Executive Summary

In many large (publicly traded) businesses, it’s common to reward employees with employer stock, often granted directly in/through a profit-sharing or ESOP plan, or at least by allowing employees to purchase shares themselves inside of their 401(k) plan. The advantage of this strategy is that it helps to encourage an “ownership mentality” of the employees – who literally become (small) shareholders of the business. The disadvantage, however, is that when employer stock is purchased/owned inside of a retirement account, it is ultimately taxed as ordinary income when withdrawn (as is the case for any distribution from a retirement account), and loses the opportunity to take advantage of favorable long-term capital gains rates.

To help resolve the situation, though, the Internal Revenue Code allows employees a special election to distribute appreciated employer stock out of an employer retirement plan, and have the “Net Unrealized Appreciation” (i.e., the embedded capital gain) taxed at favorable capital gains rates outside of the account. However, to take advantage of these special NUA rules, there are specific requirements – that the stock must be distributed in-kind, as part of a lump sum distribution, after a specific triggering event.

The good news of the NUA strategy is that it creates an opportunity to convert unrealized gains from ordinary income rates into lower tax rates on long-term capital gains instead. However, the caveat is that in order to use the NUA rules, the account owner must report the cost basis of the stock immediately in income for tax purposes, and pay taxes at ordinary income rates. In addition, if the NUA stock is quickly sold, that long-term capital gains bill immediately comes due, too.

Which means in reality, the NUA rules don’t merely allow for the gains to be taxed at lower rates. They cause the gains to be taxed at lower rates immediately (at least if the stock is sold immediately), in addition to triggering ordinary income taxation of the cost basis immediately, when all of those tax liabilities might otherwise have been deferred for years or even decades. Which means deciding whether to take advantage of the NUA strategy or not is really more of a trade-off, than a guaranteed tax savings success.

As a result, the best practice for NUA distributions is to really scrutinize the cost basis of the employer stock inside the qualified plan, and if necessary cherry pick only the lowest-basis shares for the NUA distribution to ensure the most favorable tax consequences. Fortunately, the NUA rules do allow such flexibility – to take some shares in-kind, and roll over the rest – but that still means it’s necessary to actually do the analysis to determine whether or how many of the NUA-eligible shares should actually be distributed to take advantage of the strategy (or not)!

IRS Rules For Capital Gains Treatment Of Net Unrealized Appreciation (NUA)

Internal Revenue Code Section 402(e)(4) defines the rules for getting favorable tax treatment of the “Net Unrealized Appreciation” (NUA) of employer stock held in an employer retirement plan, ultimately allowing gains that occurred inside the plan to be taxed outside the plan at preferential long-term capital gains rates.

The NUA rules originated decades ago, in a world where employees of (typically large) corporations sometimes had both a pension plan and a profit-sharing or employee stock ownership plan (ESOP) that gave employees “profit-sharing" bonuses in the form of company stock.

The upside of this approach was that the corporation could make a deductible contribution to the employer retirement plan, and by contributing shares the employer could obtain that tax deduction without any cash outlay. The bad news from the employee perspective is that stock which would have been taxed favorably (at long-term capital gains rates) if it had just been purchased and grown in the hands of the employee directly, would instead be taxed as ordinary income when coming out of the plan.

Thus, as a relief provision and tax-preference for employees (to further encourage the strategy for employers), the NUA rules provided a means for employers to still obtain their favorable tax treatment, and for employees to obtain theirs as well.

Example 1. Over the years, Jenny has received annual bonuses of employer stock inside her company profit sharing plan. The total contributions have been $105,000, and thanks to the good performance of the company stock itself, the cumulative value is now $235,000. If Jenny had simply owned the stock directly, the $130,000 of cumulative gains would have been taxed at long-term capital gains rates. However, as a standard distribution from an employer retirement plan, the entire $235,000 account balance is taxable as ordinary income (regardless of the fact it happens to be a highly appreciated stock).

Under the NUA rules, though, Jenny can still be taxed on the $130,000 gain at long-term capital gains rates, even though the stock was originally purchased on her behalf inside the employer retirement plan.

Requirements To Qualify For NUA Tax Treatment

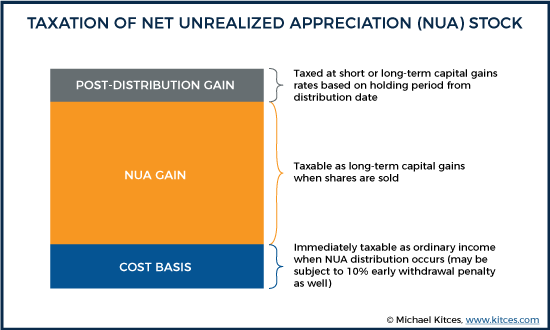

Specifically, the NUA rules under IRC Section 402(e)(4) stipulate that if employer stock in an employer retirement plan is distributed in-kind as a lump sum distribution after a triggering event, then the cost basis of the shares will be (immediately) taxable as ordinary income, but the gains on the stock – the “net unrealized appreciation” that had previously occurred inside the plan – will be taxable at long-term capital gains rates. And under IRS Notice 98-24, the net unrealized appreciation will always be taxed at long-term capital gains rates, regardless of the actual holding period of the stock inside the plan.

Notably, to meet the requirements for the NUA rules, there are three very specific requirements that must be met:

1) The employer stock must be distributed in-kind. This means it must actually be true employer stock, that is able to be transferred in-kind. Selling the stock shares, transferring cash, and repurchasing the shares outside the account doesn’t count, and TAM 200841042 similarly declared that an ESOP must actually transfer shares (or share certificates) out of the account, not merely liquidate them at termination and roll over the cash proceeds. Similarly, “phantom” stock or stock options aren't eligible for NUA tax treatment either, although an employer stock fund does qualify, as long as it holds only cash and shares of company stock and can be converted into individual shares of employer stock that can be transferred in-kind. To complete the in-kind distribution, the employer stock should be transferred directly to a taxable investment (i.e., brokerage) account.

2) The employer retirement plan must make a “lump sum distribution”. In this context, a “lump sum distribution” means the entire account balance of the employer retirement plan must be distributed in a single tax year. It’s important to recognize that this doesn’t just mean all the stock must be taken out of the plan; it means the entire account must be distributed. Although ultimately, it’s up to the plan participant to choose where the dollars end up; it is permissible to do an NUA distribution for just some of the account, and roll over the rest directly to an IRA (or even convert to a Roth). However, none of the money can stay in the plan past the end of that year.

3) The lump-sum distribution must be made after a “triggering event”. In order to be eligible for NUA treatment of an in-kind distribution of employer stock, the lump-sum distribution must be made after a triggering event. The triggering events are (a) Death, (b) Disability, (c) Separation from Service, or (d) Reaching age 59 ½. Notably, this means that an in-service distribution generally does not qualify for NUA treatment, unless it is a distribution that also happens to occur after a triggering event (e.g., upon reaching age 59 ½).

NUA Tax Treatment At Distribution And Subsequent Sale

As noted earlier, when the NUA distribution occurs, the cost basis of the shares (from inside the plan) are immediately taxable as ordinary income (and if not otherwise eligible for an exception, the 10% early withdrawal penalty may apply as well). The actual Net Unrealized Appreciation (i.e., unrealized gain above that cost basis) of the shares are taxable as long-term capital gains, but the capital gains tax event doesn’t occur until the shares are actually sold (although in many cases, due to a desire to diversify, the shares are sold as soon as they are distributed anyway). If the shares are held past the distribution, any subsequent gains will be taxed at short-term or long-term capital gains rates, based on the holding period from the distribution date until the subsequent sale. If shares are held past the distribution date and losses occur, it will simply reduce the amount of net unrealized appreciation gain reported on the sale (although if losses cause the price to fall all the way down below the original cost basis, a capital loss can be claimed).

