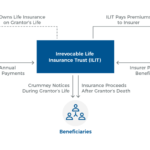

The Irrevocable Life Insurance Trust (ILIT) has long been a staple of estate planning – a means of avoiding the death benefit of a life insurance policy from being subject to estate taxes by having it owned not by the insured or family themselves, but an independent third-party trust holding the life insurance for the family’s (beneficiary’s) benefit instead. Which was necessary in a world where, as recently as 10-20 years ago, even basic term insurance for a 30-something-year-old breadwinner to protect the children in the event of an untimely death could cause an estate tax liability.

But the drastic increase in the estate tax exemption, especially with last year’s doubling to $11.2M (or $22.4M for a married couple with portability) under the Tax Cuts and Jobs Act of 2017, has not only removed more than 99% of households from Federal estate tax exposure, but has rendered a large number of existing ILITs unnecessary for families who once had an “estate tax problem” in the past (when exemptions were lower) but won’t be in any foreseeable future.

And the good news is that despite the “irrevocable” label in its name, in many cases it is possible to either “rescue” life insurance out of an ILIT that’s no longer needed, or to unwind the ILIT altogether. In some cases, it may be as straightforward as the grantor simply substituting the life insurance policy out of the ILIT in exchange for cash of equivalent value (or alternatively buying the policy back). In other scenarios, if the life insurance itself is no longer needed, it may be easiest to simply let it lapse, rendering the ILIT irrelevant because it would no longer have any assets left to oversee. And if the life insurance policy has cash value, it can simply be surrendered or sold in a life settlement transaction, with the cash potentially distributed to beneficiaries (at least if the trustee has discretion to do so). Alternatively, if the beneficiaries themselves want to keep the policy, it may be feasible to distribute the policy in-kind under the trustee’s discretion, or to terminate the trust outright (either under the terms of the trust, as a consent termination of the grantor and beneficiaries, or court-directed termination at the direction of the beneficiaries).

Of course, the caveat is that the trustee must still honor the terms of the trust, and if the trust is more restrictive in preventing various “unwinding” or policy rescue options, the parties are still bound by the terms of the trust (unless, perhaps, the ILIT can be decanted to a new trust under state law). Nonetheless, the fact remains that while the “irrevocable” nature of an ILIT means the terms of the trust itself cannot be changed, that doesn’t mean the grantor, beneficiaries, and trustee can’t work within the terms of the trust and state law to eliminate an ILIT that is no longer necessary in today’s estate tax environment!