Executive Summary

Helping clients through their estate planning is a core part of the financial planning process - and of course, the reality is that the orderly resolution of an individual's affairs after they pass away is an issue that long predates financial planning itself. Though the rules have changed significantly over the years and decades, the courts have long played a role in ensuring that property is distributed properly, albeit with some cases a bit more orderly than others.

Yet in today's world, a unique new type of property is being introduced for the first time: digital assets. In this guest post, financial planner William Bissett shares an example of a potentially problematic client scenario, where it's necessary to help a client through not only the traditional estate planning process for their "traditional" assets, but also to recognize that the matter has grown significantly more complex as clients must also resolve everything from online billpay to recovering photos from social media accounts.

Going forward, helping clients plan for their digital assets may become increasingly important as more and more of our lives are move (or at least are captured) online. Though the laws themselves are still a bit murky on how to handle such situations - and perhaps, because of that fact - it is crucial to at least help ensure that clients have an inventory of their various digital accounts and digital assets, to help surviving spouses and heirs to get through the process as smoothly as possible.

"We die only once…" - Moliere

It’s almost a 100% certainty that each of our clients is only going to die once (I would like to say that it is a medical certainty but I have learned that nothing is certain). However, the experiences that we learn from each of those can be used to help our surviving clients be better prepared for what lies ahead for their families.

In today’s day and age, it probably goes without saying that many of our clients lead complex lives. “The average user has 6.5 passwords, each of which is shared across 3.9 different sites. Each user has about 25 accounts that require passwords and types an average of 8 passwords per day.” That is from a study that Microsoft did in 2007 . I have not found a more recent study, but it’s hard to imagine the complexity has not increased.

Now think about the number of brokerage, tax-preferred, checking, savings AND now digital accounts that your clients have. Which monthly bills are paid through online bill-pay? How many online accounts do they have and where do they store their passwords? How many miles or points have they accumulated and what happens to those “assets”? Do they have significant media files through iTunes or Amazon? Do they maintain a blog with the subsequent services necessary to manage it? How is all of this tracked?

Meet Bill

Like many of us, Bill lives a complex life.

As Bill is driving to work, he calls the repairman to have him stop by his rental property to fix the kitchen sink. Before starting work, Bill checks his online bank accounts and pays the family bills. Then he starts writing his company blog post for the week.

After catching up on emails, Bill attends his weekly Rotary lunch and then returns to his office for afternoon meetings. During breaks, Bill checks his Twitter, Facebook and LinkedIn feeds – he is interested to see updates from his son and daughter who are both in college as well as his business contacts.

At day’s end, he reviews his Charles Schwab accounts, company stock options, and E-trade ‘trading account’. It was a good day in the market and after a brief view of the day’s increase he shuts down the computer.

But on the way home to see Mary, his wife, Bill loses control of his car and crashes into a tree. He’s severely injured.

Stop…. What happens next? Regardless of what happens to Bill (incapacity or death), is his family ready?

They recently updated their estate documents so the living will and advance directive are relatively new. The dispositive provisions on the trusts set up for the kids have been updated. The disability and life insurance policies were reviewed last year and determined to be more than sufficient in the event of a disability or Bill’s death. You could argue that we want to make sure that Bill’s auto insurance and umbrella policies are sufficient in case he was negligent in the wreck and hit someone else.

Does that take care of everything?

What about the ‘digital’ stuff? How does Bill’s family pick up the pieces of his digital life and utilize them in the estate settlement process?

Given all the information above (and more), how long will it take Mary and their two children to get their arms around all of Bill’s important digital information if he doesn’t survive the car crash?

What happens if Mary was with him in the car? Have they done all that they can do to allow the children to move forward if they are no longer here – or if they are in a hospital for months on end? Has their financial advisor guided them as far possible to plan for all of their estate needs?

Digital Issued Defined

Bill and Mary have a host of issues. Some of them we know and others we can assume. Let’s go through of a few of them:

- Does Mary know Bill’s password for his bank login so that she can pay “his” online bills (after all, bill pay is tied to the user login, not the account, so spouses can’t see each other’s online bill payments and banks do NOT typically release that information)? Even if she does, has she written down the bill pay accounts in case Bill’s user ID gets frozen before she transfers all the bills to her user ID?

- What about the login for Bill’s 401k and stock options, the 529 plans, his company health insurance plan and HSA account?

- Has Bill shared his username and ID for his blog? Who else has access/control?

- What are the passwords for his social media accounts?

- Did Bill keep an account with Snapfish, Flicker, or another photo sharing site?

- What are the terms and conditions for all the rewards points/miles that Bill has?

- How does Mary get in touch with the renters? Is there a list of providers that Bill uses for repairs? Where is the rental agreement? Is it in a Dropbox account or stored in the filing cabinet at home? How and when do the renters pay their rent – electronically or other?

