Executive Summary

The benefits of reducing current tax liabilities through tax loss harvesting are widely acknowledged - so much, that the IRS developed the 30-day "wash sale" rules to prevent taxpayers from abusing the strategy. Yet less widely understood is that there's one crucial caveat to tax loss harvesting - that taking advantage of the loss also reduces the cost basis of the investment, potentially exposing the taxpayer to a gain in the future that can wipe out some, most, or all of the tax benefit, and in the extreme with today's four capital gains tax brackets actually drive up future tax rates and leave the investor worse off than having done nothing at all.

Notwithstanding these issues, many investors and advisors continue to overstate the benefits of tax loss harvesting, and now "robo-advisor" Wealthfront is doing so as well, with its "Tax-Loss Harvesting White Paper" that purports Wealthfront can increase an investor's wealth by an extra 1%/year, annualized, indefinitely, through its daily tax loss harvesting strategy. Unfortunately, though, the reality is that in a review of its strategy, Wealthfront - like so many others - is confusing tax savings with tax deferral, and in the process may be drastically overstating its benefits by a factor of 10:1, and for its typical investor the true annual benefit may be a mere 1/25th of what their "white paper" claims purport.

Again, this is not to say that tax-loss harvesting is useless, and in reality while many advisors have been automating tax-loss harvesting just like the robo-advisors for almost a decade, Wealthfront's particular tools to implement loss harvesting are unique, especially in how it is able to quasi-pool investor assets to drive the transaction costs down to nothing for its clients (facilitating tax loss harvesting at very small thresholds on a nearly continuous basis!). Nonetheless, the flaws of the Wealthfront tax-loss harvesting white paper also provide a clear example of the problems with trying to come up with a generalized algorithm for an individual's specific and unique tax circumstances, and overall provides an unfortunate case study in how not to calculate tax alpha and try to apply its benefits for a wide range of clientele.

What Is Tax Alpha

The concept of measuring "tax alpha" - or the value of executing good tax strategy - is not new. In the context of portfolios, we can attribute tax alpha to several strategies, including good asset location, as well as the benefits of tax loss harvesting. So-called "robo-advisor" Wealthfront executes automated tax loss harvesting as a key value proposition, and here's how Wealthfront defines the tax alpha associated with its strategy:

TaxAlpha = (STCL * STTR + LTCL * LTTR) / PortfolioBeginningBalanceDefinitions:

STCL is the short-term net capital loss realized

STTR is the combined Federal and California state short-term capital gain tax rate. We [Wealthfront] use the maximum federal marginal tax rate of 43.4% (39.6% + 3.8% for tax payers who earn in excess of $200,000) and the maximum California tax rate of 13.3.%

LTCL is the long-term net capital loss realized

LTTR is the combined Federal and California state long-term capital gain tax rate. We [Wealthfront] use the maximum federal tax rate of 23.8% (20% + 3.8% for tax payers who earn in excess $200,000) and the maximum California tax rate of 13.3%

PortfolioBeginningBalance is the value of the portfolio at the beginning of each year

For example, imagine someone bought an investment for $100,000 and it declined by 15% to $15,000. If this is a long-term capital loss, the LTCL is $15,000. Given Wealthfront's 23.8% (Federal) + 13.3% (state) = 37.1% assumed tax rate (LTTR = 37.1%), this results in a tax savings of 37.1% x $15,000 = $5,565. Given a starting balance of $100,000, then $5,565 / $100,000 = a tax alpha of ~5.6%. In other words, the amount of (in this case, long-term capital gains) taxes avoided in the current year is ~5.6% of the original account balance.

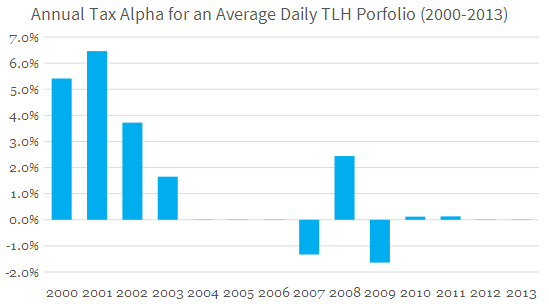

Given this framework, Wealthfront has produced a hypothetical backtest of how their daily tax-loss harvesting strategy would have fared since the start of the year 2000. Their illustration assumes a $100,000 starting investment, plus $10,000 per quarter of ongoing contributions. Tax loss opportunities were harvested in accordance with the wash sale rules, where an alternative security was bought for 30 days before switching back to the original (which in some cases produced a short-term gain during the 30-day period). Losses were harvested based on a threshold mechanism that required them to be large enough that the loss wouldn't likely be entirely recovered within a 30-day period (as that would effectively convert an entire long-term loss into a short-term gain when switching back to the original investment), which means a declining investment might be harvested for losses several times as it declines (at lower and lower price points for small incremental losses along the way). Transaction costs appear to have been ignored (ostensibly because Wealthfront can actually implement its trades with any separate transaction costs to its clientele). The results of Wealthfront's backtest in terms of Annual Tax Alpha as reported in its own white paper are shown below:

