Executive Summary

Credit cards are ubiquitous in the United States, and financial advisory clients are likely to have at least one in their wallet. And while many consumers may know about the rewards they earn on the credit cards they hold, they might not be aware of the opportunities that maximizing their rewards could offer. In fact, through a combination of credit card sign-ups and regular spending, individuals can earn thousands of dollars in cash back rewards or travel benefits each year. Accordingly, financial advisors have an opportunity to provide significant ongoing value to clients by investing the effort into helping clients find the best card(s) to maximize rewards based on their personal spending habits.

Credit card rewards come in three types: cash back, travel points/miles, and transferrable points that can typically be used for either cash or travel. Each of these can be appropriate for different types of clients. For example, clients who crave simplicity or have little interest in travel might find cash back rewards most useful. Other clients who are accustomed to economy-class airfare and only dream of flying in business or first class may want to maximize travel credit card rewards instead, to get an experience that they would not be able to have otherwise!

Rewards can be earned through sign-up bonuses and regular spending with the card. Credit card sign-up bonuses (which can be worth more than $1,000 in cash or travel expenses per card) are the fastest way to earn rewards, typically offering a bonus for spending a certain amount of money in a given period of time. For regular spending, credit cards either offer a fixed rate for spending on the card (e.g., 2% cash back for all categories of spending) or a variable rate based on the particular category of spending (e.g., 4% cash back for every dollar spent on travel, or 3% cash back for every dollar spent at restaurants).

For advisors, cash flow discussions with clients can be a good opportunity to broach suitable credit card reward programs. Advisors can discuss not only what clients are purchasing, but also how they are paying for those purchases. This can reveal important information to help advisors craft a sensible rewards strategy for clients, including the client’s regular credit card spending (to gauge their ability to meet spending requirements for sign-up bonuses), which categories of purchases (e.g., groceries, gas) they make most often (to find cards that offer bonus rewards in these categories), and whether they are planning any large one-time expenses (that could be used to meet sign-up bonus spending requirements by themselves).

In addition to understanding a client’s spending patterns, it is also important to gauge their interest in managing credit card rewards on an ongoing basis. While some clients might be interested in applying for multiple new cards each year to build up points and miles through sign-up bonuses, others might be less interested in applying for cards and would instead prefer earning rewards on a single card. Either option can be profitable for the client, so it is important that they are comfortable with the process (so that it will be easier for them to stick to the strategy in the first place!).

Ultimately, the key point is that working with clients to devise a credit card spending strategy that maximizes available rewards can help advisors demonstrate ongoing value to attract and retain clients. Because, at the end of the day, what client wouldn’t want to work with an advisor who can help send them on a ‘free’ vacation each year?

Cash flow analysis is a fundamental part of the financial planning process for advisors and their clients, so understanding all of a client’s income sources and expenses – and being able to project realistic changes to these factors in the future – are important variables in creating a meaningful plan and making recommendations. But while part of the financial planning process focuses on how much the client is spending and what they are buying, it does not necessarily consider how they are making those purchases and whether spending habits can become more efficient.

While some clients might use methods that offer little in terms of rewards for their spending, such as cash, a no-reward debit card, or even paper checks (!), by maximizing the value of credit card rewards, clients can actually earn thousands of dollars’ worth of cash or travel each year for their regular spending!

While maximizing credit card rewards does require some effort to determine the best card(s) for a given individual, financial advisors who help clients do so can nonetheless provide significant ongoing value to clients and drive loyalty by helping them optimize their spending with a credit card spending and reward strategy. Because after all, what client wouldn’t want to work with an advisor who helps them earn thousands of dollars – or even a free trip to Europe or Hawaii – each year!?

