Executive Summary

The United States tax system is set up on a “pay-as-you-go” basis, which means that taxpayers are required to pay taxes throughout the year as income is earned, whether it be through withholding income or making estimated tax payments. Individuals who don’t pay timely taxes throughout the year may be assessed Estimated Tax Penalties by the IRS, which are based on the amount of unpaid tax and the Federal short-term rate (in the first month of the quarter in which taxes were not paid) plus three percent. While understanding and helping clients comply with the requirements of tax payments can preclude Estimated Tax Penalties, advisors can also use simple arbitrage strategies to help clients maximize their savings when making estimated tax payments with tax-advantaged retirement account distributions.

While taxpayers who have income withheld to pay their tax liability generally aren’t required to make quarterly payments (as the IRS considers withholdings as if they were paid throughout the year, regardless of when they were actually paid), those who opt to make estimated tax payments must pay their estimated tax liability on a quarterly basis following a schedule of “General Due Dates for Estimated Tax Installment Payments” provided by the IRS. For taxpayers who choose to pay their taxes with estimated tax payments (versus through withholding taxes from paychecks or other qualifying accounts such as pensions or retirement plans), there are basically three options to calculate tax payments. Tax payments can be estimated based on the taxpayer’s prior year’s tax liability, where the estimated annual amount is equal to 100% of the prior year’s tax for income under $150,000, or 110% for income over $150,000, with the total estimated amount paid in equal quarterly installments. While this is generally the simpler way to calculate estimated payments (and more fool-proof in avoiding penalties, since the prior year’s tax will generally be known), individuals can also make estimated tax payments based on the current year’s tax liability instead. In this case, the amount due would be 90% of the current year’s liability paid in equal quarterly installments. The caveat to using the current year’s tax liability to calculate estimated tax payments is that, if the tax liability is underestimated, tax payments may be too low, and an Estimated Tax Penalty may result. The third way to make estimated tax payments is to use the Annualized Income Installment method, in which payments are based on the individual’s actual quarterly tax liability. While this method is cumbersome and time-consuming, it can be beneficial for taxpayers who earn income unevenly throughout the year.

Clients who pay their taxes by withholding income can benefit from the fact that quarterly payments are not necessarily required by the IRS. While paychecks are generally received on a regular basis throughout the year, resulting in withholding taxes in a true “pay-as-you-go” manner as intended by the IRS, retirement account distributions are often made only once per year, which effectively creates a “pay-as-you-go” loophole for taxpayers whose income consists of retirement account distributions! Because of this, advisors whose clients rely on retirement account distributions for income can help maximize savings by withholding taxes later in the year, thereby letting clients keep their money longer (and letting those funds grow in the meantime) without risk of incurring Estimated Tax Penalties.

For clients who may have inadvertently underpaid (or missed) estimated tax payments during the year, using an ‘erase-and-replace’ strategy can help them avoid an Estimated Tax Penalty by using a retirement account to withdraw the amount of underpaid estimated tax and withholding the entire amount from that distribution. The client can then ‘roll over’ non-retirement funds (that otherwise would have been used to make the estimated tax payment) within 60 days of the distribution to avoid any taxes due on the distribution itself, provided that no other rollovers have been made in the last year (so as not to violate the once-per-year-IRA-rollover ule).

Ultimately, the key point is that by leveraging the flexibility of tax withholding from retirement account distributions, advisors can develop strategies to help clients avoid tax penalties while keeping their money invested for longer and postponing tax withholdings until later in the year.

As many taxpayers are aware, the United States income tax system is a “pay-as-you-go” system. Accordingly, taxpayers are generally required to pay their income tax liability throughout the year as they earn their income, with any amounts owed upon the filing of an income tax return serving merely as a ‘truing up’ between what the taxpayer thought they’d owe (and paid in taxes throughout the previous year) and what they actually owe.

Notably, under IRC Section 6654, failing to pay income tax on income as it is earned – or poorly estimating the income tax due on such amounts – can lead to the imposition of what is commonly referred to as the “Estimated Tax Penalty”.

When it comes to taxes, the word “penalty” can instill a near-deathly fear in some clients, and often for good reason.

But when it comes to the Estimated Tax Penalty, the truth is that it’s really less of a ‘penalty’ and more of just an interest rate that Uncle Sam applies to payments that are not made on time throughout the year.

More specifically, IRC Section 6654(a)(1) stipulates that the ‘penalty’ is equal to “the underpayment rate established under section 6621.” IRC Section 6621(a)(2), in turn, provides that the “underpayment rate” is equal to the Federal short-term rate applicable in the first month of the quarter, plus three percent.

