Executive Summary

Tax loss harvesting is a popular tax planning strategy, especially as the end of the year approaches and investors consider their potential capital gains exposure. Yet for many investors, the benefit of tax loss harvesting is overestimated, as harvesting a loss generates current tax savings, but also reduces the cost basis of the investment, triggering a potential gain in the future that may offset most or all of the loss harvesting benefit!

Nonetheless, even if a harvested loss creates a future gain, there is still an opportunity for tax deferral in the meantime, which can create a modest but non-trivial economic benefit for tax loss harvesting. The benefits are further amplified – sometimes greatly so – if there is a potential that gains in the future will be taxed at a lower rate than losses harvested today, with the caveat that if brackets go the other direction, tax loss harvesting not only loses its positive value but can actually be wealth destructive!

To the extent that tax brackets changes are anticipated favorable, though – or at least, that rates will hold steady – some benefit to tax loss harvesting remains, and can be maximized with portfolios that hold a wide range of diversified positions (creating more loss harvesting opportunities), have ongoing contributions (again creating more loss harvesting opportunities), and are checked frequently for losses to harvest (as only trying to harvest losses in December can miss out on even greater intra-year loss harvesting opportunities!). And for those who are not at risk for adverse tax bracket changes, the tax loss harvesting opportunity is especially appealing in today’s environment, with transaction costs (including trading fees and bid/ask spreads) as low as they've ever been, and more opportunities than ever to own investment alternatives that minimize tracking error while navigating the wash sale rules!

The History Of Tax Loss Harvesting

Since the Federal government taxes an increase in the value of investment property as a capital gain, it’s only fair that investors be permitted to reduce their income for tax purposes by the amount of any losses that are generated. In fact, beyond allowing capital losses to offset capital gains, the tax code also allows individuals to manage the burden of taxation by allowing any gains on investment property to remain tax deferred until the investment is actually sold (which causes the gains to be “recognized” for tax purposes).

Yet the fact that capital losses can be deducted for tax purposes to generate current tax savings, while capital gains can be deferred by simply not selling the investment to recognize the gain, creates the potential that investors will take advantage of the tax code by trying to proactively recognize losses now for tax savings but push gains into the future. And in the first decade of the tax code, that’s exactly what happened – in fact, some investors were so aggressive about it, they would simply sell investments that had losses and purchase them back again immediately, “harvesting” the loss for tax purposes to generate current tax savings, but without even substantively changing their original investment!

To limit this kind of abuse, Congress enacted IRC Section 1091 as a part of the Revenue Act of 1921, which declared that if the investor sold an investment for a tax loss but purchased a substantially identical security that the loss would be disallowed for tax purposes. In creating these “wash sale” rules (which have been iterated upon over the decades to crack down on further abuses, such as selling for a loss and repurchasing in an IRA), though, Congress also indirectly blessed and enshrined into law the strategy of tax loss harvesting to generate current tax savings… as long as the requisite 30-day rule is navigated.

Tax Loss Harvesting (TLH) And The Problem With Annual Tax Alpha

Since the essence of Tax Loss Harvesting (TLH) is to create a deductible loss for tax purposes to generate current tax savings, the easiest way to measure the benefits of the strategy is simply to measure how much in taxes is actually saved relative to the investment.

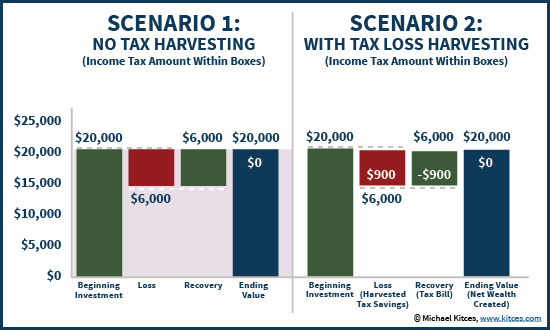

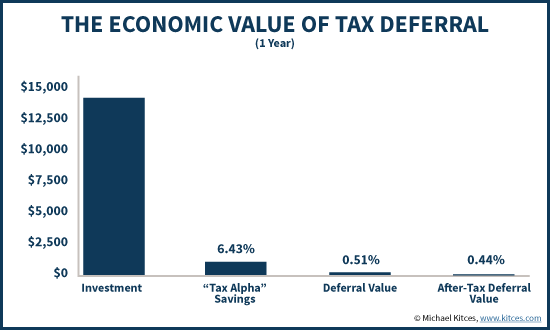

For instance, if an investment was originally purchased for $20,000 but is now down to $14,000 (a big 30% decline), then harvesting the loss generates a $6,000 capital loss, which in turn (assuming there are capital gains to offset it against) will produce a $900 tax savings at a 15% long-term capital gains tax rate. Relative to an investment value of $14,000, this means harvesting the capital loss generated a whopping “tax alpha” of $900 / $14,000 = 6.4%.