Types Of Credit Card Rewards And How They Are Generated

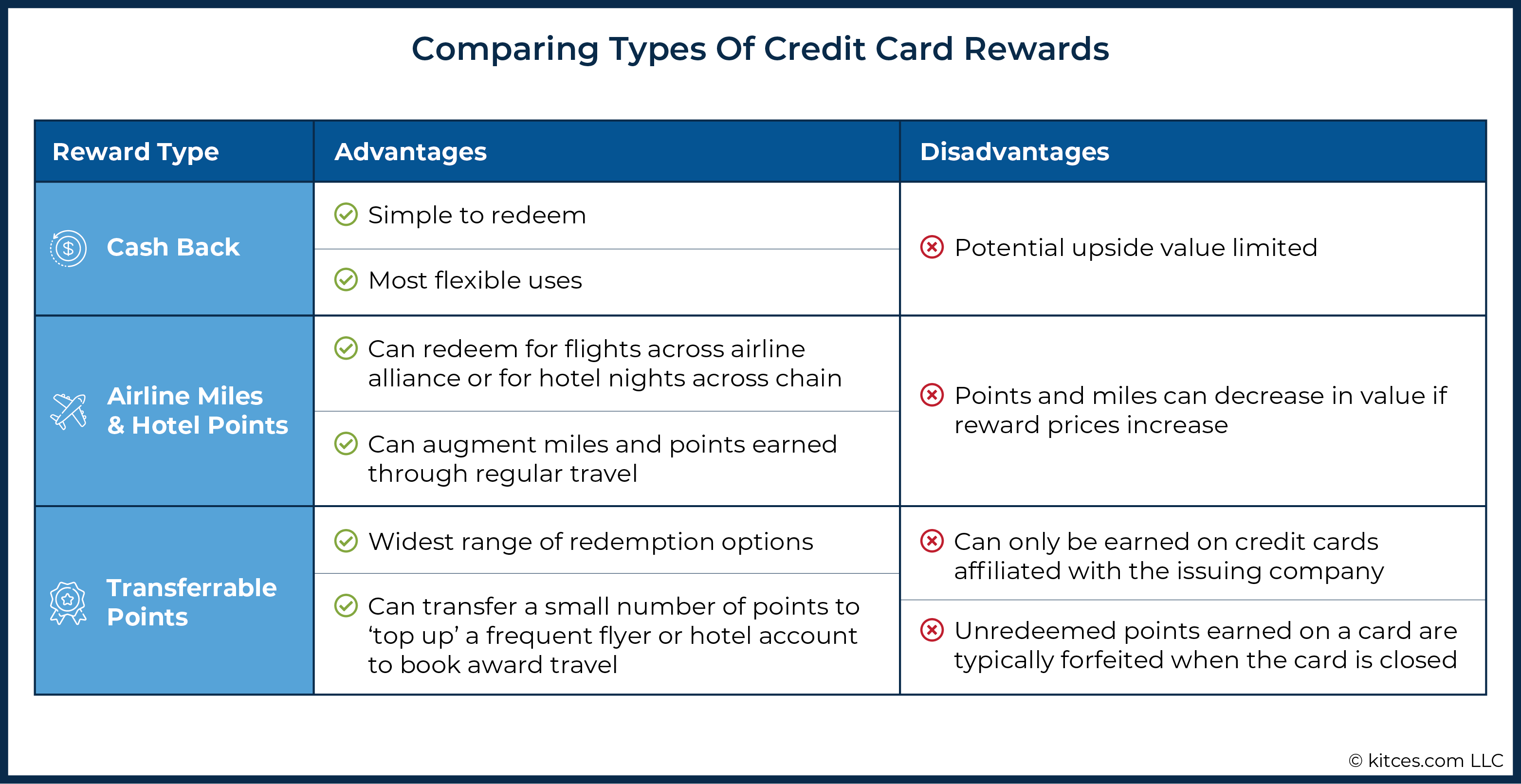

The first step to supporting clients in optimizing their credit card rewards is to understand the different types of rewards and how they can be generated. Credit card rewards can be categorized into three primary groups: 1) cash back; 2) dedicated travel points that can be used for airfare or hotel accommodations; and 3) transferrable points that can be converted into cash credits, airline miles, hotel points, or used for other rewards.

Comparing Different Types Of Credit Card Rewards

Each of the three types of credit card rewards has its advantages and disadvantages over the others, and the best kind of reward for a given individual will depend primarily on their preferences for either earning cash back or travel.

