Executive Summary

As we begin 2014, a number of issues loom that may have broad impact for advisors in the coming year. Perhaps most significant is the fact that we may finally see some activity on the regulatory front; the next fiduciary proposal from the Department of Labor is targeted for August of 2014, and while the SEC may be taking a back seat on the fiduciary issue and waiting for the DOL to act, the regulator has committed itself to step up oversight (i.e., examinations) of investment advisers, and may even take up the recent SEC Advisory Panel's recommendation to begin levying "User Fees" on RIAs to help fund increased oversight. On the other hand, the CFP Board may also face its own turmoil this way in its ability to oversee CFP certificants, as the challenging Camarda case plays out.

In the meantime, the slow-motion trainwreck that is the advisory industry's demographics problem will continue to play out; the latest Moss Adams study showed that employee advisors are now outnumbering owner advisors, yet the number of advisors available to hire who have capacity for new clients continues to dwindle. While the anticipated mass exodus of retiring advisors has been more like a trickle so far - for a number of reasons - the veteran advisors who remain still cannot solve the capacity of growing firms that need to hire younger advisors to take the lead. In the coming year, the problem is going to become a lot more noticeable.

The third key trend for 2014 will be the continued rise of the "robo-advisor" but with a more nuanced look; while the robo-advisors seem to have exploded onto the scene in 2013, the reality is that by numbers, most of them are still quite tiny (especially relative to the venture capital they raised), and none appear to actually be economically viable and even running at a breakeven pace yet (much less making the return-on-equity profits their funders expect). In the coming year, we'll begin to see which robo-advisors will outpace the others and pull ahead, and many will aim to refine their models; some may even decide that it's more constructive to be a partner with advisors than a competitor, given the reality that most robo-advisors are actually more in competition with online brokerage tools like Schwab and E-Trade than human advisors. At the same time, it may be the heavily technology-enabled advisors - the "cyborg advisors" - who really begin to shine, blending the best of technology and human skills that pulls ahead of both the robo-advisors and the humans.

And in the meantime, the potential for a bear market will continue to loom in the coming year. Whether 2014 turns out to be the next stock bear market - or a rapid unfolding of the long-anticipated bond bear market - remains to be seen. But if 2014 is the next big one, expect the decline to ripple across the industry, as advisors who have rapidly grown their AUM businesses receive a stark reminder of the importance of profit margins to protect against the inevitable revenue declines that come from time to time, as many advisory firms are now so large that they cannot simply grow their way through a bear market with new clients!

Fiduciary Regulation Redux

At the beginning of the year, the predictions (including from yours-truly) were that 2013 would be the year that we saw some kind of fiduciary regulation. The Department of Labor was promising to deliver its fiduciary proposals, updated and amended from the original offering they provided in 2010 and withdrew in 2011, while at the same time pressure was growing on the SEC to act as well and it had put proposed fiduciary rulemaking on its priority list. While 2013 turned out to be far more hype than action regarding fiduciary regulation, the building pressures suggest that 2014 could still be "the big year" for the onset of regulatory change.

On the DOL front, the fiduciary rulemaking process continues to be a regulatory priority in 2014, and as of now the "Conflict of Interest Rule-Investment Advice" is scheduled for its next draft release in August of 2014. At its core is a provision that would expand the definition of fiduciary under ERISA to include not only those who provide investment advice to employee benefit plans, but also those who provide investment advice with respect to IRA rollovers. Although it remains to be seen if it will be specifically enumerated under the rule, the fear from the brokerage industry is that a fiduciary rule extended to IRAs could eliminate commissions on investments held inside IRAs, and the brokerage industry claims that without the availability of commissions that the majority of Americans with smaller IRAs would be priced out of the market for advice. On the other hand, fiduciary advocates point out that consumers may end out paying a lesser price under a fiduciary rule with fewer commission-laden products, and that in theory brokers were only supposed to be providing limited investment advice "incidental" to the sale of securities anyway; accordingly, a fiduciary rule can lift the quality of advice the middle class receives, and reduce the conflicts of interest impacting the advice, while also reducing their costs. Ultimately, it remains to be seen what the final details of the DOL's revised fiduciary rule will contain, and whether/how it will try to accommodate all the different business models seeking to serve consumers while still applying a fiduciary standard to the delivery of advice.