So, for example, if the Federal short-term rate in January 2021 is a hypothetical 0.25%, the Estimated Tax Penalty for Q1 of 2021 will be (an annualized) 3.25%. In essence, if the taxpayer keeps their taxes in their own bank account instead of Uncle Sam’s, then Uncle Sam charges for the amount of interest that the government could have otherwise earned (or in practice, not had to pay on other government debt that the government had to issue along the way because it didn’t have the tax dollars available to spend).

In terms of tax penalties, that’s not all that bad (and, in fact, if an individual can earn an after-tax investment return greater than the Estimated Tax Penalty, it can actually ‘pay’ not to pay, and to benefit from the arbitrage opportunity between their actual return and the implied currently-3.25% borrowing rate). Nevertheless, clients generally don’t like the idea of paying Uncle Sam any more than they absolutely must (and out-earning the penalty is still a bit of a gamble, especially over a short time period as the taxes are still due at the end of the year).

To that end, the sight of anything other than a zero when looking at the “Estimated Tax Penalty” line on an income tax return (Line 24 on the 2019 IRS Form 1040) can elicit cries of despair. Accordingly, helping clients minimize and potentially eliminate an Estimated Tax Penalty to determine the best way to pay those taxes is a valuable service that advisors can provide.

How To Avoid An Estimated Tax Penalty

For many individuals, estimated tax payments are a non-issue. For example, according to the Tax Policy Center, roughly 44% of all Americans have no income tax liability at all… which kind of makes paying for that ‘liability’ throughout the year pretty easy! For others, paying income tax on income as it is earned throughout the year is made seamless through automated tax withholding from paychecks (via their employer) or similar withholding from pensions and other similar sources of income.

Some taxpayers, on the other hand, earn all or a substantial portion of their income from sources that don’t (typically) withhold amounts for Federal income taxes. For example, income tax generally is not withheld on payments of interest, dividends, capital gains, taxable alimony, and, perhaps most commonly, self-employment income. Income tax is still required to be paid on this income, as it is earned, though. And often, those payments are made in the form of estimated tax payments.

Estimated Tax Payments

Thankfully, the pay-as-you-go nature of the U.S. income tax system has its limits, both in terms of the frequency that payments need to be made and how accurate those payments must be. Estimated tax payments, for instance, only need to be made at roughly quarterly intervals. So, even if a taxpayer receives weekly payments as an independent contractor, they need not send weekly payments to the IRS to account for the estimated income tax liability accruing each week. Rather, paying four times per year, at roughly quarterly intervals, is ‘good enough’ for Uncle Sam.