However, the reality is that harvesting the loss did not really increase the investor’s wealth by $900 of tax savings in the long run. The reason is that while the harvested loss did generate $900 of current tax savings, the act of harvesting the loss also reduces the cost basis of the investment. By selling the investment at $14,000 to harvest the capital loss and then reinvesting the $14,000 of proceeds, the “new” cost basis going forward will be $14,000. Which means if/when the investment eventually recovers back to its original $20,000, the investor will face a future “recovery gain” of… $6,000, and a negative tax alpha in the year of liquidation! In fact, if that capital gain in turn results in a $900 tax bill (assuming the same 15% long-term capital gains tax rate), the net value of the transaction is actually the exact same as would have occurred if loss was never harvested in the first place!

The caveat, though, is that the true economic value of tax loss harvesting is not quite a perfect zero, even though the future gain created by harvesting the loss will offset the tax savings generated by the loss. The reason why there is still a benefit to tax loss harvesting is that the loss is created now – producing additional dollars to invest – while the “recovery gain” will not create a taxable event until some point in the future. In the meantime, the investor has the opportunity to use, invest, and grow that $900. In other words, while tax loss harvesting doesn’t necessarily produce any net tax savings, it is the equivalent of getting an interest-free loan from the Federal government to use for a (potentially long) period of tax deferral.

Measuring The Economic Value Of Tax Deferral

So given that tax loss harvesting is really about tax deferral, and not outright tax savings, how can we measure the economic value of tax deferral?

At the most basic level, the benefit of tax deferral is simply the value of the growth that can be generated on that “temporary loan” from the Federal government, until it must be returned. For instance, continuing the earlier example, if the $900 of tax savings can be invested for an average return of 8%, then the true value of the tax deferral is $72 worth of growth. On a $14,000 investment, this equates to a true tax benefit of 0.51% after 1 year (and if we recognize that the $72 of growth will itself be subject to a 15% tax rate, the net benefit is 0.44%).

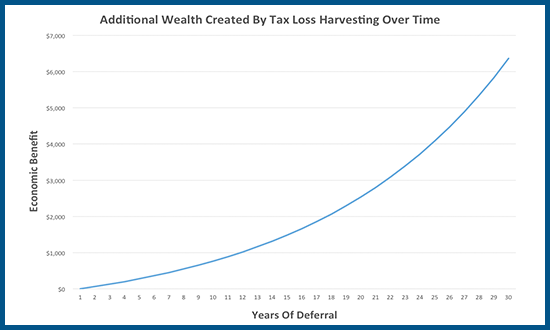

Of course, the caveat to this example is that as long as the investment continues to be held, the economic value of tax deferral continues to grow, and to compound. In other words, it’s not just that the value of harvesting the loss is $72 worth of growth, but that it’s $72 of growth, compounding over time, until it is ultimately sold! Accordingly, the chart below shows the (net after-tax) amount of additional dollars created over time by harvesting the $6,000 loss.

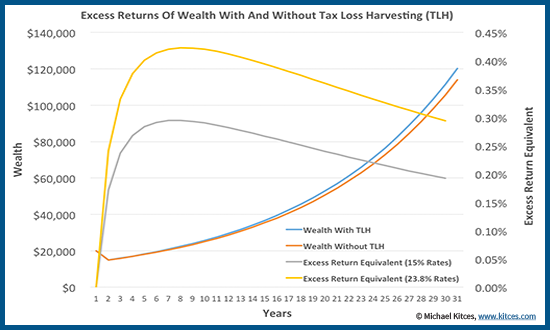

Thus, the benefit of tax loss harvesting over time is effectively a “tailwind” of additional economic growth generated as a result of investing the tax savings from the original harvesting transaction. Accordingly, we can calculate the true economic benefit of tax loss harvesting over time by comparing the amount of wealth created by harvesting the loss, comparing it to the wealth that would have existed without harvesting the loss, and comparing the internal rate of return between the two; the difference represents the “excess return equivalent” created by the tax loss harvesting transaction. Notably, in the long run, the excess wealth in dollars continues to compound upwards, but the excess return relative to the returns themselves begins to flatten and provide diminishing returns once the investment recovers above its original cost basis.