- Does Mary have a working relationship with the professionals in their financial lives? Does she know how to get online to get access to important documents?

Plus many more that we can’t determine from the simple outline above and many potential ‘non digital issues’ that can be just as worrisome. But we can start to clearly imagine that Bill can simplify things for his heirs if he starts to inventory his digital estate in advance.

Password Sharing in the Digital Age

The simple solution to solve many problems is password sharing. This solves the online bill pay issue, transfers iTunes information to another user, allows family to use the miles/rewards programs of the deceased, and grants the family access to social media and photo sharing sites. It is a simple solution that works quite well... but it is illegal under most terms and conditions and the Stored Communications Act of 1986.

Tossing aside the fact that unauthorized access is illegal, passwords also change over time. You forget the password and have to do a password reset. Did that password get marked down and/or shared? If not, the information on those sites is lost. There are some services coming online as we write that will allow simple password sharing within your browser so you don’t have to remember each time you change your password – the browser and service will do that for you automatically. This may solve the password sharing problem that we have known for many years but we need to wait and see what they can and can’t do AND how much traction they gain with consumers.

The other downside to password sharing is the evolution of technology. My wife’s cousin recently passed away at the all too young age of 34. She left behind a beautiful family, loving friends, and a trail of people who were quick to say their last good-bye on Facebook. As I read stories of the impact that she had on people of all ages, I began to realize that Facebook likely already knew that cancer finally took her life. At what point, can they shut down her access because of that knowledge?

At what point, can other services monitor social networks and utilize the information to flag account access for “suspicious” activity – or any activity. It is likely that they can’t do it without legal repercussions, especially for the few times that they get it wrong, but it isn’t impossible to imagine a not too distant future where this is something that must be considered.

There is also reason to grow more skeptical every day about the long-term viability of password sharing. Apple is supposed to have a fingerprint scanner on their new iPhone 5S. Retina scans are getting closer to being a mainstream reality. And we already have two-factor authorization and challenge questions for trying to access a site from a new device.

All of this pushes us to the reality that planning to share your passwords is likely the best solution but it may not be a long-term viable solution. After all, if retina and finger scans become a near term reality, then how helpful is it going to be that Bill’s family knows his passwords are always 54321!Abc?

Legal Landscape for Digital Assets

But you are probably thinking to yourself that this doesn’t matter because the Executor or Personal Representative will gain access to the accounts with the death certificate and some other information, right? Well in some instances yes, but websites can – and do – easily hide behind the Stored Communications Act of 1986 in which unauthorized users are not allowed access to a remote computing service (RCS).

What is an RCS? If you read the definitions straight from the bill, you will learn it is the “provision to the public of computer storage or processing services by means of an electronic communication system” where an electronic communications system means “any wire, radio, electromagnetic, photooptical, or photoelectronic facility for the transmission of wire or electronic communications, and any computer facilities or related electronic equipment for the storage of such communications.” Feel better? Me either.

It’s no surprise that the legal landscape offers no real solution. There have been updates to the legislation since 1986 but there hasn’t been a comprehensive update. Consequently, there is a patchwork of rules in place that apply to computer technology as it was in 1986. The year 1986 sounds so, 1986 in the computer world and excludes so much of what we know today.

But unquestionably, your state leaders know how to handle this right? Mostly, the answer is no. Five states have gotten involved and passed some type of digital assets law. Unfortunately, two of those only deal with emails (Connecticut and Rhode Island). The other three, Idaho, Indiana, and Oklahoma address further concerns. What about the remaining 45 states? Virginia passed a law in July 2013 that gives parents access to their kids’ online accounts if their child passes away. That is a step in the right direction, but not quite where it needs to be. Another 18 or so states have introduced various pieces of legislation but they are being met with resistance from State houses – or the lobbyists influencing them.

Nonetheless, the states do recognize the need for this. The Uniform Law Commission has come together over the course of the last two years to start the process of recommending uniform legislation. While promising, there is still a long ways to go. First, they have to agree on recommended legislation which likely got tougher this summer when the ACLU wrote a letter critiquing the current proposed bill due to privacy concerns.

Once they finally agree on the legislation, each state will have to pass it on their own. All 50 states have come together on numerous occasions to pass uniform legislation they have also failed to do so on many occasions.

Gaping Hole or Just a Leak

The question that planners have to decide is whether or not this is a gaping hole or just a small leak in a steady ship.

After all, generations have survived the passing of information at death without any real concerns. Yes, the digital age has complicated it by adding passwords and usernames to social media accounts, but this shouldn’t be too big of a concern, right? After all, the executor will be able to access most of the important information and the rest of it will fall into place over time.