Because there’s no particular requirement that the NUA stock be sold immediately (though it often is, for diversification purposes, but could be held for months, years, or even decades thereafter), the NUA gains may be deferred for an extended period of time. Only the original cost basis of the shares (inside the plan) is taxable at the time of distribution. Although notably, the NUA gain will eventually be taxed, as it is not eligible for a step-up in basis at death (under Revenue Ruling 75-125). On the other hand, under Treasury Regulation 1.411-8(b)(4)(ii), the NUA gain is also not subject to the 3.8% Medicare surtax on net investment income (just the standard long-term capital gains tax rates of 0%, 15%, or 20%, plus state income taxes where applicable).

A key point of the NUA rules is that while the lump sum distribution requirement necessitates that the entire account be emptied, there is no requirement that it all be distributed in a taxable event. It’s entirely permissible to take just the NUA stock as an (in-kind) distribution, and roll over the rest to an IRA.

Example 2. Continuing the prior example, Jenny decides to take advantage of the NUA rules, which includes both the $235,000 of employer stock (with a cost basis of $105,000), and also some mutual funds worth $80,000. In order to comply with the NUA rules, Jenny must distribute the entire $315,000 from the plan in a single tax year after a triggering event has occurred – which in Jenny’s case, is the year she retires (and therefore separates from service). Since Jenny only wants to do an NUA distribution of employer stock – and doesn’t want to liquidate her entire employer retirement plan in a taxable event – she can choose to take the $235,000 of employer stock in kind and roll over the other $80,000 to an IRA. In doing so, the $105,000 cost basis will be taxable immediately as ordinary income, the $130,000 of gain on the stock will be taxable at long-term capital gains rates when sold, and the $80,000 IRA rollover will simply be taxed whenever distributions are made from that IRA under the standard rules for IRA distributions.

Furthermore, it’s also permissible to “cherry pick” which shares of stock to distribute in kind, and roll over the rest (as long as the individual stock shares were earmarked for a particular employee’s account in the first place, under Treasury Regulation 1.402(a)-1(b)(2)(ii)(A)).

Example 3. Continuing the prior example, it turns out that amongst Jenny’s $235,000 of employer stock shares, the first $100,000 of shares purchased in the early years have a cost basis of only $10,000 (gain of $90,000), while the other $135,000 of shares purchased more recently and had a cost basis of $95,000 (gain of only $40,000, as the company hadn't performed as well recently). As a result, Jenny decides to do an NUA distribution for just the first $100,000 of shares with a cost basis of $10,000, and rolls over to her IRA both the other $135,000 of employer stock and the other $80,000 of IRA assets. (Because, again, everything must leave the employer retirement plan to meet the lump sum distribution requirement.)

The end result is that Jenny reports only $10,000 (cost basis of the NUA shares distributed in-kind) in ordinary income, will have a $90,000 long-term capital gain when the NUA shares are sold, and finishes with $80,000 + $135,000 = $215,000 in a rollover IRA.

Given the favorable treatment available for an NUA distribution – turning a gain that would have been taxed as ordinary income from an employer retirement plan or IRA into a long-term capital gain taxed at preferential rates – it might seem odd to ever cherry-pick taking some lower-cost-basis shares for an in-kind NUA distribution, but not the rest of the higher-cost-basis shares. However, as it turns out, the relative amount of cost basis to gain for employer stock shares inside an employer retirement plan is actually crucial to determining whether an NUA distribution is actually a winning strategy or not!

The Problem With The (High-Basis) NUA Distribution

The fundamental challenge to the NUA distribution is that it immediately triggers ordinary income taxation on the cost basis of the employer stock, which means the decision to distribute stock in-kind immediately forfeits to Uncle Sam a portion of the account that otherwise could have remained tax-deferred.

In addition, the subsequent liquidation of the employer stock itself triggers a second tax event, on the NUA gain. While the benefit of the NUA rules is that the gain is at least taxed at preferable long-term capital gains rates, it is again a tax event that, if rolled over, might not have occurred until many years (or even decades) into the future. Which means the faster the stock is sold – i.e., the more quickly the owner wants to sell and diversify – the more long-term tax-deferral that is forfeited. And of course, from that point forward, any future dividends, interest, and capital gains generated by the reinvested proceeds will also be fully taxable!

By contrast, simply rolling over the entire employer retirement plan to an IRA and diversifying is not a taxable event. And in a world where retirees often take no more than 4% to 5% of the annual account balance in distributions – and even RMDs begin at only 3.6% of the account balance at age 70 ½ – the value of the stock might have remained growing tax-deferred for, literally, decades. Or even longer if left as a stretch IRA for the next generation!

In other words, the NUA strategy is not merely an opportunity for “free” tax savings, by turning what would be an ordinary income distribution from a retirement account into capital gains treatment on the NUA gain. Instead, it’s more of a trade-off – a decision to pay taxes sooner, at a blend of ordinary income rates on the cost basis immediately and long-term capital gains on the NUA gain when liquidated, rather than pay all ordinary income at what might have been a much later point in time.

As a result, it’s especially important to look carefully at how much net unrealized appreciation there really is in the first place.

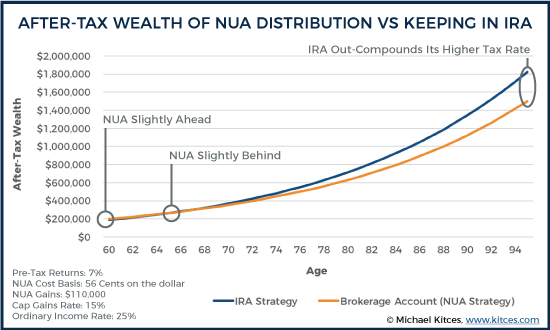

Example 4. Jeremy is 60 and has $250,000 of employer stock that was bought inside the plan for $140,000, which means it is cumulatively up about 78%, and the cost basis is effectively 56 cents on the dollar. The $110,000 gain being taxed at 15% instead of an assumed ordinary income rate of 25% in the future produces a prospective $11,000 tax savings. However, a rollover allows all $250,000 to remain invested, while an NUA distribution triggers 25% gains now on the $140,000 cost basis, plus the 15% tax liability on the $110,000 gain, for a total tax impact of $51,500. Thus, the trade-off is really $250,000 in a tax-deferred account subject to ordinary income in the future, or just $198,500 to reinvest in a taxable account (having lopped off just over 20% for immediate taxes).

Of course, if the $250,000 IRA were liquidated at ordinary income tax rates, it would be worth only $187,500, and the taxable account is still “ahead” by $11,000, thanks to the tax savings on the NUA distribution. However, until it’s actually liquidated, the $250,000 IRA can continue to grow tax-deferred, while the $198,500 has already been taxed, and going forward will continue to be annually taxable in the future!

Accordingly, we can analyze the long-term impact and after-tax value of each strategy in the above example over time. Assuming a moderate 7% growth rate and that the IRA will be taxed at 25% in the future (with RMDs beginning at age 70 ½), compared to a 5.95% after-tax growth rate in the brokerage account (assuming a 15% rate on qualified dividends and long-term capital gains), we find that it only takes about 6 years for the NUA strategy to fall slightly behind... and after several decades the NUA strategy lags dramatically!

Notably, this example “generously” assumes that the lump sum income from the NUA distribution stays in the 25% tax bracket (when in reality if all $140,000 of cost basis is taxable at once, some of it would at least bleed into the 28% bracket), and that the brokerage account has NO short-term capital gains or bonds yielding ordinary interest at higher tax rates (which would make the blended rate a bit higher than 15% and cause the NUA strategy to lag even further in the later years).

