Executive Summary

Life insurance serves a valuable social purpose, allowing families to protect themselves against the economic consequences of an untimely death of a breadwinner. In fact, life insurance is viewed as such a positive that Congress provides significant tax preferences for insurance policies, including tax-deferral on any growth in the cash value, and a tax-free death benefit for the beneficiaries.

Another popular tax feature of life insurance is the ability to access the policy’s cash value in the form of a tax-free loan. However, in reality the tax-free treatment of a life insurance policy loan is not actually a preference for life insurance under the tax code, but the simple recognition that ultimately a policy loan is just a personal loan between the life insurance company and the policyowner, for which the life insurance cash value is collateral. A credit card cash advance isn’t taxable, nor is a cash-out mortgage refinance, and a personal loan from a life insurance company isn’t, either.

However, while a life insurance loan isn’t taxable – nor is its subsequent repayment – the presence of a life insurance loan can distort the outcome if/when a life insurance policy is surrendered or otherwise lapses. Because the insurance company will require that the loan be repaid from the proceeds of the policy.

In the case of a life insurance death benefit, this isn’t necessarily problematic. The death benefit is already tax-free, and the loan is simply repaid from the tax-free death benefit, with the remainder paid to heirs.

When a life insurance policy is surrendered or otherwise lapses, though, the remaining cash value is again used to repay the loan… even though the taxable gain is calculated ignoring the presence of the loan. Which means in the extreme, it’s possible that a life insurance policy can lapse without any remaining net cash value, due to a loan repayment, yet still produce a significant income tax liability based on the policy’s gains. This “tax bomb” occurs because in the end, even if all of a policy’s cash value is used to repay a life insurance loan, it doesn’t change the fact that if the policy had a taxable gain, the taxes are still due on the gain itself!

The Tax-Preferenced Treatment Of Life Insurance Policies

Given the importance of life insurance, Congress has established numerous tax preferences to encourage its use.

The biggest by far is the simple fact that a life insurance policy’s death benefit itself is entirely tax free. Under IRC Section 101(a), “gross income does not include amounts received under a life insurance contract, if such amounts are paid by reason of the death of the insured.” As a result, even if a policyowner never pays more than a single $1,000 premium for a $1,000,000 death benefit and then passes away, the heirs will receive the implicit $999,000 gain entirely tax-free. (Notably, certain exceptions to the tax-free treatment of life insurance death benefits apply when the policy was sold to someone else, under the so-called “transfer for value” rules.)

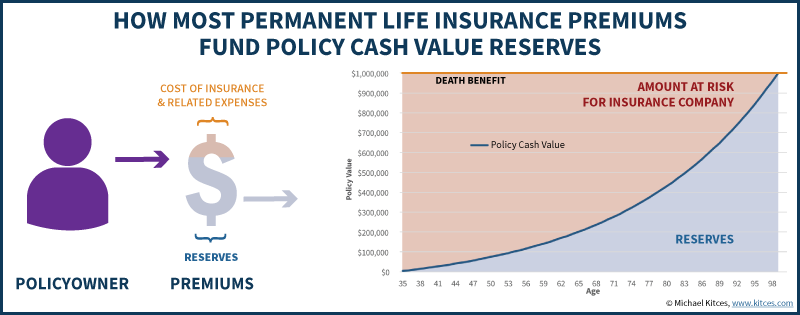

In the case of term insurance, this process of pay-premiums-for-tax-free-death-benefit is relatively straightforward. However, with “permanent” insurance that will pay out as a death benefit or “mature” as an endowment policy at the maximum age (historically age 100, and age 121 for more recent policies), the situation is more complicated. The reason is that the premiums of a permanent insurance policy cover not only the raw cost of insurance, but are partially allocated to a reserve that both helps to cover future costs of insurance and reduces the amount at risk for the insurance company over time. So-called “non-forfeiture” laws ensure that if a consumer walks away from the policy, that reserve is available in the form of a policy cash value that can be paid if/when the policy is surrendered.

To further encourage the use of life insurance, Congress has also provided under IRC Section 7702(g) that any growth/gains on the cash value within a life insurance policy are not taxable each year (as long as the policy is a proper life insurance policy in the first place). As a result, if a permanent insurance policy is held until death, the taxation of any gains are ultimately avoided altogether; they’re not taxable under IRC Section 7702(g) during life, and neither the cash value growth nor the additional increase in the value of the policy due to death itself are taxable at death under IRC Section 101(a).

The Taxation Of Withdrawals From A Life Insurance Policy

One caveat to the favorable treatment for the taxation of life insurance policies is that it applies only as long as the life insurance policy is actually held intact.

