Executive Summary

As the world moves increasingly into the digital age, technology-driven solutions continue to threaten the traditional way things are done, and the world of investment management is no exception, as numerous "robo-advisors" have cropped up in recent years with an aim to threaten and disrupt financial advisors. Yet the reality, at least so far, is that virtually all of the offerings are narrowly constrained to just portfolio solutions - where the world of mathematics and algorithms work well - with little capability of addressing the rest of an individual's financial picture.

But perhaps the biggest caveat of robo-advisor-driven solutions is that for many consumers, the real issue is not a cost-efficient portfolio solution, but managing the self-inflicted "behavior gap" where many investors, as a result of their own greed and fear, achieve inferior results. And it's not clear that robo-advisors will have any solution to these behaviorally-driven problems; just as a website that says "eat less and exercise more" doesn't solve the country's obesity problem (because it's a behavioral problem, not an information problem), it's not clear that robo-advisors and their portfolio construction recommendations will fare much better by providing information solutions for what are ultimately investors' behavioral challenges. Furthermore, at this point it's only the human advisors that address the entire set of comprehensive financial planning goals for clients.

Nonetheless, the reality is that a purely human solution isn't always better, either; many of the things advisors do can in fact be implemented far more efficiently with technology, and overall it's important to acknowledge that there are some things that humans do better but some things that really are done better by computers. Which means in the end, the real winner may not be the robo-advisors, nor the human advisors, but the technology-augmented humans - the cyborg advisors - who blend human and technology together into an optimal financial advice solution for consumers.

The Rise Of The Robo-Advisor

One major theme of recent years has been the rise of the so-called "robo-advisor" - online computer platforms that provides financial advice directly to consumers, mathematically analyzing the client situation to come up with portfolio recommendations. These companies, like Betterment and Wealthfront, claim the promise of less expensive and more accessible financial advice for the mass of consumers by cutting out the cost of the advisor.

Using the tools of modern portfolio theory, the robo-advisors have built algorithms to construct optimized efficient-frontier portfolios for their investors (assuming, of course, that you still trust purely quant-algorithm-based portfolio construction in the aftermath of the financial crisis!). Added on top of this portfolio construction advice are some additional value-adds that are conducive to technology scaling (and algorithmic analysis), such as effective asset location (at least if you have multiple types of accounts with the platform), automated rebalancing, and ongoing tax loss harvesting. Each of these features has been shown in separate industry research to potentially bring significant value to the table (although in many client situations, blindly implementing tax loss harvesting without an awareness of client circumstances can actually result in wealth destruction, not wealth enhancement!).

On the other hand, while they do leverage technology for some significant value-adds, at this point the algorithm-driven platforms are generally constrained to only analyzing investment portfolios. To date, no robo-advisors have implemented any algorithms to analyze a client's estate plan and help them understand how to best protect, manage, and distribute money to their heirs. Nor do any robo-advisors evaluate a tax return, or show clients what risks they are exposed to that need to be insured (and how much to insure them for), or coordinate retirement withdrawals with prudent tax planning and when to begin Social Security benefits, etc. In other words, robo-advisors at this point are little more than robo-investment-advisors; they do not compete with comprehensive financial planning, which remains a significant differentiator from commoditized passive strategic portfolio management.

Human Advisors Serving Human Clients

Notwithstanding the lack of comprehensive financial advice, the most significant fundamental problem with a robo-advisor-driven solution is that it assumes our problems are problems of information; if only we had more knowledge, and better tools, we could all achieve financial success. Therefore, as the business pitch goes, the robo-advisors will use technology to scale the solutions for this information problem, bringing quality portfolio solutions to the middle class.

Notwithstanding the lack of comprehensive financial advice, the most significant fundamental problem with a robo-advisor-driven solution is that it assumes our problems are problems of information; if only we had more knowledge, and better tools, we could all achieve financial success. Therefore, as the business pitch goes, the robo-advisors will use technology to scale the solutions for this information problem, bringing quality portfolio solutions to the middle class.

The caveat, though, is that most of our problems are not really problems of information. Having a website that constructs for all Americans a well-balanced portfolio and tells them to save more and spend less won't solve our country's financial woes, any more than having a website that constructs for them a well-balanced diet and tells them to eat less and exercise more would solve our country's obesity crisis. The problem is not one of information, knowledge, and technology-scaled execution. The problem is behavioral.

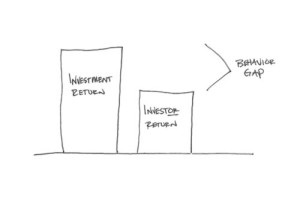

And behavioral problems are one thing uniquely suited to human-to-human interaction, as we seem to be hard-wired to feel more accountable to other human beings than we do to a computer. It's easy to just stop opening the statements showing your account balance or to stop logging into the website that shows you how badly your investments are doing; it's a lot harder to blow off an established personal relationship with a human advisor serving as your accountability partner. In fact, for years many advisors have suggested that their primary benefit is not designing quality portfolios, but helping clients stick with their portfolios and deal with the so-called "behavior gap" - the difference between the returns the investment markets deliver, and the returns investors actually earn after accounting for their potentially-poorly-timed decisions.

