Executive Summary

If clients could simply accomplish everything they wanted, at once, with the resources they had, financial planning would be unnecessary. It would simply be a world of instant gratification, as needs were satisfied on demand. Of course, in the real world, we can't simply have anything/everything we want whenever we want. Resources are limited, and as a result financial planning is essentially about trade-offs. We must prioritize which goals are most important to achieve, and allocate resources to them, recognizing that this means money may not be left to satisfy other goals (or wants or desires). Thus, in practice we might say that the essence of financial planning is to help clients prioritize trade-offs, and decide what goals will be satisfied first (and which will be second, and which won't be done until third, etc.).

However, in financial planning we have a problematic tendency to just "dump" a long list of recommendations on clients, with either an implicit expectation that they will implement everything, or with a series of priorities that the advisor (not the client) establishes as "the expert" as being most important. Yet behavioral research suggests that this can be daunting, overwhelming, or sheerly unmotivating for clients. In an effort to be comprehensive, protect ourselves from liability, and demonstrate the thoroughness of our expertise, we may be getting clients stuck into an analysis-paralysis paradox of choices, or worse simply overwhelming them into inaction.

Ultimately, the key may not merely be to give clients a comprehensive list of recommendations, or to tell them what steps they should take next, but instead to help them make the choice of what's most important to them and then hold them accountable to follow through on it. Accordingly, the ideal "Action Items" list for clients shouldn't just delineate everything the planner recommends in order, but be offered to clients with a series of blanks where they can fill in what's most important to them, what they will commit to do, and when. The goal is not to get everything done immediately, but instead to begin a process of incrementally getting a little done between (or at) each meeting, until the entire financial plan is finally implemented (and of course, by then it will be time update, change, and adapt accordingly in a continuous planning process!)!

The inspiration for today's blog post was a recent conversation I had with a fellow financial planner (we'll call him Paul the Planner), who was struggling with a client couple (we'll call them David and Susan, as names have been changed to protect privacy, of course!). The problem with David and Susan was that, as with many couples, their financial life was quite a mess, and there was a lot to be done to get them back on track. From getting life insurance in place to wrapping up old 401(k) rollovers to fixing their asset allocation to updating their estate planning documents, the list of work to be done was huge. Yet despite the urgency that Paul the planner had tried to instill, after several meetings over the span of nearly a year, virtually nothing had actually been done. David and Susan had their list of recommended action items, which numbered almost 25 in a remarkably detailed list of exactly what needed to be done, step by step, yet every time they sat down for a review, nothing could be checked off. David and Susan seemed stuck, despite the detailed list of recommendations that lay before them.

Financial Planning And Setting Priorities

At the most basic level, it might be said that all financial planning is really just about effective prioritizing. In a world where not everything can be done at once because (almost) all of us have limited resources, choices must be made about what's most important. Is it worth giving up on some spending now to have more saved for retirement later? Which will we save for first, retirement or college education for the kids? Should we save allocate more money to the emergency fund, or pay down that credit card? Should we invest time and effort to get those estate planning documents updated? Which needs and goals have the greatest priority?

Of course, in some cases there is only one technically correct answer (having estate planning documents is better than not), but in most scenarios determining which trade-off is best is in the eye of the beholder (is it worth skipping the cost of a vacation this year to save more for retirement?). With the same information, different people will prioritize differently based on their own needs and goals. Accordingly, the action items of every financial plan end out customized to the individual needs and goals of every client, based on what's most important to them (with, perhaps, some guidance and helpful nudges from the planner about what wisdom would suggest deserves a little more priority than it is currently receiving).

The caveat, though, is that prioritizing in financial planning is about more than just allocating financial resources. It's also about clients allocating time, attention, and effort towards making the changes necessary to implement those goals. If there's simply too much to decide upon and too much change to make all at once, it's overwhelming - as it was in the case of David and Susan - and clients may be paralyzed by the choices and unable to move forward. Which means that ultimately, good financial planning requires helping clients prioritize not just how they'll allocate resources towards their goals, but how they'll implement the steps necessary to make changes to achieve those goals.

Making Recommendations Too Comprehensive?

While as financial planners we're trained in how to analyze trade-offs and evaluate alternatives in crafting recommendations for clients, once we complete that part of the process we have an unfortunate tendency to "dump" all the recommendations on clients at once. Yet as the research shows, delivering clients too many choices at once about what to do next can paradoxically overwhelm them and may hinder their ability to actually move forward. In other words, in these "paradox of choice" scenarios it can be easier for clients to decide what to implement first from a list of 3 recommendations than from a list of 25, because the latter triggers a decision-making analysis-paralysis about what to do first.

So why do we as planners tend to dump all the financial planning recommendations at once, even when the outcome can actually be problematic for clients? Sometimes it's in an effort to justify and validate that we're worth the cost the client pays; although it's not quite rational, there is sometimes an implication that the sheer quantity of recommendations is related to our value. After all, if our extensive analysis and efforts lead to a single, simple recommendation, there is a fear that clients might wonder whether they're getting their money's worth; on the other hand, if the process results in a big huge list of recommendations, it justifies that our clients need us - "See all the things you need to change/fix in your life? Isn't it a good thing you hired me?" Sometimes the implication is even more overt: in the view of many (clients and planners?), the more "brilliant" the planner, the longer the list of recommendations they can come up with?!

