Executive Summary

In the financial planning world, most firms are small businesses that are struggling to get larger, trying to grow the practice by simultaneously competing for the same biggest clients and at the same time serving anyone who is able and willing to pay for financial planning services while slowly raising minimums to become more profitable. In response, many practice management consultants have suggested that financial planners establish a niche to build their businesses, focusing on a smaller market they can dominate rather than a larger market they struggle in. Notwithstanding this advice, few firms have adopted the niche approach, most commonly out of a fear that if they narrow the focus of the practice it will simply lead to fewer clients. Yet the reality is that in other industries, firms are growing like never before by focusing not on the biggest clients and opportunities, but by capitalizing on "the long tail" of smaller, niche segments that can add up to real dollars, and become accessible because of the how the internet facilitates business in the digital age. Is it time for financial planners to similarly adopt the long tail approach?

The Long Tail

The concept of the long tail comes from an article of the same name written in the fall of 2004 by Chris Anderson, which was ultimately expanded into a book as well. The basic idea is that many industries have an opportunity for tremendous profit and success by focusing not on what's most popular, but on selling a large number of niche items, each of which is sold relatively few times but which in the aggregate adds up to a significant volume.

The concept of the long tail comes from an article of the same name written in the fall of 2004 by Chris Anderson, which was ultimately expanded into a book as well. The basic idea is that many industries have an opportunity for tremendous profit and success by focusing not on what's most popular, but on selling a large number of niche items, each of which is sold relatively few times but which in the aggregate adds up to a significant volume.

For instance, as Anderson wrote in the article, then-popular subscription music service Rhapsody made available 735,000 music tracks, and found that every one of its top 100,000 tracks was streamed at least once a month; in fact, this was true for its top 200,000, its top 300,000, and even its top 400,000 tracks. By contrast, a bricks-and-mortar music store at the time might have only carried about 40,000 tracks' worth of music; in other words, Rhapsody continued to see ongoing activity with an incredible number of tracks that traditional music stores didn't even offer, which individually recorded too few sales to be practical, but in the aggregate added up to big business.

And in point of fact, this activity was mirrored in other businesses at the time as well; the average Barnes & Noble physical bookstore carried 130,000 titles, but more than 50% of Amazon's book sales came from outside its top 130,000 titles. The average Blockbuster video rental store carried 3,000 DVD titles, yet 20% of Netflix rentals at the time were outside of the top 3,000 titles (and as Netflix access has grown, demand has shifted further into the tail). More recently, the trend is showing itself in the development of "apps" for mobile devices; by the end of the year, it's estimated that only 1/3rd of the revenue will come from the top 100 apps, with the other 2/3rds coming from the long tail of app developers.

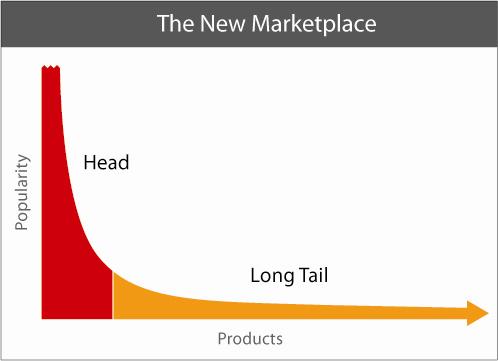

In essence, as shown in the graphic below, the amount of sales activity in the long tail (the orange area) can equal or exceed the activity of "the hits" or the most popular purchases.

Building A Tail Business

For many industries, the big trend of the past decade has been capturing the business opportunities in the long tail - a segment of the market that previously didn't exist. As noted above, more than half of Amazon's book sales come from outside its top 130,000 titles, which was all even a mega bricks-and-mortar bookstore would have carried 10 years ago. Which means that Amazon is generating a huge portion of its revenue not just by outselling and undercutting traditional book retailers in head-to-head competition, but also by creating a marketplace for books that weren't being sold anywhere before. In turn, this also means that authors whose books would have previously languished unread, now at least have some opportunity to find an audience.

What's significant about this phenomenon is that in most industries, there is an excessive focus on trying be at the head of the distribution, when the reality is that the tail has far less competition. Historically, it has been necessary to focus on the head, for the simple reason that if you were in the tail, it was as though you didn't exist at all; if you wrote the 140,000th, 175,000th, and 190,000th most popular books, you didn't see any of your books in a bookstore. But notably, that's no longer true, once Amazon came along and provided a way for them to be sold and reach a target audience. For Amazon, this was good business. For an author in the tail, though, it has created new business opportunities that never existed before. And this new trend is similarly true for those who produce movies that can be found on NetFlix, music than can be found on iTunes, or even those who want to buy other people's "junk" and sell it on eBay.