At the same time, the SEC has also put a fiduciary rule on its 2014 regulatory agenda, and SEC chairowman Mary Jo White has indicated that fiduciary rulemaking remains a priority for the SEC; nonetheless, the rule is currently flagged as a "long-term action" under the SEC with no specific timetable, suggesting that the SEC may be waiting to let the DOL propose a rule first. Which organization takes the first step matters, as there is a strong potential that the definition of fiduciary under one will likely set precedents for the other (either as an industry compromise, or simply because regulators acknowledge that there could be some overlap between SEC and DOL rules and having conflicting rules could be even more problematic for advisors to follow). At the same time, opponents of the fiduciary rule have expressed concern that the DOL's likely action may be more stringent than the SEC, and consequently have even lobbied in the past year for legislation that might require the SEC to act first (though at this point there has been no momentum on the bill). In the meantime, a recent SEC Advisory Panel on fiduciary concluded that the SEC should act to implement some form of fiduciary duty on brokers who provide personalized investment advice, providing another nudge for the SEC to act.

Aside from the prospective fiduciary action - which realistically looks more likely to be the DOL taking the lead in 2014, with the SEC to perhaps follow thereafter - the other regulatory issue likely to see some activity in 2014 are enhancements to the oversight of Registered Investment Advisers. In other words, efforts to lift the frequency of exams for RIAs. The starting point will simply be a more aggressive schedule for auditors, as Commissioner White at the SEC has already warned, but the SEC arguably still lacks the resources to visit RIAs as frequently as they'd like, which means potential proposals for RIA user fees may surface again in 2014, especially after the SEC's Advisory Panel recommended it as a way to finally move forward on Section 914 of Dodd-Frank.

In the meantime, the CFP Board may face its own challenges in its ability to "regulate" and oversee financial planners. Beyond just an ongoing imbroglio over its compensation disclosure rules, 2014 could see a resolution to the ongoing Camarda case, which at this point is about more than "just" the actual compensation disclosures that Camarda used, but about the CFP Board's capability of overseeing and enforcing its own rules; a setback in the Camarda case could be an even more significant long-term setback to the legitimacy of the organization as a potential future oversee for financial planning and keeper of the professional standards.

The bottom line: While there may be no big new final rules implemented in 2014, this may be the year where we finally see the fiduciary template the DOL is going to set forward, which could become the precedent for the SEC as well. And either way, the SEC is finally increasing its focus on more exams for investment advisers, even if it takes user fees to fund the effort. In the meantime, don't expect FINRA to be silent, either; it's still trying to position itself - a la its recent "Report on Conflicts of Interest" - to be the regulator for all advisors, both brokers and RIAs, under a "harmonization" of the regulatory standards. And stay tuned for ongoing developments with the CFP Board's case against the Camardas.

Slow Motion Demographics Trainwreck Of Advisors And Their Clientele

While the impact of "demographics" is certainly nothing new, nor is the point that the average age of advisors continues to rise every year as there are not nearly enough newer/younger advisors coming in to replace those who are retiring, 2014 may finally mark the year where we really begin to take notice of the problem. As with the proverbial "boiling frog" in the pot that never realizes when to jump out as the temperature rises, the reality appears that we may already be past the point of no return for the industry's demographic dilemma; now the only question is how the shortage plays out until the situation rectifies itself.

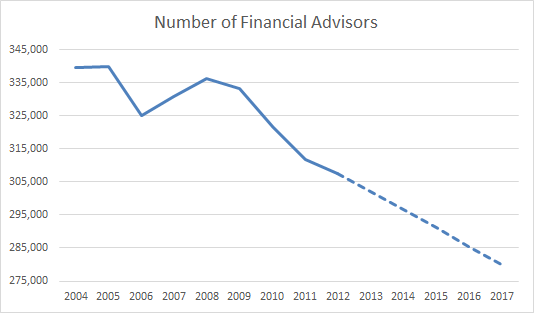

In fact, estimates from Cerulli (see chart below) suggest that the number of financial advisors may have already peaked prior to the financial crisis, and has been in a steady decline since then - a trend anticipated to continue as more and more baby boomer advisors reach retirement age and the industry attritions a net of about 2% of advisors per year through 2017.

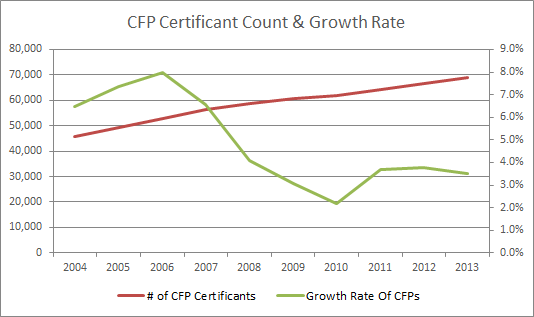

Of course, not all "financial advisors" in the Cerulli data are providing financial planning, and overall the number of CFP certificants continues to grow. Nonetheless, the rate of growth for CFP certificants is slowing as well, as the chart below shows, suggesting that the aging of the advisor population and rise of retiring advisors is beginning to take its toll there as well. In fact, as the CFP Board's own certificant demographics data reveals, there are currently more CFP certificants in their 70s than there are in their 20s!