Not surprisingly, the results show that the bulk of tax loss harvesting benefits come during bear markets, as that's when the majority of losses occur. While some small losses might occur amongst the various asset classes in the midst of a bull market, those losses are generally absorbed by ongoing rebalancing (which triggers at least modest gains to net against losses), so all of the tax alpha comes from partial- or full-year market declines in 2000, 2001, 2002, 2003, and 2008. Notably, the tax alpha is actually negative in 2007 (rebalancing triggered gains and there were no losses left to offset them) and also in 2009 (the market rebounded so quickly that some long-term losses actually were converted into short-term gains, and they show up in different tax years because the losses got harvested at the end of 2008 and the switchback gains landed in early 2009).

Over the entire time period, Wealthfront notes that the average annual tax alpha was 1.14%, through the combination of big good years, some neutral years, and a pair of bad years (although it appears they calculated the mean annual tax alpha, rather than properly calculating the annualized tax alpha, which would have been slightly lower given the volatility, just as the average return of +50% and -33% is 8.5% but the annualized return is 0% because you actually finish with the same dollar amount you started with).

The Problem With [Wealthfront] Tax Alpha

Certainly, taking advantage of tax loss harvesting and the deductions it brings has value. The problem with tax alpha - at least after a review of the way that Wealthfront is calculating it - is that it fails to capture one key issue: the fact that when a loss is harvested, the cost basis of the investment is reset, downwards, which creates greater exposure for capital gains in the future, and means the tax alpha value of capital loss harvesting is being overvalued.

For instance, going back to the earlier example, the investment had declined from $100,000 down to $85,000, resulting in a $15,000 loss, $5,565 of tax savings, and a 5.6% tax alpha. However, going forward this investment now has a cost basis of $85,000 - since the loss was harvested - which means in the future, if/when/as it recovers back to $100,000, there will be a $15,000 gain. At the same 37.1% tax bracket, that results in a $5,565 tax liability, and a negative tax alpha of -5.6%! The net result? The investment is once again worth $100,000, for a total gain/loss of 0%, and the positive 5.6% and negative -5.6% tax alphas cancel each other out entirely. This assumes, of course, that the investment does in fact recover, and is in fact sold at the end. (While appreciated securities can be donated to avoid capital gains, and/or those who buy and hold to the end of life can receive a step-up in basis, given that Wealthfront's clientele are millenials who someday wish to retire, it seems far more likely that as a baseline assumption, investments will be sold for retirement or other spending purposes, or that gains will be recognized through rebalancing, long before these clients donate it all away or die sometime around the end of this century!)

The reality that harvesting losses produces subsequent gains of an offsetting and matching amount, though, presents the first major problem with the Wealthfront analysis; after systematically harvesting losses throughout the time horizon, they fail to account for the huge embedded gain that would be present by the end - especially given the massive bull run in equities since the trough in 2009. Since that time, the S&P 500 is up well over 100%, but Wealthfront only reported the positive tax alpha from the loss harvesting and conveniently fails to acknowledge the huge negative tax alpha embedded in the investments at the end of the time horizon! If the cost basis had really been reset all the way down at the market bottom through daily tax loss harvesting, a gain of 100%+ at their 37.1% tax rate assumptions means there's a -37% tax alpha looming at the end of this chart. Ironically, this much negative tax alpha would actually obliterate the entire value over the time horizon (technically it could actually be worse, as the cumulative tax alpha may well turn out to be negative, given the ongoing systematic investments since 2009 have only net gains and no prior losses to recognize!)! Of course, this reality that the negative tax alpha at the end will offset the positive tax alpha earlier reported is simply a mathematical reality, but one that Wealthfront's methodology implicitly ignores by not adjusting for a growing level of embedded capital gains at the end of the time horizon.

True Value Of Tax Loss Harvesting

To be fair, though, this doesn't mean all is lost for tax loss harvesting. Notwithstanding the flawed Wealthfront tax alpha analysis, there is a value to tax loss harvesting. It's the value of keeping those extra tax dollars that would have gone to Uncle Sam to stay in our pocket (or really, in our portfolio) in the meantime. That still has some true economic value.

