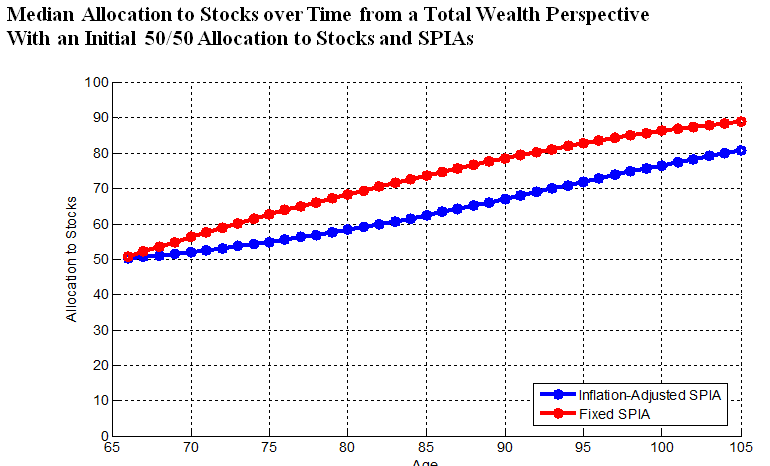

Viewed from a total wealth perspective, the reality of the Ameriks et. al. study (and others like them) is that as withdrawals are funded by a SPIA in the early years while the portfolio is allowed to grow, the retiree's asset allocation actually shifts over time. For instance, imagine a simplified scenario where Investor A holds $500,000 in stocks and $500,000 in bonds, while Investor B holds $500,000 in stocks and puts the other $500,000 into a SPIA. According to the Ameriks research, Investor B should come out with a more sustainable retirement income, due in large part to the fact that withdrawals from equities will be diminished during the early years, as the SPIA covers most of the withdrawal needs. Yet if we advance this scenario forward by 15 years, the equities will have likely risen (with long-term growth investments and a relatively small level of ongoing withdrawals), while the implied value of the SPIA will have declined (as the value goes down when the retiree doesn't have as many remaining years to live and receive payments); thus, if the portfolio is up to $700,000 (given some growth but some withdrawals), while the remaining payments of the SPIA are only worth $300,000, then the client's asset allocation is actually now 70/30 (where the 70% is liquid stocks and the 30% is the present value of the remaining annuity payments). The end result: the stocks/SPIA scenario may have started out as being 50/50, but the asset allocation has shifted up to 70/30 due to the liquidation strategy, while the 50/50 portfolio was assumed to remain at 50/50. As the years go by, the percentage of total wealth allocable to stocks would continue to rise, as shown below.

The reason this matters is that, for the purely-portfolio-based retiree, there's no reason why the same strategy couldn't be implemented without a single premium immediate annuity. In other words, if there's a benefit to disproportionately liquidating bonds in the early years and letting the stocks run, and then liquidating the stocks later, this could be done simply by using a generic 50/50 portfolio that automatically takes/most all of its withdrawals from the bonds in the early years and allows its equity exposure to rise steadily over time, mimicking the total wealth asset allocation shown above, but without actually annuitizing a portion of the wealth. Accordingly, in a new working paper that we've just posted to SSRN, retirement researcher Wade Pfau and I sought to study this exact issue, and try to determine whether or to what extent the benefits of partial annuitization are actually attributable not to the SPIA itself, but simply due to the bucketing-based declining-fixed-and-rising-equities liquidation strategy that it indirectly produces.

The results, shown in the table below, were somewhat surprising: for a 65-year-old couple at a 4% withdrawal rate, the failure rates of just taking systematic withdrawals from a portfolio that mimics the implied glidepath of a stock/SPIA portfolio were actually superior to using the inflation-adjusted (real) SPIA! In fact, the rising equity glidepath approach was so effective, it was superior to stock/SPIA portfolios and superior to fixed 50/50 portfolios! It wasn't until extreme longevity scenarios, where the 65-year-old married couple sustains withdrawals for 35+ years (beyond age 100) that the stock/real-SPIA scenarios were superior to the glidepath scenario, such that we could actually attribute the benefits of a SPIA's mortality credits to improving the outcome. And when used a fixed SPIA (not adjusting for inflation), even after 40 years (where the couple lives beyond age 105!) there was still virtually no improvement to using a SPIA over just implementing a glidepath portfolio! (For further details on the assumptions underlying this table, see the original paper.)