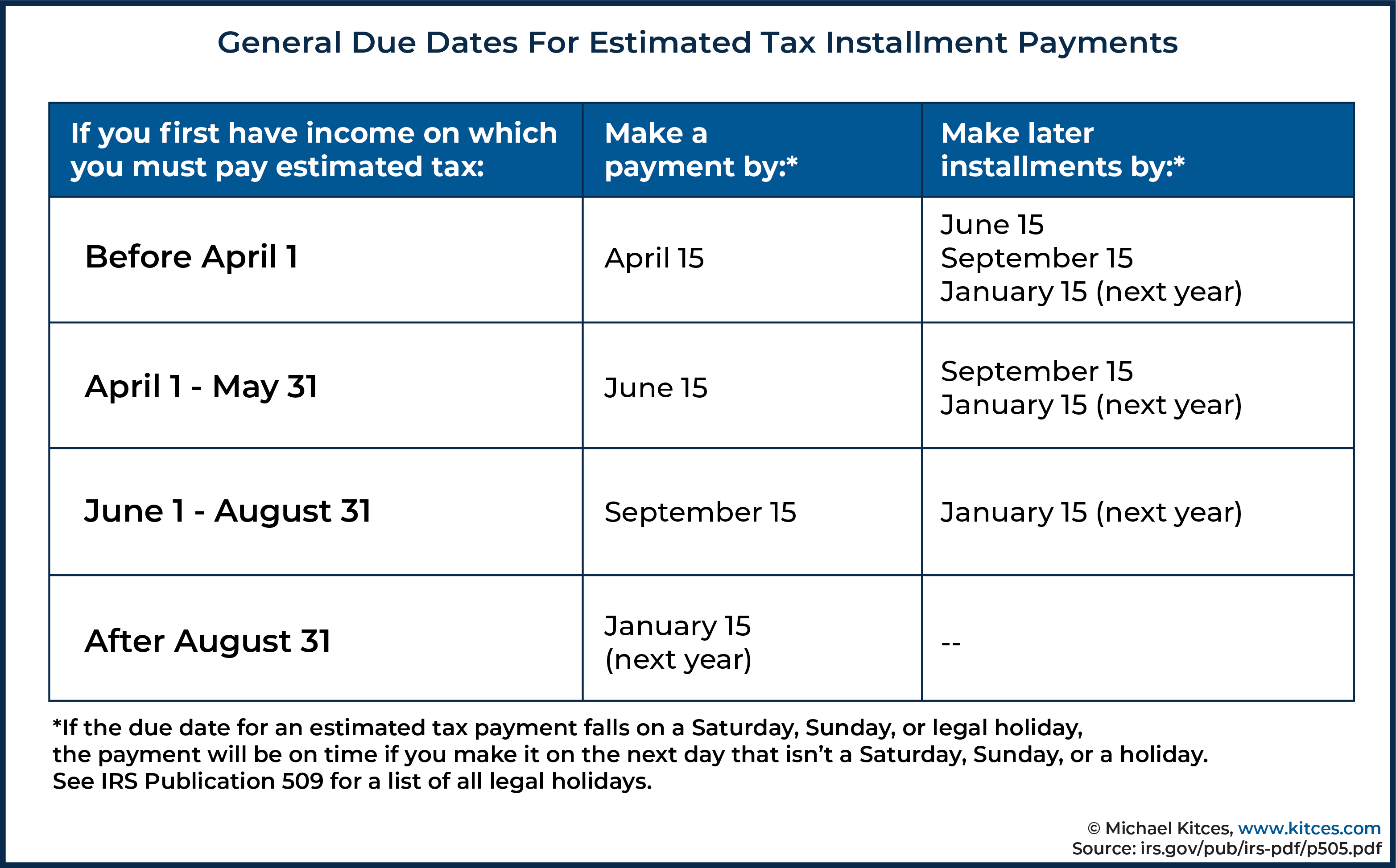

The deadlines for the four estimated tax payments for 2020 are indicated in the following chart/graphic.

While estimated tax payments are often referred to as “quarterly payments” (or sometimes, just “quarterlies” for short), the deadlines are not actually at quarterly intervals throughout the year. Rather, while there are three months (one quarter) between the prior-year Q4 payment due January 15th and the Q1 estimate due April 15th, as well as between the Q2 payment due June 15th and Q3 payment due September 15th, there are four months between the Q3 payment due September 15th and the Q4 payment due January 15th, and only two months between the Q1 estimate due April 15th and the Q2 payment due June 15th! These adjustments are made to help align estimated tax payments to other deadlines; in particular, so that the final Q4 payment doesn’t have to be made until the tax year is closed (after December 31st) when substantively all income and expenses will be known, and the first Q1 payment is due as of the tax filing deadline for the prior year (by April 15th) so any tax refund from the prior year can immediately be used towards the estimated tax for the new year.

Nerd Note:

Another favorable aspect of estimated tax payments is that they don’t necessarily have to be an accurate estimate of an individual’s actual tax liability for the quarter. Calculating each of the four estimated tax payments in such a fashion is allowed, using what’s known as the Annualized Income Installment Method, but doing so essentially amounts to filing a miniature tax return each quarter (to report that quarter’s income and deductions, and to determine the income tax liability for just that quarter).

Consider the time and effort it takes many individuals to file their income taxes each year and now multiply that by four! Couple that with the added professional costs that likely come with using the annualized method, and it becomes pretty apparent why so few taxpayers end up using it.

Nerd Note:

Use of the Annualized Income Installment Method for estimated tax payments is most beneficial for high-earners who often earn a disproportionate amount of that income late in the year, as the Annualized Income method allows them to delay the bulk of their tax payments until later in the year when that income is actually earned.

Instead of the Annualized Income Installment Method, taxpayers making estimated tax payments can choose to use one of two different ‘safe harbor’ methods. One method is calculated based on an individual’s prior-year tax liability, while the other method is calculated using the estimated current-year tax liability. Both methods, however, allow for simplified, equal payments throughout the year and, if used, will eliminate any Estimated Tax Penalty.

Calculating Estimated Taxes Using The Prior Year’s Tax Liability

The first safe harbor method of calculating estimated tax payments (to avoid an Estimated Tax Penalty) is to pay at least 100% of the prior year’s tax liability in equal installments.

