Executive Summary

The IRA aggregation rule was created to limit the ability of taxpayers to take advantage of ‘abusive’ IRA tax strategies, by requiring that all IRAs are aggregated together to determine the tax consequences of a distribution from any of them.

The primary impact of the IRA aggregation rule is to determine how much of an IRA’s non-deductible contributions are treated as an after-tax return of principal when a taxable distribution occurs, whether as a withdrawal or a Roth conversion. And by forcing all accounts to be aggregated together, the rule severely limits many individuals from taking advantage of the so-called “backdoor Roth contribution” strategy.

However, the IRA aggregation rule reaches much further than just the taxability of after-tax contributions in existing IRAs. Thanks to the recent Bobrow case, it now also applies to the limitation of no more than one 60-day rollover in any 12-month period. Though on the plus side, the IRA aggregation rules apply to required minimum distribution (RMD) obligations as well, allowing a distribution from any IRA to satisfy the RMD rules for all IRA accounts!

Fortunately, though, the IRA aggregation rules do not apply when calculating substantially equal periodic payments (SEPP) under Section 72(t), reducing the danger that a withdrawal from one IRA could constitute a “modification” of the ongoing 72(t) distributions from another that would trigger a retroactive penalty. However, even in the case of SEPPs, the IRA aggregation rules will still apply in determining how much of a 72(t) payment constitutes a tax-free return of non-deductible contributions!

What Is The IRA Aggregation Rule?

The IRA Aggregation Rule, under IRC Section 408(d)(2), stipulates that when determining the tax consequences of an IRA distribution – particularly the “pro-rata” rule under IRC Section 72(e)(8) and also the early withdrawal penalty under IRC Section 72(t)(1) – the value of all IRA accounts will be aggregated together for the purpose of any tax calculations. And notably, per IRC Section 408(d)(2)(C), the calculations are done based on the close of the taxable year, which means new contributions or rollovers at the end of the year can impact the tax treatment of withdrawals or Roth conversions that occurred earlier in the year!

Notably, this IRA aggregation rule under IRC Section 408(d)(2) is explicitly only for IRA accounts; employer retirement plans, like a 401(k), 403(b), or profit-sharing plan, are not included in applying these IRA aggregation rules. In addition, under Treasury Regulation 1.408-8, Q&A-9, an inherited IRA is not aggregated together with an individual’s own IRAs, nor is a Roth IRA. And since the IRA rules are applied individually (even as a married couple, the tax consequences are determined individually before being reported on a joint tax return), an individual’s IRA is never aggregated with a spouse’s own IRA accounts.

Given that the treatment of a traditional IRA is that any distributions are pre-tax funds and 100% fully taxable anyway, the IRA aggregation rule is often a moot point. As when a distribution is already 100% taxable, there’s no pro-rata formula to apply, and if applicable at all the 10% early withdrawal penalty would apply to the entire account anyway.

However, as soon as an IRA has any non-deductible (i.e., after-tax) contributions included, the IRA aggregation rule is immediately relevant.

The IRA Aggregation Rule And Pro-Rata Distributions Of Non-Deductible (After-Tax) IRA Contributions

When an IRA has received any non-deductible contributions, the distribution of those dollars is received tax-free as a return of (after-tax) contributions. The amount of any non-deductible contributions that have been made over time is tracked on IRS Form 8606.

The caveat, as noted earlier, is that when a distribution occurs from an IRA that includes non-deductible contributions, the calculation to determine how much of the distribution will be a return of principal must be done on a pro-rata basis under IRC Section 72(e)(8). (Unlike a Roth IRA, where under IRC Section 408A(d)(4)(B) distributions are presumed to come explicitly from after-tax contributions first.)

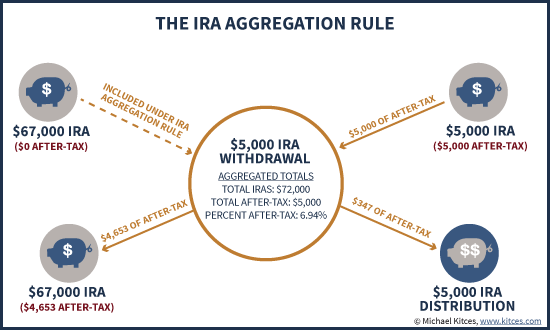

Example 1a. Charlie has a $72,000 IRA that includes $5,000 of non-deductible contributions made years ago, and tracked as such on Form 8606. If Charlie decides to take a $5,000 withdrawal, though, he can’t just take out the $5,000 of after-tax contributions on a tax-free basis (the way he could receive back his after-tax contributions from a Roth IRA); instead, the pro-rata rule applies. Since Charlie’s account is $5,000 / $72,000 = 6.94% after-tax, his $5,000 withdrawal is deemed to be only $347 of after-tax funds (6.9% of the $5,000) and the other $4,653 is taxable. In turn, the remaining $4,653 of after-tax funds remains behind as part of the $67,000 that is still in his IRA account.

