Executive Summary

As a part of the resolution to the fiscal cliff, the American Taxpayer Relief Act of 2012 (ATRA) extended and made permanent a number of important tax code provisions that impact estate planning, including the now-$5.25 million estate tax exemption (after inflation indexing), and the portability of a deceased spouse's unused exclusion amount (DSUEA) to carry over some or all of that $5.25 million to a surviving spouse. The end result of these changes: married couples can shelter as much as $10.5M of net worth from the estate tax system simply by doing nothing more than leaving everything to a surviving spouse with a simple Will and filing an estate tax return.

The ramifications of these changes will significantly impact estate planning for years to come, as the higher exemption drastically reduces how many people will be subject to the estate tax in the future, and portability in particular renders the use of bypass trusts largely irrelevant. In fact, bypass trusts actually become an adverse strategy for many, given both the direct cash costs of trust drafting and administration, and the indirect income tax consequences like compressed trust income tax brackets and the loss of any step-up in basis at death.

While bypass trusts will still remain relevant in some situations, from their usefulness to shelter future growth from taxation for very high net worth couples and to preserve the GST exemption (which is not portable), to their utility for state estate tax planning. In addition, use of trusts in general will remain relevant for many non-tax reasons, especially asset, divorce, and spendthrift protection. Nonetheless, the bottom line is that with the new rules, esecpially portability of the estate tax exemption, it may be time to bypass the bypass trust for the overwhelming majority of Americans!

Estate Planning Before And After Portability Of The Estate Tax Exemption

Prior to the creation of portability, if a married couple who each had a $5M (or some other) exemption wanted to maximize their protection from estate taxes, they had to use a bypass trust (also known as a credit shelter trust). The concept was fairly straightforward - since your estate tax exemption died with you, it wasn't a good idea to just leave all of your property to a surviving spouse who would have all the family's property (from both the deceased spouse and the surviving spouse) but only the survivor's exemption. Instead, the deceased spouse would leave property not to the surviving spouse, but a trust for the surviving spouse's benefit, that was drafted in a manner that would keep the assets of the trust from being included in the survivor's estate.

Example 1. John and Betty are married and each have a net worth of approximately $4M (a total of $8M between the two of them). With a $5M exemption but under the "old" rules prior to portability, if John passed away and left all of his property to Betty, there are no estate taxes, as John receives an unlimited marital deduction for bequeathing property to Betty. She in turn would now have a total net worth of $8M, but unfortunately only her own estate tax exemption of $5M (because John's estate tax exemption died with him). As a result, if Betty passed away shortly thereafter, she would be subject to estate taxes on the last $3M of the couple's now-combined net worth (which would be subject to $1M+ of estate taxes depending on the rate in effect at the time).

Example 2. To avoid the preceding result of $1M of estate taxes, John could instead leave his property not to Betty, but to a bypass trust for Betty's benefit. Because the trust is separate from Betty and restricts her access to the funds, it will not be included in her estate in the future if she passes away (although the trust would typically be structured to still provide access to income and/or principal if Betty really needed it, such as for her basic health, education, maintenance, or support). As a result of using the bypass trust, Betty is only subject to estate taxes on her own $4M of assets, which are sheltered by her $5M exemption. In the meantime, John's decision to leave the money to a bypass trust would not be subject to estate taxes either; although John does not receive a marital deduction, because he didn't leave his assets directly to Betty, his own $5M exemption shelters his own assets anyway. The end result - the couple escapes all exposure to estate taxes by using a bypass trust.

Once portability of the estate tax exemption is available, the picture rapidly changes. Bypass trusts are suddenly no longer necessary, as a surviving spouse can inherit the deceased spouse's exemption along with his/her assets!

Example 3. Continuing the earlier examples, assume instead that portability is available to John and Betty. As a result, if John simply leaves all of his assets to Betty, she inherits not only his assets, but also his estate tax exemption. As a result, her net worth rising from $4M to $8M, but her total estate tax exemptions rise from $5M to $10M (or actually, $5.25M + $5.25M = $10.5M in 2013). The end result: Betty will not be subject to estate taxes on the property she inherited from John, regardless of the fact that there was no bypass trust used and all of the couple's assets were "stacked" in just her estate!

Thus, as shown in the examples above, in a world with estate tax portability, most couples simply do not need to use a bypass trust to shelter assets from estate taxes. Instead, the only thing that's necessary for even a relatively high net worth couple with $8M of assets to avoid Federal estate taxation is simply to ensure an estate tax return is actually filed in the first place; although recent Treasury regulations indicated those without any estate tax liability can file a simplified return, the fact remains that portability only applies if there is a Form 706 estate tax return filed.