Nonetheless, as the results show, while the NUA strategy is appealing in the near term, over the long run the lost growth opportunity on the taxes paid sooner rather than later (both on the cost basis of the NUA stock, and the capital gains taxes on the actual NUA gain) is quite damaging. Even for a stock that was up 78%, the NUA distribution quickly falls behind, and dramatically so by the end. And of course, if there was actually money left over at the end, that IRA could have been stretched even further to the next generation (allowing the compounding to continue even further), or alternatively could have been opportunistically turned into a Roth IRA along the way via partial Roth conversions (which is impossible once the NUA stock is already fully distributed).

Finding The Balancing Point On An NUA Distribution

For very long-term employees, the reality is that employer stock shares might not “just” be up 78% (as was the case in Example 4 above), but several hundred percent, or even 1,000%.

For instance, a long-term employee at IBM for the past 40 years would have split-adjusted shares with a cost basis of just 10 cents on the dollar (a split-adjusted share price of about $17/share in 1977, versus over $170/share today), for a gain of about 900%. And an investor at Altria (formerly known as Phillip Morris, and now also the owner of Kraft and Nabisco Foods) since 1977 has a split-adjusted cost basis of about $0.30, which means with the stock now around $71/share, it is up a more than 23,500% in 40 years. Or viewed another way, the cost basis is less than half a penny per $1 of share price!

In the case of Altria, this means that even $1,000,000 of stock (at current value) eligible for NUA would face ordinary income of only about $4,000 (and a tax bill of just $1,000 at a 25% tax rate), with the entire $996,000 remainder taxed at long-term capital gains rates (likely at a blended rate of 15% and 20% given a gain of that size). And less of a tax hit upon NUA liquidation means more dollars that can be reinvested, which in turn means it would take longer for a mere IRA rollover to be more appealing.

In other words, the size of the cost basis (relative to the total value of the stock) is a key determining in the NUA trade-off, as a lower cost basis means a lower ordinary income tax hit, which in turn reduces the overall upfront tax impact, and makes the NUA strategy more appealing.

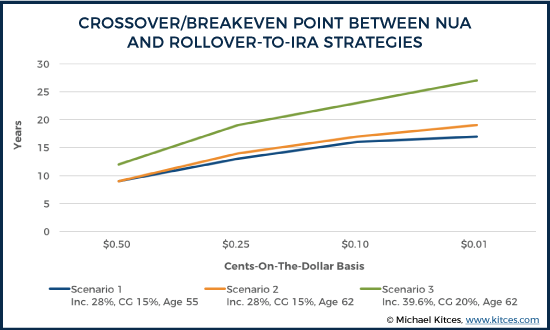

For instance, the chart below examines how long it takes for the IRA rollover (and its tax-deferred compounding growth) to overtake the NUA distribution, at various levels of appreciation and assuming different tax/age scenarios. Notably, amongst the tax and age scenarios considered, the crossover point between NUA and rollover-to-IRA strategies with a cost basis of 50 cents on the dollar ranged from 9 to 12 years (depending on assumptions), while at "just" 25 cents on the dollar and down to only 1 cent on the dollar, the crossover point ranged from 13 to 19 years and 17 to 27 years, respectively.

As the results reveal, the NUA distribution really does work better as the cost basis of the NUA distribution decreases (with the breakeven point approaching or reaching past normal life expectancy in the lower cost basis scenarios). NUA strategies are also more appealing as a retiree's age increases, which both reduces the deferral time available until RMDs need to be taken (as RMDs reduce the value of the rollover), and reduces the likelihood of living long enough for the IRA to overtake the NUA distribution (i.e., the time horizon is more limited, where the more immediate tax savings of the NUA rules are favorable).

Of course, it’s still important to recognize that for especially large NUA positions, the gain may be so large that the capital gains rate is higher than 15% (e.g., if some of the gain pops up into the 20% bracket), which makes the NUA less valuable. Similarly, even with “small” cost basis, a very sizable stock position could drive up the ordinary income tax rate on the cost basis. For instance, even at 10 cents on the dollar of cost basis, a $1,000,000 employer stock position would generate $100,000 of ordinary income, which is potentially enough to drive a married couple from the 15% bracket to 28%, or from the 25% tax bracket all the way to the lower end of the 33% tax bracket.

And it’s also notable that because the trade-off is the upfront tax hit (at lower rates) in exchange for tax deferral, the higher the overall tax impact up front, the harder it is to recover. And this can include the impact of state taxes, which apply equally to ordinary income AND capital gains. In fact, even though the IRA is ultimately taxed at higher rates later, the higher upfront tax burden can still be enough to bring the breakeven point even closer (where it's better to simply roll over to the IRA and skip the NUA strategy).

By contrast, though, if the individual can actually hold the stock, rather than sell it – for instance, if there’s not a pressing need to liquidate and diversify after the NUA distribution – the decision to hold onto the stock defers the NUA capital gain, and can greatly improve the long-term outcome. Though as a study by David Blanchett from Morningstar found, whether the decision to hold is appealing (or not) for an extended period of time should still be driven primarily by the investment risk and return of the employer stock compared to a diversified portfolio, rather than the tax deferral alone.

Best Practices In NUA Distributions

Fortunately, the reality is that the NUA distribution strategy is a choice, not an ‘obligation’ or a requirement. In other words, the investor doesn’t have to do it, and even if he/she does, the NUA strategy doesn’t have to be executed with all of the stock. As long as there are records to identify the share lots in the first place (and those lots were assigned to an individual employee’s account), it’s permissible to cherry pick them, whether from a profit-sharing plan or ESOP. Which means it often will be worthwhile to delve through the historical purchase transactions, just to identify which lot(s) may be appealing for NUA.

One straightforward approach is simply to set a cost basis threshold – for instance, don’t do NUA for any stock with basis more than 20 cents on the dollar. So if the company currently trades for $80/share, only do NUA on the shares with cost basis of $16 or less, and roll over the remaining shares to an IRA (along with anything else in the employer retirement plan, per the lump sum distribution requirement). And for those who want to liquidate the stock after distribution, but spread out the tax impact, it may be feasible to do the NUA distribution (triggering taxes on the cost basis) late in one tax year, and then complete the subsequent sale (with long-term capital gains rates on the NUA gain) early in the subsequent tax year (and even hedge the risk during the intervening period with a short-term put option). And notably, the NUA gain may even be eligible for the 0% Federal rate on long-term capital gains, especially if there is little other ordinary income to fill the bottom tax brackets.

However, it is still important to ensure full compliance with the rules. Which means don’t forget that the NUA distribution has to be a full lump sum distribution in that year, where the end-of-year account balance must read zero! The retiree can roll what he/she doesn’t want to NUA distribute, but it all must leave the account! In addition, an NUA distribution can only occur after a triggering event, which means it’s necessary to wait until a triggering event occurs, and it’s important that when any distribution occurs after the triggering event, that must be the year for the NUA distribution (or the opportunity is lost until the next triggering event).

Example 5. Sheila retired from her employer at age 56 in early 2016, after spending 30 years with the company. She has a 401(k) plan with profit-sharing with a total account balance of $1.2M, including $400,000 of employer stock with a cost basis of $45,000. During the summer of 2016 after she retired, Sheila took a $10,000 distribution for an around-the-world trip to celebrate her retirement, which she was able to do without any early withdrawal penalties thanks to the rule allowing retirees who separate from service after age 55 to take a distribution from their employer retirement plan. Now, in early 2017, she sits down with a financial advisor to plan her retirement, and explore the NUA distribution strategy for the $400,000 of employer stock.

However, Sheila’s retirement was her triggering event, and her distribution in the summer of 2016 meant that was her first distribution year after a triggering event. And she did not do a lump sum distribution (or any in-kind distribution of employer stock) that year. As a result, any attempt to do an NUA distribution in 2017 will not qualify, as it will no longer be a lump sum distribution after a triggering event (since a non-lump-sum distribution already occurred after the triggering event). Thus, Sheila will not be eligible for an NUA distribution.

