Executive Summary

One of the not-so-secret “secrets” of financial planning is that relatively few advisors actually generate the bulk of their income by getting paid for financial planning advice. Instead, despite the growth of financial planning in recent decades, the reality is still that most advisors get paid for financial planning through the subsequent products that are sold for implementation, or the subsequent assets they gather or retain through financial planning as a value-add.

And while arguably this is still not a bad way to build a business model around financial planning, the fact that financial planning remains rooted primarily in product sales and asset gathering has influenced – perhaps more than most advisors realized – the way that our financial planning software is built.

In fact, with its focus on investment accumulation (for retirement and college) and insurance-related scenarios, most financial planning software may be little more than a product sales and asset gathering tool shrouded in financial planning terms. Areas that are highly relevant for financial advice but not for product sales – from tax strategies to debt management to cash flow and budgeting – remain remarkably absent from most financial planning software tools available today.

Given that financial planning is a complex, intangible service that may be beneficial for clients but is hard for them to conceptualize, having tools to illustrate financial planning strategies, help clients adjust their behavior, and show the value of the advice we’ve delivered is essential. Yet in a world where most financial planning software remains so product-centric, have we progressed to the point where the financial planning software is not facilitating real advice, but limiting its growth?

The Product-Centric Roots Of Financial Planning

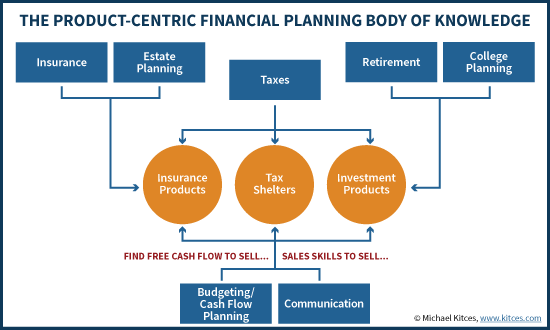

The reality of financial planning is that it was birthed from a world of selling insurance and investment products (and at the time, tax shelters as well). And since the core topic areas for the CFP marks are based on a job task analysis of what financial planners do – which in turn is based on what financial planners sell in order to get paid – it is perhaps not entirely surprising that the core topic areas of financial planning education are still based around the financial services products for which financial services professionals get paid.

After all, doing insurance and estate planning was quite effective at delivering insurance sales. Early on, most insurance agents were trained in helping people with their cash flow and budgeting as well, but only to the extent necessary to help them figure out how to “free up” monthly cash flow to pay for insurance premiums!

Similarly, college and retirement planning was/is popular because it supports the accumulation of investment portfolios, and the management of investment assets. And tax planning was an early pillar of financial planning because of the popularity of tax shelters in the 1970s and early 1980s – another way to gather assets at the time – and remains popular because of the tax planning benefits associated with various insurance and accumulation products (from tax-deferred annuities to tax-preferenced life insurance, to accumulating investments in 529 college savings plans and employer retirement plans).

Even many of today’s educational programs that teach “Communication” for advisors are most about sales and marketing skills to get paid for bringing in clients and delivering financial services products to them, rather than counseling and advice.

Product-Centric Financial Planning Software For Product-Centric “Advice”?

Given these roots of financial planning as being product-centric, it is also perhaps not entirely surprising that the focus of financial planning software is ultimately on showing the impact – the benefits – of the financial products that most advisors sell.

After all, retirement projections illustrate the ‘virtues’ of accumulating large portfolios (for advisors to manage), and provide targets for clients to save towards those portfolio accounts (which the advisor will be paid to manage). Insurance capital needs projections are built to show under-insurance shortfalls, to demonstrate that clients need to buy more insurance product coverage. Even “goals-based planning” strategies are ultimately all about how a particular financial services product or service (an annuity, a managed portfolio, a 529 plan, etc.) will fit into achieving the goal.

Of course, as financial services products and strategies wax and wane, so too does the particular focal areas of financial planning software. With the rise of the AUM model and baby boomer retirees, planning software has become more retirement-centric to illustrate the benefits of the advisor managing the retirement portfolio. As the number of people exposed to estate taxes has declined dramatically in the past 15 years, so too has the depth of estate planning modules in financial planning software been on the wane.