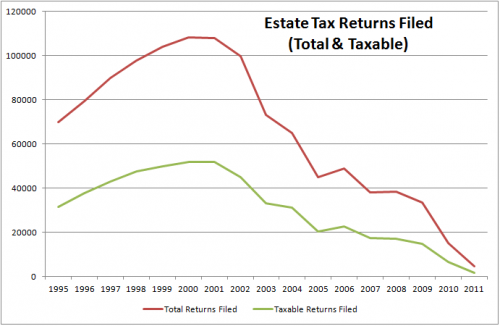

And notably, filing returns really may not be necessary for most Americans; as the chart shows below, the number of estates that even file returns, must less have any actual estate tax exposure, has fallen by more than 95% over the past decade or so, and now sits at no more than a few thousand estates total every year!

Downsides To Bypass Trusts - Losing Step-Up In Basis And Compressed Trust Tax Brackets

With the new rules, some planners have said "well, why not keep using a bypass trust anyway, just in case?" And in the early days of portability in 2011 and 2012, it was often appropriate not to bypass a bypass trust, largely because the portability rules themselves were still temporary and scheduled to lapse; as long as the client couldn't count on portability, bypass trusts were at least still a good precautionary measure.

Since the American Taxpayer Relief Act of 2012, though, portability of the exemption is now permanent, and the answer to the question "well, why not?" shifts. Not only is it often unnecessary to utilize a bypass trust to protect property from Federal estate taxes when the couple can simply file an estate tax return at the first death to preserve portability, but using bypass trusts can actually have negative tax consequences... not from an estate tax perspective, but from an income tax perspective!

For instance, assets can be eligible to receive a step-up in basis at death, but that treatment only applies to assets that are actually included in the individual's estate at the time of death. Consequently, leaving assets to a bypass trust - where the whole point is to ensure the property is not included in the survivor's estate - forfeits the potential for a second step-up in basis at the death of the second spouse!

Example 4. Harry passes away and leaves $1.5M of assets to a bypass trust for the benefit of his wife Joan. At Harry's death, the assets that go into the bypass trust receive a step-up in basis; however, when Joan passes away in the future, only Joan's personal assets will receive a step-up in basis, not the assets in the trust. On the other hand, if Harry had simply left his property to Joan outright, all of Harry's assets would have received a step-up in basis when he died, and another step-up in basis in the future when Joan passes away!

Unfortunately, the loss of a step-up in basis is not the only adverse tax consequence of using a bypass trust. In addition, a bypass trust typically requires the trustee to file an annual Form 1041 income tax return for any taxable income generated by the trust's assets that wasn't distributed to the beneficiaries. In a world where it only takes about $11,650 of income (in 2012) to reach the top tax bracket for a trust (not to mention the onset of the new 3.8% Medicare tax on investment income), the net impact is that most income will be taxed at top trust tax rates when (for all but the wealthiest of families) it could have been taxed at far lower tax brackets and potentially avoided the 3.8% Medicare surtax. The scenario can be exacerbated even further if an asset like a pre-tax retirement account is left to a bypass trust, where not only is there significant ordinary income passing through to the trust, but the ability to effectively stretch those distributions over time to defer the tax may also be adversely impacted, depending on the details of the trust beneficiaries (a problem that doesn't apply when the IRA is simply sheltered by portability of the exemption instead).

Notably, the challenge and impact of compressed trust tax brackets can be partially avoided by having the trust distribute its income to the beneficiaries (which means it will be reported to the beneficiaries on a Form K-1 and taxed on their personal tax returns instead), yet if the plan was to distribute all the returns of the trust to the beneficiaries anyway, there's even less reason to have used a bypass trust in the first place! After all, the growth will be in the survivor's estate anyway if distributions are being made, and the principal that was sheltered by the decedent's estate tax exemption could have been sheltered by simply porting the decedent's exemption to the surviving spouse anyway!

Beyond these adverse income tax consequences, including higher trust income tax brackets and the loss of a step-up in basis at the second death, it's notable that using an "unnecessary" bypass trust entails several outright additional costs, too. For instance, including the creation of a bypass trust in a couple's estate planning documents usually makes the documents themselves more expensive to prepare. And the ongoing filing of a trust income tax return for the foreseeable future also has a cost; after all, even if the trust distributes all of its income, there is still a need for an accountant to prepare the trust's Form 1041 and all the associated beneficiary K-1s, with the attendant costs. Of course, the trust also needs a trustee as well, which may have further costs if a professional or corporate trustee is necessary for additional oversight or management.

The bottom line is simply this: bypass trusts have costs, both in terms of direct dollar costs and indirect income tax consequences, which means if the trust wasn't actually necessary in the first place, using one anyway can actually result in less wealth for the family over time!