Example 1b. Continuing the prior example, assume instead that Charlie had an existing $67,000 IRA that was all pre-tax funds, and had more recently made a $5,000 non-deductible contribution to a brand new IRA #2. But Charlie has decided that he needs to use some of the money, so he now wants to distribute the $5,000 non-deductible IRA, hoping to recover the funds tax-free.

Unfortunately though, even if Charlie withdraws just $5,000 from just IRA #2 that had just after-tax funds in it, the tax consequences are still the same as the preceding example – Charlie’s total IRA accounts are $72,000, his total after-tax funds are $5,000, which means the $5,000 withdrawal will be 6.94% return of after-tax funds with the remainder taxable. Thus, Charlie will end out reporting $4,653 of his withdrawal as taxable, even though he solely converted IRA #2 that originally had only after-tax contributions!

Ultimately, example 1b and the associated chart above show how the IRA aggregation rule plays out when multiple IRAs are involved. Even a distribution comes from an account that was otherwise 100% funded with non-deductible after-tax funds, it still ends out being partially taxable if/when any other IRAs are aggregated into the calculation! And notably, the end result of this strategy in the example above is that the remaining $4,653 of after-tax funds not treated as being part of the withdrawal from IRA #2 have effectively be transmuted into after-tax contributions associated with IRA #1 (even though the contributions were never made to that account in the first place!)!

The IRA Aggregation Rule And Roth Conversion Strategies

Notably, the IRA aggregation rule doesn’t just apply to taxable withdrawals from an IRA. The aggregation rule applies to any taxable distribution/event from the IRA, and under IRC Section 408A(d)(3)(C) a Roth conversion is treated as a taxable distribution. Thus, if in Example 2 if Charlie’s goal had been to convert the $5,000 non-deductible IRA contribution, rather than just withdraw it, the same tax consequences would apply – even if Charlie just converted the $5,000 IRA #2 that contained only after-tax contributions, the conversion would have been treated as $4,653 taxable, only $347 of after-tax funds, and the remaining after-tax money that had originally gone to IRA #2 would now be treated as being associated with the other IRA instead!

This caveat of applying the IRA aggregation rules to Roth conversions can be especially problematic in situations where someone is trying to engage in the so-called “backdoor Roth contribution” strategy, where a high-income saver contributes to a non-deductible IRA with the intention of converting it shortly thereafter, effectively making a Roth contribution while circumventing the income limits that normally apply to a Roth contribution. The problem is that if the saver already has other existing IRAs (ostensibly with pre-tax dollars), those IRAs will be aggregated together with any new non-deductible contributions when the conversion occurs, effectively limiting the strategy.

Example 2a. Jenny is a high-income earner with over $300,000/year in wages, rendering her ineligible to make a Roth IRA contribution. However, Jenny can still make a contribution to her IRA, and while her income combined with her active participation in an employer 401(k) plan limits the ability to deduct the IRA contribution, she can always make a non-deductible contribution as long as she has any earned income. Accordingly, she decides to contribute $5,500 to her (non-deductible) IRA, and then after waiting an appropriate period of time to avoid the step transaction doctrine, she converts the IRA to a Roth IRA. And since the IRA was funded entirely with non-deductible contributions, there is no tax due for the Roth conversion (except to the extent of any gain between the time of contribution and subsequent conversion). The end result – Jenny put $5,500 into her Roth IRA for the year, and while she didn’t get a tax deduction (that she couldn’t have gotten anyway), she didn’t owe any more in taxes either and got the maximum contribution into a Roth!

Example 2b. Continuing the prior example, assume that Jenny also had $200,000 of existing (pre-tax) IRA funds in place. Now, when Jenny makes a $5,500 non-deductible contribution and then attempts to convert it, she cannot convert just the $5,500 IRA (when she contributed to the existing $200,000 IRA or funded a new separate account); instead, her conversion is subject to the IRA aggregation rule, and the tax consequences are determined on a pro-rata basis across all the accounts. The end result: since Jenny’s total $5,500 non-deductible contributions are only 2.68% of her $205,500 total IRA accounts, the conversion of the new IRA will be treated as only $147 of after-tax, and $5,353 of pre-tax funds that are taxable at conversion! The existence of the other IRA, due to the IRA aggregation rule, has eliminated Jenny’s ability to engage in the backdoor Roth strategy!

