Executive Summary

In the nearly 10 years since Kevin Keller took over as the CEO of the CFP Board, the rolls of CFP certificants have grown by over 35%, even amidst a global financial crisis and an advisor demographics challenge that has contributed to a nearly 15% decline in advisor headcount over that time period.

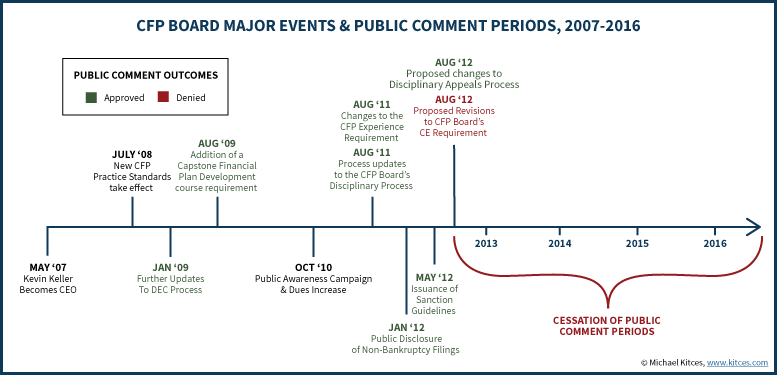

In Keller’s early days, the CFP Board’s focus was squarely on rebuilding trust with its various stakeholders, from a relationship that had suffered greatly from a string of 6 CEOs in the preceding 6 years before Keller took over. It was a time filled with growing communication from the CFP Board to CFP certificants, where initiatives were extensively vetted for stakeholder opinion and feedback, and more than half a dozen different public comment periods for various rules changes.

Yet since 2012, the first year that CFP Board “lost” an initiative due to negative feedback during the public comment period, the tone of CFP Board’s engagement with stakeholders has shifted. It’s now been a full 4 years since the CFP Board announced a single public comment period at all, despite engaging in numerous – and several unpopular – rules changes in the interim. And the CFP Board’s growing aspirations is leading towards an ever-growing path of mission creep, from being “just” the organization that maintains the CFP marks, into one that offers a Career Center, an academic home for CFP certificants, its own Journal, and even proposed to go into competition with its own CE providers.

Of course, ultimately any organization is accountable to its stakeholders who can “vote with their feet” to take their business elsewhere. Yet the growing dominance of the CFP marks as the financial planning designation of choice means financial planning practitioners have never had fewer real alternatives to choose from. And the CFP Board’s ongoing Public Awareness Campaign, with its “Certified = Qualified” message, implicitly impugns any CFP certificant to their clients if that individual decides to walk away from the CFP marks – which makes the limited complaints to CFP Board’s policy changes look less like tacit stakeholder affirmation, and more like acquiescence under duress.

While some might suggest this is all the more reason to step away from the CFP marks and find an alternative designation, I still believe that the CFP Board and its certification are still the best chance we have to become a recognized and bona fide profession. But it does mean that perhaps it’s time to recognize that the CFP Board’s success in growing the adoption and prominence of the CFP marks is fundamentally changing the stakes and its relationship to CFP certificants as stakeholders.

And so if the organization wants to maintain its legitimacy and authority with CFP stakeholders, it needs to (re-)adopt its use of public comment periods (and actually make the results public as other oversight organizations and regulators do!), not unilaterally force all CFP certificants to waive their right to hold the CFP Board accountable in court under any/all circumstances, and consider whether a governance model that deigns so much authority to its CEO and selects its board successors by purely internal means is really the right approach for its increasing role in the financial planning profession.

Approaching 10 Years Of CFP Board Under Kevin Keller

On May 1st of 2007, Kevin Keller took the reins of the CFP Board as its newest CEO, becoming at the time the 7th interim or permanent CEO in as many years for the organization. He entered an organization that had just gone through a stage of dramatic change, as the preceding full-time CEO Sarah Teslik had turned what was a CFP Board financial deficit when she took over into a surplus, at a ‘cost’ of cutting nearly 60% of CFP Board staff in under 2 years. And the spring 2007 board meeting at which Keller was approved as the CEO was also the one where the Board of Directors decided to move the organization from its original headquarters in Denver, to Washington DC instead. Which meant Keller’s first duty would be to manage the entire relocation of the organization, a task that within a year led to the turnover of more than 95% of (what after prior CEO Teslik was left of) the original Denver staff.