Example 1: Sylvie is a single taxpayer who had an AGI of $120,000 for 2019 and a tax liability of $24,000.

Using the safe harbor method of calculating estimated taxes using the prior-year tax liability, Sylvie would have to pay $24,000 ÷ 4 = $6,000 in estimated taxes for each of the four quarters.

By doing so, Sylvie would avoid an Estimated Tax Penalty for 2020, regardless of how much additional tax she owes (if any) when her 2020 income tax return is prepared.

In the event that a taxpayer’s Adjusted Gross Income (AGI) from the prior year was more than $150,000 ($75,000 in the case of an individual who is married but filing a separate return), then instead of 100% of the prior year’s tax liability, the taxpayer must pay 110% of the prior year’s tax liability in equal installments.

Example 2: Jane and Arthur are married taxpayers who had $250,000 of income in 2019 and a tax liability of $32,000.

Accordingly, using the safe harbor method of calculating estimated taxes using their prior year’s tax liability, they would have to pay a total amount of $32,000 x 110% = $35,200, which would be broken down to $35,200 ÷ 4 = $8,800 in estimated taxes for each of the four quarters.

By making these $8,800 estimated tax payments each ‘quarter’, Jane and Arthur would avoid an Estimated Tax Penalty for 2020.

It’s important to note that using this safe harbor method of calculating estimated payments does not ensure that there will be no tax liability when an individual files their tax return for the year. Rather, it simply eliminates the potential for an Estimated Tax Penalty that would otherwise be due on top of whatever the taxpayer must pay to actually fulfill their full tax obligation.

Additional amounts can, and often are, still owed by the filing deadline, especially if the individual’s income has increased from the prior year or if deductions and/or credits have decreased.

Example 3: Recall Jane and Arthur from Example 2 above, who, based on their 2019 AGI of $250,000 and a tax liability of $32,000, are paying quarterly estimates in 2020 of ($32,000 x 110%) ÷ 4 = $8,800.

Now, suppose that on January 1st, 2020, the couple hits a New Year’s Powerball jackpot and wins $500 million, creating an additional tax liability of $185 million.

Jane and Arthur can still make quarterly payments of ‘only’ $8,800 for 2020 while avoiding any Estimated Tax Penalty.

Of course, the couple will have a massive tax bill come tax time in 2021 (for their 2020 income), but they can pay ‘just’ the $185 million comprising the additional tax liability from their jackpot winnings. No penalties (or interest) will be applied, even though they effectively underpaid their taxes by more than $184.9M!

In general, the method of calculating estimated taxes outlined above is the preferred method, and for a simple reason. A taxpayer’s prior-year tax liability is generally known or, at the very least, can be reasonably estimated by the time the first estimated tax payment for the year is due (April 15th).

Thus, calculating 25% of that amount (or in the case of a high-earner, 25% of 110% of that amount) should be little more than an exercise in basic math.

Calculating Estimated Taxes Using The Current Year’s Tax Liability

While calculating current-year estimated tax payments using the prior-year tax liability is essentially a ‘foolproof’ method (to the extent such a thing can be), the second method of calculating estimated tax payments to avoid an Estimated Tax Penalty is not quite as simple but still useful in certain situations. Under the second method, an individual is required to pay at least 90% of the current year’s tax liability in equal installments.

The problem with this method is that an individual’s current-year tax liability is often far from certain in the first place (since income is still being earned throughout the current year itself). That’s especially true for those who earn a substantial part of their income from investments and/or a business… which is also the group who most likely needs to make estimated tax payments in the first place!

Estimating the current year tax liability incorrectly can result in estimated tax payments that are too small, leading to a penalty. Thus, when practical, it’s best for clients to use the prior year’s tax liability method. But… it’s not always practical!

Example 4: Recall, once more, Jane and Arthur from Examples 2 and 3 above, who won a $500 million Powerball jackpot in 2020, creating a tax liability of $185 million.

Now, fast-forward to 2021. If the couple chooses to base their 2021 estimated tax payments on their 2020 tax liability – generally the preferred method – they will have to make quarterly payments of ($185 million x 110%) ÷ 4 = $50,875,000!

That’s probably not a great idea… unless, of course, the couple ‘plans’ to win another Powerball jackpot in 2021.

Suppose, then, that the couple estimates a tax bill of $10 million for 2021 (after considering the likely investment income generated from the previous year’s winnings). Instead of making quarterly estimated tax payments of $50+ million, they could simply decide to pay $10 million x 90% = $9 million of the 2021 estimated tax liability in equal installments, or $2.25 million per quarter.

