Executive Summary

Last fall, the CFP Board formally announced its new Center for Financial Planning, a designated subsection of the CFP Board itself intended to help advance the financial planning profession. It’s stated vision was to become “the premier resource in the financial planning profession for educators, researchers, practitioners, financial services firms, and the public”, with a particular focus on cultivating the next generation of financial planners, enhancing gender and racial diversity amongst CFP certificants, and becoming an academic home for the financial planning body of knowledge.

From a financial perspective, the Center for Financial Planning was originally announced as being funded primarily from the CFP Board’s own operating budget, by outside sponsors (including a lead sponsorship from TD Ameritrade), and through the opportunity for CFP certificants to voluntarily donate. However, the CFP Board has recently begun "testing" a new CFP renewal process, defaulting every CFP certificant into a $25/year donation that amounts to a 14% increase in certification fees and “voluntary” organizational dues, or nearly $2M/year of new revenue for fund the CFP Board’s ever-expanding initiatives!

Although the Center for Financial Planning’s new initiatives themselves are laudable, the massive push by the CFP Board and its new internal entity for new revenue seems to put it on an ever-accelerating collision course with the Financial Planning Association, as their overlapping initiatives grow ever more redundant, and both organizations increasingly ask CFP certificants to foot the (redundant) bill.

Yet ironically, even as the CFP Board converges on the functions of a membership association and a certifying body, the reality is that the entire origin of the CFP Board was a spin-off from an educational institution (the College for Financial Planning) in the 1980s, in large part due to the fundamental conflict of interest that exists when the certifying organization also serves as an educator of its certificants and competes with the CE sponsors it oversees. Which means either the CFP Board has managed to entirely forget the roots from whence it came… or perhaps that it is continuing to groom the Center for Financial Planning as a spin-off membership association precisely because the leadership believe it is a way to work around the CFP Board's troubled past?

CFP Board Defaults All Certificants Into $25 “Donation” For Its New Center

As part of the certification renewal process, CFP certificants are required to obtain 30 hours of CFP CE credit every 2 years. Notwithstanding the bi-annual CE requirement, though, CFP certificants are required annually to pay a $325 annual (re-)certification fee.

Technically, the certification fee to fund the CFP Board’s core operations is actually just $180/year. But the annual assessment includes another $145/year for the “temporary” (but now repeatedly extended because it’s actually working) public awareness campaign. Thus in total, CFP Board's annual certification fee is $180 + $145 = $325 per year, ever since the CFP Board instituted its public-awareness-related fee increase back in 2011.

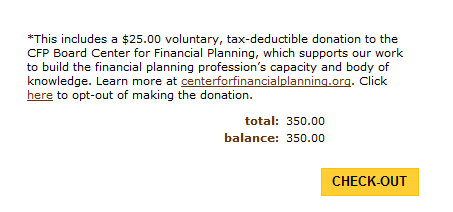

In recent weeks, though, reports have started to come in to the Nerd’s Eye View that the CFP Board has nudged their certification renewal fee higher, to $350/year instead. The $25 increase is being reported as a “voluntary, tax-deductible donation” to its new CFP Board Center for Financial Planning.

Notably, though, in what is now being characterized by the CFP Board as a "test", certificants weren't merely being given the option to add a donation to their certification renewal fee by checking a box to contribute. Instead, they were defaulted into the payment and automatically assessed a $350 total renewal fee when they get ready for the final Check-Out payment stage of renewing.

Notably, though, in what is now being characterized by the CFP Board as a "test", certificants weren't merely being given the option to add a donation to their certification renewal fee by checking a box to contribute. Instead, they were defaulted into the payment and automatically assessed a $350 total renewal fee when they get ready for the final Check-Out payment stage of renewing.

As the image to the right reveals with careful reading, there is a one-word link buried in the 5th line of the paragraph that indicates how to opt out of the “donation”. As we know, though, defaulting people in, and including an opt-out buried in the fine print, means that virtually no one will opt out, and most probably won’t even realize an extra assessment is being applied against them. Especially since there’s no clear check-box to check (or uncheck) to choose (or avoid) the “voluntary” donation.

