Despite the fact that one research paper recently found Americans are more afraid of outliving their money during retirement than death itself, and economics research has long since shown that leveraging mortality credits through annuitization is an “efficient” way to buy retirement income that can’t be outlived, the adoption of guaranteed lifetime income vehicles like a single premium immediate annuity purchased at retirement remains extremely low.

In a recent new book entitled “King William’s Tontine: Why The Retirement Annuity Of The Future Should Resemble Its Past”, retirement researcher Moshe Milevsky makes the case that perhaps the primary blocking point of immediate annuitization really is its cost, and that guaranteeing mortality credits takes an unnecessary toll on available retirement income payouts (not to mention creating systemic risk for insurance companies if there’s a medical breakthrough!).

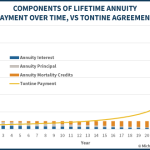

As an alternative, Milevsky advocates for an alternative retirement income vehicle, called a tontine. Similar to an annuity, a tontine provides payments that include both a return on capital and mortality credits stacked on top. The difference, however, is that with a tontine the mortality credits are not paid until some of the tontine participants actually pass away – which eliminates the guarantee of exactly when mortality credits will be paid, but also drastically reduces the reserve requirements for companies that offer a tontine (improving pricing for consumers).

Ultimately, it remains to be seen whether consumers would be willing to adopt a payment structure that involves getting more money for outliving your tontine peers. Yet Milevsky’s look through history reveals that tontine agreements have actually been very popular in the past, and nearly 100 years ago the use of tontines by Americans for retirement was similar to the adoption of IRAs today. Which means it really may not be much of a stretch to suggest that they should be brought back as a new form of retirement lifetime income vehicle for the 21st century as well!