It’s Time For Financial Planning Software To Illustrate Non-Product-Based Real Advice!

The reason why this product-centric focus of financial planning software is so significant, is that while the software does a reasonable job of illustrating the tactics and products for which advisors are paid, it does a remarkably poor job of illustrating the impact of any advice that isn’t specifically product-centric. Which ultimately is very limiting for the ability of advisors to deliver – and show the value of – true comprehensive financial planning advice!

For instance, the reality for virtually any household is that long-term financial success is driven by spending and cash flow. A couple making $200,000+ can still be “poor” and living paycheck to paycheck if their spending is out of whack. And there are couples who make $100,000/year or less together and still manage to live frugally, diligently save, and accumulate a $1,000,000 nest egg. Yet despite the rise of popular consumer-oriented cash flow tracking tools like Mint.com and budgeting solutions like You Need A Budget (YNAB), the reality is that personal financial management software to help advisors track and advise upon client cash flow and spending has lagged painfully. Why? Perhaps it’s because giving advice about cash flow and budgeting means getting paid for advice, while most of the industry is still focused on getting paid for products or gathering AUM.

Similarly, while debt is a significant financial reality for most households, from relatively ‘stable’ and low-cost debt like mortgages and auto loans, to higher-cost debts like student loans and credit cards (or the increasingly popular peer-to-peer loan), and has a material impact on a household’s cash flows and career decisions, financial planning software has virtually no capabilities to effectively model debt and debt management strategies. Yet again, perhaps this is not surprising, given that financial advisors typically are not paid for “selling” mortgage products or debt consolidation strategies… even though effective use of those tools is essential for the financial health of most households!

At the other end of the spectrum, for those at higher net worth levels, often the biggest opportunity to generate cash flow savings is not from spending and debt management, but from tax strategies, whether simply maximizing available deductions, to tactically managing tax brackets from year to year with capital gains or loss harvesting and partial Roth conversions, to more proactive estate planning strategies like rolling GRATs and shifting asset appreciation outside the estate through a sale to an IDGT. Or even in the context of retirement, illustrating not just how diversified retirement assets will growth, but how to liquidate them systematically over time in a tax-sensitive manner (which accounts should you liquidate first, and when, and in what order!)! Yet in this case as well, because creating value for clients with tax-savvy strategies would involve getting paid for the (tax-related) advice itself, and not a financial services product, financial planning software has lagged in creating solutions to illustrate these strategies.

In fact, the notable trend amongst all of these categories is that, because they don’t relate directly to the sale of a financial product, they are often relegated to relatively simple assumptions – taxes are just assumed to be a general average effective rate or calculated in an over-simplified manner, spending is just measured based on gross spending with little detail of categories, and debt is just shown as a liability on the balance sheet and perhaps a committed spending obligation but with no tools to illustrate strategies to pay it down.

Yet the real problem is that in these areas of complexity and challenging behavior change, without tools to illustrate strategies and their benefits and outcomes, it’s incredibly difficult to get clients to engage! Especially when the reality is that behavior rarely changes at once, and that ultimately financial planning is an ongoing process, not simply a one-time event!

A Call To Financial Planning Software Providers To Support Real Financial Planning Advice

So what has to change for financial planning software to become more effective at actually illustrating and supporting the value of broader, real comprehensive financial planning advice?