At the same time, Keller entered the CFP Board CEO position facing not only operational challenges, but a significant “trust deficit” with both the program directors and the CFP stakeholder community. Dating back nearly a decade prior to the infamous proposal to create an “Associate CFP” option (which was dubbed “CFP Lite” and ultimately dropped even after the board had already approved it, amidst overwhelming objections from CFP certificants), and continuing through the early 2000s as the CFP Board went through one CEO after another, by the time that Keller took over, most CFP certificants seemed happy with and proud of their marks, but were negative about and distrustful of the CFP Board itself.

The situation wasn’t helped when, shortly after Keller took over and began to make some internal staff and structural changes, his decision to restructured the Board of Professional Review into a new Disciplinary and Ethics Commission (DEC), which would include a greater role for CFP Board staff, led to a mass protest resignation by the then-current DEC leadership.

Accordingly, Keller and the CFP Board became extremely proactive in engaging with the CFP stakeholder community, in an attempt to rebuild trust. In 2010, the CFP Board engaged in an extremely proactive communication effort when it proposed its Public Awareness Campaign, including extensive data-gathering for feedback from certificants, “listening tours”, issuing Fact Sheets, and engagement with industry media doing follow-up Q&A – which undoubtedly helps to explain why the CFP Board successfully implemented the program, including with a whopping 80% increase in CFP certificant dues, and still didn’t experience any visible change in its renewal or growth rates.

More generally, over Keller’s first 5 years, the CFP Board engaged in more than half a dozen different public comment periods for various proposals. The public comment periods were very positive for rebuilding trust and buy-in from CFP certificants, giving the stakeholders an opportunity to engage and weigh in on a wide range of issues from the introduction of a Capstone financial plan development course requirement, to proposed changes to the CFP experience requirement, new rules for public disclosure of CFP certificant bankruptcies, multiple refinements to the disciplinary process and also the Appeals Process, and proposed changes to the CFP CE requirements.

However, while most CFP Board public comment periods received feedback that was generally supportive of the proposed initiatives, the responses to the CFP Board’s August 2012 proposal to increase the CFP CE requirement from 30 hours to 40 was met with dramatically different feedback. This time, a whopping 85% of CFP certificants complained that current CE quality was so low, there was no value to raising the required hours, forcing the CFP Board to roll back its plans.

CFP Board’s 4-Year Silence On Public Comment Requests

Since the failure of the CFP Board’s initiative to increase the required hours for CFP CE, a drastic shift occurred – all requests for public comment ceased.

In fact, after a string of over half a dozen public comment periods during Keller’s first 5 years as CEO, I can’t find a single request for public comment from the CFP Board since it failed to garner support for its proposal to increase the hours of required CE.

In other words, as long as the public comment periods concluded with feedback that was supportive to the CFP Board’s original plans, the organization continued to ask for public comments. As soon as the feedback from a public comment period derailed a planned CFP Board initiative, the CFP Board stopped asking for public comments from stakeholders. (Michael’s Note: Apologies to the CFP Board if there was at least one more public comment period that occurred since August 2012. Since the CFP Board does not actually post its Public Comments, nor even record its proposed rule changes in any central location, it’s extremely difficult to track!)

Notably, though, the elimination of public comment periods has not stopped the CFP Board from continuing to make rule changes to the CFP marks. In fact, despite its history of engaging public comments from CFP stakeholders, especially around anything relating to the “Four E’s” of the CFP Education, Exam, Experience, and Ethics requirements, the CFP Board has made several substantial – and controversial – changes in the past 4 years, without any public comment requests, including:

- Reducing the duration of the CFP exam from a 10-hour 2-day exam, to a 6-hour 1-day exam (in addition to switching the exam from being paper-based to electronic)

- Reducing the stringency of what constitutes “experience” to satisfy the CFP experience requirement (despite having not implemented such a change after the prior public comment period!)