If a withdrawal is taken from the policy, the gains may be taxable (as ordinary income), although under IRC Section 72(e)(5)(C), any distributions are treated first as a return of principal (the “investment in the contract”), and gains are only taxable after all the cost basis has been recovered. (Though policies treated as a “Modified Endowment Contract” or MEC are taxed gains-first.)

If the policy is fully surrendered – which means by definition all principal and all gains were withdrawn (at once) – any gains are fully taxable as ordinary income under IRC Section 72(e)(5)(E), to the extent the total proceeds exceed the cost basis.

Notably, when it comes to life insurance, the cost basis – or investment in the contract under the rules of IRC Section 72(e)(6) – is equal to the total premiums paid for the policy, reduced by any prior principal distributions (which could include prior withdrawals, or the previous receive of non-taxable dividends from a participating life insurance policy).

The Taxation Of Receiving A Life Insurance Policy Loan

One of the more popular features of permanent life insurance with a growing cash value is the fact that the policyowner can borrow against the policy without incurring any tax consequences. By contrast, as noted above, surrendering the policy could cause a taxable gain (as would taking withdrawals in excess of the policy’s cost basis, if the policy even allows withdrawals in the first place).

In reality, though, the “tax-favored” treatment of a life insurance policy loan is not actually unique or specific to life insurance. After all, technically a life insurance policy loan is really nothing more than a personal loan from the life insurance company, for which the cash value of the insurance policy is collateral for the loan. The fact that the life insurance company has possession and controls that policy cash value allows the company to be confident that it will be paid back, and as a result commonly offers life insurance policy loans at a rather favorable rate (at least compared to unsecured personal loan alternatives like borrowing from the bank, via a credit card, or through a peer-to-peer loan).

Accordingly, the cash from a life insurance policy loan is not taxable when received, because no loan is taxable when you simply borrow some money! Just as it’s not taxable to receive a credit card cash advance, or a business loan, or the cash from a cash-out refinance, a life insurance policy loan is not taxable because it’s simply the receipt of a personal loan.

Example 1. Charlie has a $500,000 whole life insurance policy with an $80,000 cash value, into which he has paid $65,000 of cumulative premiums over the years. Due to the nature of the whole life policy, Charlie is not permitted to take a withdrawal from the policy (against his $65,000 basis), but he can request a loan from the life insurance company against his $80,000 cash value. If Charlie takes out a $20,000 loan, the loan itself is not taxable, because it is simply a personal loan between Charlie and the insurance company. The life insurance company will use the $80,000 cash value of the policy as collateral to ensure the loan is repaid.

For better or worse, the taxation of the underlying transaction – of the life insurance policy and any gains that have been generated – is determined by what the policyowner ultimately does with the policy itself, not the mere fact that the policy was used as collateral for a loan in the meantime.

Taxation Of Life Insurance Policy Loan Repayment

Since receiving the proceeds of a personal loan are not taxable, it is perhaps not surprising that the repayment of that loan isn’t taxable either. Repaying the principal of a mortgage doesn’t have tax consequences, repaying the balance on a credit card doesn’t have tax consequences, and repaying a personal loan for which a life insurance policy is collateral doesn’t trigger any tax consequences either.

However, the “no tax consequences” outcome of repaying a life insurance policy loan can be impacted by how the loan is repaid. To the extent that it is repaid with ‘outside’ dollars (unrelated to the life insurance policy itself), the repayment is not taxable just as the receipt of the loan proceeds weren’t taxable either. On the other hand, if the repayment of the loan involves drawing money from the life insurance policy itself, the outcome may be different.

Repaying Life Insurance Loans On Policies Held Until Death

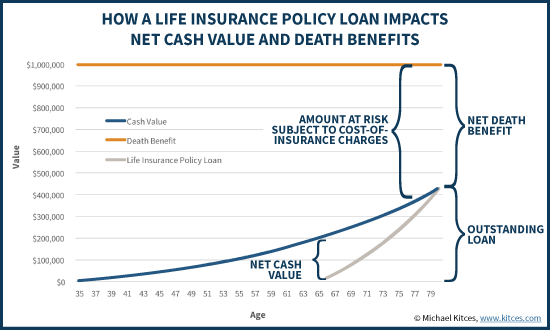

If a life insurance policy with a loan is held until death, the insurance company ultimately uses the death benefit proceeds of the life insurance policy to repay the loan, with the remainder paid to the policy’s beneficiary.