Fortunately, though, because the triggering events include death, disability, separation from service, and reaching age 59 ½, Sheila will have a second chance for an NUA distribution in 2019, once she actually turns 59 ½, and can take advantage of the NUA rules then. As long as she makes certain that once she does take a distribution after age 59 ½, that is the year she does a full lump sum distribution, and takes the employer stock in kind!

Notably, if Sheila had separated from service after age 59 ½ – which means the separation from service and age 59 ½ triggering events would have passed, and the disability trigger is a moot point once retired – then the NUA strategy would be totally lost to her, and the only opportunity would be for her heirs to do an NUA distribution from the inherited employer retirement plan (as death is a triggering event, too!), though that would require her to keep the employer retirement plan, and hold the stock, without using it, until the day she dies (which may not be feasible due to both investment risk, and her retirement income needs!).

It’s also notable that the NUA strategy may be appealing for those who separate from service prior to age 59 ½, even if they’re not eligible for the age-55 exception to the early withdrawal penalty. For instance, a 52-year-old who separates from service can still do an NUA distribution. The cost basis of the shares will be subject to ordinary income taxes, plus the 10% early withdrawal penalty. However, if the cost basis is low enough, the penalty may be so small that the NUA strategy is still worthwhile for the overall tax savings. And once the shares are distributed from the account, they're freely available to use - unlike with an IRA rollover, where all of the retirement account would still face the early withdrawal penalty (with only more limited exceptions, such as 72(t) substantially equal periodic payments).

Example 6. Charlie retired from his company at age 52, with an ESOP holding nearly $650,000 of employer stock, which had an internal cost basis of just $45,000. Charlie decides to do an NUA distribution of his ESOP shares, even though the distribution will subject him to the early withdrawal penalty, because he doesn't want to wait until age 59 1/2 to diversify his concentrated stock position. However, since the cost basis is only $45,000, the early withdrawal penalty will only be 10% of that amount, or $4,500, which is a mere 0.7% of the value of the stock - a "cost" that Charlie decides is quite worthwhile, in order to diversify and still otherwise take advantage of the NUA rules! And going forward, Charlie has access to the entire $650,000 of employer stock, without needing to worry about further early withdrawal penalties!

On the other hand, it’s also important to recognize that it is an option to do the NUA distribution and keep the employer stock. Doing so allows the NUA gain to be deferred, and if the cost basis is low enough, the immediate tax impact (on just the cost basis) may be small or negligible. Clearly, holding a concentrated stock position just to defer taxes can be risky from an investment perspective, and also may not be feasible simply due to a need to use the asset for retirement income purposes. Nonetheless, in scenarios where the employer stock actually is a small portion of the retiree’s total net worth, or where the risk of the stock can be reasonably hedged (e.g., with put options), continuing to hold the stock may be both economically feasible and still reasonable from an investment perspective (as a modest portion of the overall portfolio), while also allowing the retiree to enjoy the tax benefits of the NUA strategy (by still enjoying the preferential capital gains tax rate on the NUA gain in the future, but being able to defer it to the future!). In addition, stock held in a brokerage account can also be margined (unlike in an IRA, which cannot be loaned against), providing a securities-based lending option for further liquidity (without actually selling the stock). Conversely, for those who “need” to diversify, don't need the liquidity outside of a retirement account, and truly don’t want to absorb the immediate tax impact, it’s always an option to simply roll over the employer stock to an IRA, and sell and diversify there without any immediate tax consequences while continuing to enjoy subsequent tax-deferred growth.

Overall, though, one of the biggest caveats of the NUA strategy is simply to recognize that cost basis inside an employer retirement plan actually matters. Given that employer retirement plans – and rollover IRAs – are simply taxable on all distributions as ordinary income, “basis” of stock inside the accounts are normally ignored. But in the case of a potential NUA distribution in the future, it matters, and can have substantial consequences for those who don’t bear it in mind while managing their employer retirement plan.

Example 7. Johnny had worked at his company for almost 40 years, and collectively had $900,000 of employer stock with an original cost basis of just $120,000. In the financial crisis, though, the price of the company crashed by 40%, and rumors abounded that the company could even go under, despite its decades of success. To avoid the risk, Johnny had sold the stock back then at $550,000. Once the rumors passed, he had bought back in at $600,000, only causing “limited” damage due to bad market timing (and allowing his shares to recover to their current $900,000 value).

However, because Johnny sold the stock inside the plan and bought it back, the transaction reset his cost basis on all the shares to $600,000, the value on the day he re-purchased. As a result, his “old” cost basis of $120,000 was completely overwritten, eliminating the value and potential benefit of the NUA strategy now that he is preparing for retirement!

Ultimately, it remains to be seen how long the NUA strategy will remain available. President Obama’s budget proposals in 2015 and 2016 characterized it as a “tax loophole” to be closed (though it would have grandfathered anyone who was already age 50 at the time), although President Trump’s tax plans still haven’t taken a position either way.

Nonetheless, as long as it’s still around, it does remain an appealing strategy. Though still, it’s important not to be overly exuberant about pursuing the NUA rules, as there’s still a real trade-off to consider, given the upfront tax impact versus being able to defer taxes until later, tempered by how quickly the investor does (or doesn’t) want to keep the stock in the first place!

So what do you think? Are the downsides of NUA distribution strategies often overlooked? How do you help clients evaluate NUA strategies? Are NUA strategies a "tax loophole" that will be closed in the future? Please share your thoughts in the comments below!

Michael, thanks for the clear explanation and helpful examples. I have a few questions: Would the NUA option be more attractive if someone plans to make annual charitable contributions throughout their retirement years? I’m thinking it might make sense to take an NUA-eligible distribution and then donate a portion of the shares to charity each year, with the assumption that the charity would get the full value of the shares at the time they were donated and donor wouldn’t owe any capital gains tax on them.

What about another possibility: Could the entire NUA-eligible distribution be donated to a donor advised fund (after the shares were placed in a brokerage account) without incurring any capital gains tax?

Thanks!

Don,

Yes, the NUA shares can be placed into a Donor Advised Fund. It is a great solution to diversify the clients portfolio and meeting their charitable gifting needs.

Having used the NUA rules in 2012 for myself, this is exactly what my husband and I did.

We also gifted some shares to a sister who needed some help. My basis carried over to her, but she was in a very low tax bracket so she only owed a bit of state income taxes on the sale.

The only caveat is that you should wait till at least one year after NUA. In the first year of NUA the DAF contribution will be considered short term. For example if 42000 was sent to DAF and the cost basis is 7 to 1 only 6000 will be counted towards charitable deduction.

If someone asked me this I would ask them to consider a QCD Qualified Charitable Distribution, which also satisfies your required minimum distribution RMD. Perhaps its feasible to pay tax on the NUA and subsequently donate the appreciated shares in-kind taking a schedule A charitable deduction. A financial analysis should be done to determine the tax efficiency versus a QCD.

Michael,

Worth mentioning that if the client is a qualified purchaser they may be able to do an exchange fund after the NUA.

Having placed several clients’ low basis shares, representing millions of market value, i have yet to find an exchange fund sponsor accept shares acquired through a distribution from a qualified plan under an NUA election.

Micheal,

I wanted to note one thing about ‘Cherry Picking’ the stock lots. This feature is plan specific and many companies do not allow participants to pick lots. Instead most plans use the average cost of the shares in the 401k account.

With that being said I believe confirming if a participant is able to ‘Cherry Pick’ is an absolute must before starting any NUA analysis for clients.

Check the Frank Duke method discussion with @JimLeBlond, above, and my response.