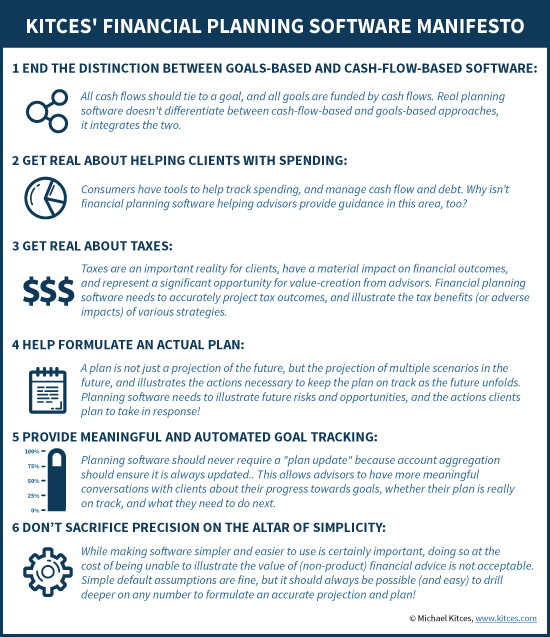

First and foremost, it’s time to end the increasingly meaningless distinction between “goals-based” and “cash-flow-based” financial planning software. The whole point of planning is to tie every cash flow to a goal, and a goal can’t be effectively evaluated without considering all of the relevant cash flows. In fact, just making a distinction between the two highlights the failure of integrating an accurate projection of cash flows to the goals they related to (whether it’s goals-based software that glosses too lightly over cash flows, or cash-flow-based software that gets so mired in the trees that advisors and clients can no longer see the forest!)!

Second, it’s time to get real about working with clients on spending (at least, those who are ready and willing to go there). Financial planning software needs to have capabilities for account aggregation not only for assets and account balances, but for cash flows from bank accounts and debit/credit cards. Few clients out there will ever take the time to manually account for their monthly cash flows, but the reality is that in today’s increasingly cashless society where almost all spending is digital, there’s no need to agonize over spending tracking. Technology can automate most of that process (and gets better every year). But financial planning software needs to gather that data, pull it into the software, and help us as advisors produce relevant insights and guidance for clients.

Third, it’s also time to get real about taxes. They are an enormous financial reality for clients, material to the long-term financial health and success of a plan, and grossly oversimplified in most financial planning software today. At a minimum, financial planning software should be able to take projected cash flows – particularly once spending is captured at a more granular level, as noted above – and be able to project a pro-forma tax return each year into the future, so that the true impact of taxes can be shown across the plan. But ultimately, it’s about more than just illustrating how a plan will play out in the future given the real impact of taxes. It’s about having tools to then illustrate the ways that planning strategies can alter those outcomes. If I project a client does a partial Roth conversion of $50,000/year throughout their 60s to mitigate the impact of taxes in their 70s, the planning software should show the benefit. If I’m going to recommend the client liquidate portfolios in a tax-savvy manner by harvesting gains in low-income years and losses in high-income years, planning software should show that benefit too. Planning software should be able to easily show year by year when tax rates will be high enough it’s best to contribute to a traditional IRA, and when rates are low enough that a Roth would be preferable.

Fourth, financial planning software needs to help us actually create a plan with clients, which means not only being flexible enough to show alternative scenarios on the spot, but also the ability to modify the plan in response to show how the client will get back on track. Don’t make planning software the equivalent of a flight simulator where all you can do is see the plane crash but have no means to practice steering out of the crash. The software tools should be capable of showing a baseline scenario, potential adverse events, and the successful strategies to respond to them. And of course, it wouldn’t hurt to be able to illustrate how clients will respond to unexpected positive events like a strong bull market, either!

Fifth, financial planning software makers need to embrace the reality that financial planning is a process, not an event. The entire idea of culminating in a single financial plan and then stamping it done is the equivalent of a general drafting a battle plan and then walking away from the battle, “secure” in the knowledge that the troops have a battle plan that tells them what to do… and ignoring the reality that the general needs to be there to help continuously guide and adapt the plan as reality unfolds. In practice, what this means is that financial planning software needs to update itself continuously (through account aggregation), and provide more meaningful ways for clients to track progress towards goals on a continual basis, and see the points at which they’ll have to adjust along the way, so they always know where they stand.

Sixth and final, while it’s true that detailed financial planning software of the past was clunky and cumbersome – and one of the virtues of early goals-based software was that it became simpler to use – ultimately the goal of financial planning software should be improving ease of use without throwing out the complex reality of our clients’ lives (and the planning opportunities that lie within). While making software easier to use is crucial – and there’s nothing wrong with starting out using simple default assumptions – not having the ability to drill down further, and sacrificing precision and compromising accuracy, should no longer be acceptable.

In the past, the reality is that financial planning software was little more than a behind-the-scenes calculator that “financial advisors” used to calculate and illustrate the impact their products would have in the client’s financial future. And while that process was fine for selling products – and meant that financial planning software only had to illustrate financial issues relevant to the associated products – if financial planning is to evolve into a full-fledged profession that goes beyond just products, so too much the financial planning software we use.