As the results show, while the benefit of tax loss harvesting is positive, it is not “huge” and is far smaller than “tax alpha” (calculated based on single-year tax savings alone) implies; with a 30% decline followed by 7% growth, the economic value of tax loss harvesting rises as high as almost 0.30%/year of additional annualized return equivalent at 15% tax rates (or 0.42% at 23.8% top capital gains rates), falling just below 0.20% and 0.30% (respectively) in the long run. As the results show, the benefits are greater if tax rates are higher – as there are more losses to be harvested for an economic benefit in the first place! Similar, the benefits are greater if the market decline is larger, producing more losses to harvest and more tax savings generated in the first place; and the benefits are also greater if subsequent returns are higher (allowing more compounding on the tax savings). Conversely, with smaller market declines, lower tax rates, and lower returns, the benefit of tax loss harvesting is diminished.

Given this somewhat modest benefit, it’s important to weigh the benefit of tax loss harvesting against the risks, which include transaction fees that may erode its value, along with the risk of “tracking error” (that the alternative security held to avoid the wash sale rules does not perform consistent with the original investment). On the other hand, though, as transaction costs continue to decline towards zero (with tighter bid/ask spreads and low trading fees), and the risk of “tracking error” is often diminished (as with today’s ETFs, it’s easier to hold a not-substantially-identical security to avoid a wash sale while still maintaining a relatively high correlation to the original investment), even these benefits for tax loss harvesting make it sufficient to consider pursuing systematically over time.

How Tax Bracket Arbitrage Changes The Benefit Of Tax-Loss Harvesting (For Better Or For Worse)

In all of the above examples, the benefit of tax loss harvesting was measured assuming tax rates stay the same at the time the loss is harvested, and when the subsequent recovery gain is recognized (whether at 15% or 23.8%). However, the reality is that sometimes, the tax rates will differ, creating a “tax bracket arbitrage” opportunity for additional tax loss harvesting benefits.

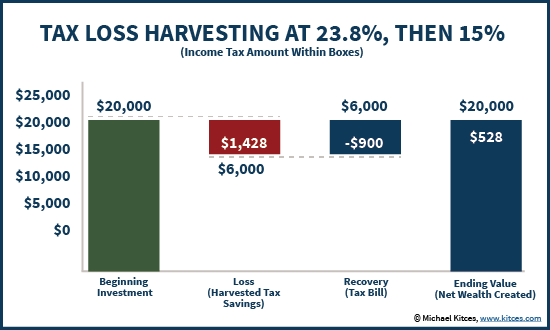

For instance, assume instead that the investor is at “peak” wages right now, boosting overall income to the top tax brackets and the capital gains rate to 23.8%, but anticipates retiring soon and that the associated capital gains rate will fall to only 15% from that point forward. In this context, the economic value of harvesting the loss is not merely the opportunity to invest the tax savings until it must be “repaid” from the recovery gain; wealth can also be created simply by the difference between the current and future tax rates.

Continuing the earlier examples, this means that with a $6,000 loss, the tax savings at 23.8% would be $1,428, while the subsequent $6,000 recovery gain would only be taxed at a 15% rate for $900 of subsequent taxes. As a result, harvesting the tax loss now (at 23.8%) and repaying it in the future (at 15%) creates $1,428 - $900 = $528 of “free” wealth, simply by effectively timing the tax rates!