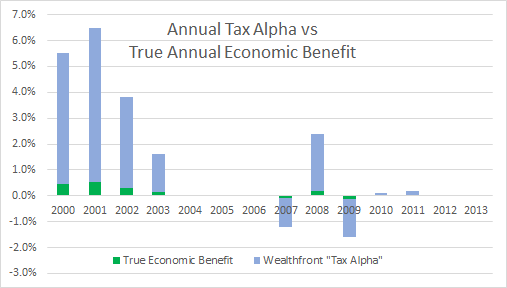

For instance, continuing the earlier example, the $15,000 loss resulted in $5,565 of tax savings that could remain invested. Assuming an 8% growth rate, that $5,565 that remained invested would have produced an extra $445.20 of growth. Relative to the original $100,000 investment, this means the true annual economic benefit of tax deferral - essentially, the "time value of money" of having those tax dollars invested on your behalf and paying the bill later - was $445.20 / $100,000 = 0.45%. At least, for the year where a big loss occurred (producing the big tax deduction and tax savings to keep invested). The chart below recreates the Wealthfront "tax alpha" in blue, and then in green shows the true annual economic benefit that the Wealthfront "tax alpha" would have produced, assuming an 8% growth rate on the dollar amount of tax savings (but recognizing the tax savings itself will be repaid in the future when the investment recovers).

In case you're having trouble seeing the "green" parts of the chart that represent the true economic benefit of the tax deferral, you should. They're tiny green bars. Almost by definition, the height of each green bar representing the true economic benefit is 8%, or 1/12th of the blue bar symbolizing tax alpha. Which means that while Wealthfront was claiming an average annual tax alpha of 1.14%, the true economic value of their strategy was closer to 8% of that 1.14%, which is about 0.09%. Or stated another way, Wealthfront was overstating the true economic value of their tax loss harvesting by a factor of about 12:1.

To be fair, it's worth noting that over a 13-year time horizon, this framing will slightly understate the cumulative value of systematic tax loss harvesting, because the harvesting benefits at the beginning do compound over the whole time period (and "fortunately" for the Wealthfront backtest, there are big tax losses to harvest with the tech crash at the beginning, though I'm sure it's no coincidence that Wealthfront chose the peak of the tech bubble as a starting point for their illustration). Of course, the reality is that compounding a 0.09% tax savings won't amount to all that much, and it's even less given that their example assumes ongoing contributions (with a $100,000 starting balance and $520,000 of cumulative contributions dollar-cost-averaged into the market over the span of 13 years, that $445.20 economic value of tax savings just doesn't compound enough to be all that much more material).

On the other hand, while compounding means that just looking at the true one-year economic benefit of tax loss harvesting will slightly understand the compounding cumulative benefits of tax deferral - once properly calculated at about 1/12th the value that Wealthfront claims! - there are also several issues that may still be causing Wealthfront to systematically overstate the realistic value of tax loss harvesting for most [of its] investors.

Further Complications To The Value Of Tax Loss Harvesting

The first additional concern regarding the value of tax loss harvesting emerges with a review of Wealthfront's tax assumptions themselves. To amplify the value of tax deferral, Wealthfront assumes an investor facing the maximum Federal income tax rates, along with living in California with the highest state income tax rate. This is how they reach a whopping 37.1% long-term capital gains assumption.

However, the reality is that in order to reach the top Federal income tax bracket - where the top capital gains rates apply - the investor must have taxable income (that's after all deductions) of $405,100 in 2014 (or $457,600 for a married couple, and a married couple needs more than a million of income to hit the top California bracket as well!). Given that Wealthfront recently announced they had crossed half a billion of AUM and were up to $538M with 6,000+ clients, some simple napkin math shows that their average investor has around $90,000 of total assets with them. Only 16% of Wealthfront clients even have reported a liquid net worth over $1,000,000, and 58% of Wealthfront clientele are Millenials aged 18 to 35. To say the least, it seems unlikely that the average client being a 20- or 30-something with $90,000 of investments is really staring down annual taxable income in excess of $400,000 to be subject to the top Federal tax rate (and it's over $500,000 to hit the top California rate, or $1,000,000 as a married couple to hit that top bracket!). Granted, Wealthfront does have a techie-centric presumably-high-income professional clientele, and one recent survey indicated the average Silicon Valley software engineer is starting at $165k, but the actual capital gains tax rate for someone at that income level is 15% (and the California rate is only 9.3%, for a total capital gains tax rate of 24.3%).

Unfortunately, though, using a more realistic 24.3% tax rate instead of 37.1% cuts the tax loss harvesting benefit by about 1/3rd, from 0.09% of true economic benefit down to only about 0.06% of annual economic value. And if the investor actually lives in Texas, Nevada, Florida, or some other state without a state income tax, where the capital gains rate is 'just' the Federal 15% with no state income tax? Now the true annual economic benefit of tax loss harvesting is down to an average of about 0.04%, or about 1/25th the value that Wealthfront states in its white paper.