When Bypass Trusts Remain Relevant

Notwithstanding the prior discussion, it's notable that the bypass trust isn't rendered entirely useless in a world with portability of the Federal estate tax exemption. There are many scenarios where bypass trusts will remain relevant.

For instance, while the decedent's estate tax exemption is carried over to the surviving spouse with portability, it does not increase in the future, even though the assets it's intended to shelter may continue to grow. As a result, if a couple's assets exceed the combined estate tax exemption threshold, the bypass trust remains useful not just to use the decedent's exemption but to shelter their future growth from estate taxation.

Example 5. David and Mary each have $8M of assets. If David passes away and leaves his property to Mary, she will inherit his assets and his estate tax exemption, resulting in a total estate of $16M and a total exemption of $10.5M in 2013, with exposure to estate taxes on the last $5.5M. If Mary survives another 10 years and her assets double, though, her estate tax exposure rises dramatically, as her net worth increases to $32M, and while her personal exemption may rise from $5.25M (in 2013) to about $7M with inflation adjustments, David's exemption remains locked at the original $5.25M. With a total future exemption of $12.25M and a future net worth of $32M, Mary is subject to future estate taxes on a whopping $19.75M of estate taxes!

Example 6. Continuing the prior example, if David instead leaves $5.25M to a bypass trust and only the remaining $2.75M to Mary, and Mary survives long enough for the assets to double with growth, then in the future Mary will only have $21.5M in her own name (her $8M plus David's $2.75M, plus growth) and the bypass trust will have $10.5M of its own assets (excluded from Mary's estate). With a future inflation-adjusted estate tax exemption of about $7M, Mary will only be exposed to estate taxes on $14.5M of assets, instead of $19.75M from the preceding example. The end result - Mary avoided future estate taxes not on David's assets (which were sheltered anyway), but on the growth on David's assets after he passed away.

Notably, the preceding examples illustrate not only why the bypass trust remains relevant for those with a very high net worth in excess of the estate tax exemptions, but also for those who are merely close to those levels. For instance, if David and Mary had a combined net worth of $8M, the example would still be relevant; although they are not exposed to estate taxes today, with enough growth in the survivor's estate there may be an estate tax problem in the future, which could be partially mitigated by funding a bypass trust at the first death. In addition, if a couple's net worth is high enough that their estate plan includes any multi-generational planning, bypass trusts remain relevant for the purposes of Generation-Skipping Transfer (GST) tax planning, because the GST exemption is not portable as the estate exemption amount is.

For many couples with a net worth not anticipated to reach/exceed $10M+ of value, bypass trusts will continue to remain relevant not for Federal estate taxes but for state estate taxes, in the 20+ states that have decoupled and still maintain a state estate tax system, often with an exemption of no more than $1M. Notably, for many of these states a bypass trust isn't "necessary" to avoid estate taxes, as mere gifting strategies can be effective given current state estate tax loopholes; nonetheless, given the uncertainty of many gifting strategies, bypass trusts will likely remain relevant for most couples' state estate tax planning.

Of course, beyond all of this, the fact remains that estate planning using bypass trusts can remain relevant at nearly all levels of net worth if the driving reason for the trust is a non-tax reason in the first place, such as asset or divorce protection, control for spendthrifts, management and oversight of the assets themselves, etc. On the other hand, trusts in such situations arguably would not really be "bypass trusts" - in that the intent is not the estate tax savings of having assets bypass the surviving spouse's estate - but would simply be trusts using for various other planning purposes. In addition, it's notable that these rules changes do not impact the usefulness of revocable living trusts, which are intended not for estate tax savings but for privacy, probate avoidance, and to expedite the settlement and distribution of estate assets.

Ultimately, the reality is that the higher estate tax exemptions do not entirely render bypass trusts irrelevant. But the permanence of an inflation-adjusted $5M+ estate tax exemption, and portability of that exemption to a surviving spouse, will drastically reduce the need for using such trusts for Federal estate tax planning for all but the wealthiest of clients, or unique client-specific circumstances like a state estate tax issue, or a non-tax-related concern like asset, divorce, or spendthrift protection. For everyone else, though, it may be time to skip the bypass trust altogether, not only for its unnecessary complexity, but because the family may actually end out with more money in the long run but avoiding a bypass trust's adverse income tax consequences!

(This article was included in the Carnival of Wealth, Fictional Girlfriend Edition on Control Your Cash, the Carnival of Financial Planning on Master the Art of Saving, the Carnival of Retirement, and also Nerdy Finance #22 on NerdWallet.)