While it's not clear how large the behavior gap is for all investors in the aggregate - although DALBAR has tried to measure the phenomenon for years, its results are highly sensitive to the point of comparison - it's nonetheless clear that there is certainly at least some subset of investors who experience the problem. And for those investors - arguably the ones who need the most help, and are most likely to seek out a human or robo-advisor for assistance - it's just not clear whether a robo-advisor alone can talk them off the ledge while they're in the midst of panicking from a market decline, when there are no human beings to talk to at all (although to their credit, several of the robo-advisors have now hired behaviorists to at least try to tackle the problem). Similarly, it's not clear whether robo-advisors will be able to keep investors from just chasing returns in a bull market (nor is it clear whether the entire growth of robo-advisors in the first place is just investors chasing appealing short-term returns in the first place, as all of the robo-advisors have been established since the financial crisis and none have ever navigated a single bear market!).

The Advisor Of The Future - Not Just Robot Nor Human, But Cyborg

Notwithstanding the importance of having human beings to engage other human beings in their behaviorally-driven financial problems - in addition to the other wide range of tax, estate, insurance, retirement, and additional topics that comprehensive financial planners address - the reality is that while purely robot-driven solutions may not drive enough behavior change, purely human-driven solutions can be remarkably inefficient, which leads to higher costs for consumers and makes financial advice unaffordable for many. While there are some things that humans do far better than computers, there are also many things that computers do far more efficiently than humans.

This is one of the reasons why technology has been on the rise with advisors in their own firms as well. In fact, the aforementioned list of robo-advisor investment value-adds are not unique; most rebalancing software packages used by advisors, from iRebal to Tamarac to TRX, are capable of implementing some or all of this, from good asset location decisions, to timely rebalancing, to tax loss harvesting. Good advisors have actually been leveraging dedicated software and technology to provide all of these features for nearly a decade already since the first rebalancing tools came out, and long before the robo-advisors appeared on the scene! At best, the robo-advisors have simply repackaged (and perhaps done a better job at marketing and communicating) what the best human advisor firms already do (but without the rest of the financial planning advice)!

On the other hand, this kind of technology adoption thus far has been a best practice, not a standard practice. Not all advisors have embraced and implemented technology, as the latest technology survey from Financial Planning magazine revelead that nearly 70% of advisors still have not adopted rebalancing software in their practices. And the distinction is starting to matter, as a recent Fidelity industry study found that the practices of younger Gen X and Gen Y advisors are starting to outperform more established baby boomer advisory firms, larger as a result of their better, smarter tech use.

As time passes, it's becoming increasingly clear that the threat to human advisors is not technology and robots, but technology-augmented humans, bringing together the crucial relationship aspects of working with a human being with the scaled benefits of leveraging technology. This represents both the cutting edge of what many technology-focused advisors are doing now (as supposed by the Fidelity study), as well as recent venture-capital-funded start-ups like Personal Capital and LearnVest that pair technology and an online platform with real human financial planners to connect with (and thus aren't really "robo" at all). In fact, as I've written in the past, heavily-technology-augmented human advisors in a model like LearnVest may be a glimpse of how financial planning to the masses will be delivered in the future.

The bottom line, though, is simply this: in a competition between human advisors and robo-advisors, the real winner may be the technology-augmented human, which I am hereby dubbing the "cyborg" advisor - part human, part technology, integrated together to allow each part to do what it does best for the most efficient, most comprehensive, and most behaviorally accountable client solution!

Learnvest is close, but the best representation of what you are deceiving is NestWise.

Learnvest only works with clients virtuall and doesn’t offer investment advise. Nestwise really leverages technology to keep cost and price low in order to maximize accessibility, however Nestwise advisors are a hybrid of virtual meetings and local face to face meetings. Most Nestwise advisors don’t have high overhead offices but they will meet local clients at day use office space or even the clients home. Nestwise uses technology but still maintains a one-to-one client/advisor relationship. Thre is no robot produced cookie cutter one-size fits financial plans.

In a nutshell, Nestwise provides comprehensive financial planning and full service investment Management thru a hybrid virtual/ traditional model with high level of technology leveraged to keep the cost structure low while maintains a 1 on 1 client and Advisor relationship.

Hi Eric,

How long have you worked for Nestwise?

Michael. Let me add another level/question to the conversation.

What kinds of problems do people face and how are they different?