In turn, even that benefit assumes that when a loss occurs, it can actually be used for tax purposes. After all, the capital loss rules limit the deduction to only apply against capital gains (with a small $3,000 ordinary loss for any excess that doesn't amount to much when Wealthfront assumes its typical client earns more than half a million dollars annually!). Thus, given that Wealthfront started its example in 2000, there would be no gains to offset at that time, and the bulk of the losses would actually just manifest as loss carryforwards that wouldn't actually start getting used until rebalancing trades began to trigger material gains in 2004 and beyond. So even when acknowledging the compounding benefit of the tax deferral value, the clock for losses harvested during the tech wreck wouldn't have begun until several years later; in other words, the blue bars in the 2000-2003 time frame should mostly be appearing in 2004-2006 or so, allowing less time for the economic value to compound at all. Of course, a tiny portion of the losses would have been deductible at ordinary income rates, but at the more-realistically-Wealthfront-typical $165k of income the individual's ordinary income bracket would have only been 28% + 9.3% = 37.3% (which means what Wealthfront was assuming for capital losses in the first place should actually have been the ordinary income rate!), and the tax alpha would have been $3,000 x 37.3% = $1,119 or 1.1% calculated Wealthfront's way (assuming the first year where the account balance was still only $100,000 and there weren't more contributions), which again is only about 0.09% when adjusted to account for the true economic benefit of tax deferral at an 8% growth rate.

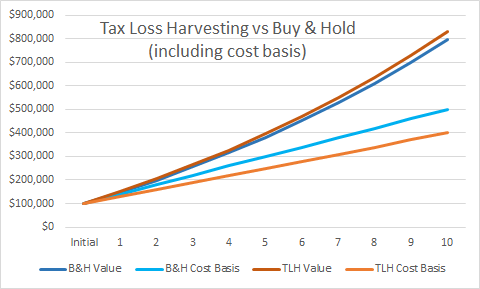

Another complication of the Wealthfront approach is that systematic loss harvesting can actually create an even more unfavorable result by creating a large deferred tax liability for the future. For a simplified example, assume a scenario where the investor takes a $10,000 loss on a $100,000 portfolio, and with ongoing $40,000/year contributions actually manages to continue to find $10,000 of "temporary" losses to harvest from the portfolio each and every year. For our Wealthfront engineer client facing a 24.3% capital gains rate, this produces $2,430 of tax savings each year (Wealthfront would characterize this as a 2.4% tax alpha). However, if this was done systematically for a decade, by the end of the decade the cost basis through loss harvesting has been so whittled down that there is now an extra $100,000 capital gain looming, as shown below assuming $100k starting balance, $40k end-of-year annual contributions, and 8%/year growth (B&H is for buy-and-hold, TLH assumes annual $10,000 losses being harvested):

As the chart above shows, while the value of the TLH strategy is slightly higher than the value of the B&H scenario, the cost basis of the TLH strategy is materially lower than the B&H scenario, which in turn will chop away most (though not quite all) of what little excess there is for the TLH strategy over just buying and holding. In other words, at the end of the chart, the TLH client is exposed to an extra $100,000 of looming capital gains above and beyond what the B&H investor faces.

Yet the caveat is that in our engineer's situation, the outcome actually is worse, because at his $165k income, liquidating an extra $100,000 of capital gains can actually drive his capital gains rate up, pushing him over the line of the 3.8% Medicare surtax on investment income. As a result, while the engineer was saving $2,430 x 10 = $24,300 in taxes over the decade, liquidating them at 24.3% + 3.8% = 28.1% is a tax liability of $28,100. In other words, the investor is $24,300 (savings) - $28,100 (final taxes) = -$3,800 of taxes in the hole because of this "negative tax arbitrage" effect, where systematic loss harvesting produces such large future gains that it actually drives up the future tax bracket, resulting in less wealth through tax loss harvesting.

The effect can be even worse for lower income investors (e.g., those Wealthfront participants who perhaps aren't at the Silicon-Valley-engineer salary level). For married couples whose taxable income after all deductions is below $73,800 (in 2014), the long-term capital gains tax rate is actually 0%! Which means systematic loss harvesting produces a tax savings of... nothing. At all. The tax alpha is zero. You can't get an economic benefit from tax deferral when there is no tax liability to defer! Except it does reduce cost basis, increasing exposure to gains in the future, and potentially turning 0% capital losses into 15%+ capital gains, resulting in a significant destruction of wealth! In such scenarios, the wealth creation strategy is actually not automated loss harvesting at all, but harvesting gains instead.

