Executive Summary

Communicating with clients effectively has become increasingly challenging in today’s world, not because it’s difficult to find a way to communicate with clients but because there’s often uncertainty about how much communication is appropriate, and by what means/channels. Are in-person meetings best, or are phone calls preferable? Is email better than a phone call? Where do one-to-many communications like newsletters and social media fit in?

A recent Australian study of how clients prefer to be communicated with from their advisors sheds some interesting light on the challenge. The results suggest that while meetings still dominate as a primary mode of communication, there is a great deal of variability about where those meetings should occur (in advisor’s office or elsewhere), how formal they should be, and where email, phone calls, and other communication plays a role. And notably – though perhaps not surprisingly – there are material differences in communication preferences amongst Baby Boomer, Gen X, and Gen Y clients.

Notwithstanding these challenges, though, the study supports a great deal of other research suggesting that effective client communication remains a key for client satisfaction, retention, and referrals. And amazingly enough, not only is getting the “right” communication channels an enhancement to the client relationship, but even just communication in clients more ways – across more channels – shows an increase an client satisfaction!

The inspiration for today’s blog post was a recent study I read, entitled “Connecting With Clients: Solving the Communication Matrix for Financial Advice Practices” by the Beddoes Institute, a practice management benchmarking and consulting firm for Australian financial advisors. While undoubtedly there may be a few differences in some of the details of client communication styles and preferences in Australia versus the US, the study is still one of the more comprehensive – and interesting! – I have seen regarding advisor-client communication.

The Beddoes study starts by examining the different types of communication available to advisors (the “communication matrix”, broken into two broad categories: One-to-one personal communication with clients, and One-to-many communication. The former includes communication like emails and phone calls, meetings at the advisor’s office or client’s work/home location, as well as more informal meetings, and even digital meetings like Skype. The latter one-to-many category, on the other hand, includes electronic and printed newsletters, webinars, printed information materials, and various forms of social/digital media.

Generational Differences In Client Communication

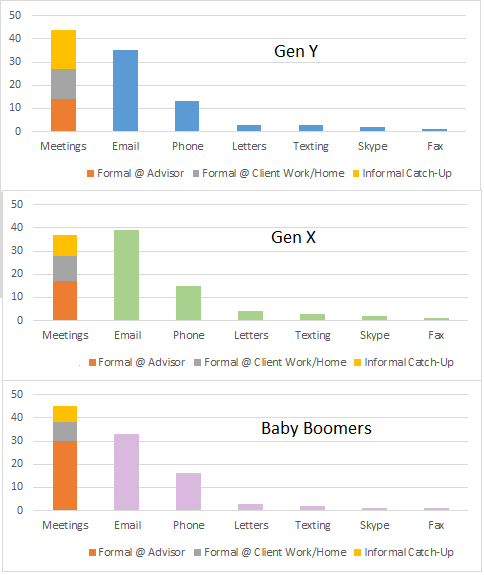

As the results of the study reveal – see Figure below – in the context of one-to-one communication, there are some material differences in communication preferences across the generations. While in general meeting in person is the leading option, there is little consistency to the type of meeting preferred. Overall, communication by email was consistently preferred more than any particular meeting type (formal at the advisor’s office, formal at the client’s work/home, or an informal catch-up).

However, within the meeting types, there were significant generational differences; both Gen X and Y’s preference for formal meetings at the advisor’s office was half that of Baby Boomers, while Gen Y in particular showed a strong preference for informal catch-ups (at a rate twice that of baby boomers). And notably, all groups showed a very strong preference for email communication over telephone calls – Gen X to the point that email was even (slightly) preferred over any type of in-person meetings at all! On the other hand, it’s notable that at least as a primary communication channel, none of the generations (even Gen Y) showed much of a preference for texting or video meetings via Skype.

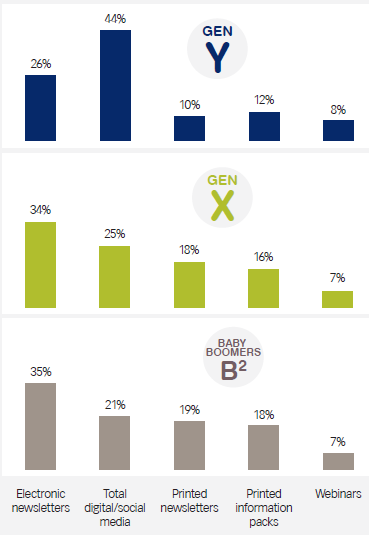

In terms of one-to-many communication, further generational differences emerged, as Gen Y in particular showed – perhaps not surprisingly – a strong preference for digital/social media communication as a one-to-many tool (a further breakout revealed a preference not just for ‘typical’ social media channels like Twitter and Facebook, but also the availability of some sort of advisor “app” as well). Beyond social media, Gen Y also had a strong preference for electronic newsletters as a second alternative, and fewer than 1-in-4 amongst Gen Y had an interest in printed newsletters or information. On the other hand, the desire for printed communication was not all that much higher with the baby boomer generation, where barely more than 1-in-3 preferred printed materials, though baby boomers did demonstrate a clear preference for electronic newsletters via email over digital/social media channels.

In terms of one-to-many communication, further generational differences emerged, as Gen Y in particular showed – perhaps not surprisingly – a strong preference for digital/social media communication as a one-to-many tool (a further breakout revealed a preference not just for ‘typical’ social media channels like Twitter and Facebook, but also the availability of some sort of advisor “app” as well). Beyond social media, Gen Y also had a strong preference for electronic newsletters as a second alternative, and fewer than 1-in-4 amongst Gen Y had an interest in printed newsletters or information. On the other hand, the desire for printed communication was not all that much higher with the baby boomer generation, where barely more than 1-in-3 preferred printed materials, though baby boomers did demonstrate a clear preference for electronic newsletters via email over digital/social media channels.