Understanding the definitions and the differences between the various problem types is important because:

•Different types of problems suggest different methods and tools to solve them

•Match them appropriately and greater value is created

•When they are mismatched, value is decreased

The Type Of Problem is part of the story. (TOP)

Planning has many levels or types of problems. Simple,complicated, complex,chaotic,etc

It’s not simple stupid. See chapter 6 my book ScenarioSelling- Technology and the future of Advice

…most firms/advisors start solving a problem before defining the type of problem and resources/experience/tools as part of the strategy 2nd.

All these cute little Gen X/Y start-ups and VC backed programs can pound their fists on the table all they want. At the end of the day the value of comprehensive planning is lost on the majority of middle class.

People are terrified of the markets and a recent survey even pointed this out in saying 80% are more comfortable talking about their own death. This fear cascades into other areas like insurance and estate planning.

#1 issue is not behavioral its educational. Champlain college does a decent job outlining how all of our fine states stack up when it comes to Financial Literacy:

http://www.champlain.edu/centers-of-excellence/center-for-financial-literacy/report-making-the-grade/results-summary

Planning for the middle class needs to start in the classroom before they move into the work force, otherwise its like talking to deer in headlights when it comes to their own financial future and retirement.

While I am a big proponent of financial education and more open discussion regarding investments, finance, and personal finance, I absolutely disagree that any of this is a “lost” on the majority of the middle class. There just weren’t enough good options available to the middle class. As this “new” segment of the market that offers low-cost and diversified portfolios with a more transparent investment process continues to the grow, there will be more and better options available to the middle class. This will drive more discussion, learning, and investing.

As for learning in the classroom, again big fan of more learning in the classroom. However, there is nothing that says learning has to stop outside of the classroom. Part of the industry’s role should be helping continue financial education and lowering the barrier to investing rather than making it an inaccessible field. Deer have eyes that are optimized for very low light (they’re crepuscular). So when a highlight beam strikes their eyes, they are essentially blinded and “freeze.” Rather than making the analogy that its like “talking to deer in headlights,” I think the analogy is that there is a growing segment of the market working on providing well-engineered sunglasses that will work when headlights shine. This will help you see, and keep you from being blinded by the headlights.

(Full disclosure: I am a co-founder of WiseBanyan, one of the Gen X/Y startups you reference.)

-Vicki

http://www.wisebanyan.com

Vicki makes a good point – planning should expand beyond the classroom. Essentially these new startups are filling the void left by traditional advisors. The industry – for good business sense – has ignored virtually everybody with less than ~$250K to invest. This has left a void for the robo-advisors to fill.

I’m not sure I understand Mr. Lucid’s point – should those who lack financial literacy not be presented with options? Should firms not be able to educate those about their finances? I see nothing wrong with a company like WiseBanyan explaining to people the benefit of investing diversified low cost ETF’s. To claim that people should not be able to do that because they are not educated enough seems pretty damn paternalistic to me.

I fully agree that the cyborg advisor will rule the day…but also think we’re going to be surprised by how quickly the technology component will evolve and which tasks it will excel at.

Turbotax certainly doesn’t handle all tax planning scenarios, but for the vast majority of Americans, it handles all of their needs. Similarly, I think it won’t be long before we see planning software that handles ‘holistic financial planning’ for most families. We’re seeing startups like FlexScore and Guide Financial that seem to be heading in that direction.

Similarly, I think we’ll be surprised with how powerful technology can be for behavioral change/decision-making. While pure information does little to make a behavioral impact, we’ve seen exercise and diet apps have a big behavioral impact for many, particularly when paired with a device (e.g. Fitbit). It won’t be long before a firm invests in developing a behavioral guidance engine to reinforce good behavior and push the clients to tweak unhealthy financial behavior. And that guidance can be personalized using account aggregation data. Mint.com already does a bit of this.

Further, companies can use human intervention at scale by having peer accountability, rather than advisor driven accountability. Again, we’ve seen examples of this with the various diet and fitness apps and sites.

Finally, I want to reiterate that I think your vision of cyborg advisors is absolutely right. I just wonder what tasks will ultimately land on the human…and thus what the ideal skill set of that human is. Because I think we’ll be surprised with how quickly the technology will evolve.

Hi Michael

One thing that hasn’t been discussed is the opportunity for open source technology to enable the cyborg advisor model.

Just like this website is built on WordPress, in my vision of the future, advisors will be able to build their wealth management solution on top of an open source platform. Just to name a few benefits:

– eliminate the extravagant % of AUM fees you have to pay to TAMPS or other portfolio management SAASs

– own your data and technology

– flexible, customizable, open

The question I’ve been asking is simple – “is fintech ready for open source?”. What do you think?

(full disclosure: I’m building a community around the exact solution I’m describing – http://wealthbot.io)

– Gene