I have been asking estate attorneys if my clients that have bypass provisions in their trusts need to have them removed, and no one seems to have a good answer right now. Some of my clients have trusts that are written so the bypass (Or QTIP) trust receives enough funding to reduce the estate tax to $0, then another trust will receive the remainder funds. Still trying to figure out if they need to get rid of the QTIP provision… (this is for clients with $3-$4 million NW)

Since portability only carries over from the most recently deceased spouse, how are planners and attorneys addressing situations were remarriage is a possibility? Has any thought been given to this scenario?

Katie,

Thus far, I don’t know that a lot of strategies have been put forth yet.

Certainly, a bypass trust is one option, but bear in mind that remarriage isn’t actually a problem, per se. Imagine husband dies, leaving an exemption to wife, and later wife remarries husband #2. As long as husband #2 is alive, wife still has her exemption from husband #1. Even if husband #2 dies, if he leaves property to wife, then wife will STILL have an exemption (husband #2 will simply INCREASE wife’s exemption by overwriting husband #1’s exemption with a higher amount). The problem only arises if husband #2 dies first, AND either has used his gift exemption during life, or uses his exemption at death to leave the assets to someone besides the wife.

– Michael

Assets passing into a bypass trust are included in the decendent’s estate and should get a step up (if they’re non-qualified assets), or at least that’s what I was always taught. Maybe I’m missing something.

Also, the bypass has usefulness in states (like mine, NY) that have their own estate tax and the exemption is much lower than the federal exemption and there is no protability.

Amy Jo,

The point is not the assets in the decedent’s estate that go INTO the bypass trust. It’s that the assets are not in the SECOND spouse’s estate and receive no second step-up in basis.

For instance, with a bypass trust step-up occurs when husband dies and leaves assets to bypass trust for wife, but that’s it. Without a bypass trust, the assets receive a step-up TWICE – once at husband’s death, and then again at wife’s death.

– Michael

Ohhhh, got it, thanks!

I said this before on a previous thread but I am a remarried widow carrying a bypass trust from 2000 with which I have a love hate relationship. I hate the yearly tax return, I hate the high trust tax rate etc BUT I have loved the concept of the segregated growth. It is a bucket ( along with my 529s) – it feels like my children’s fathers gift to them but it was 625G that year so my assets are largely outside it (thank you Northwestern) Still, for me, portability is nirvana – I am so thrilled. I am about to re-do our documents since we moved to a new state and good bye ABC trusts etc.

The key is you are doing a bypass trust, going after that growth, is tax efficiency. In my time my then-Advisor had no concept but maybe now with only HNW seeking them there will be better treatment of clients.

PS Michael, I passed the November CFP

🙂

I know someone asked you about removing bypass trust provisions. Does it make sense for clients who are not going to be in an estate tax situation to redo their estate documents to remove the bypass provision if it will ultimately hurt them?

I assume that there is no way to close the bypass trust once the first spouse has passed away. It would be good to get the step up in basis on the whole estate if under $10M.

Charlo

I’ve been wondering real estate law firms in the event our clientele which have go around conventions into their trusts have to have all of them taken off, with out just one has a great reply at the moment. Several of our clientele have got trusts which have been prepared and so the go around (Or QTIP) rely on is provided with adequate finance to relieve the particular real estate levy to $0, after that a different rely on will obtain the rest resources. Nonetheless trying to figure out when they need to have to reduce the particular QTIP supply… (this is for clientele using $3-$4 trillion NW).

Starting a few years ago, some wills I saw included an option for a trust by the survivor disclaiming assets. That replaced trying to guess what Congress would do. And there is no question that out of date bypass provisions (for ex quoting exact amounts, or formulas) could have disastrous results.

Since no tax law is permanent, and the disclaimer decision is made after all the facts are known including even DOD, to me its looks like a good idea to have the bypass-disclaimer provision. It could assist with taxes, but it doesn’t ensure assets will eventually pass to children, since it’s voluntary.

Michael,

If a spouse died in 2004 and filed a Federal 706 form, does the portability that apply to the living spouse depend on 2004 levels or 2013?

Thanks,

Rich

If a couple has a AB trust and the first spouse died in 2012 with less than $5 million to their estate but the surviving spouse has close to $5 million and growing in their A trust, is it possible to access some of the unused spouses exemption through portability? In other words can the surviving spouse take advantage of portability though the bypass trust was in play and not completely used?

Thanks!

On whether the now-permanent portability rules will have an impact, check out Robert Denham’s blog post: Portability—Game Changer for Estate Planning or More of the Same?

http://blog.ceb.com/2013/10/07/portability-game-changer-for-estate-planning-or-more-of-the-same/