Executive Summary

As the buzz around the "robo-advisors" continues, this week marks another two big announcements: Betterment has raised another $32M in a fresh round of venture funding, with another $28M for Learnvest, following on the heels of $35M from Wealthfront just two weeks ago. Collectively, the three platforms have raised a whopping $95M in just the past two weeks, with the total collective funding for the robo-advisor space approaching a quarter of a billion dollars.

Yet despite all this focus, the actual business and revenue growth results for robo-advisors has been fairly meager, at least so far. The latest fundraising for these three platforms brings their total venture capital funding up to more than $150M, despite the fact that after 3-5 years the companies have been around with "exponential" growth, they cumulatively have less than $5M of revenue. Collective across all the robo-advisor-labeled platforms, actual assets under management (not just fuzzy "advisements") is no more than a few billion dollars, which at the fee schedule for these platforms likely amounts to little more than $10M of revenue for platforms that have cumulative venture capital funding in excess of a quarter of a billion dollars. Which implies, to say the least, that at least a few of these VC investments probably won't work out so well.

Nonetheless, this doesn't mean the robo-advisor trend should be ignored, despite the fact that they have little more than roughly a 1/1000th market share of household investable assets. While there's still little evidence to suggest that robo-advisors are drawing any volume of clients from human advisors, they are demonstrating how the core of constructing and implementing a passive, strategic portfolio can be commoditized for an extremely low cost. In the end, we may look back on this 2009-2014 era as one that transformed technology-driven portfolio construction the way the introduction of the index fund transformed the world of stockpickers 40 years ago. Notably, the introduction of the index fund did not eliminate the need for or value of human advisors, but it did force advisors to continue to evolve their value proposition to keep up, as today's evolving robo-advisors will likely do as well. In fact, in the end, the primary players that get "disrupted" by robo-advisors may not actually be human advisors at all, but the custodians, broker-dealers, asset management, and technology firms that support them!

Fresh Rounds Of Venture Capital For Betterment, Wealthfront, And LearnVest... For How Much Revenue?

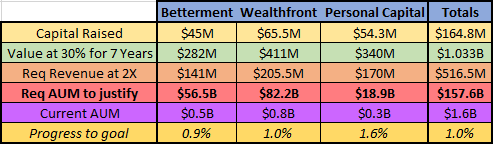

Today, "robo-advisor" services Betterment and LearnVest announced big new rounds of capital, with another $32M for Betterment (bringing its total to $45M) and a fresh $28M for LearnVest (its fourth round of funding after its initial seed, bringing the total to $69M). The announcements come fresh on the heels of competitor Wealthfront's announcement just two weeks ago that it, too, had raised another $35M of its own, bringing its own total to $65.5M. One wonders if an announcement by Personal Capital might soon be coming as well (which has already raised $54.3M through last year), just to round out the group!

Yet despite the somewhat astounding amounts of capital flowing into the robo-advisors, the actual amount of revenue involved is still remarkably low. While Wealthfront has grown "explosively" in the past year, from barely over $100M to now more than $800M of AUM, at its 0.25% fee that's still only about $2M of revenue. With Betterment at $500M (also assuming an average fee of 0.25% on its graduated fee schedule), that's another $1.25M of revenue. And as of the end of March, Learnvest's ADV was reporting 3,700 clients (if 100% of them are enrolled in LearnVest's $19/month fee, that's less than $1M of ongoing revenue). Which means the three companies have raised $95M of venture capital in the past 2 weeks - on top of the ~$84M they had already gathered - on what is collectively less than $5M of revenue even after 5 years of "exponential" growth.

The math isn't much better for Personal Capital, which by the end of January was reporting $324M of AUM for just over 1,000 accounts; even at their maximum fee schedule of 0.95%, Personal Capital would still have the highest revenue of all at just over $3M, but still little more than 1/20th of the capital it's raised after nearly 5 years of growth. In fact, given that many of the robo-advisors have a staff of 30-50 engineers, it's not even clear whether any of them have reached a breakeven on expenses yet.

Justifying Robo-Advisor Valuations With Growth - What Does It Take To Succeed?

Viewed from the perspective of a venture capitalist's ROI, the numbers are even more daunting. Let's say that "conservatively" a venture capital firm wants to generate a 30% return on their funds (to compensate for how many ventures don't succeed at all) invested over a time span of the next 7 years. Even if we assume that "the past is prologue" (i.e., we ignore the fact that some venture capital rounds are already 3-5 years in and are still funding organizations that haven't broken even yet), that means AUM-based companies like Betterment, Wealthfront, and Personal Capital, that have now raised $45M, $65.5M, and $54.3M, need to be worth $282M, $411M, and $341M, respectively. Assuming fee schedules of 0.25%, 0.25%, and 0.90%, respectively (based on their average account sizes), and a "typical" multiple of 2X revenue for a "mature" AUM-based company, this implies that by the beginning of the next decade, Betterment needs $56.5B of AUM, Wealthfront needs $82.2B, and Personal Capital (thanks to their higher fee schedule) needs "just" $18.9B to justify their valuations.