In other situations, the problem may be more insidious; the desire to dump all the recommendations at once may be viewed as a way to mitigate professional liability. After all, no planner wants to be in the position of having something go wrong where the client (or the client's spouse or heirs) comes back and blames the planner for not having addressed and recommended a solution to the problem. Thus, the giant list of recommendations essentially becomes documentation for the planner to escape any culpability for adverse outcomes: "See, I directed the client address this issue in the recommendations in the financial plan; it's not my fault the client failed to implement [this one item amongst a list of two dozen other items]."

Yet ultimately, the fact remains that these concerns of the planner to justify value, demonstrate brilliance, and protect from liability, may actually be hindrances to clients actually following through on the action items they need to implement to achieve their goals. While it's appealing to the planner to deliver a long list of recommendations, what we see from the behavioral research is that a huge number of choices can be paralyzing. In other words, if we really want clients to implement the recommendations, perhaps we need to present fewer of them at a time, and/or truly help clients truly prioritize which to do first/next/last.

How To Better Help Clients To Prioritize

So what can we do to help clients prioritize? What could Paul do to help David and Susan through their roadblock? Given that entirely skipping recommendations may not be feasible for many, in light of the perceived liability risks, the key appears to be truly spending time focusing on the prioritization process. In other words, it's not about just crafting the list of recommendations, or putting them in an order that Paul the Planner thinks is important, but to specifically discuss with the clients what is most important to them and get their agreement about what will be done first. In other words, get David and Susan to explicitly state what is most important to them, and what they will do first. It's not about prioritizing the whole list, but simply about picking the top 1 or 2 items that will be done between now and the next meeting. When the next meeting comes, those items can (hopefully) be checked off, and the next can be done. After a period of time, eventually all the items will be checked off.

Notably, this path is likely quite unsatisfying for many planners (including Paul), who want to see clients act immediately to make all the changes necessary to "solve" their financial issues (what if something bad happens and they hadn't yet gotten to that item on the list!?). Yet the reality is that for many (most?) people, that amount of change all at once is not only realistic, but can be overwhelming. As with David and Susan, the more we try to get clients to do at once, the less they sometimes will actually do. The incremental approach may actually get more done in the long run. And which do you do first, given the risks involved for the recommendations that might be skipped? Well, that's for David and Susan to decide and prioritize. That's the point.

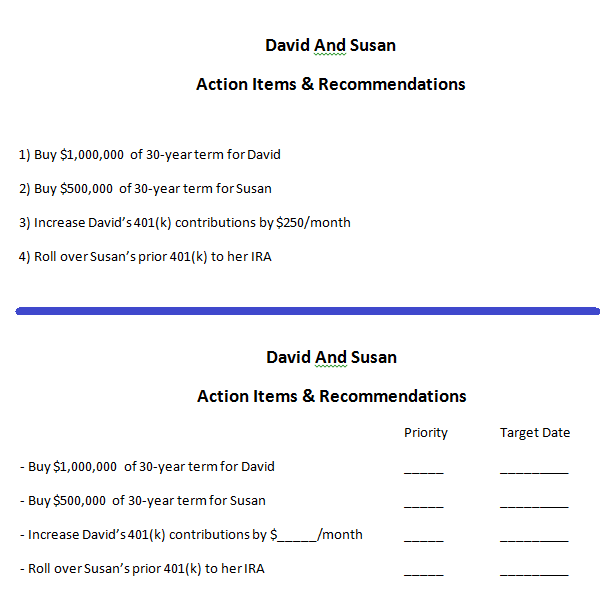

Of course, from there, it's still necessary to help clients ensure that they really do follow through and implement the recommendations that are prioritized and committed to. In this regard, it may help to take additional steps to help clients commit to the actions they state they will take. For instance, research shows that we are more likely to follow through on actions we write down; accordingly, rather than just presenting the ordered list of recommendations to David and Susan, there could be a blank next to each item where they write down which one or two or three will be top priority and done first. Similarly, another blank could be included where David and Susan choose - on their own - the deadline by which they intend to complete the action item. For instance, compare the two Action Item/Recommendation lists below:

With the second format for the action item list, the planner doesn't tell clients what to do and when to do it; David and Susan choose for themselves what to do and by when to do it, and Paul the Planner's job is to help hold them accountable to the decisions they made for themselves. Yes, Paul could figure all of this out on behalf of his clients, but the point here is not just about telling clients what to do, but about helping them actually do it, which means taking the steps necessary to get buy-in and commitment are absolutely crucial to the ultimate success. In fact, this is one of the key insights of Robert Cialdini's book "Influence: Science and Practice" (which I highly recommend as essential reading for financial planners!) - that it can be far more effective to influence people by getting them to commit to an action and then holding them accountable to it, rather than simply trying to get them to do what you say in the first place.

With the second format for the action item list, the planner doesn't tell clients what to do and when to do it; David and Susan choose for themselves what to do and by when to do it, and Paul the Planner's job is to help hold them accountable to the decisions they made for themselves. Yes, Paul could figure all of this out on behalf of his clients, but the point here is not just about telling clients what to do, but about helping them actually do it, which means taking the steps necessary to get buy-in and commitment are absolutely crucial to the ultimate success. In fact, this is one of the key insights of Robert Cialdini's book "Influence: Science and Practice" (which I highly recommend as essential reading for financial planners!) - that it can be far more effective to influence people by getting them to commit to an action and then holding them accountable to it, rather than simply trying to get them to do what you say in the first place.

Ultimately, this kind of prioritization approach still does not fully eliminate or resolve the tendency of planners to "dump" a long list of recommended action items on clients (as realistically, there may not be a way around that in today's litigious society), but it does focus on what steps can be taken to incrementally work through the list until everything is completed. If you've got clients who are stuck at an implementation roadblock, you might give it a try.