Cash Back Rewards

The simplest type of credit card reward is cash back for purchases made on the card. For example, a card might offer 2% cash back on purchases that can be redeemed as a credit on the user’s monthly statement or deposited into their bank account.

The primary benefit of cash back rewards is their simplicity and fungibility, as the user knows exactly how much the rewards will be worth and can be used for any spending needs. For clients who want to keep things simple, earning cash back can be a good choice. On the other hand, the upside value of the reward is limited to the cash back received, whereas other types of rewards can have significantly more value depending on how they are redeemed.

Travel Points/Miles

Another type of credit card reward is points and miles earned for a specific airline or hotel company’s loyalty program. Most travel providers offer loyalty programs, which reward users of the service with frequent-flyer miles or points that can be redeemed for travel as well as upgrades and other service perks when flying on the airline or staying in the hotel.

These loyalty programs are extremely lucrative for the travel providers, but also offer significant benefits to travelers as well. In addition to earning miles and points from travel, many airlines and hotels also offer co-branded credit cards that consumers can use to earn additional miles. For example, an airline credit card might offer one frequent-flyer mile for each dollar spent on the card. Earning frequent-flyer miles and hotel points through credit card spend can be a good way to augment the miles or points with an airline or hotel that the consumer already uses, and redemptions for flights or hotel stays can often be worth much more than the equivalent cash back that could be generated on a different card. On the downside, airlines and hotels sometimes increase the price in miles or points for a given flight or hotel, making the rewards less valuable.

Transferrable Points

The third type of credit card reward consists of points issued directly by a credit card company that can be redeemed for a variety of uses. For example, credit card users can earn Chase Ultimate Rewards, American Express Membership Rewards, or Citi ThankYou Rewards by paying for expenses with credit cards issued by each of these companies.

What makes these points unique is that they can typically be redeemed for a variety of uses. For example, the credit card user can opt to receive cash back as a credit on their statement, book travel using the points (instead of paying with dollars) directly through the card provider, or can transfer points to be used as travel points/miles with a range of airline and hotel partners.

This flexibility and the range of partners make these points particularly valuable. For example, while miles earned on a United Airlines co-branded credit card can be used to book flights through United, Chase Ultimate Rewards points can not only be converted into United miles, but also into miles on Southwest, JetBlue, British Airways, and other airlines, as well as into hotel points with Hyatt, Marriott, and IHG. Also, because the points can be transferred in increments (typically 1,000 points at a time), they can be used to ‘top up’ balances with the travel programs themselves.

While transferrable points can be very useful, they can only be earned on credit cards affiliated with the issuing company. Individuals must also make sure to use their points before canceling their card because, unlike airline miles or hotel points earned through credit card spending, these points are typically forfeited when the card is closed (unless the individual has another card that earns these points).

How Credit Card Rewards Are Earned Through Regular Spending

Just as there are many different types of credit card rewards that can be earned, there are also many ways to earn those rewards through regular credit card spending. The simplest reward-earning structure offers a fixed return for each dollar spent, no matter the spending category. For example, the Citi Double Cash card offers 2% cash back on all purchases. For a client who values simplicity, prioritizes cash back, and does not want to think about which card to use for a given transaction, this style can be attractive.

A more common structure offers a base amount of rewards for each dollar spent, with extra points earned in certain categories that remain fixed throughout the year. For example, the Chase Sapphire Preferred card offers three Ultimate Rewards points per dollar spent at restaurants, two points for spending on travel, and one point for all other purchases. The categories vary across the different cards, but some of the more popular options include gas, groceries, travel, and restaurants. For a client who spends significant money in one or more of these categories, a card with this structure can be valuable.

A third earning structure offers a base amount of rewards for each dollar spent, with additional cash back or bonus points for purchases in certain categories that rotate throughout the year. For example, the Discover It card offers 5% cash back on up to $1,500 in purchases in certain categories each quarter and 1% back on all other purchases. The category for one quarter might be grocery stores, while the next quarter might offer 5% back on purchases at gas stations. Taking advantage of these bonus categories in each quarter can lead to better rewards relative to spending on a fixed-return card, but it does require the user to remember which categories earn bonus rewards in a given quarter.