Of course, given what is still a relatively modest attrition rate, it's not likely that there will be any sudden catalyst in 2014 (though an 'unexpected' bear market that puts pressure on a large number of advisory firms could accelerate the trend). And as I've noted in the past, it's not entirely clear if advisors are even going to exit as quickly as anticipated, or if a rising number of veteran advisors will simply decide to convert their businesses into "lifestyle practices" and simply let them wind down slowly throughout their later years (which means the 'great exodus' of advisors could be less about retirement and succession planning, and instead more about holding practices until death and 'final exit' planning). On the other hand, the pace of baby boomers retiring from the advisory industry may accelerate now that the earliest baby boomers will be turning 70 in 2014!

Nonetheless, the fact that baby boomer advisors may be retiring more slowly than once anticipated doesn't resolve the underlying problem - a dearth of new advisors who actually have capacity to take on new clients, coinciding with a stage of industry growth where firms are getting larger and larger and are increasingly looking to hire "employee advisors" who have capacity for client growth. In the emerging "age of employee advisors" a veteran advisor at capacity with a lifestyle practice may as well be retired for a firm that's looking to hire.

Which means from the practical perspective, where the dearth of advisors is about to become most noticeable are the firms that are actually growing and trying to hire more financial advisors for capacity. Whether trying to hire a newer financial planner, or an experienced one (that isn't already full of clients), we're seeing this trend play out in our recruiting businesses, and the trend is becoming apparent in the Moss Adams benchmarking surveys, which are showing upward pressure on compensation for experienced "lead" advisors that can be responsible for client relationships. Of course, what may be a shortage of talent for firms that want to hire also paints a remarkably positive outlook for any newer advisors looking to enter (or who have recently started) in the business, as the dearth of younger advisors and competition for top talent should help to lift the financial benefits of a financial planning career in the coming years!

The bottom line: As the number of advisors falls down towards multi-decade lows, the squeeze for talent and the industry's demographics problems are going to become noticeably worse. Ultimately, this will put upward pressure on the compensation of advisors that helps to rectify the problem as the supply eventually rises to meet the demand, but not without a significant lag, which means the problem is likely to get worse before it gets better!

Robots Vs Cyborgs (Vs Humans)

In retrospect, it seems like 2013 may have been the year of the robo-advisor, given how much attention they received in the industry and consumer media. From Betterment and Wealthfront to LearnVest and Personal Capital, the robo-advisors have made a big splash in the advisory world. Notably, though, the reality is that their actual businesses are still small; while Betterment and Wealthfront are each touting several hundred million in AUM, at their billing rate of 0.25% or less, this amounts to less than a million of revenue, which doesn't likely even cover the salaries of their dozens of computer engineers and other staff. Which means that while they're visible and perhaps gaining some traction, none of the robo-advisors are even at breakeven viability yet, much less profitable (and certainly not at the levels of return-on-equity that their venture capital funders likely expect), and none have ever tried (much less successfully) navigated a bear market with their clients to find out whether the websites, apps, and algorithms are really enough to help investment clients "stay the course" in the midst of turbulent markets.

From a broader perspective, though, the reality is that many "robo-advisors" are really not online financial advisors at all; they're purely online investment-only tools, and do not provide comprehensive personal financial advice beyond the portfolio itself. In fact, as online investment-only tools, the reality is that perhaps most robo-advisors are more directly in competition with other brokerage firms with online tools for self-directed investors, from Schwab to E-Trade, than they are with financial advisors who provide a wide swath of other personal advice services to people who generally have chosen to delegate to advisors rather than do it themselves (with online tools or otherwise). In other words, robo-advisors may not really be competition to human advisors in the first place, because each provides substantively different services for a different type of clientele.

Nonetheless, the fact remains that while the robo-advisors may be too much computer and not enough human to help clients really change their behaviors and avoid market panics, arguably many of today's advisors are "not enough robot" and grossly underutilize tools and technology that could make (financial) life easier for themselves and their clients. To some extent, this may be because of a dearth of venture capital and private equity being invested into solutions for advisors in key areas, but it's hard to deny that the industry has been slow adopters of new technology as well, from social media to client financial dashboards to basic website design and overall adoption of the cloud. Yet the potential for advisor benefits from technology is tremendous; a Fidelity study earlier this year showed that on average Gen X & Y advisors have more profitable practices than baby boomer advisors, and the key distinction was their heavier utilization of technology.

