Executive Summary

Retirement accounts and annuities used as accumulation vehicles can create significant tax-deferred account balances over time, with the caveat that eventually the tax bill must still come due. If the accounts are liquidated during life, the account owner faces the tax consequences; if the accounts are held until death, the tax liability falls to the beneficiaries instead. To help ameliorate the potential for a large liquidation to thrust the beneficiary into higher tax brackets after the death of the owner, Congress created the “stretch” rules for retirement accounts and annuities that allow distributions to be taken in small amounts over the life expectancy of the beneficiary.

However, the rules for stretching an inherited account are more problematic in the case of a trust as the beneficiary, because a trust is not a living breathing human being, and therefore doesn’t have a life expectancy to stretch against! In the case of retirement accounts, the IRS and Treasury have created the “see-through” trust rules that allow post-death required minimum distributions to occur based on the life expectancy of the underlying trust beneficiaries. However, in the case of annuities, no see-through trust rules exist, compelling trusts to instead liquidate inherited annuities over the far-less-favorable 5-year rule!

As a result, consideration of whether to use a trust as the beneficiary of an annuity must weigh the adverse tax consequences against the favorable/desired non-tax provisions of the trust. In some situations, using an annuity’s own beneficiary designation with “restricted payout” may be a viable alternative, saving on both the cost of the trust itself and preserving the stretch. However, in situations where it is most important to limit a beneficiary’s access to a trust – such as irresponsible spendthrifts, asset protection, and estate planning scenarios – there may be little choice but to accept the less favorable tax treatment, at least until/unless the rules change!

Editor's Note: Please see Restructuring Conduit Trust Beneficiaries Of Retirement Accounts To Avoid The SECURE Act’s 10-Year Rule and also Why Discretionary See-Through Trusts May Require Reform After The SECURE Act’s 10-Year Rule for some further thoughts on the trust-as-beneficiary rules in 2020 after the SECURE Act.

Post-Death RMD Stretch Rules For The Beneficiary Of An Inherited (Non-Qualified) Annuity

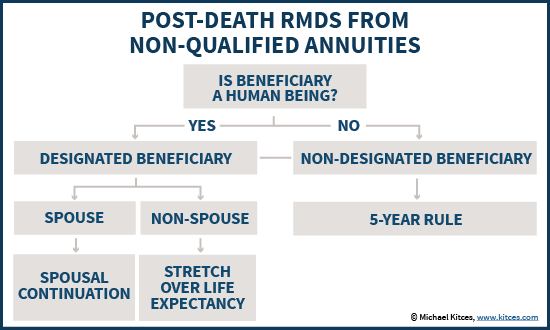

While non-qualified annuities (i.e., those NOT owned in a retirement account) do not subject their owners to required minimum distributions (RMDs) while alive, the beneficiary of an inherited annuity is subject to post-death RMD rules that are very similar to those applicable to retirement accounts. In fact, the rules for post-death RMDs from annuities under IRC Section 72(s) are virtually identical to those for retirement accounts under IRC Section 401(a)(9), where the word “annuity” is simply substituted for the word “retirement account” instead!

Accordingly, beneficiaries of inherited annuities generally have three options for how to take distributions after the death of the original annuity owner (note: because these rules apply after the death of any owner under IRC Section 72(s)(1)(A), they are triggered even if a joint annuity owner is still alive!). Similar to retirement accounts, one set of rules applies if the beneficiary is a “designated” beneficiary (i.e., a living, breathing human being), and another applies if the beneficiary is not an individual (i.e., a “non-designated” beneficiary). Under IRC Section 72(s):

- If the designated beneficiary is a surviving spouse, the beneficiary can continue the contract in his/her own name (known as the “spousal continuation” rule, similar to the spousal rollover of an IRA);

- If the designated beneficiary is a non-spouse (i.e., any other living breathing human being besides the annuity owner’s surviving spouse), the beneficiary can stretch distributions over his/her life expectancy beginning in the year after death; and,

- If the beneficiary is a non-designated beneficiary, the annuity must be liquidated within 5 years of the annuity owner’s death.