And while it might seem minor, the ramifications of defaulting the entire base of CFP certificants into an extra $25/year assessment is significant. By the CFP Board’s latest demographics headcount, there are now almost 75,000 CFP certificants. So charging an extra $25 per person is a whopping $1.8 million in extra annual revenue!

In turn, the reality is that $1.8M of extra revenue is a massive potential increase in the size of the CFP Board, given that its core operations run on only $180/year certification fees (since the other $145/year is for the public awareness campaign). Or viewed another way, the CFP Board is now "testing" the equivalent of a 14% increase in renewal fees to fund the organization, without asking (or barely even telling) anyone.

To put the size of the payments in further context, the total national dues for the entire 24,000 member Financial Planning Association are only about $5.5M (plus about $1.2M of local chapter dues). Which means in one fell swoop, the CFP Board’s Center for Financial Planning in just its first year has default-contributioned itself into generating 1/3rd of the revenue the FPA spent the past several decades building up to! (And that’s before considering the Center for Financial Planning’s institutional sponsorships, which are already comparable to the FPA’s entire annual sponsorship revenue!)

What Is The Purpose Of The CFP Board’s Center for Financial Planning?

The fact that the CFP Board’s Center for Financial Planning has gone, nearly overnight, to an organization with multi-million dollar sponsors and nearly $2M of annually recurring “voluntary donation” dues raises the question once again of what the purpose of the Center really is, and what all this revenue is intended to fund.

As the CFP Board puts it, the Vision for the Center for Financial Planning is for it to be:

“The premier resource in the financial planning profession for educators, researchers, practitioners, financial services firms, and the public.”

The purpose of this broad-based vision for the Center for Financial Planning is to achieve the following Mission:

“The Center will build capacity for the financial planning profession by creating a sustainable supply of new and more diverse advisors to replace the retiring workforce, and by building an academic home to create a respected body of knowledge and support highly qualified faculty who will deliver job-ready financial planners from top colleges and universities.”

Accordingly, the CFP Board announced at the launch of the Center that its (initial) areas of focus would be on: “workforce development” (attracting and developing the next generation of financial planners); “diversity” (including both gender and racial diversity initiatives); and “building an academic home” (to advance the financial planning body of knowledge and support more qualified faculty to teach [undergraduate and graduate] CFP programs).

And in practice, these initiatives have already been manifested in a wide range of activities, either being implemented directly through the Center for Financial Planning, or having been previously done by the CFP Board but now being shifted to the Center. Current and proposed Center for Financial Planning initiatives include last year’s launch of the CFP Board Career Center, the Women’s Initiative (and a planned diversity initiative), updates to the Financial Planning Competency Handbook, and the announcement of a new academic journal to support financial planning academics looking for a place to publish financial planning research that can get them credit towards tenure.

Are The Financial Planning Association And The Center For Financial Planning Redundant?

While the reality is that all of the Center for Financial Planning’s initiatives are laudable, profession-advancing programs, it raises the question of why the CFP Board is pursuing them. After all, the FPA also has a job board, and a diversity initiative, and the Journal of Financial Planning, and an academic gathering at its national conference, and student chapters to help promote young people coming into financial planning (along with the NexGen community to support young planners).

All of which raises the question: at what point are the CFP Board’s efforts redundant to the FPA? Is it really necessary for the CFP Board to try to do what the FPA is already doing? Especially now that we as CFP certificants are being pushed to pay for these initiatives twice, once to the FPA through membership does, and then again by being defaulted into a $25/year dues-like structure from the CFP Board? Is it really healthy for both organizations to be pursuing these initiatives at the same time? Or a sign that one organization or the other is failing to do its part, forcing the other to try to pick up the slack?

After a prior article on Nerd’s Eye View raised the question of whether the CFP Board’s Center for Financial Planning and the FPA are on a collision course, the CFP Board made the claim shortly thereafter at the Financial Planning Association’s Chapter Leadership Conference that their positioning is “We mint them, [FPA] nurtures them” and that the CFP Board’s efforts were constrained to maintaining the CFP marks and building the pipeline of new CFP certificants.