| Real SPIA | Fixed SPIA | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| Failure Rates | Contributions | Failure Rates | Contributions | ||||||

| Retirement Period |

Fixed 50/50 Stocks/Bonds |

50/50 Stocks/SPIA |

Implied Glidepath |

Glidepath | Mortality Credits |

50/50 Stocks/SPIA |

Implied Glidepath |

Glidepath | Mortality Credits |

| 15 | 0.1 | 2.3 | 0 | 1925% | -1825% | 1.3 | 0 | 1042% | -942% |

| 20 | 3.6 | 9.4 | 1.4 | 372% | -272% | 7.2 | 1.6 | 281% | -181% |

| 25 | 13.7 | 18.2 | 10 | 219% | -119% | 16.4 | 10.2 | 178% | -78% |

| 30 | 26.5 | 26.1 | 22.2 | 1054% | -954% | 25.8 | 21.9 | 622% | -522% |

| 35 | 37.9 | 32.7 | 33.1 | 92% | 8% | 34 | 32.6 | 137% | -37% |

| 40 | 47.3 | 38 | 41.6 | 61% | 39% | 40.6 | 40.7 | 98% | 2% |

In the case of single individuals (as opposed to a married couple), the results of the research were similar, though notably because the life expectancy of an individual is shorter, it takes fewer years before mortality credits began to make a material contribution. Accordingly, while it took 40+ years for mortality credits to make a material contribution beyond the value of a rising equity glidepath for married couples (as shown above), for individuals the benefit becomes material after "only" 25 years. As with individuals, though, the outcomes of using real SPIA continue to dominate the use of fixed SPIAs for those who do choose to partially annuitize.

Implications Of SPIA Research For Financial Planners

The implications of this research on the prospective benefits of partial annuitization are significant. First and foremost, it shows that most prior studies which indicated a benefit of partially annuitizing a retiree's portfolio were actually just showing the benefits of a bucketing strategy that liquidates fixed income assets first (allowing overall equity allocations to rise). The benefit was not actually due to the single premium immediate annuity at all - in fact, the SPIA's contribution (as represented by their mortality credits value) as actually negative but was masked by an overwhelming positive rising equity glidepath effect! On the other hand, it's notable that at least this SPIA form of bucket strategy was improving retirement outcomes, a notable difference from cash reserve "buffer zone" bucket strategies that have been shown to decrease income sustainability!

A second notable implication of the results is the mere recognition that retirees can actually have better retirement outcomes by increasing their equity allocation over time. In other words, annually rebalancing to an asset allocation that increases equity by something like 1%/year actually produces better results than just rebalancing to the same 50/50 portfolio (and certainly provides better results than decreasing equity through retirement, which has been repeatedly shown to result in lower withdrawal rates). This surprising effect - that the best approach to retirees may be to increase their equity exposure over time - is certainly one that deserves further study. Though it isn't entirely surprising; if the greatest risk to a retiree is a series of ongoing mediocre market returns throughout the first half of retirement, then it makes a lot of sense that income sustainability will be better if the retiree continues increases the weighting to stocks as they get cheaper. Notably, if stocks are in a bull market and going up, the rising equity exposure increases the impact on the retiree of a future bear market, but if stocks are in a bull market, then there was no danger to a 4% withdrawal rate in the first place (and if the client finds themselves unexpectedly wealthy, they can always take some risk off the table at that point!).