The Tail Business In Financial Planning

In the financial planning world, the reality is that most firms essentially run a "tail" business. Given the relatively few number of very large firms, and the incredible number of solo practitioners and 2-3 planner partnerships, the majority of financial planning ultimately gets delivered to the public from the tail.

However, many firms operating in the tail try to push themselves towards the head, notwithstanding the fact that the competition is tougher. This is common in other industries as well: movie studios that try to land mega blockbusters instead of "just" making a good, profitable movie; book publishers that hunt for the next bestseller instead of putting out quality titles that generate moderate sales produced at a reasonable cost; recording studios that hunt for the next great star.

Yet the irony is that while most firms tend to try to serve everyone, get the same biggest clients, drive up their minimums, and hunt for big fish in the same bloody ocean, the reality is that since most firms are in the tail, the optimal strategy is actually not to push towards the more competitive head, but instead to differentiate and focus on a clear segment of the tail that the firm can "own" and be dominant!

In turn, this is why it's increasingly viewed as a best practice for financial planning firms to progress towards operating in a niche, rather than trying to do everything for everyone. The niche practice is the tail business; the everything-for-everyone and bigger-and-bigger clients approaches are the most difficult markets to reach. Historically, an excessive focus on the niche would have been dangerous, for the same reason that trying to write books that wouldn't be bestsellers or produce movies that wouldn't be blockbusters was dangerous: if you couldn't make it to the head of the distribution, you might never be found at all.

What's different in today's world, though, is the emergence of the digital age, and the presence of the internet and services like Google that allow consumers to find exactly what they want, that best matches their interest, tastes, or financial planning needs. Just as the internet made niche authors read, niche music heard, and niche movies seen, so too does it create the opportunity for niche financial planners to actually be found, and to thrive in the tail like never before. If a financial planner creates a niche business that might only serve 100 people in the country, the reality is that now the financial planner actually can find those 100 people and work with them (or alternative, can be found by them), creating a successful business for which there is no competition!

So what do you think? Is your business in the head, or in the tail? Where do you want to compete? If your goal was to focus on the tail, how would you market and grow your firm differently?

Michael

It may be relevant that your examples of businesses that exploited the long tail are businesses that are all things to all people. They didn’t go looking for a niche – the niche found them.

The problem for a small planning business adopting a niche strategy is that the profitable niche may be difficult to successfully identify and even more difficult to successfully market to.

I’m not saying it isn’t a potentially valid strategy – just that it is easier for niches to find you if you are able to service everybody.

Regards

John

John,

Thanks for the feedback.

I would actually disagree with you to some extent, though.

The analogy of services like NetFlix and Amazon are not that they are businesses that serve everyone. It’s that they are aggregators of niches. And ultimately they don’t produce and sell the product or service; they match a buyer to a seller and take a small fee for what is essentially providing the infrastructure and being the matchmaker. But the person who makes the content is still in a niche to some degree or another.

The true seller, the one who creates the core value, is the musician or author. And there aren’t very many successful country/hip-hop/classical/rap/pop musicians. Nor are there very many successful mystery/romance/historian/self-help authors. Simply put, the creators of the deliverable don’t succeed by being generalists. They succeed by effectively serving a niche, and having access to a marketplace to reach consumers; NetFlix, Amazon, etc., provide that marketplace.

If we extended the analogy to financial services, this would suggest that the best way to be a profitable financial planner is still to have a niche. And one way to build your business is to affiliate your niche under a larger marketing organization where you can be the best at your niche, earning 100% of the business in your niche from the aggregator while reaching more people thanks to the aggregator’s reach.

At this point, though, there’s really only one aggregator service for finding financial advisors: it’s search engines like Google. And as Google metrics make it quite clear, you have virtually no possibility of being found if you try to be everything to everyone, just as the mystery/romance/historian/self-help author doesn’t sell very many books on Amazon, for the primary reason that consumers intuitively understand, and the results usually make quite clear, that people who try to be everything to everyone are often mediocre at all of it.

Respectfully,

– Michael

Do you think it is realistic for people to choose a financial planner from a google search?

Jeremy,

Bear in mind, most people probably won’t type “financial planner” into Google.

They’ll type their problem into Google and go looking for a solution. The niche planner that is the best fit for their solution will win the business.

In a similar manner, we might ask our friends for a referral to a generalist, but when we want a specialist, we search by other means. Our friends and family don’t necessarily know the best specialists in the country. You find them through searching or other resources.

– Michael

Jeremy,

As a starting point for their research, yes absolutely, and increasingly more so.