More broadly, the simple reality is that capital gains tax planning is far more complex than just always harvesting losses to attempt to defer a tax liability, given our current progressive four bracket capital gains tax structure with the new top bracket and the 3.8% Medicare surtax where pushing too many gains out to the future actually leads to a higher tax bracket when they're actually liquidated, and those eligible for 0% rates should actually be harvesting gains to take advantage of their "free" annual step-up in basis!

Overstating Tax Benefits As An Investment Value Proposition

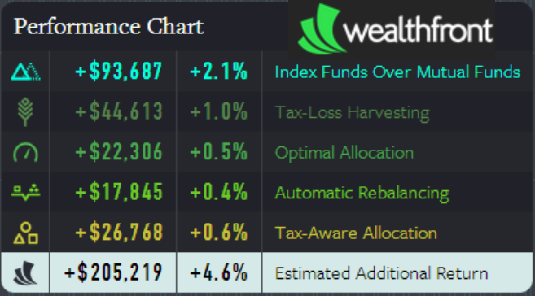

While simply overstating the value of tax deferral in a white paper is one thing, the concern in the context of Wealthfront is that they convert their overstated tax alpha benefit into an actual wealth compounding factor. For instance, the chart below from their website shows an investor who has $52k of greater wealth due to a 0.93% additional compound growth rate on investments due to "tax alpha" for capital loss harvesting - i.e., they literally project future wealth to grow at an extra 0.93%/year of annual return based on their estimated tax alpha.

However, the problem, as we now know, is that they are failing to disclose that the red line in the chart below - the greater value due to systematic loss harvesting - would have a substantially lower cost basis than the blue line and a much larger embedded capital gain that would wipe out virtually all of the differential, as already shown in the figure earlier (in other words, the Wealthfront illustration below only shows the gross value of the two lines and not the different cost bases and significantly different embedded tax liabilities associated with each). And of course, this also ignores the fact that as previously shown, the true economic return differential isn't ~1% of tax alpha in the first place, but closer to 0.09% instead (which is the outcome once the fact that the two lines have substantially different cost bases is accounted for).

Similarly, the Wealthfront home page explains their economic value as shown below, again implying an additional average annual growth rate of 1.0% attributable to tax loss harvesting, even though the true economic value should be no more than a fraction of that even at top tax brackets, and even less for what Wealthfront itself proclaims is their "typical" investor - a millenial engineer who has $90,000 invested with them... and isn't likely facing a marginal tax anywhere rate near the top tax brackets. And of course, that assumes the investor is using a taxable account in the first place, and not a retirement account where the built-in tax deferral means there is no value to tax-loss harvesting (though Weatlhfront's charts do not exactly make it clear that the benefits apply exclusively to brokerage accounts).

In addition to all these concerns, there's also the simple fact that the Wealthfront tax loss harvesting alpha is even further overstated by their choice of time horizons for their hypothetical back test. As their own charts show, the bulk of tax loss harvesting value is created in the midst of significant bear markets, while no tax alpha is produced in bull markets (and in fact the tax alpha can even be negative as rebalancing trades trigger capital gains recognition in the midst of an extended bull market with no available losses to harvest). Thus, Wealthfront's backtest starting point of the year 2000 is notable. Had they backed it up to start in the early 1990s instead, nearly doubling the length of the time period but with a long bull market that would have produced negative tax alpha for a decade and few opportunities to produce positive tax alpha, that alone would have cut their annual tax alpha by as much as 50% (as the same benefits from two bear markets would have been averaged over twice as many years), dropping it to little more than 0.50% and the true economic value (still assuming an 8% growth rate) to only about 0.05% (or no more than 0.02% or 0.03% per year with more realistic tax bracket assumptions). Notwithstanding their cherry-picked time horizon, it's also notable that on a net basis, even with their approach and favorably-chosen time period, the tax loss harvesting strategy has actually produced virtually no "tax alpha" since 2004, as the one positive year in the past decade - 2008 - was entirely offset by the negative tax alpha in 2007 and 2009 (because their rebalancing slowly started to force them to recognize some, but still not all, of the giant embedded tax liability their strategy is creating).

In the end, it's worth noting that none of this is meant to suggest that tax loss harvesting is a bad thing to do. With the exception of doing it so extensively that it drives up future tax brackets - or for those who are currently eligible for 0% capital gains rates - it does have some value, especially if it can be implemented systematically and inexpensively (as many advisors have already been doing for a decade on an automated basis with rebalancing software like iRebal and long before that with "manual" spreadsheets). And frankly, Wealthfront's tax loss harvesting capabilities are unique, in that their platform allows daily tax-loss harvesting to be executed without any net transaction costs to investors, a substantial difference from advisors where even low transaction costs do increase the friction of implementing loss harvesting strategies.