In the past, the reality is that financial planning software was little more than a behind-the-scenes calculator that “financial advisors” used to calculate and illustrate the impact their products would have in the client’s financial future. And while that process was fine for selling products – and meant that financial planning software only had to illustrate financial issues relevant to the associated products – if financial planning is to evolve into a full-fledged profession that goes beyond just products, so too much the financial planning software we use.

Ironically, then, one of the greatest challenges that comprehensive financial planners face today is that there are few financial planning software tools to actually illustrate non-product-centric financial planning strategies. The shortcomings of our financial planning software are becoming inhibitors to our growth as a profession. It’s time for a change.

So what do you think? Are you happy with the current state of financial planning software? Where do you think the gaps are? What do you wish financial planning software did different/better than it does today?

I am surprised that social security was not mentioned. It can be a critical component of (retirement) financial planning. And it can be pretty tricky too.

We launched a new financial planning application recently combining or “coordinating” Social Security, Medicare with a withdrawal strategy (withdrawal sequence, asset allocation, asset location, and tax minimization). We fit in the Income Drawdown and Tax Specialization categories defined in the blog. You can run partial Roth conversions to fill up tax brackets or to dedicated effective marginal levels. Go to http://www.IncomeSolver.com to check it out or get a demonstration. It is based on the academic studies Bill Reichenstein and I have published over the last 10 years.

Agreed! I would add one more item to the wish list: reasonable expected rates of return or the ability to change the return assumptions EASILY. I’m in the middle of comparing two of the larger (by market share) planning software packages.

One has the option to use Ibbotson historical or expected rates of return. You can also EASILY create your own expected returns and standard deviations for Monte Carlo (I use the low end of the Vanguard forecast for retirement plans).

The other product has historical returns wired in and not easily changed. Wade Pfau recently wrote that using historical returns borders on ridiculous (http://tinyurl.com/zo39jko). This products canned 60/40 growth portfolio has a 8% expected return (same as historical) vs. 6.3% for Vanguard (median return). It’s quite a job to change these assumptions in the software and I suspect that few do. Not surprising that the products “Getting to Know XXX software” videos start by showing you how you can quickly and easily see “your book of business”.

Further, I once had a couple in their late 70’s call. They were running out of money. They showed me their plan (from a broker dealer) that had a fixed 7% year over year expected return!

BTW, I’m an hourly, fee-only firm.

Amen! Retirees don’t need modules on saving for retirement or saving for college. What about factoring in Medicare/retiree health premiums? More on Social Security timing? Modeling reverse mortgage usage (like taking withdrawals in negative investment return years)?

Also, let’s not forget about modeling investment returns (like you recently wrote about). Let me show what a time period of lower returns followed by higher returns, overlaid with variable spending in the “go-go”, “slow-go”, and “no-go” phases of retirement.

There are so many ways that we, as financial coaches, could improve our clients’ financial behaviors if we could help them better visualize the consequences of their choices.

Elliott Weir

III Financial

I could not agree more!

Yes! As a tax-focused CPA building a fee-only practice as a CFP® & Accredited Financial Counselor to serve a moderate/middle income client base, I have to find or build stand-alone worksheets & tools all the time to do what I need. The only software I’ve looked at that’s even going in that direction is rightcapital, and it’s still in beta.

I agree. if you build it i will buy it.

Duly noted, Jeremy. 🙂

– Michael

Hi Michael- I couldn’t agree with you more. Large portions of my clients’ financial plans are detailed in notes and self-written executive summaries with all the details software doesn’t allow. Having the capabilities would save a lot of time and show how valuable my comprehensive, detailed fee-only planning services truly are.

Amen John.

It’s also ironic to me that the planning software doesn’t allow us to add in and overlay our notes and comments INTO their software output. So not only does the software have shortcomings, but we have to do our separate analyses, AND our separate write-ups and print-outs, and then collate it all together. Oy. :/

– Michael

I have been a financial software developer for about 25 years, with a primary focus on retirement. I agree with pretty much everything Michael has written here. BUT….