Keller draws the lines between @CFPBoard and @fpassociation - "We mint them, you nurture them" #FPACLC pic.twitter.com/A2slqgHK59

— MichaelKitces (@MichaelKitces) November 21, 2015

Still, it’s arguably a sign of organizational mission creep for the CFP Board to be spending dollars and effort on building their pipeline of CFP certificants in the first place. It may be good growth business for the CFP Board, and certainly some organization needs to support the effort to attract future financial planners into the profession, but is it really part of the CFP Board’s core Mission?

The mission of Certified Financial Planner Board of Standards, Inc. (CFP Board) is to benefit the public by granting the CFP® certification and upholding it as the recognized standard of excellence for competent and ethical personal financial planning.

As the CFP Board’s mission reveals, it is meant to be the holder of the CFP marks and to uphold them as the standard of excellence. It was created to be the certifying body, not necessarily to do the self-interested ‘work’ of further growing its ranks, pushing for more racial and gender diversity in who holds the marks, or providing an academic home to the faculty who do financial planning research, or do whatever else the Center for Financial Planning’s “Design Summit” may suggest for the future. The mere fact that those are important things to be done for the profession does not mean it's the CFP Board's work to do.

In turn, perhaps the reason the CFP Board is trying to generate dues for the Center for Financial Planning through “voluntary, tax-deductible” contributions in the first place is because it already recognizes that trying to drive such an effort through its core certification fees revenue is so far off its core mission that it could threaten its 501(c)(3) status as unrelated business taxable income?

Is The CFP Board’s Mission Creep Driving The Center To Become A Membership Association?

Notably, the real concern over the CFP Board’s increasingly aggressive mission creep through its Center for Financial Planning is not merely its current initiatives, but where it goes from here.

After all, if the CFP Board can successfully layer on a $25 “voluntary contribution” dues payment for the Center for Financial Planning now, and quickly rack up nearly $2M of operating revenue, what’s to stop the organization from increasing its default “donation” to $30, $40 or $50 in another year or two? At what point is it an outright abuse of the CFP Board’s power to take 75,000+ CFP certificants who pay for the organization’s “core mission” and default them into millions of dollars of revenue for other off-mission purposes (however laudable they might be for some organization to do)?

Similarly, last month the CFP Board announced a new “Academic Research Colloquium for Financial Planning and Related Disciplines” to be held immediately preceding its 2017 Program Directors conference in February of 2017. Like the FPA Academic Track at their Annual Conference, the CFP Board’s Colloquium includes a Call for Papers to present, and will include “Best Paper Awards” prizes. Along with a “modest” $449 conference registration fee and sponsorship opportunities!

Given the scope of the event, already bringing together Registered Program directors and Academic researchers, the CFP Board's expansionary efforts raise the question of whether it will soon invite CFP practitioners to the event as well, to see the latest research, and perhaps earn from CFP CE credits. From there, a few practice management sessions might be included as well – to better bolster participation from CFP practitioners. Which in turn will attract more sponsors. The potential end result: in another year or few, might the CFP Board’s Center for Financial Planning start running its own National conference, in direct competition to the FPA (and NAPFA) national conferences as well?