Notwithstanding all of this, it's crucial to note that the results of our new research do NOT show that SPIAs are useless or irrelevant, but simply that retirees must live materially beyond life expectancy in order to receive to gain a significant benefit from the use of a SPIA (though it's notable that the necessary time horizon is so low there's a very low likelihood that couples will live long enough to benefit, and even if the retiree does live long enough, some of the SPIA benefit is still simply due to the glidepath effect). It's also notable that because the primary scenario where SPIAs benefit are where retirees live significantly beyond life expectancy - and rack up huge mortality credits in the process - it may be even more beneficial to begin partial annuitization later than age 65 (where mortality credits are more leveraged for those who outlive life expectancy), or even to consider deferred income annuities (also known as longevity annuities) where payments are not scheduled to begin until the later years (which means few will receive any payments, but those who do survive long enough will receive absolutely enormous mortality credits). Similarly, because the primary value of SPIAs is truly living far beyond life expectancy, SPIAs that produce larger payments in the final years are superior - accordingly, rising-payment inflation-adjusted SPIAs dominate level-payment fixed SPIAs in the scenarios we analyzed.

The bottom line, though, is simply this - when evaluating the prospective benefits of a single premium immediate annuity, it's crucial to recognize that when annuitizing part of the portfolio and spending that money first, there is a beneficial liquidation strategy that has nothing to do with the actual benefits of the SPIA and everything to do with simply exercising a favorable bucketing liquidation strategy. If the former is the goal, that can be accomplished without using a SPIA at all, and simply managing the portfolio with a rising equity glidepath. If the genuine concern is to protect against extreme longevity, though, the reality is that SPIAs and the mortality credits they accumulate still produce long-term fixed returns far beyond any available alternatives for those who really do live a long time, allowing SPIAs to retain the throne as the ultimate longevity hedge (especially for those who have no bequest motive, and enough liquidity to handle health care shocks and other unexpected retirement costs along the way)!

In the meantime, for those who are interested, you can see a full copy of the study on SSRN here, and we are submitting it for publication in the Retirement Management Journal as well. You can also read my co-author Wade Pfau's own summary of some of the key takeaways from this research on his blog, and if you're looking for further objective information and education about annuities, check out my book "The Advisor's Guide To Annuities" as well!

Thanks for a very thought provoking article.

The biggest weakness I see is the singular focus on failure percentages without considering the magnitude of failure.

Here is an extreme example. Imagine a person wants a retirement lifestyle of and inflation adjusted 5% of their portfolio. And lets assume that a rising equity portfolio has an 80% chance of success. We can compare this to using all the money to buy a inflation indexed immediate annuity which let’s assume pays 4.5%. Clearly this second option has a 0% chance of success since it will never be able to support 5%.

But what does failure look like for each of these scenarios? In the first one failure could mean a lifestyle drop of more than 50%. In the second one, while failure is guaranteed, the worst case lifestyle drop is only 10%. At this point it is clear that one is not necessarily the slam dunk choice the success percentages might lead one to believe.

If you want to use a single metric, you probably want to use something akin to expected shortfall of utility – chance of shortfall x amount of lost utility (amount of loss plugged into utility function that takes a loss aversion parameter).

Other thoughts that came to mind.

* What happens if you keep allocation constant through buying additional SPIAs as person ages (e.g., when stocks become more than 60% of the allocation “rebalance” by buying additional SPIA – realistically this becomes problematic 85+). This would actually be a more traditional following of the bucket strategy.

* How does using an immediate variable annuity for the stock portion change things?

Keep up the great work!

David

very thoughtful article, of course since you’ve spoken so eloquently about reverse mortgages in the past they could be the assurance needed to make up for lack of survival rates spoken of in your article (along with other, proper planning)

Regarding ….”This surprising effect – that the best approach to retirees may be to increase their equity exposure over time – is certainly one that deserves further study.”

Spitzer and Singh (2007 June Journal of Financial Planning) tallied up the drawdown choices in their Table One. At the higher starting equity % allocations the portfolios failed less when bonds were drawn down first, than when stocks were drawn down first. But re-balancing did better than both.

Research Associates did work at http://www.researchaffiliates.com/ideas/pdf/fundamentals/Fundamentals_Sep_2012_The_Glidepath_Illusion.pdf and Estrada did work at http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2217406

Regarding the idea that a certain annuity can be better replaced with “a managed portfolio with its equity % allocation growing in importance” seems to me lacking in practicality. An 85 year old will simply have lost mental acuity and the emotional tolerance for equity volatility, and will be ripe for the picking if relying on ‘helpers’ to do this for him/her.

I can just see myself at 95 reading the web every week to check my stock portfolio.