Thanks for the article. What are your thoughts on the “Frank Duke Method” of NUA distributions? (Frank Duke was a former P&G exec that implemented an approach whereby at the end of the day through a series of transactions (exchanges from Preferred Stock to Common Stock etc.) a high basis is allocated to stock rolled out to the employee and the remaining shares without basis are rolled into an IRA.)

My thought on the Frank Duke method was it’s brilliant. Essentially it involves changing the accounting method of the NUA stock from, say for example, “FIFO” First In First Out, to either specific identification, or weighted average. So by changing the accounting method, you can effectively change the basis of the individual shares of stock. In other words, if you have a basket of stock that was purchased during rising stock prices, the stock purchased later has a higher basis. By changing the accounting method, you can say that the first share sold is the low basis stock. And obviously, the stock is then distributed in part to the taxable account and part to the IRA, with different basis. So this works when there are baskets of stock and multiple purchase prices. Keep the high basis stock in the IRA because you’re not getting much benefit from the NUA. Roll out the low basis stock. So it’s obviously brilliant. I have helped clients do this in the context of charitable giving, so it’s certainly possible with the NUA. I would recommend hiring tax counsel though.

NUA is a tricky issue: As financial planners we advise our clients to diversify, and generally NUA flies in the face of that because the company stock ends up as a overly large portion of the portfolio. I had a real life example of this when a client of mine was laid off in the late 90’s with a boatload of AOL stock. We sold a lot of it to diversify. It was clearly the right move. My client thought I made a great stock call on AOL stock, but I was merely being prudent. Of course it could have gone the other way, and it could make sense implement NUA and use a trail stop of 10% (or whatever the client is comfortable with) to protect against a drop.

Michael, these types of tax management strategies are what we are turning our focus to more and more, not just to demonstrate the value of financial planning (as opposed to investment management), but also facing the reality of the unfunded liabilities our country faces in the future. I would be interested to see an article in the future on Indexed Universal Life insurance.

A sincere thank you for huge contribution to making improving our profession.

Hi Michael, and thanks for the NUA discussion. I agree that in my experience, one near normal retirement age, a stock basis greater than about 20% means it generally is not worth the cost of the tax in the rollover year.

Question: if this is a private company (and about 90% of ESOPs are private companies), how does the in-kind stock transfer work? Will a brokerage accept private stock? And wouldn’t there have to be a repurchase agreement with the company on these shares?

Technically speaking, most custodians may not accept private stock unless conditions are met but you could ask them. You may not be required to distribute the NUA stock to an account per se, you could simply hold them in bearer form for example. As far as a repurchase agreement, that’s not a requirement that I am aware of. Please seek tax counsel and speak with the ESOP trustee. It is the Trustee who could provide the stock basis and report the NUA on a 1099-R to the IRS.

There’s no NUA-driven agreement for a repurchase agreement, but privately-held stock in general often has limitations in the shareholder agreement that prevent it from being held by ‘outsiders’. So the shareholder agreement may have to be revised just to permit the stock to be held in a brokerage account outside the ESOP, and the repurchase agreement (if there is one) may have to be adjusted to allow the stock to get to the brokerage account long enough for the repurchase agreement to actually be exercised outside the ESOP.

In essence, it’s not that the NUA rules limit its use with ESOPs. It’s that ESOPs (and closely held businesses in general) often have restrictive shareholder provisions (to protect the owners of the closely held business) that make it difficult to execute the mechanics of an NUA transaction. The good news is that because it’s a closely held business and the owners are often involved, there may be a willingness and opportunity to amend the shareholder agreement to make the NUA transaction feasible. 🙂

– Michael

Michael – any thoughts on how the company must calculate basis? Someone below mentioned using average basis, but is it really as simple as the stock purchase price? I thought I had read a while back that employers used a formula of some kind.

The plan administrator of the 401(k) or ESOP or LESOP will calculate your basis for you. If it does not then it is possible to recalculate, and I’ve done it by using prior statements or pay stubs. But it takes a long time because I had to go through every statement over the course of many years.

Do you know if you can allocate after-tax money directly to the cost basis? For example, if you had a $2mil IRA with $1mil of NUA stock (cost basis $200k). If there was $100k of after-tax dollars, could you roll $1mil to an IRA, do a transfer of stock to a taxable account for the remaining $1mil and only pay tax on $100k ($200k less $100k basis)?

Thanks

Jeremy

You have to be careful with this. If you are still working at the company, doing an in-service distribution could affect your ability to use NUA. You must check the 401k Plan Document to see what’s allowed. Furthermore, if you have after tax dollars you would likely be better off rolling the $100K over to a Roth iRA. After all, the whole goal of NUA is tax savings, so it doesn’t get any better than a tax free Roth IRA.

Yes, I believe this is an option if you qualify. Otherwise you could go with rolling it to a Roth if that benefits you. If not, then use the money to pay the NUA bill. Brilliant. Seek tax counsel to ensure you qualify.

Michael,

Very informative article. However, there is a step-up on death for any appreciation that occurs after the date of NUA. Shouldn’t that have been calculated into some of your analysis?

Usually people separate in the beginning of their retirement, but it is possible to separate for health reasons. In my mind, the step-up in basis is a bonus to the NUA, as otherwise an heir would inherit an IRA subject to ordinary tax rates. So if the NUA was viable to begin with, then perhaps to the extent the NUA is not subject to tax, it’s truly a tax-free gift.

Can you sell high cost basis shares in the 401k, diversify those proceeds and then roll out the remaining low cost basis shares into a taxable account and roll over the remainder to an IRA?

If your 401k plan allows cherry picking, then just do as Michael said and execute NUA on low cost basis shares and rollover everything else to the IRA. If your plan doesn’t allow this, then I doubt they will allow you to sell just the high cost basis shares within the 401k. But you should contact the 401k company to find out for sure.

Yes, generally speaking, one could liquidate shares prior to the NUA rollover, or one could simply roll-over the account to an IRA and do it there. I suggest you speak to a tax advisor.

Fun topic Michael, thank you. I have a question related to RMDs. It is my understanding that you can use the market value of the stock to satisfy the RMD, but still only have the cost basis as the taxable amount of the distribution. So, $2 million 401k, around $73,000 RMD. Company stock market value in 401, $65,000, cost basis $10,000. I do NUA plus $8,000 and my RMD is satisfied, but the taxable amount comes to $18,000. Is this correct?

You are getting into a level of genius that warrants applause. If this strategy works, you effectively satisfy a required minimum distribution requirement, while deferring the recognition of income, and with the NUA, you are also deferring and reducing your tax rates. Bravo.

Yes, you are correct. The IRS is clear that NUA on employer securities is a distribution amount that a plan participant may count toward satisfying his or her RMD for the year. Of course your would have roll over the remainder of your 401K to an IRA.

In addition to my other contributions below, I wanted to add one VERY IMPORTANT point to paragraph (2) The Employer retirement plan must make a ‘lump sum distribution’ in a single tax year…a plan participant may NOT have any other distributions from the plan during that year or it would likely disqualify the NUA special treatment. Traps: a partial distribution earlier in the year, or even a loan. This would not be a non-lump sum distribution during a single tax year, even if the NUA lump sum distribution was attempted later in the year. Be wary of this point and seek tax advice immediately.

Still confused. I have to start taking RMD this year and am planning to rollover my 401K into an IRA. Say I rollover everything in my 401K to an IRA except for the company stock which I transfer in kind to a brokerage account. I must pay ordinary income tax on the RMD AND on the cost basis of the company stock. Every year going forward, I must pay ordinary tax on the RMD and any time I sell some of that company stock, I would have to pay long-term capital gains tax on that sale. Which sounds like double taxation to me. The longer I hold that company stock, or the more slowly I sell shares to limit the tax consequences, the more I’m locked into a stock position that may not be advantageous. If I sell the stock all at once outside the IRA, there’s a huge capital tax gains on top of the RMD. I just don’t see the advantage.