- Eliminating the Capstone requirement for CFP exam challengers, after having instituted the requirement pursuant to a public comment period

The notable commonality amongst all of these is that they were changes that made it easier to obtain the CFP marks (or at least, created the perception that it would be easier) – which are the exact kind of changes that CFP certificants have historically objected to (dating back to the days of the CFP Lite controversy). By not requesting public comment – and/or ignoring or not updating prior public comment periods – the CFP Board drove through the changes directly, as individual CFP certificants who objected were unable to stop the changes, and the membership associations refused to take a public position on behalf of CFP certificants. And who knows what other internal policy changes may have been implemented by the CFP Board in recent years, that we don’t even realize because they didn’t get announced in a press release at all?

Similarly, while the CFP Board was very proactive in communicating in advance the proposed Public Awareness Campaign, listening to certificant feedback, issuing Fact Sheets and conducting surveys to validate its support, and proactively gaining buy-in from stakeholders, last year the CFP Board announced its major new Center for Financial Planning, a multi-million-dollar initiative, as a fait accompli (and then tried to default CFP certificants into voluntary dues). Similarly, the CFP Board engaged little to no CFP certificant feedback before the rollout of its pricey and conflicted Career Center, and its 2013 proposal to compete against independent CE providers with its own CFP Board CE offering was only narrowly beaten back after an uproar from stakeholders (who voiced their concerns despite the lack of a public comment period).

The latest in this series of unilateral changes was the CFP Board’s announcement in March that it would be changing its Terms and Conditions to which all CFP certificants are bound, requiring all certificants to waive their right to sue in court and instead require a mandatory arbitration process, while also requiring CFP certificants to waive most of their rights to recover any damages against the CFP Board (beyond their $325/year certificant dues). After a strenuous objection on this blog about the overly broad scope of the required waivers of liability and mandatory arbitration, and the dangerous lack of transparency that would result, the CFP Board did partially relent with an agreement that the outcomes of the arbitration proceedings would be publicized (on an appropriately anonymized basis). But this outcome still doesn’t fully address why the CFP Board needs such a broad-scope mandatory arbitration agreement in the first place. And ultimately, such a change should have been accomplished with a public comment period to begin with… which in turn raises the question of what else CFP certificants might have objected to in the details of the Terms and Conditions, were they ever given the chance for feedback before they were required to sign the contract.

How The Public Awareness Campaign Changed The Stakes Of Stakeholder Engagement

Of course, the looming caveat to all of this discussion is that technically, the CFP Board doesn’t have to engage CFP certificants at all. Legally, the CFP Board is not a 501(c)(6) membership association; it’s a 501(c)(3) charity, with a mission to benefit the public by granting the CFP certification and upholding it as the recognized standard of excellence for competent and ethical personal financial planning. A mission that the CFP Board fulfills in large part by being the owner of the CFP® trademark, and controlling the terms of its licensing and use (by CFP certificants).

In other words, the CFP Board is not a membership association of CFP certificants; instead, the CFP Board chooses to allow CFP certificants to license the use of its CFP marks as a part of fulfilling its public charity consumer-oriented mission.

On the other hand, the reality remains that the CFP Board can only feasibly accomplish its mission if financial planning practitioners are willing to adopt the CFP marks in the first place. If the collective practitioner community rejects CFP certification as a path to becoming more technically competent, and no longer finds value in licensing the use of the marks, the CFP Board has no one to whom the CFP marks can be granted in pursuit of its mission.

And in Keller’s early years, the CFP Board appeared to be wholly embracing this perspective, with its greatly improved communication after the move to Washington, and proactive use of public comment periods when considering changes that could impact the CFP marks and affect existing CFP certificants. Yet since the failure of the initiative to expand the number of CFP CE hours as a result of a public comment period with a ‘negative’ outcome, the tone of CFP certificant engagement from the CFP Board has shifted in a way that’s problematic. Not just because the CFP Board literally isn’t engaging CFP certificants the way it once did – in a manner that is already beginning to undermine its credibility, and risks further delegitimizing the organization in the long run – but also because the CFP Board’s Public Awareness campaign has changed the rules of the game.