Jump-Starting Rewards Through Sign-Up Bonuses

While consumers can earn significant rewards through ongoing spending on cards throughout the year, the fastest way to earn rewards is through bonuses from signing up for new cards. Some cards offer a bonus simply for signing up, while the best bonuses typically require a minimum amount of spending on the card in a certain period of time.

For example, an airline co-branded credit card might offer 50,000 frequent-flyer miles for spending $3,000 on the card in the first three months after the account is opened, and one mile for all purchases made on the card. A person who successfully spends $3,000 using the card in three months would get 3,000 miles (earned for spending $3,000) + 50,000 miles (as an introductory bonus) = 53,000 miles in total. Without the bonus, a cardholder would have to spend $53,000 on the card to earn the same number of points!

Limitations And Caveats Related To New Credit Card Accounts

Because of the lucrative nature of credit card sign-up bonuses, individuals might be tempted to sign up for many cards during the course of a year. While this is possible, credit card companies do impose restrictions on how many cards an individual can have with the company and how frequently they can receive sign-up bonuses. These restrictions vary across card issuers and change over time. For example, Chase typically does not approve applications for cards when applicants have opened five or more credit cards from any issuer during the previous 24 months (referred to as the “5/24 Rule”), while Citi restricts users from earning a sign-up bonus within 24 months of either opening or closing the same card.

Another consideration, especially pertinent for clients preparing to apply for a major loan (e.g., a mortgage or auto loan), is the impact of opening new credit accounts on an individual’s credit score calculation. While opening a new credit card account can positively contribute to one’s credit score (e.g., by increasing the total credit available and reducing their credit utilization ratio), credit applications typically result in a ‘hard’ inquiry on the individual’s credit report, which can negatively impact scores.

New accounts can also decrease the average age of an individual’s credit accounts and the age of the most recently opened account, which are other factors impacting one’s credit score. Ultimately, the net impact of applying for a credit card is likely to vary by individual, which means it may be prudent for clients interested in sign-up bonuses to start by opening only one new account at a time to see how each account impacts their credit score before applying for additional cards.

Importantly, while credit card rewards can be lucrative, advisors can help individuals manage their spending by advising them to pay off their balance in full at the end of each month, as the interest due on remaining balances will likely negate much (if not all) of the benefit from sign-up bonuses.

Individuals who sign up for multiple cards should also be mindful of the various payment due dates, as late payments will not only incur interest charges and penalties but will also create a negative mark on the individual’s credit report!

How Credit Cards Can Generate Thousands Of Dollars In Cash And Travel Rewards Annually

While significant rewards can be earned simply through normal ongoing spending, one of the fastest ways to collect substantial benefits is through credit card sign-up bonuses, as a single credit card sign-up bonus can be worth thousands of dollars’ worth of travel! But given the wide range of credit card rewards available, how can advisors help clients develop a strategy to maximize their earning potential?

Finding The Best Credit Card Sign-Up Bonuses

Credit card companies are often aggressive in marketing their cards (as anyone who looks through their mail or walks through an airport can attest). And while some of these offers come with attractive sign-up bonuses, the best are typically found online and are often only available for a limited time.

The travel blog Frequent Miler keeps an updated list of the best currently available credit card sign-up offers across a wide range of credit card issuers that can be a useful resource for advisors looking for recommendations for clients, and to evaluate bonus offers sent directly by credit card companies. For example, Frequent Miler estimates that the current top credit card sign-up offer is worth more than $1,500 in the first year, with several other cards also having bonuses worth more than $1,000!

Nerd Note:

Credit card sign-up bonuses are not only offered for personal cards available to the broader public, but also for ‘business’ credit cards limited to business owners. These business cards can offer bonuses that rival, or even exceed, those of personal cards, so financial advisors with clients who are business owners (or the advisors themselves!) can consider both types of cards. For business owners, credit card sign-up bonuses can be a nice way to earn significant rewards for ongoing expenses!