Once your company stock comes out of the 401(k) and into a brokerage account, it’s already distributed. There’s no more RMD applicable to the company stock. You can’t be forced to distribute something that’s already fully distributed.

The only part that would remain subject to an RMD is whatever you DON’T take out as company stock, and roll over to an IRA. So the IRA would simply continue to be subject to RMDs as IRAs are.

Nothing is double taxed. Company stock is taxed once (ordinary income on basis, capital gains on the rest). IRA distributions are taxed once (when taken, as distributions and/or RMDs).

– Michael

But the stock transfer does not count as an RMD. I still have to take the RMD, pay taxes on it AND pay taxes on the cost basis of the stock. Going forward, every year I must pay taxes on the RMD and, if I sell any of the stock, taxes on the capital gains.

If I convert the entire 401K, including stock, into the IRA, I pay taxes on the RMD every year. But there are no taxes on capital gains because there is no stock in a brokerage account.

In other words, in Case I, I am paying taxes on both the RMD and the stock and every time I sell the stock I pay taxes on it.

In Case 2, I simply pay taxes on the RMD.

“Double taxation” is perhaps the wrong way to describe this. What I see is that I will end up paying more taxes by using the NUA as well as put myself at a long-term risk from ownership of the company stock which is too high for my comfort.

Selling the stock all at once in the brokerage account, as many sites suggest, would result in a huge tax bill. If I needed the cash, it might make sense, or if I were 40 years old, the NUA might make sense. But I don’t see how it makes sense for somebody who is required by law to take an annual RMD when they do they 401K->IRA rollover.

I’m truly not trying to be argumentative for the sake of argument. I’ve got to decide what to do in the next month, and I need to understand the NUA to make the right decision.

Yes, the difference is that every dollar that ever comes out of the IRA will be taxed at ordinary income rates up to 39.6%.

The NUA stock will be taxed at a maximum rate of 20%.

The bad news of NUA is that stock gains will be taxable. The good news is that it may be taxed at half the rate.

The whole point of the NUA strategy is the ability to get long-term capital gains rates instead of paying ordinary income rates on all the gains (which is what happens if you simply take them out of the IRA directly in the future).

There’s nothing about NUA that avoids or eliminates taxes. You’ll always have to pay them (whether on the stock as capital gains, or from the IRA as a distribution). But NUA allows for the potential for a more favorable (lower) long-term capital gains tax RATE on that NUA gain.

– Michael

The NUA would count as an MRD.

You may not be grasping the concept. An example to help. If the FMV of the stock is $20–assume you pay as much as 39.6%, or ($8) tax on every share if you do not do an NUA.

If your basis in the stock is $12, you pay 39.6%, or ($4.80) on the basis of $12, and pay 0%, 15%, or 20% or ($0, $1.20, $1.60) tax, on the NUA part of $8. So would you rather pay tax of ($8) or ($5.40) per share of tax in this scenario? Obviously you’d like to pay less so you would choose an NUA. Now multiply that by 100 shares, 1,000 shares, 10,000 shares. You save $2 bucks/share in taxes x 10,000=that’s $20,000!

To determine whether or not to sell the stock, that decision should be made jointly with the financial adviser.

Please immediately seek tax counsel as if your financial future depended on it! Good luck and great questions.

A Minimum Required Distribution (MRD) often called a Required Minimum Distribution or RMD is a mandatory distribution from an IRA at 70 1/2 years of age. If you are eligible for the NUA and it makes financial sense and tax sense, and you’ve had tax counsel model your tax exposure and discussed it with your family, then the distribution of the NUA stock counts as an MRD or RMD at its fair market value, FMV, except you only have to pay tax on the basis of the NUA stock, not its FMV. If the FMV of the NUA stock is insufficient to satisfy your MRD for the year (which by the way you must have one heck of a large retirement account like Mitt Romney’s $100,000,000.00 IRA) then you could satisfy the balance of the MRD by taking a taxable distribution from the newly rolled-over IRA. You would pay ordinary tax. The alternative is not to do an NUA and roll the whole 401k to an IRA. In this case you would pay ordinary income on the entire MRD. So isn’t it clear how you save money with the NUA? You pay ordinary income only on the basis and pay long term capital gains rates, 0% 15% or 20% on the NUA and avoid the 3.8% NIIT if applicable to you. So what happens is if the basis of the stock is say $12 and the FMV is $20, then the NUA is the difference or $8, which is taxed at long term capital gains not ordinary tax rates. The taxes on the NUA are simply deferred until you sell the stock. Please seek tax counsel so you can have your personal situation explained to you. I usually prepare a financial model to show you how much tax you would pay in both scenarios so you understand. As such I recommend you do this.

In regard to the “entire balance in a single tax year lump sum” requirement, would an in-service distribution to an IRA at age 59-1/2 affect the ability to use NUA treatment of company stock at age 65 retirement?

Hi, if you qualify and make the distribution, bear in mind you need to make a lump sum distribution. So you would be effectively liquidating your 401k. Thus, I had a client go back to the same firm after retiring. The question raised was whether he would be eligible for the NUA a second time and I believe I opined yes, but I’d recommend retaining tax counsel. In other words, I see no reason why not but I’d have to see the mechanics of it, because right now it’s a pure hypothetical exam question. The warning I routinely give is — it’s not only whether you qualify for the NUA, it’s really whether you have something that disqualifies you. Good luck.

Michael, well written and very useful. If the company is being acquired in a cash deal, would that qualify as a triggering event, AND, should the lump sum distribution occur before the acquisition? In this case, separation of service occurred in 2016, participant is age 55, and has kept the 401k with former employer, which is now being acquired.

Thank you for being such a valuable resource.

Hi, let me preface that tax counsel should be sought but generally: The triggering events are (a) Death, (b) Disability, (c) Separation from Service, or (d) Reaching age 59 ½. Notably, this means that an in-service distribution generally does not qualify for NUA treatment, unless it is a distribution that also happens to occur after a triggering event (e.g., upon reaching age 59 ½). So perhaps the acquisition is not a triggering event, generally speaking. I am not aware of any authority for that. So if the separation occurred in 2016, the person would have until the end of the subsequent tax year 2017 to make the NUA distribution. The problem I’ve encountered with clients like this is they’ve taken a distribution in the current year, which could make them ineligible. If the client made a distribution in the prior year, they might still be eligible, as long as no distribution in the current year. Loans also make them ineligible. So the caution and big warning is make sure you seek tax counsel to determine whether the client is eligible. Ive had scenarios where we had to unwind an NUA, which I know how to do, but that’s beyond the scope of the article.

Thank you Charles. Sadly, the company being acquired hasn’t offered any tax guidance to employees/former employees other than seek tax guidance.

I have 4 questions. please help me understand?

1) What happens to NUA if stocks are still in 401K plan and the company is acquired by another company with 50% cash and 50% stock deal? Does opportunity for NUA goes away?

It depends. If you make a distribution before the transaction, then perhaps the NUA can be completed. The other consideration is whether the new stock is employer stock? Is the employee employed by this new company? If you do not make the distribution, then the question is whether you still qualify for the NUA and if it is employer stock.

(2) How cost basis and taxes would be reported if after NUA transaction(in-kind transfer), the current stock is acquired by 50%cash and 50% stock deal with a new company. Do you loose the long term cap g/l tax advantage? The custodian tracks the basis in the 401(k). But it can be re-calculated if needed and I have done it.

(3) After the NUA transaction, isn’t your cost basis for the transferred stocks in brokerage account = o since you have already paid ordinary taxes on the cost basis?

After the NUA, the cost basis of the stock is the same as the cost basis of the stock held in the 401(k). The cost basis does not change because of the distribution.