If the couple’s $10 million estimate was accurate, they’d owe $10 million (actually owed) - $9 million (already paid as safe harbor) = $1 million in remaining taxes due when they filed their 2021 tax return. But there’d be no Estimated Tax Penalty!

While the example above is a bit extreme, it highlights the type of client who will most often benefit from calculating estimated tax payments using the 90%-of-current-year’s-tax-liability method… a taxpayer who expects a significant drop in income from the prior year.

Common situations when it makes sense to use the current year’s tax liability to estimate tax payments include when an individual retires, after the receipt of an unusually large bonus, after an unusually high-profit year, after a highly appreciated asset has been sold, or after making a large Roth conversion.

Tax Withholdings As An Estimated Tax Alternative To Avoid Penalties

As noted earlier, an alternative to making estimated tax payments is to pay taxes via withholdings from paychecks, pensions, etc. Typically, the nature of such payments is that they are made at regular intervals, and thus, taxpayers ‘naturally’ pay their income tax liability throughout the year. But when it comes to withholdings, it’s not entirely necessary that they actually be evenly interspersed throughout the year.

More specifically, IRC Section 6654(g)(1) states:

For purposes of applying this section, the amount of the credit allowed under section 31 for the taxable year shall be deemed a payment of estimated tax, and an equal part of such amount shall be deemed paid on each due date for such taxable year unless the taxpayer establishes the dates on which all amounts were actually withheld, in which case the amounts so withheld shall be deemed payments of estimated tax on the dates on which such amounts were actually withheld.

Translated out of legalese and into ‘English,’ IRC Section 6654(g)(1) provides that, by default, withholdings are treated as though they were paid in ratably throughout the year (tying to each quarterly payment’s due date), regardless of when they were actually withheld. However, if a taxpayer can prove when amounts were actually withheld, and it is to their benefit to treat the full amount withheld as paid in on that date, they may elect to do so.

Example 5: Khadgar is an employee of the Draynor Company and earns a salary of $60,000 per year. He also has substantial investment income of an additional $50,000 per year.

In 2019, Khadgar’s tax liability was $20,000, and it is expected to be the same in 2020. Accordingly, he should be paying income taxes of at least $5,000 per quarter in order to avoid an Estimated Tax Penalty.

Khadgar’s salary withholdings equal $3,000 per quarter, so in order to avoid an Estimated Tax Penalty, he generally pays additional quarterly estimates of $2,000.

Suppose, however, that Khadgar forgets to send his quarterly estimates for the first three quarters of 2020, and so as of September 16, 2020, he has only paid 3 x $3,000 = $9,000 from his paychecks in taxes for 2020 (instead of the $15,000 he should have paid so far).

He could simply write a check for $6,000 to catch himself up, but while that would help him prevent future Estimated Tax Penalties, he would still owe a penalty for underpaying his taxes in Q1, Q2, and Q3.

Alternatively, he could work with his employer to adjust his Federal income tax withholdings to have $11,000 of his Q4 paychecks withheld for Federal income taxes.

By doing so, Khadgar will have withheld a total of $20,000 for the year. And thanks to IRC Section 6654(g)(1), even though he will have withheld the majority of that amount from his Q4 paychecks, the entire amount will be treated as though it had been paid in ratably, throughout the year, in equal installments.

Thus, by using withholdings instead of an estimated tax payment, he will have eliminated what would have been an Estimated Tax Penalty for 2020!

It’s worth noting that in Example 5 above, the withholding ‘fix’ to the underpayment of estimated taxes earlier in the year only works if Khadgar is alive at the time the amounts are withheld. Any income that he was entitled to, but that he had not yet received prior to his death, would become Income In Respect of a Decedent (IRD) and would belong to his estate or another beneficiary. As such, the amounts withheld from those distributions would be withholdings for Khadgar’s estate or for his beneficiaries, but not for Khadgar himself.

Stated more simply, you cannot withhold income taxes for a decedent!

IRAs, 401(k)s, 403(b)s, And Other Retirement Accounts As Sources Of Estimated Tax Withholding

Using paycheck withholdings to satisfy one’s estimated tax liability offers some significant benefits when compared to using estimated tax payments… of which the primary benefit is simply that there is a clear cash flow from which taxes can be withheld, and in small enough increments (from each paycheck throughout the year) to minimize any cash flow disruptions. The challenge some individuals face, though – particularly retirees – is finding an income source from which taxes can be withheld when paychecks are no longer a part of the equation.