After all, when any organization fails to engage its stakeholders, the most fundamental level of accountability is the fact that stakeholders can “vote with their feet” and take their business elsewhere. But with the ongoing success of the CFP Board’s public awareness campaign, which now puts the CFP marks over the CPA license as the most top-of-mind designation for finding a financial planner (and substantially beating out other alternatives from CFA to ChFC to PFS), advisors can’t vote with their feet and abandon the CFP marks without hurting their own credibility.

In fact, with the CFP Board’s most recent stage of the campaign, built around the theme “Certified = Qualified”, any CFP certificant that opts to walk away from being “Certified” with CFP Board will be implicitly criticized in public by the CFP Board as no longer being qualified to serve their clients! In other words, while the campaign may be ‘edgy’ in pushing consumers to find a CFP certificant, for existing CFP certificants who are unhappy with the CFP Board’s direction, it borders on forced acquiesce under duress to CFP Board’s policies (and policy changes).

In other words, the CFP Board doesn’t seem to recognize how its own (successful) public awareness campaign has materially changed the stakes and dynamic of its relationship with CFP certificants. And the larger the ranks of CFP certificants get – and especially the higher the percentage of financial advisors who have the CFP marks, making it less and less ‘optional’ and more like the minimum stakes to be a bona fide professional – the greater the tension becomes. In turn, this risks resulting in a further breakdown in CFP Board’s accountability to its stakeholders, as they cannot hold the organization accountable when they have no meaningful alternative choice – a dynamic the CFP Board seems to have implicitly realized in its willing halt to allowing for public comment periods.

Is It Time To Revisit CFP Board Governance And Accountability?

As the CFP Board will quickly note, they have a Board of Directors that is intended to provide this key level of governance oversight and organizational accountability. And that Board of Directors does include numerous CFP certificants and current and former practitioners, including current Chair Mike Greene, Chair-Elect Blaine Aikin, and incoming Chair-Elect Richard Salmen.

Still, the ongoing challenges of the CFP Board in recent years suggests that its Board of Directors may not be an entirely effective point of accountability as it is currently constituted. After all, virtually all of the recent changes of concern – from reducing the CFP exam length and experience requirement, to the unilateral changes to certificant Terms and Conditions, not to mention its expansionary efforts to launch the Career Center, the Center for Financial Planning, and the CFP Board’s ill-fated proposal to become a CE provider – were either discussed or fully approved by the Board of Directors.

Of course, it’s not hard to see why all these initiatives and decisions were approved by the Board of Directors. With the narrowing of the Terms and Conditions, how could a Board of Directors be expected to come to any other conclusion besides a decision to impose on certificant Terms and Conditions that are favorable to limiting the organization’s liability exposure? And with the current board-level focus on AGRA – Awareness, Growth, Recognition & Regulation, and Authority – virtually all of recent changes fit within the category of the CFP Board’s push for growth. And while we don’t know what initiatives have been voted down amongst the board of directors, it is nonetheless striking that anytime a controversial position is taken by the board of directors that pits the current standards and organizational scope against opportunities for potential growth and expansion, the board of directors has continued to vote in favor of growth and mission creep over holding the line on current standards and current organizational size and focus.