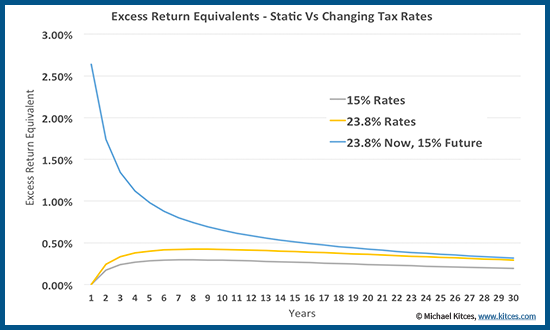

When added on top of the pure tax deferral benefits, the opportunity for tax bracket arbitrage creates significant additional wealth opportunities over time. The chart below shows a comparison of the tax loss harvesting benefits (in terms of “excess return equivalent” measured by the difference in internal rates of return between wealth with and without tax loss harvesting) depending on whether tax rates are a constant 15%, a constant 23.8%, or a higher 23.8% now and a lower 15% in the future. As the results show, the additional wealth potential by tax bracket arbitrage can be significantly larger than the tax deferral benefits (though ultimately tax bracket arbitrage benefits diminish, as the benefit is stretched out over time).

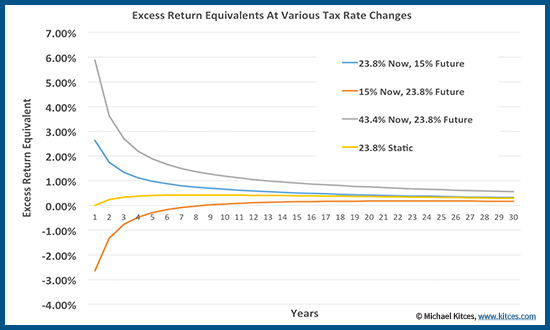

An especially favorable version of the comparison emerges if there is an opportunity for the investor to harvest a loss at ordinary income rates (e.g., by applying it against ordinary income to the extent of the $3,000 limit, or by harvesting a short-term loss and having short-term gains to offset it against); in such scenarios, the tax bracket arbitrage is significant, with a spread of 43.4% vs 23.8% at the top tax rates!

On the other hand, it’s worth noting that tax loss harvesting can also face adverse tax bracket changes as well. For instance, an investor harvesting at 15% capital gains rates might actually harvest so much in losses that the future recovery gain actually drives the future tax brackets higher! For instance, a relatively affluent investor might harvest $50,000/year for 10 years at 15% rates, but doing so brings down the cost basis of the portfolio by a cumulative $500,000, which means the subsequent recovery gain may be large enough to drive that investor into the top 23.8% tax bracket. Such negative tax arbitrage scenarios are a risk of tax loss harvesting (if not planned for) and can be wealth destructive, or at least require significant time for the benefits of tax deferral to overcome the adverse change in tax brackets. In fact, in situations where future gains may be “too large”, the optimal approach is actually not to harvest the losses, but to harvest the gains instead; similarly, for lower income individuals eligible for 0% long-term capital gains rates, it’s better to harvest gains for a “free” step-up in basis, rather than harvesting losses!

A comparison of these scenarios – including 23.8% static tax rates, harvesting at 23.8% but liquidating at 15%, harvesting at top ordinary income rates (43.4%) and liquidating at top long-term capital gains rates (23.8%), and an example of a “negative tax arbitrage” scenario of harvesting at 15% but liquidating at 23.8%, are shown below. As the results reveal overall, the benefits – or potential adverse consequences – of tax loss harvesting when tax brackets change can be far more impactful than the underlying benefit of tax deferral itself!

It’s also important to note that an especially “extreme” tax bracket arbitrage opportunity is available for those who ultimately plan to either die with the investment or donate it; the former allows for a step-up in basis that implicitly the future tax rate 0%, and similarly the latter also avoids any future taxation on the recovery gain through the rules for charitable deductions. To the extent that the future tax bracket is 0%, the associated tax bracket arbitrage will make the loss harvesting outcome be even more favorable!

Daily Checking, Diversification, And Other Factors That Impact The Benefits Of Tax-Loss Harvesting

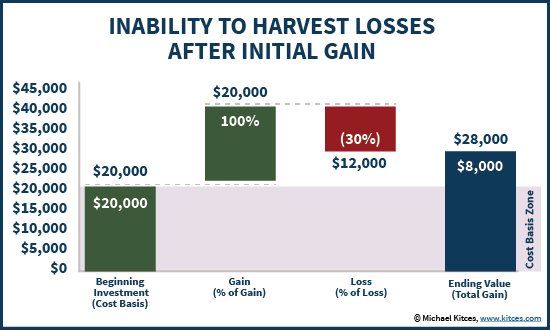

Thus far, we have looked at tax loss harvesting in what is arguably one of the “most favorable” possible scenarios – a dramatic -30% loss (a 2-standard-deviation event!) occurs immediately, in the first year, creating a significant long-term tax loss harvesting opportunity, with all the associated benefits of compounding growth on tax deferral and the potential for tax bracket arbitrage. However, in many (or even most?) cases, investments don’t immediately go down right after purchasing them. And in fact, if an investment rises enough in the early years, it may be so far ahead that even with a subsequent market decline, there will be no loss, as the investment may already be so far ahead there the decline doesn’t actually trigger a loss below cost basis!