As when an individual is retired and does not have a salary from which to withhold income taxes, what other sources are there? Social Security benefits are one option, but what about those who have yet to begin receiving such benefits, or for those with tax bills that exceed the maximum amount that can be withheld from such benefits (a person can’t withhold more than 100% of their available income!)?

In such instances, distributions from IRAs, 401(k)s, and/or similarly defined contribution retirement accounts can provide the answer. As taking a distribution from an IRA (or other retirement accounts) is a simple way of creating income… from which taxes can then be withheld.

Tax withholding from IRA distributions is especially appealing because individuals typically have a significant amount of flexibility when it comes to electing the amount of taxes to be withheld on a distribution from retirement accounts. More specifically, when it comes to IRA distributions, IRS Regulations stipulate that 10% of IRA distributions will be withheld, as a default, for Federal income taxes. IRA owners, however, are able to opt out of this default and elect to have none of their distribution withheld for such purposes. Additionally, such persons also have the option to withhold more than the default 10% amount, should they so choose. And all of this can usually be done with a single, (relatively) simple form, or in some cases, with a few clicks of a mouse!

Similarly, while eligible rollover distributions taken from (non-IRA-based) employer-sponsored retirement plans, such as 401(k) and 403(b) plans, are generally subject to a mandatory withholding requirement of 20%, that is just the minimum amount that is required to be withheld from such distributions. Accordingly, an individual can generally elect to have anywhere from 20% to 100% of such distributions withheld for Federal income tax purposes.

Nerd Note:

Some states, such as Iowa, Kansas, Massachusetts, Nebraska, and Vermont generally require that state income tax payments be withheld from IRA distributions as well as any Federal tax withholding (with the precise amount required to be withheld varying from state to state). In such instances, the amount that can be withheld for Federal income taxes is generally the total amount of the distributions, less any tax amounts required to be withheld for state income taxes.

The ability to easily withhold all, or a large portion, of a retirement account distribution gives some individuals a simple way to eliminate the hassle of making multiple estimated tax payments by various deadlines throughout the year and replacing them with withholdings with a much simpler deadline.

Example 6: Upon completing his 2020 income tax return, Varian determined that he should be making estimated tax payments of $4,000 per quarter, for an annual total of $16,000, to the Federal government for 2021. Furthermore, he must take a total of $40,000 of distributions from his IRA in 2021 to satisfy his 2021 Required Minimum Distribution.

Here, Varian could certainly write a check for $4,000 to Uncle Sam each quarter in order to avoid an Estimated Tax Penalty. Alternatively, he could simply withhold $4,000 x 4 = $16,000 from his IRA distributions throughout the year. Notably, as withholdings, the $16,000 amount could be satisfied in a virtually endless number of ways. The only thing that matters is that the withholdings happen during 2021.

So, for instance, Varian could take quarterly distributions of $10,000 from his IRA and withhold 100% of the first payment and 60% of the second payment for Federal income taxes. Alternatively, he could take the two quarterly distributions without any withholdings and withhold 80% of the 3rd and 4th payments.

Alternatively, he could take monthly distributions from his IRA and withhold $16,000/$40,000 = 40% of each of the distributions.

He could even wait until December 31, 2021, and take one distribution of $40,000, and withhold 40% of that distribution.

It. Does. Not. Matter.

As long as, at some point during 2021, Varian withholds $16,000 or more from his IRA distributions (or from any other source), he will have no Estimated Tax Penalty.

Notably, though, in order for withholding from an IRA distribution to count towards estimated taxes for the year, it’s still important to actually do so before the end of the year! As while the Q4 estimated tax deadline is January 15th of the subsequent tax year, using tax withholdings to satisfy estimated tax obligations only counts if the income is paid (and the taxes are withheld) during the tax year itself.

IRA (And Other Retirement Account) Planning Strategies Using The Withholding ‘Loophole’

For some individuals, the combination of a retirement account and the withholding rules creates a compelling opportunity to maximize cash flow, reduce complexity, and/or even to ‘borrow’ from Uncle Sam for free (for a limited time) to create favorable growth arbitrage opportunities.

Of course, these strategies will make sense for some more than others. For example, a 65-year-old retiree looking to maximize Roth conversions during her ‘gap years’ (i.e., the low-income years between an individual’s retirement and when they begin to take Required Minimum Distributions (RMDs) from their retirement accounts and/or collect Social Security benefits) probably should not use up her ‘bracket space’ by taking voluntary additional IRA distributions just to be able to withhold from those distributions during these gap years (because it will reduce the amount that can be converted to a Roth IRA tax-efficiently).