Ultimately, this seems to play out in one of two ways:

– Search for a planner on Google

– Ask a friend for a planner, and then verify the legitimacy of the planner by also searching for them on Google and seeing what comes up

Right now, I suspect the latter is more common than the former, but the former is gaining. We see new prospects and clients that came to our website from a Google search.

In fact, Rydex’s benchmarking study from last year found that “Online Searches” was one of the fastest growing marketing methods for advisory firms. I wrote about it earlier in the year at https://www.kitces.com/blog/in-the-future-the-best-firms-wont-find-new-clients;-the-new-clients-will-find-them/

– Michael

100% of my firms business comes from long tail, niche oriented search. And it’s not a small growth segment – we’re growing at a $3+ million per month AUM clip.

Great article Michael. Totally agree.

jw

Michael,

Excellent post! I agree wholeheartedly (as you would have guessed!).

The highest earners in every field are the specialists. Advisors who fear not being able to generate enough business in a niche need only look at the medical field. I live in a mid-size market, and there are doctors who specialize in practically everything right here in town. And they make a pretty good living.

Even if an advisor does not have the courage or direction to develop a niche practice, they can tailor their practice to the wants and needs of their current clients. You linked to Blue Ocean Strategy in your post, and any advisor can do the main exercise from that book: Find out what specific things about your practice that clients value most and least. Determine which of those things require a lot of resources to provide, and which require little. Plot them on a graph. Focus on the high value/low resource activities and limit or eliminate the low value/high resource activities.

That just gives your best clients more of what they want, without all the work and risk involved in discovering and exploiting a niche market.

Michael,

What I’m focused on is identifying some good working definitions of niches that are not based upon the occupations of the clients (but rather on other characterisitics) and how to market to those kinds of niches. Some examples might be: 1)philanthropically inclined 2) passive or active investors 2)outdoor enthusiasts vs. indoor enthusiasts 3) business owners vs. corporate executives 4) truly interested in deep legacy planning, etc.

These just seem to be more meaningful differentiators (focused on a wealth management deliverable) than whether someone is an orthodontist as opposed to a periodontist.

Can anybody think of any more?

Jeremy, yes, people find their financial planners on Google.

Amazon and Netflix didn’t innovate by making MORE products available, they created a process innovation that allows them to serve the long-tail. Although enabled by the internet, Amazon’s innovation isn’t selling online. Amazon’s innovation is how it organizes and presents products. No longer is browsing a random exercise limited to the fraction of available titles that happen to be on a particular store’s shelves. Personalized recommendations and user reviews allow Amazon users to quickly find items that interest them. The result is far more sales than would be possible in a traditional retail setting. Netflix offers a similar innovation. In both cases the companies have not succeeded simply by using the postal service/fed ex/UPS/etc. to deliver goods. Their innovation is providing a useful window into, and access to, a much broader universe of entertainment content – books, movies, music, etc. – than had been previously available.

So, how can we relate this to the financial planning industry? …and of course I welcome your thoughts on the subject — We are in a saturated market, and new advisors need a niche to survive. But declaring a niche is scary because, once declared, customers more than likely have to find YOU rather than you finding them (with the exception of advisors serving one firm where they attend all of the company parties). Just as authors selling fringe titles on Amazon wouldn’t survive without a huge market to draw from, we have to increase our geographical borders and make it easy for our customers to find us. Dipping our toes in the niche won’t work, it requires 100% commitment (to the marketing, I’m not saying you turn down a $5M client who asks really nicely), a persuasive web presence that encourages opt-in before the client is ready to buy, then a very effective drip marketing campaign that can keep communicating with people and adding value, fantastic SEO and good relationships with the press who write about our niche. I think in THAT way, you set yourself up to be a successful niche advisor.

Thoughts?

Hilary,

I do think part of the fear in pursuing an inbound marketing strategy is the idea that it builds around people finding you, but that doesn’t mean you can’t go out and find people, too – including, and perhaps especially, those in the niche.

Thus, for instance, someone building a niche around ophthalmologists (as an arbitrary example) might build a business and content and marketing around ophthalmologists. But that doesn’t mean the planner can’t also join the ophthalmology association, volunteer, go to ophthalmology networking groups, submit articles to ophthalmology publications, begin establishing relationships with ophthalmology centers of influence, etc.

In reality, much of this activity might look very similar to what many planners already do. The difference is that when you’re one of 17 planners who solicits doctors, it makes little impact. When you’re the one premiere planner that specializes in ophthalmologists, you’re the one they say “yes” to because you’re clearly differentiated and specialize in their problems and needed solutions.

From that perspective, having a niche isn’t about abandoning traditional marketing approaches. It’s actually about making those traditional marketing approaches more effective… in addition to the opportunities around content and inbound marketing.

– Michael