Nonetheless, the loss harvesting value must be measured on the basis of the true economic benefit, not the gross tax savings as a misrepresentative form of "tax alpha", should be done with realistic tax assumptions for the client (and not overstated with tax assumptions that clearly exceed what is known to be the average client), and especially should not be converted into an annual return that's assumed to compound for 20 years without accurately characterizing the tax results throughout the time horizon or at the end in the form of the growing embedded gain that the strategy creates.

Where Does Wealthfront Go From Here?

To be fair, the problem of overstating the benefits of tax loss harvesting and tax deferral is not unique to Wealthfront; there are many advisors who do the same thing, which is why this blog includes many cautionary posts that capital loss harvesting may be overvalued. Which means this review of the issues with Wealthfront's tax loss harvesting white paper is far more a case study of the problem than the sole instance of it.

Nonetheless, one might expect that a technology company which is built on the basis of having savvy mathematical algorithms control your portfolio would know how to do the arithmetic of tax and cost basis calculations properly, yet this error has remained in their tax loss harvesting white paper for nearly a year. Perhaps this is the problem with trying to build an "online financial advisor" platform with savvy tax strategies using only an Investment Team and sharp engineers but without actually having a CFP or CPA in a high-level advisory or leadership position? And lest anyone think this is just picking on a robo-advisor out of the blue, it's worth noting that I've pointed this issue out to the Wealthfront leadership repeatedly over the past year to give them a chance to fix it, yet the issue has remained unaddressed and unresolved.

.@adamnash Reasons value of tax loss harvesting is limited & risky, that your white paper doesn't cover: http://t.co/VuUUn0XMha @ddjanowski

— MichaelKitces (@MichaelKitces) May 24, 2013

And then again later last year after an article by Felix Salmon that inappropriately extolled their overvalued tax alpha calculations:

@adamnash Tax loss harvesting is relevant & has value. But looks like your calc methodology overstates it >10:1. @felixsalmon @Wealthfront

— MichaelKitces (@MichaelKitces) December 10, 2013

Of course, the reality is that Wealthfront can fix this issue, and hopefully will do so sooner rather than later for their own sake (as Ray Lucia found, misstating the projected investment returns of your strategies due to a faulty backtesting white paper can get you banned by the SEC!). And "fixing" the issue of misstating tax loss harvesting benefits will not completely undermine the Wealthfront value proposition, both because their particular no-transaction-cost implementation of loss harvesting is unique, and because as noted above they claim to deliver other benefits as well (though ironically, those Wealthfront benefits almost perfectly mirror the advisor benefits researched by Morningstar's David Blanchett as "advisor Gamma"!).

From a broader perspective, the fact that Wealthfront has been drastically overstating the value of its tax harvesting strategy doesn't make the presence of such "robo-advisors" irrelevant. In fact, I've repeatedly noted that robo-advisors like Wealthfront, along with its similar counterpart Betterment, are steadily commoditizing the core construction of a passive, strategic portfolio for investors, which is a genuine cost-reduction value for consumers and will force advisors to continue to evolve to a more genuinely-personal-advice-centric value proposition. And while the reality is that many advisors have been doing this with their own software for nearly a decade already - no matter what the robo-advisors claim, their implementation of these strategies using technology is not new nor unique - the 'robo-advisors' are finding ways to potentially make it even more efficient, especially through their quasi-pooled investment structures that are allowing them to execute transactions for clients without needing to apply any separate/additional transaction costs (how they actually do this is a conversation for another day).

Yet at the same time, this entire exercise illustrates perhaps the greatest weakness of Wealthfront: that developing broad-based algorithms for investment purposes can miss out on the nuances of individual tax planning - an entirely different core competency that must be integrated into the picture, as advisors routinely do and "robo-advisors" are still struggling to do. The situation is especially true given that Wealthfront will harvest losses for all clients on an ongoing basis, regardless of the fact that for some doing so will eventually drive them into a higher tax bracket and destroy wealth, while for others it should not be done at all because they're young and in the lower tax brackets and eligible for 0% capital gains rates and consequently harvesting gains is the best strategy for them. These are the exact kinds of nuances that good advisors can address when doing client-specific personalized financial advice that is beyond at least today's algorithm-based robo-advisors broad-sweeping investment implementation. In other words, Wealthfront's failings in this regard demonstrate exactly why some investors that need more individually-suited tax-sensitive advice must be cautious of a robo-advisor that looks solely at investments and fails to take into account the whole personal financial planning picture.