In point of fact, this is why any form of life insurance policy loan is shown as a ‘reduction’ to the death benefit of the policy. Because the life insurance company uses a combination of the policy cash value (while alive) or the policy death benefit (after death of the insured) to provide collateral and ‘guaranteed’ repayment of the loan. In other words, technically when a life insurance policy loan occurs, the death benefit is not actually reduced (which means the cost-of-insurance charges don’t decline for any reduction in the amount-at-risk to the insurance company); instead, the insurance company simply recognizes that any final death benefit to be paid will be reduced first by the repayment of the loan balance.

Example 2. Andrew has a $1,000,000 whole life insurance policy that, by the time he has now turned 65, has almost $200,000 of cash value, and since he has only put in about $140,000 in premiums over the years, he faces a potential $60,000 gain if he surrenders the policy to use the cash value as a retirement asset. To tap the policy’s cash value, and free up available cash flow, Andrew decides to stop paying the $5,000/year premium on the policy, and take out $15,000/year in the form of a policy loan. (Notably, the total annual policy loan would be $20,000/year, as with a whole life policy the premiums are required to be paid, and so “not paying premiums” simply means the insurance company will automatically take out a loan every year and use the proceeds to pay the annual premium obligation.)

By the time Andrew turns 80, his cash value will have risen to nearly $450,000, through a combination of ongoing growth and the ongoing contribution of premiums (paid via the personal loans from the life insurance company). The loan balance itself will be up to $400,000, with loans of $20,000/year (in total) plus accrued interest.

Given this dynamic, if Andrew were to pass away, the policy would pay a net death benefit of $600,000, based on the $1,000,000 life insurance death benefit reduced by the $400,000 loan balance. Notably, though, even though the net death benefit is only $600,000, Andrew’s life insurance policy still has cost-of-insurance charges calculated based on the original death benefit, not just the reduced death benefit amount.

From the tax perspective, though, the repayment of a life insurance policy loan from the death benefit of the policy is tax-free, because the payment of a death benefit itself (by reason of the death of the insured) is tax-free in the first place. In other words, to the extent that a life insurance loan is simply a personal loan with the insurance company that is repaid from the death benefit proceeds, the policy loan repayment is as “not taxable” as any loan repayment is, and the tax-free life insurance death benefit remains tax free.

Life Insurance Loans On Policies That Are Surrendered

As noted earlier, when a life insurance policy is surrendered in full, the gains on the policy are taxable (as ordinary income) to the extent that the cash value exceeds the net premiums (i.e., the cost basis) of the policy.

As a result, if a life insurance policy is surrendered to repay an outstanding life insurance loan, the net transaction can have tax consequences – not because the repayment of the loan is taxable, but because the surrender of the underlying policy to repay the loan may be taxable.

Example 3. Sheila has a life insurance policy with a $105,000 cash value, a $60,000 cost basis, and a $30,000 loan. In the event that Sheila surrenders the policy, her total gain for tax purposes will be $45,000, which is the difference between the $105,000 cash value and her $60,000 cost basis. Notably, the tax gain is the same $45,000, regardless of the presence of the $30,000 loan. If Sheila didn’t have the loan, she would receive $105,000 upon surrender of the policy; with the loan, she will only receive $75,000, because the remaining $30,000 will be used to repay the outstanding loan. Either way – whether Sheila had received the $105,000 value (without a loan) or only $75,000 (after repaying the loan) – the taxable gain is the same $45,000.

In this context, the reality is still that the life insurance policy loan itself has nothing directly to do with the taxation of the transaction. The policyowner did use the proceeds from surrendering the policy to repay the loan, but the tax consequences were determined regardless of the presence of the life insurance loan.

The Life Insurance Loan Tax Bomb On Lapsing Policies

In the preceding example, the presence of the life insurance policy loan reduced the net cash value received when the policy was surrendered, even though it didn’t impact the tax consequences of the surrender. Given how much cash value was available, though, this wasn’t necessarily “problematic”; it simply means the policyowner would use a portion of the $75,000 net proceeds to also pay any taxes due on the $45,000 gain.

However, the situation is far more problematic in scenarios where the balance of the life insurance policy loan is approaching the cash value, or in the extreme actually equals the total cash value of the policy – the point at which the life insurance company will force the policy to lapse (so the insurance company can ensure full repayment before the loan collateral goes ‘underwater’).

The reason is that in scenarios with a large loan balance, the fact that there may be little or absolutely no cash value remaining does not change the fact that the tax gain is calculated based on the full cash value before loan repayment. Because, again, a life insurance policy loan is really nothing more than a personal loan from the life insurance company to the policyowner, for which the policy’s cash value is simply collateral for the loan.

As a result, the lapse of a life insurance policy with a large loan can create a “tax bomb” for the policyowner, who may be left with a tax bill that’s even larger than the remaining cash value to pay it.