To the extent that available losses to harvest in practice are lower than the examples shown previously, the likely benefit of tax loss harvesting for most investors will be smaller in practice, all else being equal.

On the other hand, the reality is that most investors don’t hold 100% of their portfolio in a single fund or investment. Instead, investors own multiple investments in a portfolio, which means even if some investments go up (possibly enough that there will never be losses to harvest because the investment will never again fall below cost basis), other investments that are not perfectly correlated might still decline below cost basis, creating a loss harvesting opportunity. Broadly speaking, this means that the more diversified a portfolio is, and the more granular the positions are (in the extreme, holding each of the 500 stocks in the S&P 500, rather than an S&P 500 ETF), the more opportunities there will be to do at least some tax loss harvesting. Similarly, ongoing contributions into the portfolio over time create the potential that even if some investments never have a loss harvesting opportunity (e.g., they are invested right before markets rise significantly), other investments into the market may be “less well timed” and experience early declines that create loss harvesting opportunities.

Similarly, it’s notable that while many advisors and investors have historically implemented tax loss harvesting on an annual basis (e.g., in the month of December), trying to harvest more regularly throughout the year creates more opportunities to actually harvest at the point of maximal loss. For instance, in 2011 the S&P 500 was down more than 10% in the middle of the year, but finished up 2%; annual tax loss harvesting would have found no losses to harvest, but trying to harvest more frequently would have generated some tax loss harvesting benefits. While there is some debate about exactly how much additional loss harvesting opportunities are created by “checking” for losses more frequently (some contend the value is significant, while others suggest it’s a fairly modest incremental benefit), there is clearly at least some improvement in practical tax loss harvesting efficiency by seeking out losses to harvest more often than just once a year. However, investors should be cautious about being too aggressive in frequent loss harvesting, as it is still possible to harvest too frequently; if the incremental losses to harvest are too small, they may be overwhelmed by what will likely still be some transaction costs and bid/ask spreads to contend with, and while tracking error can be reduced with today’s investment vehicles, it’s not zero and shouldn’t be ignored either. The combination of continuous checking of loss harvesting opportunities, especially for those making ongoing contributions, along with minimized transaction costs, has been a key advertised benefit of the Betterment and Wealthfront tax loss harvesting programs.

Of course, perhaps the greatest caveat to tax loss harvesting, though, is simply that none of these more granular loss harvesting opportunities, or the ability to check regularly for losses to harvest, will matter if there are no capital gains to offset with those losses in the first place! Under the Internal Revenue Code, if there are no capital gains to match against the losses, then up to $3,000 of losses can be applied against ordinary income, but the remainder must simply be carried forward for future use, generating no tax deferral savings, no opportunity for compounding growth, and no potential for tax bracket arbitrage at all! In fact, for many investors, harvesting losses when there are no gains to offset simply creates carryforward losses that just get used in the future to offset the gains created by harvesting the loss in the first place, which produces no economic benefits to harvesting the loss at all!

The bottom line, though, is simply this: tax loss harvesting (TLH) does have some economic benefit over time, although it’s driven not by the outright savings (typically measured by “tax alpha”), but instead by the economic value of tax deferral, which leads to modest but non-trivial economic benefits over time. For those who may experience tax bracket changes, the benefits can be significant amplified – for better or worse – and in fact, the impact of tax bracket arbitrage can be many times more significant than the underlying benefits of tax deferral itself. As a result, it’s crucial to focus not just on the tax deferral value of loss harvesting, but also the potential tax bracket impacts… and to the extent any anticipated tax bracket changes are favorable, and there are gains to offset with the losses in the first place, harvest as much as possible, maximizing the opportunity for each contribution, each investment/asset class being held, and by “checking” for loss harvesting opportunities as often as possible!