(4) I don’t understand the crossover/breakeven point graph. Why rollover IRA (with cost basis of say 10% and 62 years of age employee) ever overtake the NUA distribution assuming same investment assumptions.

This is because of appreciation of the stock, and the avoidance of capital gains taxes in the 401(k) and IRA accounts. They are tax deferred and do not pay capital gains taxes.

I have 4 questions. please help me understand?

(1) What happens to NUA if stocks are still in 401K plan and the company is acquired by another company with 50% cash and 50% stock deal? Does opportunity for NUA goes away?

(2) How cost basis and taxes would be reported if after NUA transaction(in-kind transfer), the current stock is acquired by 50%cash and 50% stock deal with a new company. Do you loose the long term cap g/l tax advantage?

(3) After the NUA transaction, isn’t you cost basis for the transferred stocks in brokerage account = o since you have already paid ordinary taxes on the cost basis?

(4) I don’t understand the crossover/breakeven point graph. Why rollover IRA (with cost basis of say 10% and 62 years of age employee) ever overtake the NUA distribution assuming same investment assumptions.

•Reply•Share ›

•Reply•Share ›

(1) This is an interesting scenario. First, the client must have a triggering event. If you have a triggering event, and employer stock held in a qualified retirement account, such as a 401(k), then upon a lump sum distribution, the Net Unrealized Appreciation (NUA) opportunity may be available. You could check with your 401(k) custodian to see if the opportunity is available. And then you would be directed to retain tax counsel to determine whether it makes sense. So I ultimately believe it could be available, just with the new stock. You also could acquire employer stock in your 401(k) and just buy it with the other 50% cash. But you should check with your financial adviser to see if that makes sense for your portfolio. If the stock isn’t going to appreciate, then it may not be wise. So yes, its possible.

(2) By rule, upon a triggering event, all NUA stock is automatically treated as Long Term Capital Gain upon lump sum distribution. Any SUBSEQUENT gains (after distribution) are treated as short term unless held for a year. Theoretically you could acquire stock in a 401(k) the day before the lump sum distribution. At that point the NUA would not make much sense, however, because the appreciation would not be that high and subsequently it might not make financial tax sense to do such a move unless there was an IPO and the stock appreciated wildly for example.

(3) So basically, when you elect a lump sum distribution, the NUA stock is put into a standard brokerage account (taxable account) and the 401(k) is rolled to an IRA. The 401(k) plan administrator is supposed to calculate your basis (or acquisition costs) of the NUA stock and the NUA. You pay ordinary income tax on the basis of the NUA stock and that becomes your basis–you actually keep the same basis as the acquisition cost in the 401(k). So its as if you just bought the stock from your 401(k) except you only pay taxes because you already paid for the stock. The appreciation over all that time you held it is eligible for long term capital gains treatment, which are 0%, 15% or 20% depending upon your AGI. People erroneously think their capital gains rate, which there’s three, is based solely on sales of capital assets, when its not, it includes other income. Furthermore, the gains from NUA stock are not subject to the Net Investment Income Tax or NIIT of 3.8%, if applicable. Any subsequent appreciation of the stock after you transfer it to the taxable account is a short term capital gain.

(4) The chart attempts to demonstrate how long it would take to keep the money held in the IRA for the tax rates to be equal to the NUA strategy. A breakeven means you could do either strategy and you would pay the same tax either way. It wouldn’t matter what you chose as far as a tax perspective only was concerned. You would then make the decision to do an NUA based upon other factors only like which was easier to do or what your financial adviser said–hold it, sell it. In other words, the chart assumes the NUA gets 15% tax bracket, and the ordinary income gets 28% to 39.6%. Thus, if you consider compounded growth, in many cases the NUA stock would have to stay in the IRA for another 10 years minimum assuming the basis of the NUA stock is at least $0.50 to its FMV $1.00. The NUA stock pays ordinary taxes up front and lower capital gains rate on the appreciation, while the IRA is completely tax deferred. So that’s what he’s showing. In essence, the lower the basis relative to the fair market value FMV, the better the NUA opportunity. But is is worth speaking to tax counsel to consider your options and have tax counsel prepare a chart that you can easily understand and sleep on it and discuss it with your family and other advisers. So in your case, please seek tax counsel. All custodians require it. Good luck.

Is there a time limit for taking action following the Triggering Event? Say you work for an employer, and contribute to the 401k, in which about 25% of each contribution buys company stock units. One day you leave the company, but decide not to rollover the old company 401k into your new employer’s plan. You just kind of leave it alone and forget about it; no new contributions go in and it becomes just a passive portfolio. Then say 4 years later, that former employer stock literally triples, and produces a nice gain in that old 401k. At this point, a new employer requires you to rollover any old 401k’s you have into their plan.

So does the Separation of Service triggering event 4 years prior still apply, or is it too late to take advantage of the NUA strategy?

You would need to take advantage of the NUA lump sum distribution within 1 year following the year of the triggering event. It does not necessarily mean that there may be another triggering event. So please contact tax counsel to discuss this, but generally speaking, I advise my clients to consider this strategy as soon as possible to avoid this possible scenario where the NUA COULD be lost. Seek counsel.

Thank you Charles

What about if I die before I sell my NUA stock and my son inherits the NUA stocks. Will the appreciation (as of the date of my death) in excess of NUA escape taxation? Will the stock receive step-up in basis?

Adas,

As noted in the article, NUA is not eligible for step-up in basis, under Revenue Ruling 75-125.

– Michael

I have done a lot of reading on this, and it still isn’t perfectly clear with regards to the step up in basis. However, as noted in my reading this best explains how the step-up in basis rules do not apply to property that constitutes a right to receive an item of income in respect of a decedent, and net unrealized appreciation constitutes a right to receive income in respect of a decedent. Thus, upon the death of the owner of the appreciated employer securities, there is no step-up in basis and there will be a realization of capital gain upon the subsequent sale of the employer securities by the estate or a beneficiary of the estate. I.R.C. §§691, 1014; Rev. Rul. 75-125.

My 62 year old spouse worked for the same company for 36 years, in 2014 the company released several hundred people during a reorganization, my spouse retired. The 401k is loaded with mostly company stock. The company split into two companies a little over a year prior to retirement, issuing stock in the company being split off on a one for one basis. Now the 401k has two company stocks, of which both were derived from employment. The two stocks have a relatively low cost basis of 29%, and 14% of market value. This cost basis is provided as the basis of the shares by the 401k administrator. The 401k hasn’t been touched since retirement, or before retirement, no loans, 100% vested, and continues to earn dividends which are reinvested, some in stock, some in a target date fund. The target date fund will roll over to a IRA.

1 – Has too much time elapsed to use a NUA plan? We were planning on doing this in 2018.

2 – Does the tax on the cost basis need to be paid at the time of taking the stock in like kind? Lot of money.

3 – Can some of the NUA stock be gifted in increments to young adult children who don’t earn enough money to pay long term capital gains? Maybe a trust for their benefit?

4 – If some of the NUA stock was held until death of my spouse and I, would the step up in value apply to the children?

1. No, as long as you take your lump sum distribution in one calendar year after a qualifying event. The year she reaches 70.5 will be her last opportunity because that is the year her RMD will start which is a distribution.

2. You must pay the tax for the year the distribution is taken. So if you take it in 2018, you must pay the tax with your 2018 taxes.

3. You can gift it after the lump sum distribution but if you are trying to avoid or reduce the tax on the NUA this won’t work. You must pay the tax before you gift the stock to your children.

4. There is no step up in value applied to stock held in a 401K or IRA. If the stock was put into a taxable account after the lump sum distribution then, yes the step up in value would apply to the children.

To clarify, since I retired a few years ago at age 55, I’m not disabled and don’t plan to die soon, is the only time frame I have remaining to take advantage of the NUA strategy the year after I turn 59 1/2 ?