Notably, though, since the IRA aggregation rule only applies to IRA accounts, Jenny does have a potential workaround – she can roll over the existing pre-tax IRA funds into an employer retirement plan, which separates them from the IRA-only aggregation rule. Once rolled over, she can now convert the remaining now-just-non-deductible funds in the IRA, to complete the Roth transaction. And in point of fact, the rules under IRC Section 408(d)(3)(A)(ii) explicitly state that when a rollover occurs from an IRA to an employer retirement plan, the pro-rata rule does not apply and the pre-tax funds are rolled over first. Which means, ironically, the rules operate perfectly to allow any ‘unwanted’ pre-tax dollars to be “siphoned off” from the IRA to a 401(k) or other employer retirement plan, so the after-tax remainder can be converted! The caveat, of course, is that the strategy is only feasible if the saver has an employer retirement plan that accepts roll-ins in the first place!

Example 2c. Continuing the prior example, Jenny has just made her $5,500 non-deductible contribution to her existing $200,000 IRA, and now realizes the problem that the IRA aggregation rule presents. To resolve this, she contacts her employer and confirms that she is able to make a rollover contribution from her IRA to her current employer’s 401(k), and proceeds to do so for the entire $200,000 of pre-tax dollars in her IRA. Once the roll-in is completed, Jenny is left with a $5,500 IRA, which now includes only the after-tax dollars (because the roll-in to the 401(k) siphoned off all the pre-tax dollars!). Jenny can now convert the $5,500 IRA to a Roth, and because it still contains only after-tax contributions, there is no tax liability on the conversion!

Bobrow v. Commissioner, The Once-Per-Year IRA Rollover Rule, And The IRA Aggregation Rule

In the past, the IRA aggregation rules were applied primarily for the purpose of determining the tax consequences of a distribution (or Roth conversion) that included after-tax contributions. But thanks to the recent court case of Bobrow v. Commissioner, the IRA aggregation rule is now used in the context of the once-per-year IRA rollover rule, too.

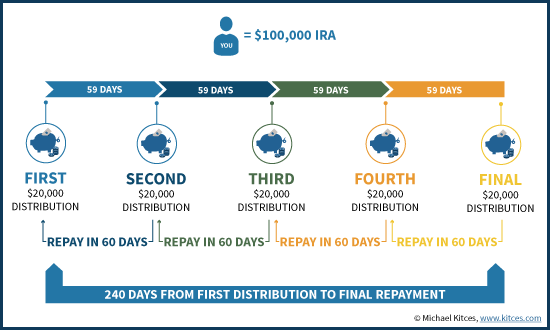

The once-per-year IRA rollover rule states that when a distribution occurs from an IRA and it is rolled over within 60 days (under the normal rollover rules), another rollover cannot occur for the next 12 month period (measured from the day the distribution occurred). In the original interpretation of these rules – and as previously explained in IRS Publication 590 – the Service had interpreted this rule to mean that no additional rollovers could occur from either the IRA that the distribution came from, or the IRA that the new funds went to. However, if the taxpayer had another entirely separate and unrelated IRA, that IRA could still engage in another rollover. And some people had actually used this rule to chain together multiple IRA rollovers (where IRA #2 repays IRA #1, then IRA #3 repays IRA #2, then IRA #4 repays IRA #3, etc.), effectively extending themselves a long-term “temporary” loan.

However, in the Bobrow case, the Tax Court reviewed the strategy (after Bobrow made a mistake in executing it, raising the attention of the IRS in the first place), and declared that the IRA aggregation rule under IRC Section 408(d)(3) should apply for the purposes of the once-per-year rollover rule, not just in the context of calculating the pro-rata tax consequences of an IRA distribution.

As a result of the court’s ruling, the IRS declared in IRS Announcement 2014-15 that starting in this current year of 2015, any IRA distribution-and-60-day-rollover from any IRA will render all of the taxpayer’s IRAs ineligible for another 60-day rollover in the next 12 months! Notably, since the IRA aggregation rule only applies to IRAs and not employer retirement plans, a distribution-and-60-day-rollover from an employer retirement plan does not trigger this rule, but any other IRA distribution-and-rollover does. In addition, it’s important to remember that a trustee-to-trustee transfer is not treated as a 60-day rollover, and consequently there is still no limit on the number of trustee-to-trustee “rollover” transfers that can occur within a year. But for any situation where the taxpayer actually takes possession of the money as a distribution, and then rolls the funds over within 60 days, the IRA aggregation rule applies to render all IRA accounts ineligible for another 60-day rollover for the next 12 months!

The IRA Aggregation Rule And Satisfying Required Minimum Distribution (RMD) Obligations

While in most contexts the IRA aggregation rule “complicates” situations by limiting proactive tax strategies (e.g., eliminating the sequential-60-day-rollovers-as-loans strategy, or the backdoor Roth contribution strategy), when it comes to required minimum distributions (RMDs) the IRA aggregation rule is actually helpful.