The alternative view is that maybe it won’t all “fall into place.” What if our client’s right to privacy is providing internet providers a shield to hide behind in NOT releasing this information? What happens if all of this information is hidden behind closed doors that are extremely difficult for our client’s families to access? Do our clients want their families to go through the additional stress of sorting through important information in the trying days, weeks and months after their death?

Addressing the Digital Estate

The issue is gathering the vast, and growing, amount of digital information that our clients are accumulating AND THEN helping clients maintain it. With the frequency that accounts are added and passwords are changed AND the way that we access our accounts from multiple devices the solution seems far from solved.

At the end of the day, the best way to prepare is to develop a comprehensive inventory of the client’s digital assets. Of course, you, the advisor, can’t have access to it because of custody issues.

But even that may be elusive from many clients considering how many accounts may be forgotten over time.

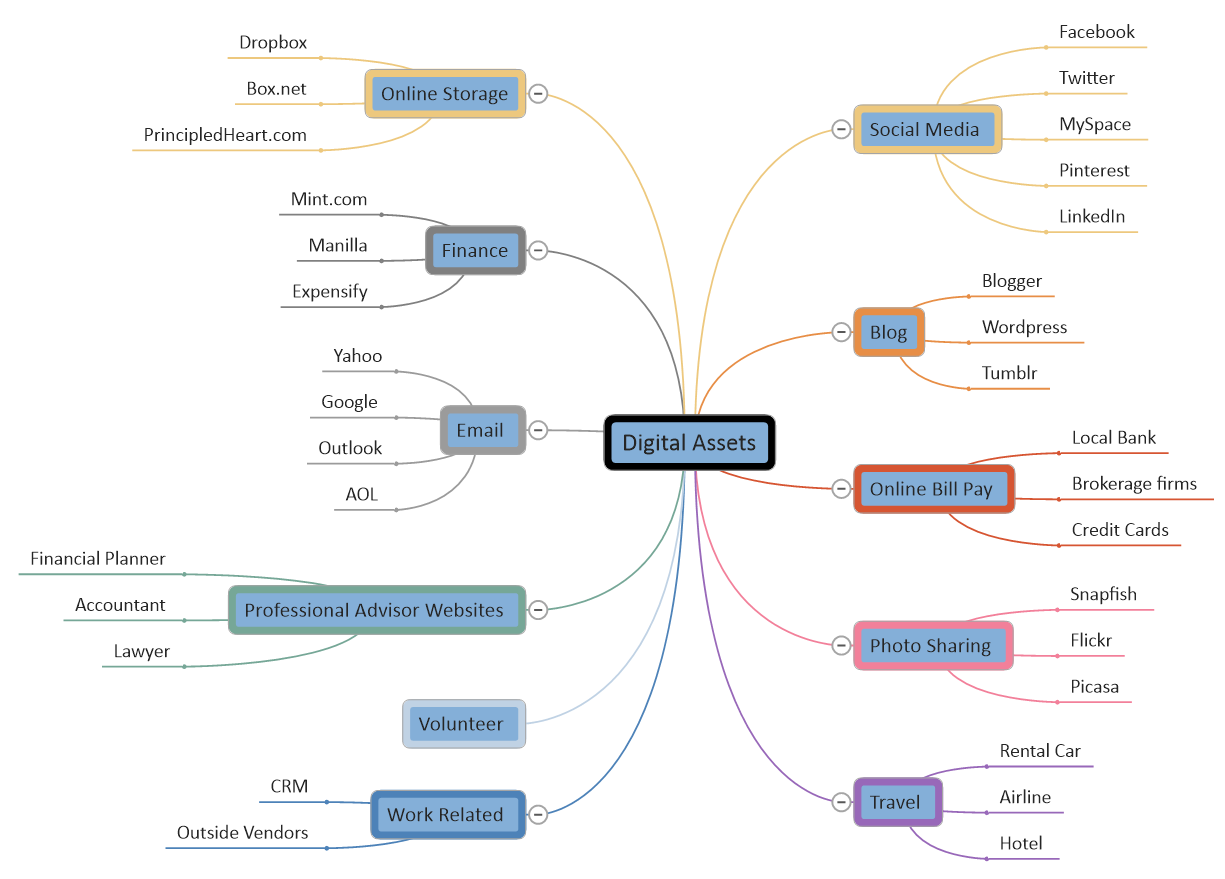

For that, sitting down with the client and a list of types of digital accounts would be useful. For example, you may find yourself with a MindMap (see right for example; click for larger image) that lists the popular – and unpopular – ways that we may “own” or “lease” a digital account.

For that, sitting down with the client and a list of types of digital accounts would be useful. For example, you may find yourself with a MindMap (see right for example; click for larger image) that lists the popular – and unpopular – ways that we may “own” or “lease” a digital account.

Obviously capturing the important ones is the goal, but some of the obscure ones can be just as relevant. For example, my passwords to the charities where we contribute annually are important because it contains a history of what we have done each year. Several of them also contain neat facts about where our money has gone that my family may want to see.