Yet in the end, while even I would argue that long-term growth of the CFP marks is important for seeing the CFP marks ultimately enshrined in supporting regulation, the CFP Board’s paternalistic “our Board of Directors always knows best” approach to governance is clearly flawed. It was the board of directors that unilaterally decided to change the Terms and Conditions, only to later roll back at least partial transparency after an outcry on this blog. It was the board’s growth initiative that implicitly sanctioned an effort to collect ‘voluntary dues’ from CFP certificants for its new Center for Financial Planning, despite never asking for CFP stakeholders to buy into the concept in the first place. And it was the board of directors that tried to expand the CFP Board into being a CE provider (with apparently a total ignorance to the fact that the CFP Board itself originated as a spin-off from the College for Financial Planning, in large part because it was being threatened with an anti-trust lawsuit by being the credentialing organization and education provider at the same time!). And these challenges are not new; it was the board of directors, without CFP stakeholder input, that launched the ill-fated “CFP Lite” effort and almost ended out being sued over it (even though in retrospect with the lens of history, it was actually a good idea that was doomed by its poor communication to stakeholders, further emphasizing the importance of the Board of Directors to get CFP certificant buy-in!).

Fortunately, it has at least been demonstrated that when there is enough of an uproar from CFP stakeholders – albeit sometimes after the fact – the CFP Board and its Board of Directors will at least consider making adjustments to or rolling back proposed initiatives. Nonetheless, with membership associations taking positions of deafening silence on key issues, it should not fall to self-organizing CFP stakeholders and select CFP certificants with widely-read blogs to foment a public outry in an attempt to hold the CFP Board accountable on issues where stakeholder input should have been solicited in the first place.

Time To Update CFP Board’s Transparency And Governance Structure?

If CFP stakeholders continue to feel that the standards of the CFP marks are going backwards, and that the board of directors is tone-deaf to the concerns of CFP certificants about the direction of the organization, it’s only a matter of time before building pressure causes the dam to break. What direction that might take is anyone’s guess. Perhaps the CFP vs ChFC war will re-emerge. Or the RFC designation will try to gain traction again. Or maybe a group of dissidents will try to form a new designation, supported by a standards-pushing organization like NAPFA, with even higher standards than the current CFP marks.

Ultimately, I will admit that I believe at this point, trying to stake the financial planning profession on a new or alternative designation would be a significant and harmful step backwards. The CFP marks are our best and most realistic path to establishing a formal minimum standard for financial planner competency, the culmination of a rallying cry for “One Profession, One [Minimum] Designation” that industry luminary P. Kemp Fain put forth nearly 30 years ago.

Nonetheless, if the CFP Board itself wants to achieve this outcome – as the board of directors’ AGRA initiative appears to be building towards – it’s crucial for the CFP Board to recognize its changing role and evolving relationship with its CFP stakeholders and the financial planning profession. The larger the CFP Board gets, the more power and control it has over CFP stakeholders. But the more power and control the organization gains, the more it must share that power back to the CFP certificants themselves, or risk de-legitimizing its own authority and inviting a competitor – a fundamental tension that any organization faces in leading and overseeing a (professional or other) community.

As a starting point, some initial changes that the CFP Board’s Board of Directors should consider include:

1) Bring Back Public Comments. The failure of the CFP Board to have a single public comment period in nearly 4 years, since it first “lost” a proposal, is a serious issue of stakeholder accountability. While the CFP Board has already announced that there will likely be a public comment period this fall regarding the looming updates to the Standards of Professional Conduct, it’s not enough for the organization to just selectively offer public comment periods on some issues (where it believes public comments will work in its favor) and not others (where stakeholders might object to the proposal). The public comment process needs to be reinstated, in a consistent manner, with clear criteria about what does – and does not – go into a public comment period, especially given recent inconsistencies (e.g., where the Capstone proposal was affirmed in public comment but its elimination for challengers was not, or where the introduction of the 2-year apprenticeship option for the CFP experience requirement was affirmed in public comment but the change to what constitutes “experience” was not).

2) Make Proposed Rulemaking And Public Comments Actually Public. The CFP Board needs to create a clearly identified location on its website, where all proposals can be found, and which actually includes links to the public comments, along with the final outcomes of the rules. The SEC has a dedicated section on its website with an entire “Rulemaking Index” of proposed rules, final rules, and supporting public comments (either already made regarding a final rule, or guidance on how comments can be submitted for a still-proposed rule). Similarly, the Department of Labor has a dedicated Rulemaking section, and a publicly accessible central database of all Public Comments issued on all proposed rules. These organizations conduct very public and stakeholder-engaged processes to change their rules and regulations, in recognition that doing so is essential to legitimize their authority. By contrast, CFP Board’s rulemaking proposals cannot be found in any central location, and virtually none of the public comments submitted on any rule in the past 10 years are actually public (e.g., despite the CFP Board’s claim that 85% of the public comments to the proposed increase in CE hours were negative, those comments were never actually shared with the public).