Benefits Of Effective Client Communication

Perhaps not surprisingly, the results of the study showed that advisors who are effective in delivering client communication in desired channels had clients who were more satisfied (along with reporting a stronger overall relationship with the firm, and a higher propensity to refer).

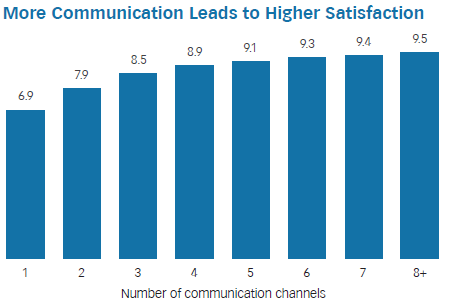

However, beyond just the fact that good matching of communication channels to preferences was a positive, the results also found that the sheer volume of client communication channels itself has a correlation to client satisfaction, with diminishing returns (but still a benefit) as the number of communication channels increases to 5 and beyond.

Further analysis by Beddoes found that this preference for communication breadth was significantly more noticeable for Gen Y clients in particular, who were materially less satisfied than their Gen X and Baby Boomer counterparts with “only” 3-4 communication channels, and were far satisfied with 5+ communication channels. Notably, the results also found somewhat counter-intuitively that for clients who were already being served comprehensively, there was less sensitivity to communication frequency (perhaps because their advice needs were already being so well met?), while for clients for whom only one/some needs were being met (e.g., perhaps modular one-off planning rather than a full comprehensive financial planning relationship), there was a high sensitivity for communication. Those being served in a limited manner were by a large margin the least satisfied, especially with limited communication (1-2 channels), but were almost as satisfied as comprehensive advice clients once the number of communication channels increased.

Practical Implications For Financial Planners

So what conclusions can be drawn from the Beddoes communication study regarding client communication?

The first key aspect to acknowledge – as has been supported by other studies as well – is that there is a clear “more is more” relationship with client communication. Even amongst the survey sample – which were all leading advisors in Australia (being considered for their AFA Adviser of the Year award) – an ever-increasing number of client communication channels improved client satisfaction. From a practical perspective, this suggests that a good target might be a mixture of at least two types of meetings (some at advisor office, some at client location or informal setting), some communication between meetings by telephone and email, and some form of ongoing one-to-many communication (e.g., an electronic newsletter), which would add up to the target 5 channels of communication. Beyond that point, it still pays to add more communication channels, but as noted earlier the incremental benefits of more communication isn’t much beyond 5 channels.

Second, the study emphasizes the value and importance of not just communication channel volume, but getting communication channel “right” as well. In the Australian context, the results found that even amongst leading advisors, there may be an over-reliance on formal meetings at the advisor’s office and phone calls, in lieu of more informal catch-ups and email. Use of one-to-many communication channels showed deficits across the board – in every channel measured, the amount being done was less than preferred (though close to on target for electronic newsletters). While these results many not translate perfectly to what advisors are actually doing for clients in the US, it’s not hard to imagine a similar parallel here, given advisor reliance on ‘traditional’ in-person meetings and phone calls, and limited forms of systematic one-to-many communications (e.g., newsletters, social media). To say the least, the study raises the simple question of whether/how often advisors are even asking and trying to gauge client communication preferences in the first place; do you consistently ask (and record in your CRM) whether your clients prefer email to phone calls, and formal meetings to informal catch-ups?

Beyond the client-specific communication preferences, the study results also show more broadly that different generations are beginning to exhibit consistently different communication preferences, suggesting at a minimum that advisors broadening their client base should be cognizant that they may well need to broaden their communication channels as well. This appears especially true if trying to reach Gen Y clients, who not only appear to demand and expect communication on a broader range of channels, but are also the most prone to being dissatisfied if their communication needs are not being met. On the other hand, relative to channels like social media, it’s notable that while there was a strong preference for Gen Y to see advisors using social media for one-to-many communications, their preference for one-to-one advisor communications still came back to more ‘traditional’ in-person meetings and use of email (albeit with a preference for informal over formal meetings).

Regarding social media in particular, it’s also notable that given the pace of social media adoption, and shifting demographics in that regard – Pew Research now finds that 55-65 year old females are the fastest growing Facebook demographic! –social media may soon become an increasingly key communication channel for all clients. After all, the survey results show that amongst boomers, social media now exceeds printed newsletters or printed information packs as the preferred one-to-many channel, despite the fact that iPad tablets have only existed for a mere 3 years!

The bottom line, though, is that the Beddoes study clearly emphasizes the importance of not just effective client communication overall, but the importance of choosing the right channels and having the right breadth and variety of communication channels, a significant challenge given the proliferation of tools and options available.

In the meantime, if you’re interested in more details about the study itself, you can request a copy of the research and results directly from the Beddoes Institute.

So what do you think? When you look at your practice, how many communication channels do you typically use with your clients? Do you focus on using different channels for different client types? Are there any revelations for you in this research?

Excellent blog! Thank you for letting us know the benefits of customer communications management. Customer communication management plays a vital role in a business. It boosts customer experience and trust that will surely help your brank reputation and credibility. If you want to improve the customer communication of your business, I suggest to use the best customer communication management tool.

Your website is really cool and this is a great inspiring article. مكتب استقدام