Clients will also have to decide how they are going to store these passwords. Are they going to use an online storage solution like Lastpass, PasswordBox, Dolphin, or the host of other sites that store passwords? If so, what are the terms and conditions for those sites? In other words, is ‘unauthorized’ access permitted or not?

If unauthorized access is not permitted, is the client going to store it in a spreadsheet? How will the spreadsheet be protected? How often will you remind the client to review the spreadsheet to make sure it is updated? Is there a back-up copy in case that gets lost? Who knows the location of the backup and how to access it?

If the solutions above are not right for clients, then what is? How about sticky notes? Do they store them in their head only? Or is there another system that works for them but maybe not for their heirs.

After helping clients understand the significance of cataloging their username and passwords to the various sites – which seems daunting in itself – the next step should be having them outline why each site is important. Clearly knowing about the online bill pay is more important than the username and password to the Baltimore Ravens Fan Forum, at least from February through July. Nonetheless, clients need to outline what is stored where and why it is important. If not, listing the accounts could end up creating more confusion than it solves.

Summary

Our job as financial planners is to help clients prepare for the future. We regularly talk about the clients’ goals and dreams. We talk about risk management and planning for the unknown. We ask them to plan the dispositive provisions for their children years in advance. We discuss utilizing life insurance to help the surviving spouse through the painful transition upon their death. We talk about education, vacation homes, retirement and endless future events.

It may be wise for us to start conversations around the total needs of the estate as well. It may not lead to any practical solutions for the client and their family. But at least you can know that you led the client down the path in a beneficial discussion. Alternatively, it could open another door to how they want to be remembered and what they can do now to make sure that goal is accomplished.

Given the complexity in today’s world, it is becoming clearer that this discussion is becoming just as important as the others as it goes a long ways to alleviating the stress of the family at its darkest hour.

Estate planning for digital assets is becoming more important and prevalent. It is good to be ahead of things on this. Good info.

Bill, thanks for the interesting article and helpful Mind Map that you use to start the conversation with your clients. This is an area of increasing awareness and I know that the estate planinng attorneys that I deal with struggle with this issue, too. As well as access to digital sites, there is the aspect of “owned” digital assets. That is, books purchased on Amazon or iBooks, video content from Netflix, Amazon, Vudu, etc. How will they pass to heirs? Lastly, the AICPA Advanced Personal Financial Planning Conference in January in Las Vegas will have a session on this issue.

Norm,

Thanks for your kinds words on this. I have really enjoyed learning about Mind Maps and using them more over the last 6 to 8 months. The actual assets that carry monetary value are very much an interesting problem. It’s amazing how this has crept up on us over the last couple of years and is now a very real problem for at least some of our clients. Gerry Beyer has been following this for several years and is involved with the Fiduciary Access to Digital Assets Act being developed by the ULC so his presentation in Vegas should be very good. Hope you enjoy it!

William,

Your article raises some interesting questions. Giving someone access to your digital accounts especially banking access can allow your agent to make payments that are not tracked by a signature under a power of attorney or even after the person is deceased. Just clicking to make a payment does not signal the same finanial responsiblity as putting your signature on a check. Nevertheless, we rountinely include digital assets in powers of attorney and trust documents. You need to discuss limits on the access with your agent. Great topic!

smberger41 – thanks for your contribution to the article. The current laws in place surrounding access to digital accounts does make it complex. It is something that clients aren’t usually aware of until its too late. If they understood part of the problem ahead of time, they could at least have discussions around the important items. They could also put legal documents in place that COULD help. It will be interesting to watch this develop from a legal perspective over the next couple of years.

It’s fascinating to see how estate planning has evolved in the digital age. The concept of “digital estate planning” has become increasingly important as our lives become more entwined with technology. It’s no longer just about tangible assets; it’s also about safeguarding our digital footprint.

Digital security vaults and digital vaults have truly become essential tools in this process. They provide a secure way to store not only financial assets like cryptocurrencies but also valuable digital assets like domain names, online storefronts, and cherished memories in the form of photos and videos.

The legal challenges surrounding the transfer of control over digital assets are significant, and it’s crucial for individuals to understand the limitations imposed by Terms-of-Service agreements. Simply sharing usernames and passwords is not a viable solution, as it may fall afoul of the law.

Legislative action to create a uniform legal standard is indeed a necessary step forward in ensuring that our digital assets are properly managed and passed on to heirs or designated individuals. In the world of digital security vaults, this legal framework becomes even more critical, as it ensures that the rightful owners can access and manage their digital treasures in a secure and legal manner.

As technology continues to advance, so too will the need for robust digital estate planning solutions like digital security vaults.It’s not just about protecting our physical wealth but also safeguarding our digital legacies for future generations.