3) Narrow The Scope Of Mandatory Arbitration In The Terms and Conditions. The original case made by CFP Board staff to justify the new mandatory arbitration clause in the Terms and Conditions was that it could provide a means for unhappy certificants who “lost” a case to the Disciplinary and Ethics Commission, and the CFP Board’s internal Appeals Process, to have a final (non-CFP-Board) venue to make their case… in a manner less costly than the toll that the Camarda case has clearly taken on the CFP Board. And to that extent, the changes to the Terms and Conditions seem reasonable. However, the current changes to the Terms and Conditions, even with the recent acquiescence to provide transparency on outcomes, still does not justify why any and all disputes that any CFP certificant will ever have, should be bound to mandatory arbitration. Other bona fide regulatory agencies allow for the reality that stakeholders have the right to sue – thus why the Department of Labor is being sued over its fiduciary rule (and while I hope the Department of Labor wins, I’ll readily defend the right of the fiduciary opponents to have their day in court), and let’s not forget that a decade ago it was the FPA that sued the Securities and Exchange Commission in a breakthrough case for advancing the fiduciary rule as well. And at least the threat of a lawsuit was rumored to be a key factor in the CFP Board’s rollback of its unpopular CFP Lite proposal, and it was the threat of a lawsuit that originated the CFP Board as a spin-off from the College for Financial Planning in the first place. Simply put, the U.S. legal system is a fundamental layer of organizational accountability, including and especially for organizations that have a professional oversight or regulatory role. While again the acquiescence for greater transparency of mandatory arbitration outcomes is a positive, for the CFP Board to unilaterally strip away the right of CFP certificants to hold the CFP Board accountable in court if it runs astray is a deeply concerning decision by the current Board of Directors.

4) Revisit The Carver Governance Model And Board Selection Process. It is the nature of boards and leaders in virtually all industries and fields to rarely ever surrender any of their power. Nonetheless, the CFP Board needs to recognize the transition it is in the midst of, from merely being a 501(c)(3) entity that promotes a CFP certification trademark, to the anchor certification of a profession where the CFP Board has not only the power to grant the marks, but also to rescind them, and to publicly discipline stakeholders for failing to adhere to its Standards of Professional Conduct. It’s worth recognizing that the Carver governance model that the CFP Board’s board of directors uses to direct and oversee its CEO, and their board selection process predicated on existing members selecting their successors with no process for stakeholders to vote or give input, may well have helped the organization to grow and succeed over its first 30 years; but is this still the appropriate model for governance and stakeholder accountability given where the CFP Board and the CFP marks seem to be heading over the next 30 years?

There will undoubtedly be some naysayers who may use this discussion as an excuse to pile on to whether it’s time to abandon the CFP marks and the CFP Board, or call for Keller's resignation. But ultimately, I'm not convinced that this is the time for that kind of change. As noted earlier, the growth of and public acceptance of the CFP marks means they’re still the best path for financial planning to become a bona fide profession, and while Keller has made missteps (including many discussed on this blog), his success in growing awareness and adoption of the CFP marks amidst a difficult time for financial advisors is notable.

However, the ongoing rise of the CFP marks still means that it's time for the CFP Board to (re-)consider its future role, and the evolving nature of how it must engage CFP certificants as stakeholders. Is the CFP Board's Board of Directors and its executive leadership ready to make the changes necessary to maintain its authority and legitimacy in the coming years?

So what do you think? Are the CFP marks still the right path for the financial planning profession? Do you think the CFP Board is already doing a good enough job of listening to CFP certificants and gaining input from stakeholders? What changes do you think the CFP Board leadership needs to consider? Please share your thoughts in the comments below!