And of course, the reality is that the venture capital invested actually purchased only a fraction of the companies, not the entire amount, so for a venture capital firm to get its ROI on its share, the numbers would have to be significantly bigger still! To be fair, these numbers aren't "impossible" if the exponential growth continues (though 10%/month growth gets very difficult on an ever larger base!), and there can obviously be some debate about the exact ROI assumptions and valuation multipliers as well, but it's important to keep the sheer magnitude of these numbers in context.

These three platforms, combined, have all been around for 3-5 years, and collectively have about $1.6B of the almost $160B they need in another 7 years to justify their value, and are at barely 1% of their goal. By contrast, Ric Edelman's firm alone added 4,000 clients and what should be approximately $1.6B of AUM in just 2013 alone, equal to the cumulative total of all three robo-advisors. MFS invented the first open-end mutual fund in 1924, and after 90 years they still have "only" grown to $71B of AUM; Wealthfront needs to beat that in 7 years. Collectively, these three robo-advisors alone would be almost 50% larger than the entirety of what the PIMCO mutual fund family has accumulated over its entire existence. And that's looking only at these three offerings, not to mention their wide and growing competition including FutureAdvisor, MarketRiders, SigFig, JemStep, Motif Investing and more - which have themselves raised another $85M of venture capital. When we add them all together, the collective venture capital raised for robo-advisor platforms of various sorts is now more than a quarter of a billion dollars, for what may collectively amount to no more than roughly $10M of cumulative revenue across all of the players!

And of course, there are still about 300,000 human advisors as well, who make the compelling case that there are still some parts of personal financial advice that can't be replaced by a computer alone. And other major players like Vanguard are starting to throw their hat into the ring, too (as discussed a few weeks ago in Weekend Reading). And new robo-advisor competitors like WiseBanyan are showing up, threatening to undercut even the existing robo-advisors by offering investing for free (offering to provide services with no apparent business model at all, certainly a concerning sign of a potential bubble!?).

Notably, all this competition and daunting growth numbers doesn't necessarily mean that all robo-advisors will be doomed. The AUM the robo-advisors must gain to be viable is still quite small relative to the estimated $28T of household investable assets out there (though it also means robo-advisors right now only have about a 1/1000th market share, which is not exactly "disruptive"!). There is certainly room for at least some to survive, and a few of the start-ups will likely be acquired for their technology by larger, established custodian and asset management players. Yet given that all of these firms have been built in the aftermath of the financial crisis - and raising barely enough AUM to approach breakeven despite a raging bull market of nearly 175% run in the S&P 500 from the trough in March of 2009 - it's not difficult to imagine that there are going to be some losers in this robo-advisor arms race. None of them have even faced, let alone survived, a single bear market, despite the fact that the ability to retain and "behaviorally manage" clients in the midst of a bear market is one of the most critical questions to the business model (except perhaps for Personal Capital, which does employ human advisors as relationship managers).

Who's Disrupting Who?

Perhaps the most notable impact of the robo-advisor trend, though, is to simply recognize who and what is really being disrupted. In the early days of robo-advisors, they primarily positioned themselves against traditional advisors, implying that robo-advisor assets gained would be human advisor assets lost.

Yet the reality is that in most situations, several different companies all "touch" the assets in a traditional investment management relationship. For instance, an advisor that follows the DFA philosophy and has $100M of client assets means there's $100M for "the advisor", $100M for DFA, and $100M with Schwab or some other custodial platform. It's the same $100M, impacted by (with costs allocable to) three different businesses that are all part of the delivery chain. Which means that there is also potential for robo-advisors to be disruptive, not by impacting the human advisor part of the service, but the other parts instead.

In fact, as I've written in the past, the primary competitor for the robo-advisors may not be human advisors, but do-it-yourself platforms like Vanguard and Schwab. And similarly, Betterment's recent "Betterment Institutional" offering could disintermediate traditional custodians (and there are rumors that other "robo-advisors" are exploring partnerships with human advisors to supplement what the robo-advisor platforms alone cannot do for personal interaction). For instance, our XY Planning Network is exploring a relationship with Betterment Institutional, which would be able to provide advisors with access to a "TAMP" to support their clients on investment management through Betterment, without the need for a custodian, broker-dealer, trading software, or portfolio performance and reporting software. In other words, it would be the advisors and the robo-advisors together disrupting the rest of the value chain, especially start-up advisors that have simpler needs and are not tied in to legacy platforms (and implies that ultimately, the exit strategy for some robo-advisors may be to sell to 'traditional' platforms that want to assimilate their technology to work with human advisors!).