But there are a variety of situations where using a retirement account as a (or the) source of withholdings is an absolute home run. Such situations include when individuals are subject to RMDs, or when they otherwise ‘need’ to take distributions from their retirement account(s) to meet living expenses… including taxes!

Using Withholdings To Create Tax-Free Government Loans To Win The Arbitrage’ Game’

As noted earlier, the U.S. is a pay-as-you-go income tax system, which is the reason estimated tax payments are required from certain taxpayers in the first place. Failing to make those payments in a timely manner throughout the year, as opposed to just before the April 15th tax deadline, can lead to an Estimated Tax Penalty, which, as noted, is really ‘just’ an interest rate. In essence, it’s simply the government’s way of accounting for the time value of money.

But two can play that game… at least when withholdings are involved. More specifically, by delaying estimated taxes earlier in the year and then utilizing tax withholdings to satisfy estimated tax liabilities later in the year, a taxpayer can hang on to their own money (and keep it invested and growing!) until the end of the year, rather than paying (and parting with their money) throughout the year. That swings the time-value-of-money benefit over to the taxpayer, essentially providing an interest-free loan from Uncle Sam equal to the estimates that would otherwise have been paid. This allows those funds to remain invested longer and (potentially) increase a taxpayer’s return.

Example 7: In March of 2021, upon completing her 2020 income tax return, Sera’s CPA calculates that for 2021, she should be making quarterly estimated tax payments of $10,000 per quarter. Sera will be 75 years old in 2021 and has an RMD of $40,000 (i.e., her total RMD happens to equal her total required estimated tax payments for 2021).

Up until this point, Sera has opted to receive her RMD in quarterly installments and has used the proceeds of her distributions to pay her estimated tax payments. While doing so is certainly an OK way of paying her tax liability throughout the year and will ensure she avoids an estimated tax penalty, it’s likely not the optimal strategy.

Rather, instead of taking quarterly distributions from her IRA and making regular estimated tax payments, Sera should consider waiting until later in the year to take her RMD and withholding enough of that payment to satisfy the year’s total estimated tax liability.

Suppose, for instance, that Sera earns a 6% annual return on her IRA investments. If she processes distributions from her IRA quarterly, beginning on March 31, 2021, and ending on December 31, 2021, she will earn a total of (($40,000 x 6%) ÷ 4) + (($30,000 x 6%) ÷ 4) + (($20,000 x 6%) ÷ 4) + (($10,000 x 6%) ÷ 4) = $1,500 in 2021 on her RMD/tax payments, prior to their distribution (throughout the year).

By contrast, if Sera waits to process a distribution of $40,000 that is 100% withheld for Federal income tax purposes until December 31, 2021, she will still avoid an Estimated Tax Penalty but will have generated $40,000 x 6% = $2,400 of earnings on her RMD/tax payments.

That's $2,400 – $1,500 = $900 more in Sera’s pocket than in Uncle Sam's!

Not to mention the fact that she can repeat this each and every year (until the year of her death) to take advantage of the interest-free loan that utilizing withholdings can provide (versus making estimated tax payments quarterly) to keep her funds invested as long as possible.

Is this strategy going to be the thing that makes or breaks the success of most clients’ retirement plans? Unlikely, but if the choice is between more money in a client’s pocket or in Uncle Sam’s, it shouldn’t be all that difficult of a choice!

Caveats To Structuring Year-End Distributions To Maximize Interest Earnings

While clients can potentially maximize their interest earnings by waiting until year-end to take distributions from their retirement accounts to cover their estimated tax liability, there are a couple of caveats to bear in mind.

First, waiting until December 31st of a year to process a distribution may maximize a taxpayer’s ability to hang on to their money for as long as possible, but it’s probably not the best idea. Many custodians, for instance, have policies that require individuals to submit year-end requests several days (or in some cases, several weeks) before the end of the year to ensure timely processing. Even where such requirements don’t exist, it’s probably best to process any such distributions by mid-December to ensure their timely completion.

Second, it’s worth noting that while keeping money invested longer tends to work out in an individual’s favor over time, it may not necessarily be the case each year. If, for example, investments decline during the year, playing the year-end withholding game can hurt a client.

For individuals sensitive to such concerns, advisors can simply liquidate the amounts as scheduled (e.g., on a quarterly basis) but hold such amounts in (relatively) risk-free assets, such as U.S. Treasuries or short-term CDs, for a ‘risk-free’ return arbitrage.