But who knows, perhaps this article will just propel Wealthfront forward to improve their offering, and bring even more attention to them, because there's no such thing as bad press, right?

So what do you think? Have you ever made the 'error' of overstating the benefits of tax loss harvesting by focusing on the immediate tax savings rather than the more limited value of tax deferral? Is it appropriate to state the annual tax savings of loss harvesting as an outright return enhancement? Given that advisors can and do implement loss harvesting their technology as well, should advisors be more actively claiming the benefits of tax loss harvesting as something they bring to the table as well (once calculated properly!)?

Disclosure: In addition to being a partner with Pinnacle Advisory Group, a private wealth management firm, Michael Kitces works on a consulting basis with companies in the financial services industry looking to serve advisors, and has consulted in the past with Betterment (commonly viewed as a competitor to Wealthfront).

Stupid question from a layman… The TLH can get me a $3k deduction on ordinary income, but the deferred gain is taxed at capital gains rate, right? So isn’t there is an additional benefit for arbitraging the difference? It seems like your calculations have the gain taxed as ordinary income.

By the way your blog is a great reference, thanks!

Ned,

Yes, you’re correct that the gains are capital, while the $3k deduction can be ordinary income – assuming there are no capital gains from sales or rebalancing, as capital losses must net against capital gains first if available.

This arbitrage effect is definitely a legitimate value for loss harvesting (and one I didn’t specifically calculate separately here), though again it’s only value for those who have no other gains to net against, and some may debate its materiality (the tax rate arbitrage on $3,000 isn’t a huge number for clients whose baseline assumption is $500k+/year of income, though clearly it’s more valuable at more ‘modest’ average levels of income and wealth).

But again, yes it’s definitely a legitimate value for the subset who can take advantage of it. I just don’t know how you’d “know” which clients to do this for on a systemwide basis without evaluating the tax and income circumstances of each client individually. If you take the loss and it nets against ordinary income it’s a win (favorable tax rate arbitrage), but if it nets against 0% capital gains it’s potentially a loss (negative tax rate arbitrage). We do this routinely for some clients, but only because we’re going through a full planning process with them and know exactly which years it’s fruitful and which years it’s not.

– Michael

Thanks for the reply. Makes sense.

Good post Michael, although I will admit the second half kind of went over my head.

I was actually wondering this too though as soon as I saw your ex. Your thinking/ex’s probably apply to most people but I’d say there are quite a few people out there who this would benefit. Think about millennials who are starting early saving, they can max out 401k, hsa, ira, and probably don’t need after-tax investing but if they start dropping money into betterment (I haven’t read much about wealthfront’s tlh but assuming they’re similar) they can now get the 3k arbitrage of ordinary income – ltcg or if they’re really smart since they probably don’t need the money, just use it to donate to charity as they get older or to their heirs with the stepped up basis. That seems like a pretty sweet deal to me, similar to what i do with my rental property.

Laying it out like that makes me even more sure that it’s a good strategy for me, maybe you can prove me wrong 🙂

Michael,

What are your thoughts on the Wealthfront 500 fund? I feel the benefits of this fund are largely overstated as well. The theory is that there is substantial benefit to stock level tax loss harvesting, but in practice is not most of this “tax alpha” generated in major bear markets when the same tax loss harvesting can easily be done at the mutual fund level?

Eric

Eric,

While I’d have concern about whether the benefits of the Wealthfront 500 fund are overstated – in a similar manner to the critiques noted here – I would consider it a more effective way to implement tax-loss harvesting than “just” using an S&P 500 index fund as most investors (and advisors) would traditionally do. To the extent there are loss-harvesting opportunities on the table, have a more granular way of implementing it – per the Wealthfront 500 – is a better way to execute it.

The obvious caveat to this is that it’s only more valuable if it can be executed in a manner where the transaction costs don’t erode much/some/all of the value, but I believe Wealthfront absorbs all the trading costs for their implementation of the strategy.

So in that regard, I really would view Wealthfront 500 as a valuable – and uniquely valuable – form of tax-loss harvesting that Wealthfront implements (that advisors can’t), and was part of the feature set I was alluding to in my comment in the blog that Wealthfront’s tax-loss harvesting capabilities are unique.

Again, important not to overstate the value, but I definitely DO view their Wealthfront 500 strategy is legitimate (and unique) value.

– Michael

I agree that the value of the tax alpha is overstated but Wealthfront has come up with a better way of tax-loss harvesting for a fraction of the fee charged by most advisors. That is a good thing and I wish Wealthfront success!

http://www.cbsnews.com/news/a-tax-friendly-strategy-thats-better-than-indexing/

Allan,

Indeed, I specifically note in the article here that Wealthfront’s tax loss harvesting capabilities are unique, albeit with the value overstated. Their Wealthfront 500 implementation, and the pooled trading capabilities that make it feasible for them to absorb transaction costs to allow for frictionless daily tax-loss harvesting at an individual-stock-level of granularity is something that neither advisors nor mutual funds can fully replicate.