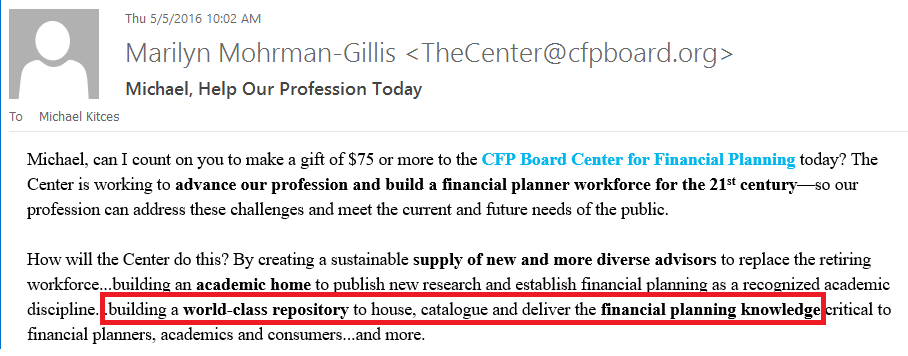

And with an ever-expanding Center for Financial Planning building out the “academic home” for the financial planning body of knowledge, there’s also the question of whether it’s only a matter of time before the CFP Board tries to reinstitute its ill-fated attempt to become a direct CFP CE provider. After all, the CFP Board has already begun to expand the description of its “academic home” initiative for the Center to include “building a world-class repository to house, catalogue, and deliver financial planning knowledge”. In other words, the Center for Financial Planning already seems to be positioning itself to be the CFP CE delivery vehicle the CFP Board tried and failed to be itself.

Has The CFP Board Forgotten Its Troubled Past?

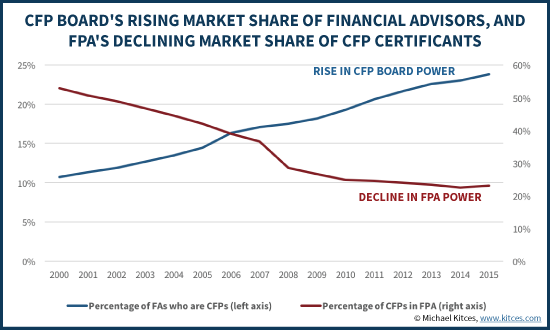

As the FPA’s share of CFP certificants (and thus its relevance to the profession) continues to wane, the CFP Board continues to expand in an ever-more aggressive manner towards the functions that a membership association typically fulfills. From reaching out to students, to building an academic home, and now building the base for what may soon become its own national conference and a platform to deliver CFP CE (which are core functions of a membership association, and what groups like FPA and NAPFA financially rely upon to sustain the organization in the first place), the CFP Board’s Center for Financial Planning increasingly appears to be the new arm of the organization to conduct all the membership association functions it can’t do (or isn’t “supposed” to do) for itself.

With the FPA’s declining reach, fulfilling the functions of a (competing) membership association is becoming a bigger and bigger business opportunity for the CFP Board. And one for which the organization has a distinct marketing advantage… because it controls and owns the list of CFP certificants who might be interested in attending for those CFP CE credits!

And ironically, the concerns of the CFP Board (or its Center for Financial Planning subsidiary) going into competition with membership associations to teach and train CFP certificants and offer CE credits isn’t merely a theoretical concern… because in reality the entire origin of the CFP Board was a spin-off from an educational organization after conflicts over being the sole organization that could grant the marks (and that the educational institution, the College for Financial Planning, didn’t want to be responsible for the enforcement of professional standards against its former students).

In other words, the whole reason that the CFP Board (then the International Board of Standards and Practices for Certified Financial Planners) exists as a standalone entity from where it originated (in the College for Financial Planning) was because it’s a necessary and crucial separation for a fundamental conflict of interest. Which suggests that the CFP Board would be well served to remember its roots when it comes to the importance of keeping the certification and enforcement body separate from the organization that teaches and trains CFP certificants. Unless, of course, managing the conflict through a potential spin-off organization is the whole reason the CFP Board is gearing up a separate Center for Financial Planning in the first place?

At a minimum, though, if the CFP Board really wants to expand its revenue base by extracting more dollars from CFP certificants to fund its expanded efforts, it should formally propose an increase in certification fees, and make the public case to CFP certificants for why we should pay for its (redundant) efforts as a part of the core operations of the organization. Because not telling anyone it's conducting a "test" and just defaulting certificants into a "voluntary" charitable contribution that amounts to a 14% fee increase just makes the organization look like it has something to hide.

So what do you think? Are the CFP Board's efforts through the Center for Financial Planning redundant? Should they be left to the FPA? Or is the FPA redundant and would it be better for CFP certificants to just pay the CFP Board to fulfill both certification and membership association functions?