Using Withholdings To ‘Fix’ An Underpayment Of Estimated Taxes

Playing the withholding game can often be a win for those who have to (or plan to) take a distribution from their IRA or other retirement accounts anyway, such as for RMDs or for covering basic living expenses. The same strategy, though, is generally best avoided by others who don’t have the same distribution needs because taking retirement account distributions that aren’t otherwise needed would create an unnecessary additional tax liability (and a 10% penalty for those under 59 ½).

But as with most things when it comes to tax planning, there’s an exception to that rule when it would make sense to take a distribution to pay for estimated taxes, even if the distribution is unnecessary for any other reason. Here, the most likely exception to the rule is when an individual would like to fix an underpayment of income taxes (that would otherwise lead to an Estimated Tax Penalty) by using a retirement account and an “Erase-and-Replace” strategy.

Using The ‘Erase-And-Replace Strategy’

So what is the “Erase-and-Replace” Strategy?

Simply put, it’s a two-part process that not only allows an individual to ‘fix’ an Estimated Tax Penalty issue using an IRA or other retirement account but also eliminates any tax liability associated with the retirement account distribution!

Sound too good to be true? It’s not (at least not usually). Here’s how it works.

First, the individual takes a distribution for any shortfall in estimated tax payments that were not timely made during the year and withholds the total distribution. That erases the Estimated Tax Penalty.

Of course, now the taxpayer has another problem; a taxable distribution from the retirement account! Well, there’s an easy way to fix that. As long as it wouldn’t be a violation of the once-per-year IRA rollover rule, simply take the non-retirement-account funds that would have otherwise been used to pay the estimated tax liability, and roll them into a retirement account within 60 days, and you’ll complete a rollover! By replacing the funds back in a retirement account via a proper rollover, the income tax liability that would have otherwise applied to the distribution will be erased… but the dollars that were taken from the IRA to be withheld have still been withheld for tax purposes!

Example 8: Alex is a 45-year-old successful high-income business owner. For 2020, Alex’s estimated taxes were supposed to be $50,000 per quarter, but in the chaos that is 2020, she set aside the $200,000 in her brokerage account, but completely forgot to actually make her first three $50,000 payments (and the fourth is now looming large as well).

Thankfully though, Alex has a sizeable IRA and a tax-savvy advisor. Accordingly, on November 15, 2020, her advisor helps facilitate a $200,000 IRA distribution, of which 100% is withheld for Federal income taxes. The $200,000 total is enough to fully satisfy Alex’s estimated taxes for the year.

Of course, absent further action, Alex would now owe income taxes on the $200,000 IRA distribution, along with a $200,000 x 10% = $20,000. Hardly a winning ‘trade’ at this point.

But as the pièce de résistance, Alex’s advisor has her write a check for $200,000 to her IRA (or effects a journal to the IRA of cash from her taxable brokerage account for the same amount). Provided such action is completed in 60 days (and does not violate the once-per-year IRA rollover rule), Alex will have completed a successful rollover and negated the tax consequences of the original IRA distribution!

She will erase the Estimated Tax Penalty by using her IRA and has replaced the distribution in a timely fashion back in her IRA, which will eliminate the income tax and 10% penalty that would have otherwise applied to that distribution.

The U.S. income tax system operates on a pay-as-you-go basis. Accordingly, in order to avoid an Estimated Tax Penalty, a taxpayer must generally pay throughout the year, in some combination of estimated tax payments and withholding, an amount equal to the lesser of 90% of the current year’s tax liability, or 100% (110% if AGI was $150,000 or over) of the prior year’s tax liability.

But while estimated tax payments are treated as paid to Uncle Sam when they are actually paid, amounts withheld from income sources and directly paid to the government are afforded the benefit of being treated (by default) as though they were paid in, ratably, throughout the year regardless of when they were actually withheld (assuming they were withheld at some point during the calendar year).

Certain taxpayers can use this rule to their advantage by avoiding (or minimizing) estimated tax payments throughout the year, and instead, having large amounts withheld near year-end.

IRAs and other retirement accounts, in particular, can be excellent sources of withholding, as they can create instant income that can often be withheld entirely for Federal income tax purposes. This can create unique opportunities for certain taxpayers, including the ability to retain their own funds longer as an interest-free loan from the government to increase earnings and to fix an underpayment problem using the “Erase-and-Replace” strategy.

Ultimately, the key point is that while income taxes must generally be paid in throughout the year, savvy advisors and clients can utilize the special treatment afforded to withholdings to simplify their lives and improve outcomes.