– Michael

Good article , looked at Wealthfront 500 fund thought is was pretty unique for such a low fee but could not figure out on how stocks were picked on day one if they buy 250 stocks and each stock has a mirror to get the other 250 for the tax harvest side. Why is KO picked on day one and not PEP etc and how dividend exposure was calculated so you do not get chopped up missing dividends on both sides or takeovers etc. I think Fidelity does something similar at higher fees.

Good article, Wealthfront 500 fund seems good idea for that fee structure . Fidelity I think does something similar for higher fees. I was unsure how they selected the first 250 stocks and the mirror 250 stocks . On day one which stocks are picked first , KO or PEP?etc and questions of dividend management so you not getting chopped up. Yes tax advantages are overstated would not be surprised if company if company is bought out or absorbed by bigger firm.

Nice analysis, Michael.

As an RIA, one client-specific loss harvesting situation that comes up is tax rate arbitrage, i.e.:

New client has an unrealized long term capital loss that is large in relation to the size of their taxable investment account. (They just couldn’t bear to sell it.)

So advisor sells the position, resulting in a LTCL carryover. Advisor can then make opportunistic short term trades- which would usually be taxable at the client’s ordinary tax rate- to gradually ‘work off’ the large LTL tax carryover over a period of years. The tax arb is the difference between client’s marginal ordinary tax rate and the ordinary rate applied to STCG. [Of course this assumes that the advisor is a good trader :-)]

Alternatively, the client’s taxable account(s) can be positioned passively so that no meaningful CG are realized over the period of the ‘workoff’. In this case the tax arb is between the embedded LTCG rate (which you described in the article) and the client’s current rate on ordinary income.

Basically, $3000/ year of income or STCG gets favorable treatment over the period of the workoff. In some cases I have seen workoff periods of up to ten years. Note: in many cases the clients’ tax CPA fails to advise the client or RIA about the carryover. It’s incumbent on the RIA to suss out the situation during the intake interviews.

Parametric, smart and thoughtful folks though they are, in their separately managed account presentations makes similar assumptions that overstate tax alpha.

I would also note, if I didn’t somehow miss this point above, that there is a distinct possibility of only having long term gains to match against valuable short term losses, which further lower the effectiveness of the strategy.

However, although briefly alluded to above, much of the problems so well inventoried by Michael are resolved if the investor actually leaves the highly appreciated portfolio to heirs with a stepped up basis.

Michael, I’m very much looking forward to learning from you at CPWA class at Booth school next month!.

Michael,

I don’t agree with some of your comments, specifically of the benefit of TLH for people in the 0% LTCG tax bracket. If I have retired clients with TAXABLE income below $73,000 they don’t pay any tax on their capital gains (and Dividends), but if they harvest $3000 in losses against their income from TLH then they save $450 in taxes and MAY not pay any taxes on the capital gains in the future because they are still in the 0% LTCG bracket or step up of basis at death. I do have clients in this situation, retired, large inherited trust with little social security and pension income.

Obviously there are some big errors on this Wealthfront whitepaper outright ignoring the $3000 max loss against income per year but there are certainly advantages for TLH in many cases.

JT,

Certainly taking a loss if there are NO gains, and claiming it against ordinary income, is appealing. However, that at best would only be available opportunistically, not systematically. If portfolios are going up on average, and you’re harvesting losses (creating offsetting gains in the future), at some point the client will run out of loss assets, and then the (larger and potentially higher tax rate) gains start kicking in.

So yes, on a one-off basis there’s value to harvesting a loss when there are NO gains, but if there are NO gains FOREVER and the client’s portfolio is never producing any gains, there are some other problems going on… How many clients are really seeking out investment solutions that have a goal of only losing money and NEVER making money at any point until they die? 🙂

– Michael

Michael,

This is a new client who sold out in 2009 and has a $150k carry forward loss. His portfolio was almost all bonds, purchased in 2010 so he hasn’t used a lot of his losses. Although, in just the past few months of working with him and changing a few things he is realizing some gains. His carry forward loss will be around for a while to be used against his ordinary income.

Are there any other robo-advisors that do a better job of accurately showing the positive impact of tax loss harvesting?

I guess a major benefit of tax loss harvesting is to realize a short term capital loss and convert it to a long term capital gain in the future. The difference in the tax rates is the savings you gain. As stated by JT, if the long term capital gain rate is 0, then all tax loss harvesting savings are real savings.