Notably, while these rules are substantively similar to retirement accounts, they are not precisely the same, due primarily to the fact that the rules for retirement accounts have been slightly “relaxed” under subsequent Treasury Regulations to make them easier to follow. Thus, for instance, stretching over the life expectancy of a non-spouse designated beneficiary of an IRA requires the first distribution to occur by December 31st of the year after death, while with an annuity it must actually occur within precisely 1 year (i.e., 365 days) of the annuity owner’s death. Similarly, while the Treasury Regulations allow retirement accounts subject to the 5-year to be distributed by December 31st of the 5th year after death, in the case of annuities the tax code is read literally to require the distribution by precisely 5 years after the date of the annuity owner’s death.

On the other hand, when an annuity is held inside a retirement account, the retirement account rules do apply (as they would for all retirement accounts, regardless of whether the account owns an annuity or some other investment asset).

Qualifying A Trust As A Designated Beneficiary Of An Inherited Annuity

In general, a trust is not considered to be a (non-spouse) designated beneficiary, because it is “just” a piece of paper, not a living, breathing individual human being. After all, it would be difficult to “stretch” an inherited retirement account or annuity over the life expectancy of a trust as beneficiary, when a trust isn’t alive to have a life expectancy in the first place!

In the case of retirement accounts, though, Treasury Regulation 1.401(a)(9)-4, Q&A-5 permits trusts to qualify as a designated beneficiary by meeting certain requirements. If the trust is treated as a designated beneficiary, this permits the post-death RMDs to be calculated by looking through the trust to the underlying beneficiaries, and using the life expectancy of the oldest beneficiary to determine the stretch period for the retirement account.

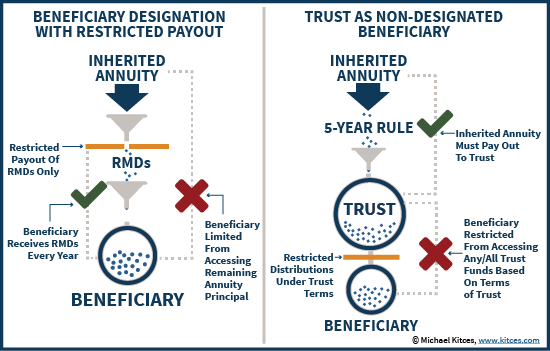

However, annuities have no such regulations defining how to make a “see-through” trust that can qualify as a designated beneficiary. As a result, when a trust is named as the beneficiary of an annuity, it is “stuck” with the 5-year rule as a non-designated beneficiary! (Notably, though, this is about a trust as the beneficiary of an annuity; the consequences of having a trust as the owner of an annuity are entirely different!)

Notably, given the fact that the IRS and Treasury have interpreted the tax code rules pertaining to inherited retirement accounts as permitting (certain) trusts to be treated as designated beneficiaries, in theory the same rules could be applied to inherited annuities as well. Especially since the underlying tax code itself is substantively identical between the two. However, given that no such rules have actually been promulgated yet, most annuity companies will not acquiesce to such treatment, and refuse to do so until/unless new rules are published, and/or a trust-as-beneficiary actually submits a Private Letter Ruling to the IRS requesting such treatment (which hopefully will happen someday, to provide clarity on this issue for everyone!).

Using A Beneficiary Designation With Restricted Payout As A Trust Alternative

Notably, while the tax code does allow an inherited annuity to be stretched (at least for a designated beneficiary), an annuity is still a contract and can be even more restrictive than what the tax code permits. Thus, for instance, some annuities may require all beneficiaries to take under the 5-year rule rather than allowing a stretch, may require that a stretch be accomplished with annuitization but not via systematic withdrawals, or may simply mandate that the contract be liquidated in a single lump sum (not even permitting the funds to be spread out under the 5-year rule).

However, the fact that annuity contracts can have more restricted payout provisions for (designated) beneficiaries can also become a proactive planning strategy, given the less favorable treatment otherwise accorded to trusts as non-designated beneficiaries. In fact, some annuity companies have specifically crafted “beneficiary designation with restricted payout” forms that annuity owners can use to deliberately restrict payouts to beneficiaries after death, a form of “control from the grave” that can be accomplished without using a trust!