About 10 years ago, my company (which I will not name, so you won’t think this is an advertisement) introduced a planning product for older employees and retirees that pretty well meets all six criteria, plus several others that are not named. Within the realm of retirement issues, it was comprehensive, integrated, detailed, and user-friendly. There was also no market for it.

Financial companies were not interested precisely because it dealt with issues beyond what their employees and field reps were qualified to discuss. Financial planners were not interested either because it did too much of the work for them (inevitably in ways different from their own) or because it imposed a workflow that was not familiar and comfortable to them. Employers and other organizations did want to sponsor it because they didn’t want to pay for it or, even if the individual were to pay, to be responsible for endorsing something they didn’t really understand. Consumers did and sometimes still do license it directly, and a company with more financial resources than most financial software developers have might have made that into something, but it would mean not only advertising a better mousetrap but, what is much harder, explaining to people why they need something they have never heard of before. Apple can afford to do this sort of thing, but most of the rest of us can’t. And in the end, whatever “word of mouth” we received from customers who did like it, we did not achieve a referral threshold of more than one referral per customer, so maybe the product was not good enough, but it was damn good, so maybe it’s the concept that isn’t good enough.

I’m not saying that this approach could not possibly work, but we gave it a hell of a try, and spent a lot of effort developing, testing, and promoting such a product. So if anyone else out there is actually interested in pursing a similar development, feel free to get it touch with me and I can tell you a lot more about our own experience.

Chuck, maybe you were too far ahead of the times! If your product did what you say (and I have no reason to doubt it did), then please see if you can get a buyer to bite. That way, you get some coin for the efforts, a bigger player gets a head start on what Michael describes, and we planners who need it find our answer!

(fingers crossed)

Thanks for the vote of confidence, but the product is still out there, even though I have pretty much given up on it (we do have a smattering of individual customers, so we leave it up and running mostly for them), and there is no more interest now than there ever was. The reasons I gave why financial companies and individual professionals do NOT want something like this remain valid, as far as I can tell.

Chuck,

Thanks for the comment.

I won’t deny that the challenge around this kind of planning software is that SO much of the industry itself is anchored to product sales and distribution, that it’s difficult to get adoption. I’m not surprised large financial services firms were more interested in software that helps illustrate their products, than objective planning.

The dynamic with planners is a more nuanced one I think. Yes, software that does “too much” can feel like it undermines the planner, but I believe the path out from there is to make the software more like a tool we can use interactively and collaboratively with clients (rather than just ‘calculate the answer for us/them’), which supplements the advisor rather than implicitly (or explicitly) replacing them. See https://www.kitces.com/blog/designing-the-financial-planning-software-of-the-future-calculator-collaboration-tool-and-client-pfm/ and also https://www.kitces.com/blog/real-time-collaborative-financial-planning-and-the-evolving-role-of-the-financial-advisor/ for some further thoughts on the evoling nature and role of planning software itself…

– Michael

I agree that’s an important factor, Michael, but it didn’t dominate the feedback we received. The biggest issue, I sense, is the amount of data that needs to be input to do the job right. I hoped we had solved that by building the software in a way that would enable the client to do all the input, but then we were up against advisers having their own formats for collecting client data, which invariably were very different from ours. Plus they just weren’t used to working that way. Also, given that almost everything about our software was unlike anything they had seen or even heard of, I think they figured their own learning curve would be too deep.

My own sense is that the way to reform the industry is to get a tool like this into the hands of the public, because before long clients would start asking their advisers why they’re using such lame analytical methods when something so much better is readily available at a reasonable price. If we rely just on mutual competition and one-up-manship as an incentive for the financial industry, all we get are tiny steps forward, when in reality there are miles to go. Think how much progress has been made in the last 15 years, and weep. But if the public demanded a revolution, they’d get it. Unfortunately, it would take deep pockets to fund the necessary marketing campaign.

Chuck –

Working on developing financial planning software as I speak! I am a financial planner and not a techie, but I recognize a need in our own firm for the product we are trying to develop. Would love to chat with you and get a better understanding of your approach to your products if possible. I am in trying to ‘absorb’ as much as I can from as many sources as possible and sounds like you could be a valuable resource!