There is no stated time limit, but you must take your lump sum distribution (LSD) of company stock before you take any other distributions in intervening years. You must take your company stock in-kind as a LSD within one taxable year, which may be taken in one or more payments, of your entire balance from all like-type qualified plans sponsored by your employer. You couldn’t delay the LSD longer than the year you reach 70.5 because the plan is required to distribute an RMD to you at that time so that year is the longest you could wait and retain the NUA option.

I have a tax question related to my company stock held in a 401k. In looking at NUA and IRA rollover options, I understand that the IRS allows you to rollover stock equal to the total cost basis of total into an IRA and take distribution of the stock equal to the NUA. By rolling over the taxable cost basis to the IRA, I would delay the payment of ordinary income tax (until mandatory distribution at age) and have the NUA (large majority of stock value) outside of the IRA that is subject only to long term capital gains tax when I decide to sell and diversify my investment.

Is my understanding of this provision accurate?

Thanks in advance for your help.

I have read many posts and guides on the tax treatment of NUA stock, even the IRS publications. What I have not found is the answer to this question – when you take NUA stock out of a 401K and place it in a taxable brokerage account, what date do you use as the acquisition date of the NUA stock for any future sales of the NUA shares?

– the original acquisition date (which my 401k provider does not provide/track)

– the distribution date from the 401K

– some other date?

thanks,

As the article text and supporting graphic state in the section “NUA Tax Treatment At Distribution And Subsequent Sale”, gains that occurred inside the plan are ALWAYS taxed at long-term capital gains rates (the acquisition date is literally irrelevant), and any subsequent gains after distribution are short- or long-term based on the holding period from the date of distribution until the final sale date.

– Michael

I have been taking the dividends, instead of reinvesting them, on the company stock in my 401K. Does this considered a distribution by the IRS?

As I understand there is no step up on taxable NUA. What would the cost basis be if the original cost per share was 20.00.The distribution rate into taxable account was 120.00. Beneficiary was his wife .The share price at death was 150.00. Wife died several years later. At this time the share price was 220.00. My question is what is the cost basis for the daughter who is the beneficiary? Second question is how is reinvested dividends handled from a tax basis.?

Thank you for this detailed analysis. I have what is probably a more unusual question. A portion of the 401(k) employer stock purchases were made with after-tax funds. We have the option to designate which shares were purchased with the after-tax funds up to the amount of after-tax contributions. In that case, the NUAs do not trigger any taxes (as the tax has already been paid) on the basis of the employer stock. So, as a hypothetical, what if we were to take the high basis shares, some of which are under water, and designate those as NUAs. Upon the sale of those shares, a capital loss would be realized – to be used against other gains or carried forward. Is this strategy allowable?

How do I treat a sale with a mix of NUA Gain and short-term Post-Distribution Gain?

After 30 years, I retire and do an NUA distribution of all 750 shares of my 401k company stock (cost basis of $20/share) into my taxable account on 1/8/19, when price is $150/share. On 2/20/19, I sell 115 shares at $175/share. My broker wants to call all of this a Short-Term sale on the 1099-B, but I say, “Not so fast…” because it seems to me that this sale is a mix of NUA gain and a Post-distribution gain. But I can’t figure out how to report it as such.

One thought is to treat this as two seperate events with the same 125 shares: the first selling on 1/8/19 (Long-term gain), and the second, starting 1/8/19 and selling on 2/20/19 (short-term gain). Does this sound right? What would be a better or correct way of treating this?

To reduce the ordinary taxes in the NUA year I was going to contribute a small portion of the stock to a Donor Advisor Fund; however, I was told by the brokerage house that the NUA was less than 1 year old (Short term not long term) and the amount that would be considered for deduction is reduced from 42,000 to 6000. My cost basis was 1/7 of NUA value. We’re you aware that DAF would consider the stock as short term? As a result I will execute the stock to DAF next year to reduce my ordinary taxes.

If you have a defined benefit pension and a 401(k), does the lump sum distribution requirement (which, I understand means that you must fully distribute all qualified plans of the same type in a single year) mean you cannot qualify for NUA treatment on the company stock in the 401(k) plan unless you also take early distribution (i.e., liquidate) the pension in the same year as the 401(k)? In other words, for purpose of the lump sum distribution requirement, is a 401(k) plan considered to be the same type of qualified plan as a defined benefit pension plan? Not really sure how to take early distribution of the defined benefit pension. Thanks.

What would be the best practice for company stock held in a Roth 401K? Is there any benefit for NUAs in this case?

The firm handling my 401k mishandled and delayed the distribution of my account, and I will probably not meet the one-year lump sum distribution requirement. Are you aware of any way I can still salvage the NUA benefit?

So I have a client who elected to use the NUA strategy. Received all the tax documents, met all the requirements, received the total distribution with a 600k cost and a 110k NUA. That client ended up rolling over the entire 710k into a IRA. what happens to the 110k NUA? is it just reported as short term capital gains taxed at ordinary tax rates? I see the benefits of the NUA strategy, but I don’t find anything in regards to if the distribution is in fact rolled over. So guidance is much appreciated… Thanks

In this scenario below can an employee do a lump distribution while still employed say in December. Turn off contributions to 401K so balance at the end of the year is $0 and then begin contributions again in the following calendar year?

The participant is over 59.5 and wants to access the low basis stock and have dividends paid to cash outside of 401K.

2) The employer retirement plan must make a “lump sum distribution”. In this context, a “lump sum distribution” means the entire account balance of the employer retirement plan must be distributed in a single tax year. It’s important to recognize that this doesn’t just mean all the stock must be taken out of the plan; it means the entire account must be distributed. Although ultimately, it’s up to the plan participant to choose where the dollars end up; it is permissible to do an NUA distribution for just some of the account, and roll over the rest directly to an IRA (or even convert to a Roth). However, none of the money can stay in the plan past the end of that year.

Thank you for everything that you do Michael. Looking for some clarity on the distribution date. I just used an NUA strategy for one of my clients. His 401k was with Fidelity. Fidelity took the NUA instructions and told us the shares would be sent in-kind from their plan. They used Computershare as a means of doing that. The transfer settled today from Computershare to our BD and we sold the shares immediately . My question is would we use a distribution date of today since the transfer settled today? During this “in-kind” process my clients shares jump by roughly 67k. Just trying to determine if there are any post distribution gains. Thanks in advance

Hi @Michael_Kitces:disqus — the article's main arguement mentions paying tax on even a modest amount of basis isn't great because you lose ability to defer these taxes….BUT doesn't this ignore their projected tax rate over time and the potential to harvest ordinary income at a lower rate now vs. later? It also ignores their asset balances across tax buckets, and ignores their projected required withdrawals. I have a client sitting on a MAJOR tax time bomb (SS + SS + Pension + Real Estate income + 5M 401k (of which 1.5m is employer stock))…

Doing an NUA in 2026 once retired would:

-Allow them to pay a much lower average rate than what they are projected to be at in the future.

-Allow for sorely needed taxable assets to pay for lifestyle AND allow them to do Roth conversion in lower brackets (they have almost no taxable assets, and without NUA assets they would be forced into the 24% bracket as they would have to rely on pre-tax assets anyways to pay for lifestyle. When going with an NUA strategy, the employer stock in a taxable account would provide a large chunk of that needed income anyways at LTCG (roughly 60%).

Have you done any blogs that demonstrate these other important variables to consider? Thoughts?

They cannot cherry pick low basis stuff, since the plan administrator is not required to track this and did not.

to add to the below. Doing the $1.5m NUA would allow them to optimize their asset location substantially, as a 70/30 investor, they would be able to shift a huge chunk of stock from pre-tax to taxable, and thus de-risk in their pre-tax bucket, reducing future RMDs (assuming stocks continue to grow faster than bonds).