Looking Back From The Future

Ultimately, I do think we'll look back at this 2009-2014 era as the one where the core construction and implementation of a passive, strategic portfolio became commoditized by technology for an ultra-low cost, in a transitional moment as seminal as what Vanguard's first launch of the index fund has been slowly and steadily doing to the world of stockpicking and mutual fund managers for the past 40 years. In truth, this trend towards lower cost portfolio implementation is not new - it dates back to the de-regulation of trading commissions on Wall Street, which brought on the rise of the discount broker in the 1980s and 1990s, the rise of online discount broker in the 2000s, and now the rise of the online portfolio construction solution in the 2010s. It will lead to a few winners, and some traditional players that will be losers.

But when we look back, I suspect the greatest "surprises" may actually be that good human advisors were not eliminated at all (though a few bad ones clearly will be), just as they were not eliminated by the index fund either. In fact, arguably the growth of indexing and portfolio management and the decline of traditional "stock brokering" helped support the first wave of growth in financial planning - as shown below from a College for Financial Planning publication from 1972! - and in turn the growth of robo-advisors may simply drive financial planners even further in the direction of providing quality personal financial planning advice to maintain their unique value for clients while leveraging technology for the (commoditized) core portfolio management.

In other words, robo-advisors may simply represent the future of how human advisors too will manage client portfolios (in fact, many human advisors utilize technology to run their firms like a "robo-advisor" already!), and in that world the biggest losers will actually be traditional custodial and brokerage platforms that are 'disintermediated' and disrupted in the process of transitioning investment management from simply being a mechanism to distribute investment products to the actual fiduciary management of investment portfolios! In turn, this suggests that what we are witnessing now, just as with so much other technology innovation in the past 15 years with the rise of the internet, is not a world where the robots are replacing the humans, but instead a world where humans are increasingly forced to recognize what humans don't do well (and let technology do it better, such as with the implementation of portfolios), and shift their own focus to what they are able to do well to deliver value (e.g., the delivery of personal financial advice and helping clients with the necessary behavior change that goes with it).

In the meantime, though, it seems there's no shortage of venture capital dollars better than the robo-advisors will disrupt... something, whatever it turns out to be. At least, the venture capital firms are sure betting a whole lot of money that's going to be the case. We'll see after the next bear market comes...

Edit: A previous version of this article incorrectly cited the total capital raised by the three firms as $105M, instead of $95M. That's what I get for trying to feed the blog after midnight.

Great breakdown of venture capitalist’s ROI. I agree with your assessment that these online advisors are disrupting and stealing away business from discount brokerages- Scottrade, TDAmeritrade, etc. There are two online advisors to keep on the radar that are providing a platform to advisors now or in the near future- Motif Advisors (in Beta now) and Capital Engines (in Beta soon I am told).

Michael, the numbers work out very clearly from a pure mathematical/ROI perspective the way you show. It’s fairly obvious that most of these “robo-advisor” firms will never deliver an ROI to their investors (and in some cases may never even break-even, which I think may be the case, at least with a firm like LearnVest). However, if you look and think a little deeper, I think the identify of the VC investors might shed some light on the underlying strategy. When firms like American Express and Northwest Mutual are investing, it leads you to believe that they may not necessarily be chasing a pure ROI on the operations component of these firms. Rather, they are backing these firms in order to build a captive client base – a client base that they will eventually own and have the ability to market/cross-sell to.

I don’t know all the numbers off-hand, but if you assume collectively between the four firms mentioned that there are somewhere in the neighborhood of 45,000-50,000 clients currently, and thousands more joining all the time, it seems plausible that other financial services firms would LOVE to have the ability to market to a captive audience of exiting clients that have already displayed a willingness to purchase financial services online. So let’s say within a few years these firms collectively serve 100,000 clients (regardless of AUM or revenue), don’t you think there are plenty of large financial services firms that would be licking their chops to serve these clients?

I think being a “robo-advisor” is not an end in itself but rather a means to an end (selling their businesses).

Very interesting analysis…I agree completely with your conclusion that robo-advisors will make “the core construction and implementation of a passive, strategic portfolio became commoditized by technology for an ultra-low cost,” I believe the future is very bright for human advisors but they will need to dramatically lower the current cost of implementation portfolio management.

I am still trying to figure out the business model of WiseBanyan…they use FolioFn as their B/D…did you uncover anything else

Michael, with only $230,000,000 in AUM for Betterment at an average of .25%, how are they even profitable?

see this article… http://iheartwallstreet.com/2014/05/29/paint-by-numbers-roboadvisors/

This post coveys my thoughts pretty well… http://iheartwallstreet.com/2014/05/29/paint-by-numbers-roboadvisors/. And, I think the robo portfolios are getting killed right now. “Why not just buy an index fund”? and save one more layer of fees? You can get an asset allocation anywhere for FREE!