Would you be willing to chat on the phone or provide a way to get a hold of you?

Thanks,

Eric

Hi, Eric — I’d be happy to chat with you. Tuesday is not good for me, but I could be available pretty much anytime on Wednesday, Thursday, or Friday of this week. Pick a time and let me know at [email protected], and I’ll reply with my phone number. –Chuck

All great ideas that are available in some form already, but not yet all in a single solution. However, technology is the enabler and efficiency driver of what Advisors actually do, and there has not been broad market demand for tools beyond those supplementing the sale. Market feedback trends toward minimizing the effort rather than making it deeper. So the fun challenge is not to create functionality, but to match the deep calculation engine with the tools to intuitively match the input/output to the clients needs combined with the Advisor’s education and skill set.

I agree that automated goal tracking in terms of balance verification is helpful, but you also have to update the plan for actual versus recommended spending. It’s easy for a plan to derail if the spending plan goes awry!

Thanks, Michael! Ever since I started with American Express in ’95, we always wrote an executive summary. It is the prescription, where the software output is the blood-test and x-rays. You will always need both. A discerning advisor should always add commentary.

Hi Micheal, I do agree with you that financial planning software was originally “product-centric” and focused on helping advisors get bigger commissions, increase AUM, or both. However, I also believe that the modern financial planning programs and the growing list of collaborative tools can provide many of the benefits that you have outlined above. There are three elements that need to come together to make this a reality:

1. Deep integration across existing SAAS providers in the “plan & advise” space

2. Training specifically focused on the development, implementation, tracking, & adjustment of planning recommendations and

3. A Clearly defined and regulated Financial Planning Profession subject to the recognition, legal responsibility, and respect of related professions (Such as CPAs and Attorneys).

Many of us have taken on the Mantle of Financial Planner (Certified or otherwise) and work hard to provide the best service to clients. Yet, as you have pointed out in multiple posts, there is no legal definition for our role and clients don’t really know what our title means or entails. Clients still equate investment performance or insurance type to financial planning. A notion true financial planners still struggle to overcome. In addition, It seems (to me at least) that the education provided in formal planning courses are still structured around three key areas: retirement, investments, & risk management. the advanced planning methods techniques you share are seldom modeled in the classroom for new planners entering the field.

I think my point is that the technology already exists to provide the type of planning experience you describe above. The challenge may be to truly identify what financial planning is (beyond calling it a “process) and teaching Financial Planners how to actually build a financial plan.

Guardian has a product called The Living Balance Sheet does pretty much what you ask for. Though I have no affiliation with them and don’t use it. They were pretty pissed off when they lost control of eMoney. So they threw a bunch of resources at The Living Balance Sheet to make damn sure it didn’t walk out the door one day.

Michael, 100%… I am seeking a tool that works in South Africa. A challenge here is that there doesn’t appear to be appetite to develop other international tools to cope with local taxes, laws etc. and local software providers either don’t understand or can’t see the demand (because of the reasons you mention)

If anyone has ideas, please let me know… [email protected]

Brian,

You might check with Figlo (via Advicent). Last I heard, their chassis was built to accommodate and localize for taxes in many countries, and they may have (or be willing to build) towards a solution for South Africa?

– Michael

Thanks Michael,

Dave Kirkeby has been in touch already, having read my comment, and there is an offer for SA so we will chat next week.

Brian

Fantastic! Glad the blog could help! 🙂

– Michael

IMHO, budgeting and cash flow need a tight feedback loop with the client. Perhaps the advisor can add value at first to facilitate a plan, but beyond that I think a tool should be client-facing to give them the information and functions they need to manage it on a monthly, weekly, or daily basis.

This also changes *what* is made. Design that is user-centric is going to look less like eMoney and more like Simple.com’s “Safe to Spend Number”. Take user-centricity a step further and you get a tool that says, “I’ve monitored your cash flow and moved the excess into a money market fund for you. And — good news — since you set up your goals I can report you now have enough to buy that new bathtub.” That could be incredibly helpful, but I’m not sure there’s a role for an advisor there.

Victor,

Agreed on the importance of the tight feedback loop on budgeting and cash flow. This is the primary reason I’m such an advocate for PFM tools. They provide (or can provide) the technology to fill the gap on the feedback loop in productive ongoing cash flow monitoring and goal tracking.