Accordingly, this suggests that the real winners in the battle may not be the "robo-advisors" or the humans, but instead the "cyborgs" - part human, part technology blends that seek to leverage the best of both worlds to provide the best solutions and experience for their clients. In point of fact, this is actually the case already for both LearnVest and Personal Capital, which heavily leverage technology to have "virtual" relationships with clients, yet build entirely around individual human being advisors as the core of the relationship with clients. And as advisors increasingly go to the cloud, this kind of offering becomes more and more feasible for the average advisor as well. In a world where advisors can easily have digital presences, communicate effectively using virtual tools, and have effective collaboration tools with clients, the lines between "human" and "robot" may begin to blur.

In any event, if 2013 was the year that robo-advisors first really got noticed, 2014 will be the year they start to mature and we begin to see which will take the lead and which will fall behind. Although it's unlikely that any of the robo-advisors will actually go out of business entirely until the next bear market comes along, expect to see this space heat up more in 2014, and for the robo-advisors to begin to further distinguish and refine their business models. Some may ramp up their competitiveness with advisors - Personal Capital is the most direct competitor for traditional advisors now - while others may decide that advisors are better partners than competitors, and that online investment tools can complement a human providing more holistic advice.

The bottom line: while it still remains to be seen which robo-advisor models will prove viable - if any of them - and all of them are still small businesses (especially relative to the amount of capital they were funded with), expect to see a lot more activity in this space in the coming year. Along with, perhaps, a few more new tools for advisors to become more "cyborg-like" and take the robo-advisors on head-to-head.

Honorable Mention: The Next Stock (And Bond) Bear Market

While the aforementioned issues will play out throughout 2014, the reality is that the biggest potential issue for all of 2014 is also a total wild card: the next bear market in stocks, and the emergence of a potential bear market in bonds, which may or may not occur in 2014. Certainly, it seems presumptions to just "call" a bear market for 2014 without a catalyst - not that all bear markets even need catalysts, but there have been no shortage of potential stock and bond bear market catalysts in the past several years which haven't come to fruition either. But it would be remiss not to acknowledge what a significant impact a prospective bear market could have, in part because of how it may interrelate to the other trends underway.

On the one hand, a sharp bear market could spell the early demise for a number of robo-advisors; if a severe bear market takes 25%-35% off their asset bases (bearing in mind most are very equity-centric due to their relatively young clientele), and they experience client attrition on top of the decline, chopping their revenue by half or more, the funding for robo-advisors (whether new funding for new entrants or additional funding for existing entrants) will likely dry up altogether. While this doesn't mean the "robo-advisor threat" will vanish altogether in a bear market - in fact, the few that survive may grow even stronger as they learn from their experiences - it would likely put a pall on the space for several years, potentially giving advisors some "breathing room" to catch up.

On the other hand, a bear market will likely hit advisors quite hard as well, as it always does. The impact may be even more noticeable this time around, though, as the ongoing transition of financial advisors to AUM practices will provide a stark reminder of the importance of having a sufficient profit margin in the advisory practice to absorb the consequences of a bear market and its revenue impact. While a firm with $20M of AUM can often grow enough new clients to replace the lost revenue in a bear market, it's much harder to do with $200M under management, and virtually impossible for all but a few super-fast-growing-firms with more than $500M of AUM. While this doesn't necessarily mean that the AUM model is a "bad" one, it will be an important reminder that such businesses much be managed over the entire economic cycle, and may slow the pace of hiring, as well as the pace of practices being sold (as few want to sell their businesses at the bottom of a market decline). On the other hand, for a number of advisory firms that were only marginal in the first place, a bear market may simply put them out of business altogether, leading a number of veteran advisors to simply walk away from their practices and retire at that point.

Notably, though, a bear market - especially one in bonds - will have some benefits, too. While low interest rates have had a pervasive negative effect on the industry, and rising interest rates may be bad for bond prices, and the housing market, they're actually good for the profitability of many other parts of financial services. For instance, higher rates will give room for money markets to pay a decent yield, but also for money market providers to finally earn a spread again; expect to see an explosion in the profitability of the custodian business as providing money markets becomes profitable again. Rising rates will also provide some welcome relief to much of the insurance industry, as everything from secondary-guarantee universal life to long-term care insurance has suffered mightily in the extended low-return environment, and higher interest rates should dramatically slow the pace of premium increases.

The bottom line: while it's hard to know whether the next bear market will really come in 2014 or some point down the road, the next one that comes - especially since it may be a stock and bond bear market simultaneously - could be very disruptive for today's advisory practices, especially if they are not run with an appropriate margin of safety. At the same time, though, higher rates may be a boon for other parts of the financial services industry!

[…] These Are The 3 Biggest Issues Facing Financial Planners This Year (Nerd’s Eye View) […]