The reason is that under Treasury Regulation 1.408-8, Q&A-9, an IRA owner can satisfy the required minimum distribution obligations for all of his/her accounts by taking those RMDs from any of the accounts. In other words, thanks to the IRA aggregation rule, a distribution from any IRA can be applied towards satisfying the required minimum distribution from all IRAs!

Example 3. Harriet just turned 75-year-old this year, and has two IRA accounts; the first, with a value of $175,000, is invested into a variable annuity with a guaranteed minimum income benefit rider, and the second is held in a $40,000 CD. Under the Uniform Life Table in Appendix B of IRS Publication 590, Harriet’s RMDs this year will be $175,000 / 22.9 = $7,642 from her IRA annuity, and $1,747 from her IRA CD, for a total RMD of $9,389. However, thanks to the IRA aggregation rule, Harriet can actually withdraw $9,389 from any of her IRA accounts to satisfy this RMD obligation. As a result, if she wants to not withdraw from the IRA annuity – although often unfavorable, perhaps she prefers to wait on the annuity income distributions and allow the GMIB rider to continue to accrue its guaranteed income floor – she could choose to take all of the $9,389 RMD from just the IRA CD, and still satisfy her RMD obligation.

This flexibility to satisfy the RMD of all accounts by taking an RMD from any one of them can be highly valuable in situations where there are multiple IRAs but one holds assets that are less liquid, whether it’s an annuity with various guarantees that would be adversely impacted by a withdrawal, or a piece of illiquid real estate. The retiree can use the IRAs that are liquid to satisfy the RMD obligations for all the accounts, without touching the particular IRA assets that would be better to just hold in place.

Notably, though, since the IRA aggregation rule only applies to an individual’s own IRAs – whether for the purposes of calculating pro-rata distributions of after-tax dollars, or for RMD purposes – an RMD taken from one IRA may not satisfy the RMD requirements of any inherited IRAs, a spouse’s IRA, or any employer retirement plans (e.g., a 401(k), 403(b), profit-sharing plan, etc.). In the case of those other accounts, each of those accounts must still take its own RMDs attributable to the value of that account directly from that account.

When The IRA Aggregation Rule Does Not Apply – 72(t) Substantially Equal Periodic Payments (SEPP)

Notwithstanding the wide scope of where the IRA aggregation rules apply, one notable situation where aggregation does not have to be considered is when an early retiree is taking early withdrawals from an IRA under the substantially equal periodic payment (SEPP) rules of IRC Section 72(t)(2)(A)(iv).

Instead, under PLR 200309028, the IRS explicitly stated that IRAs are handled on an account-by-account basis when doing substantially equal periodic payments. This is important for situations where an individual is doing 72(t) payments from one IRA, and then wants to take additional distributions, or begin new 72(t) payments from an additional IRA; if the accounts were aggregated, changes to the second account could be construed as a modification to the first, triggering retroactive penalties as the substantially equal periodic payments are disqualified. Instead though, because the IRA aggregation rule does not apply, each account is treated separately to determine the appropriate amount of distributions under 72(t), and changes to distributions from another account do not impact (or constitute a modification to) ongoing withdrawals from a current account engaged in SEPPs.

On the other hand, it’s worth noting that while IRA accounts are not aggregated together in determining the required amount for substantially equal periodic payments, or whether withdrawals from other accounts constitute a modification to the original 72(t) payments, the IRA aggregation rule would still apply in determining the tax consequences of those distributions. In other words, if any of the IRAs have after-tax contributions, even the ongoing 72(t) substantially equal periodic payments will be subject to the pro-rata rule on an aggregated basis, even though the calculation of the 72(t) payments continues to be done on an account-by-account basis!

Example 4. Gerald is a 56-year-old with two IRAs, the first worth $400,000 (all pre-tax), and the second worth $11,500 that includes $10,000 of non-deductible IRA contributions made in recent years. Gerald is currently taking $15,000/year of distributions from his first ($400,000) IRA, using the 72(t) substantially equal periodic payments exception to avoid an early withdrawal penalty (which would otherwise apply, since he is under the age of 59 ½). While for the purposes of the 72(t) the $400,000 IRA is handled separately from the second $11,500 IRA, the tax consequences of the $15,000/year distribution is still subject to the IRA aggregation rule in calculating the pro-rata allocation of after-tax funds. Thus, since $10,000 / $411,500 = 2.43% of the total accounts are after-tax, each $15,000 withdrawal will be treated as $365 of after-tax and $14,635 of pre-tax funds, even though all the 72(t) distributions are being taxed from an account that was originally funded exclusively with pre-tax dollars!

So what do you think? Have you had situations where the IRA aggregation rule created a challenge? Did you come up with a workaround? What questions do you have about the IRA aggregation rule? Leave your questions/comments below!