– Michael

Michael, Thanks for the time you spent clarifying our needs. Question: Per MGP (which I use), it is now integrated with eMoney (which I am considering). How close does using both come to meeting what you described?

Rob,

It’s an improvement on the PFM side for MGP to pull in eMoney, but I’m still not sure either fully gets to all of these issues. For instance, both suffer with shortcomings around really facilitating cash flow conversations, real planning for adverse scenarios, etc. :/

– Michael

I’m a retired international tax attorney and CPA. When I retired I applied the skills gained over my career to creating a retirement model that I could use for my personal planning, which I have now used for several years. The model I created does everything that Michael suggests in his six point manifesto. I know my annual cash flow until age 100 under all relevant and material scenarios. The model computes the tax I will incur in each of the model years. I can easily adjust the model to take into account any perceived future spending changes in any year(s) for any purpose. The model is continually updated, and by hitting a hot key this morning I can see how today’s market drop affects the annual cash flow in the model.

Some financial advisors could set up and run such Excel models for clients, but why would they. It has less marketing appeal to the uninformed; it would take several hours to implement for each client; and it requires very good analytical skills. Since fees are typically set at a percentage of AUM, all of the financial advisor’s extra work and responsibility would bring no additional revenue.

John, they could be useful for advisers like me who don’t use the planning phase for marketing purposes, have analytical backgrounds, and charge a flat fee that isn’t based on AUM size. I’d happily spend several hours on each client if I could achieve the six points in Michael’s manifesto!

-Elliott

I completely agree with you. I have been a fee only financial planner for over 30 years. My business has always been planning around goals and objectives first and only implementing recommendations afterward. I don’t sell any products and this has worked very well for me over the years. In 1984 I looked at the Leonard Financial Planning software and was completely underwhelmed. There was no way to determining how they made the necessary calculations and and I constantly got different answers than when I did the calculations myself. However, it did create a lot of paper all aimed at selling various products. The result was that I created my own analyses using Lotus 123 to create schedules to help clients do real financial planning. In the last couple of years I have been drawn back into the search for financial planning software by the siren song of greater computing capacity along with the ease of aggregating information. We reviewed 2 of the big planning programs. We found a mistake in the investment return calculation in the first program that they were not even aware of. I started using the second program and continue to find mistakes in the programs. How about a program that does not give a client’s money market any cost basis so that taxable capital gains are generated when that money market is used. When pointed out, they said they were aware of the problem, but hadn’t done anything about it.

These are programs that are used by an enormous number of planners who apparently have never bothered to make sure the programs actually work. Again, they create fancy reports that are used blithely to sell products. The disclaimer even states “This report provides broad and general guidelines on the advantages of certain financial planning concepts and does not constitute a recommendation of any particular technique. The consolidated report is provided for informational purposes as a courtesy to you.” They readily admit that there are no recommendations and that it is for informational purposes only. How in the world is that considered “financial planning”? What kind of profession makes no recommendations and only supplies information? And yet, these programs are widely used.

Please keep pushing for software that does real financial planning.

Chuck, have you considered approaching the big designation houses, ie., American Society, CFP, OR NAEPC?

We are a professional carding team with a large ring around the globe. With

over 2 million ATM infe https://uploads.disquscdn.com/images/3e8a8f5e068e2575720b5da034d3c7ed241792169d1ad5eb12261c8dc1fa19fe.jpg cted with our malware and skimmers, we can grab bank

card data which include the track 1 and track 2 with the card pin. We in

turn clone this cards using the grabbed data into real ATM cards which can

be used to withdraw at the ATM or swipe at stores and POS. We sell this

cards to all our customers and interested buyers worldwide, the card has a

daily withdrawal limit of $2500 on ATM and up to $50,000 spending limit on

in stores.

Here is our price lists for the *ATM CARDS* *:*

*BALANCE: PRICE*

*$10,000: $500*

*$20,000: $1000*

*$35,000: $1700*

*$50,000: $2500*

*$100,000: $5000*

The prices include the shipping fees and charges, order now: Contact us:

[email protected]