Example 4. Continuing the prior example, assume that Sheila had accumulated a whopping $100,000 policy loan against her $105,000 cash value, and consequently just received a notification from the life insurance company that her policy is about to lapse due to the size of the loan (unless she makes not only the ongoing premium payments but also 6%/year loan interest payments, which she is not interested in doing).

Sheila can allow the policy to lapse, ‘escaping’ the $6,000/year loan interest by using the $105,000 cash value to repay the $100,000 loan, and receiving a check for the $5,000 net proceeds. However, upon lapse of the policy, which had a cost basis of only $60,000, Sheila will still face a taxable gain of $45,000, which is the difference between the actual cash value of the policy and her original investment into the contract.

The end result is that even though Sheila will only salvage $5,000 from the surrender of her life insurance policy, she’ll receive a Form 1099-R for the $45,000 gain, and at a 25% tax rate will owe $11,250 of income taxes… which is more than the entire net surrender value of the life insurance policy, due to the loan!

The fact that the lapse of a life insurance policy with a loan can trigger tax consequences even if there is no (net) cash value remaining is often a surprise for policyowners, and has even created a number of Tax Court cases against the IRS over the years. However, as illustrated in the recent case of Mallory v. Commissioner, the Tax Courts have long recognized that the gain on a life insurance policy is taxable, even if all the cash value itself is used to repay an existing policy loan!

Common Life Insurance Loan Tax Bomb Scenarios

An important caveat of the potential danger of the life insurance loan tax bomb is that it doesn’t matter how the loan accrued in the first place.

For instance, in the earlier scenario, it may be that Sheila actually borrowed out $100,000 from her policy, triggering its imminent collapse. Or it’s possible that Sheila only borrowed $50,000 long ago, and years of unpaid (and compounding) loan interest accrued the balance up to $100,000, to the point that the policy would no longer sustain. The fact that Sheila only “used” $50,000 of the loan proceeds directly doesn’t change the outcome.

In some cases, a life insurance policy tax bomb is simply triggered by the fact that the policyowner stopped paying premiums at all. This is especially common in the case of whole life insurance policies, where technically it is a requirement to pay the premium every year (unless the policy was truly a limited-pay policy that is fully paid up), and if the policyowner stops paying premiums the policy will remain in force, but only because the insurance company by default takes out a loan on behalf of the policyowner to pay the premium (which goes right back into the policy, but now the loan begins to accrue loan interest). In turn, years of unpaid premiums leads to years of additional loans, plus accruing loan interest, can cause the policy to lapse. The end result: the policyowner never actually uses the life insurance loan directly, and finishes with a life insurance policy with a net cash surrender value of $0, and still gets a Form 1099-R for the underlying gain in the policy. Because the fact that premiums were paid via loans, for years, still doesn’t change the fact that it was a life insurance policy with a gain, even if all the underlying cash value was used to repay a personal loan (that, ironically, was used to pay the premiums on the policy itself!).

Another scenario that can trigger a ‘surprise’ life insurance loan tax bomb is where the policy is using to as a “retirement income” vehicle, either through a version of the “Bank On Yourself” strategy, or simply by taking ongoing loans against the policy to supplement retirement cash flows, and the loans grow too quickly and cause the policy to lapse. Once again, even if the life insurance policy’s cash value is depleted to zero by ongoing policy loans, the lapse of the policy and the lack of any remaining cash value at the end doesn’t change the tax consequences of surrendering a life insurance policy with a gain (since in essence the gains were simply ‘borrowed out’ earlier and still come due!).

Fortunately, the “good” news is that the policy loan tax bomb can be avoided by actually holding the life insurance policy until death – allowing the loan to be repaid from the tax-free death benefit, instead of the (taxable) surrender of the policy. The bad news, however, is that some policies have such significant loans that it’s not affordable or economically feasible for the policyowner to keep the policy going, which may entail paying ongoing premiums, and life insurance loan interest (to keep the policy loan from further compounding to the point it forces the policy to lapse), or even paying additional cost-of-insurance charges to keep enough cash value in the policy to remain in force (in the case of universal life policies). Nonetheless, to the extent that the policy can remain in force until death, the life insurance loan tax bomb is at least potentially avoidable, though of course in many situations it may have been preferable to just not take out the loan in the first place!

So what do you think? Have you ever had a situation where a life insurance policy lapsed due to a loan, and there was no remaining cash value but a big taxable event? Have you ever tried to keep a policy afloat just long enough to pay out as a death benefit and avoid any tax consequences that would occur if the policy lapsed?