Although such restricted payout forms have somewhat limited options – they are not as flexible as trusts – a restricted beneficiary designation might limit the beneficiary to only taking required minimum distributions (but not any more), require the beneficiary to stretch for a specific period of time (e.g., for 20 years or until age 40), or could even split and allow some of the contract to become payable as a lump sum, with the rest required to be paid out over time. Notably, though, in no event can the restricted payout on a beneficiary designation be more restrictive than what the tax code requires in post-death RMDs.

Planning Implications Of The Inability To Stretch An Inherited Annuity Through A Trust

Given that stretch annuity treatment will generally not be available to a trust beneficiary in the current tax environment, post-death and estate planning strategies with an annuity should take into account this fact, especially where a beneficiary designation with restricted payout may be a viable alternative.

Notably, though, the biggest caveat of a restricted payout beneficiary designation is that, to comply with the tax code, the contract must still pay out at least the post-death required minimum distribution every year. As a result, the beneficiary may be restricted from accessing the annuity’s remaining principal, but there will be at least some payments flowing to the beneficiary every year. In many situations where a restriction is necessary, this will simply not be sufficient. For instance, if the beneficiary is an irresponsible spendthrift, this still gives them access to the money (albeit in small pieces over time); if the goal is to shelter the assets from estate taxes, the funds will still distribute over time into the beneficiary’s taxable estate; and if the desire is for asset protection, a known payment stream for life may still be one a creditor could try to collect against. Alternatively, by using a trust as beneficiary, the funds that are required to come out of the annuity can still all be collected by the trust, keeping a barrier between the beneficiary and all of the money, where it is really necessary to do so.

Nonetheless, where the trust is necessary, its benefits must be weighed against the adverse consequences of the trust. The primary negative impact of using a trust is losing the tax-deferral opportunity for a “stretch” of the existing gains embedded inside of the annuity at the death of the original owner. Thus, for instance, if an annuity originally purchased for $100,000 but now worth $150,000 is inherited, the $50,000 of gains will be forced out and taxed within 5 years of death, instead of being stretched for far longer (though notably, the benefit of the stretch is partially limited by the fact that gains are assumed to be distributed first from an annuity, including an inherited one). The situation is exacerbated by the fact that trusts are subject to compressed trust tax brackets, with the top 39.6% tax bracket (and the 3.8% Medicare surtax that also applies to annuity gains) kicking in at just $12,300 of taxable income.

On the other hand, where the annuity is likely to be liquidated shortly after death anyway, the potential for a stretch is a moot point… though presumably, using a trust or a restricted payout form is being done specifically to limit such access. Nonetheless, being able to stretch out an inherited annuity is only relevant in situations where there is a likelihood that it will be stretched anyway. Though bear in mind that if the beneficiary would like to stretch, and simply isn't happy with the investment options of the annuity, it may be possible to do a post-death 1035 exchange under PLR 201330016.

In addition, the potential for a post-death annuity stretch is irrelevant if the annuity doesn’t actually have a (material) gain in the first place; after all, there’s little purpose or benefit to a stretch if there’s no gain to stretch! Although alternatively, in situations where there is no gain anyway, the adverse consequences of using a trust are also somewhat diminished, making it “less problematic” to use a trust and making the beneficiary-designation-with-restricted-payout less beneficial as an alternative.

The bottom line, though, is simply this: until the IRS and Treasury update their rules, or a private letter ruling is issued, the use of a trust as the beneficiary of an inherited annuity will mean trading off the opportunity to stretch post-death RMDs over the life expectancy of the beneficiary in exchange for achieving the control restrictions of having the trust in place. In situations where there is some desire to limit access to the inherited annuity principal, but it is ok to make partial payments over time, a beneficiary designation with restricted payout may be an appealing alternative, as it does allow a stretch over the beneficiary’s life expectancy. However, in the situations where trusts are most necessary – for severe spendthrifts, significant asset protection, and sheltering assets from estate taxes – annuity owners may simply have to accept the adverse tax consequences of a reduced stretch as being outweighed by the importance of the non-tax benefits and goals accomplished by the trust!