Evaluating Credit Card Sign-Up Bonuses

The size of credit card sign-up bonuses can vary greatly, so it is important to consider not only the size of the bonus, but also whether the reward is appropriate for the individual. For example, a bonus of 50,000 points that an individual can choose to transfer to a variety of travel loyalty programs or to use toward a cash back bonus could be more valuable than 60,000 frequent flyer miles if the individual does not plan on redeeming rewards for flights.

When comparing sign-up bonuses, it can be useful to use a ‘cents-per-point’ framework. This allows an individual to compare the value they should expect to receive from different types of points or miles. For example, if an individual received a sign-up bonus of 50,000 hotel points and redeemed those points for a hotel stay that cost $750, they would have received $750 ÷ 50,000 points = 1.5 cents of value per point redeemed.

The cents per point an individual receives for a given airline or hotel loyalty program will vary based on the specific company and type of reward redeemed. While no two redemptions for a specific airline or hotel are exactly the same, the Frequent Miler blog has estimated cents per point values individuals can reasonably expect to receive from travel redemptions through these programs.

Example 1: Jerry is deciding whether to apply for a United-affiliated credit card with a sign-up bonus of 50,000 miles, or a Hilton-affiliated card with a sign-up bonus of 100,000 points.

According to the Frequent Miler website, the United Airlines MileagePlus miles have an estimated cents per point value of 1.3, while Hilton Honors points have a cents per point value of approximately 0.4.

Based on these values, Jerry estimates the United bonus would be worth about 50,000 (sign-up bonus miles) x 0.013 (estimated cents per point value) = $650 worth of flights, and the Hilton bonus would be worth approximately 100,000 (sign-up bonus miles) x 0.004 (estimated cents per point value) = $400 worth of hotel stays.

In the example above, even though the Hilton bonus was worth more points, Jerry is likely to get more value from the United miles. Often, the best cents-per-point value comes from redemptions for premium-class travel, which can have a very high cash cost and cents-per-point value.

Assessing the relative value of reward points can also depend on how points will be redeemed. In the following example, business-class travel offers twice the cents per point value than economy-class travel.

Example 2: Elaine is planning a trip from New York to Paris. She recently earned 100,000 American Express Membership Rewards points after signing up for the American Express Platinum Card.

A round-trip economy-class airplane ticket costs $900 in cash and would require 60,000 points if she were to transfer them to one of American Express’ partner airlines. Thus, the purchase of an economy-class ticket would be equivalent to $900 (ticket price) ÷ 60,000 points = 1.5 cents per point.

However, a business-class ticket costs $3,000 in cash or 100,000 points, for a value of $3,000 ÷ 100,000 points = 3 cents per point.

Even though Elaine could fly economy and save the remaining miles for another trip, she chooses to take advantage of the higher-value option and uses her points to purchase a business-class ticket, especially because she enjoys traveling business-class but is not willing to pay for the expense in cash.

Ultimately, the best redemption offer for an individual can come down to their unique preferences. Just as there is no single 'right' choice for all financial planning clients, there is no 'right' miles or points redemption choice for everyone!

Converting Credit Card Rewards Into Travel

Clients who amass credit card rewards for travel have several ways to redeem them. Transferrable points (e.g., Chase Ultimate Rewards and American Express Membership Rewards) typically offer the most value because of their flexibility. They can be used to book travel directly through the credit card company’s travel portal, and can also be extremely useful for transferring to other airline and hotel reward programs, particularly when the individual has already earned miles or points (e.g., from business travel) but needs more for a given flight or hotel stay.

Example 3: George currently has 60,000 Ultimate Rewards points through his Chase credit card, and 35,000 United miles earned from flying for his job.

He wants to book a United flight that costs 40,000 miles, but instead of earning the additional miles through airline travel, he simply transfers 5,000 Ultimate Rewards points from his Chase card to his United reward account and is able to book his flight with reward points.

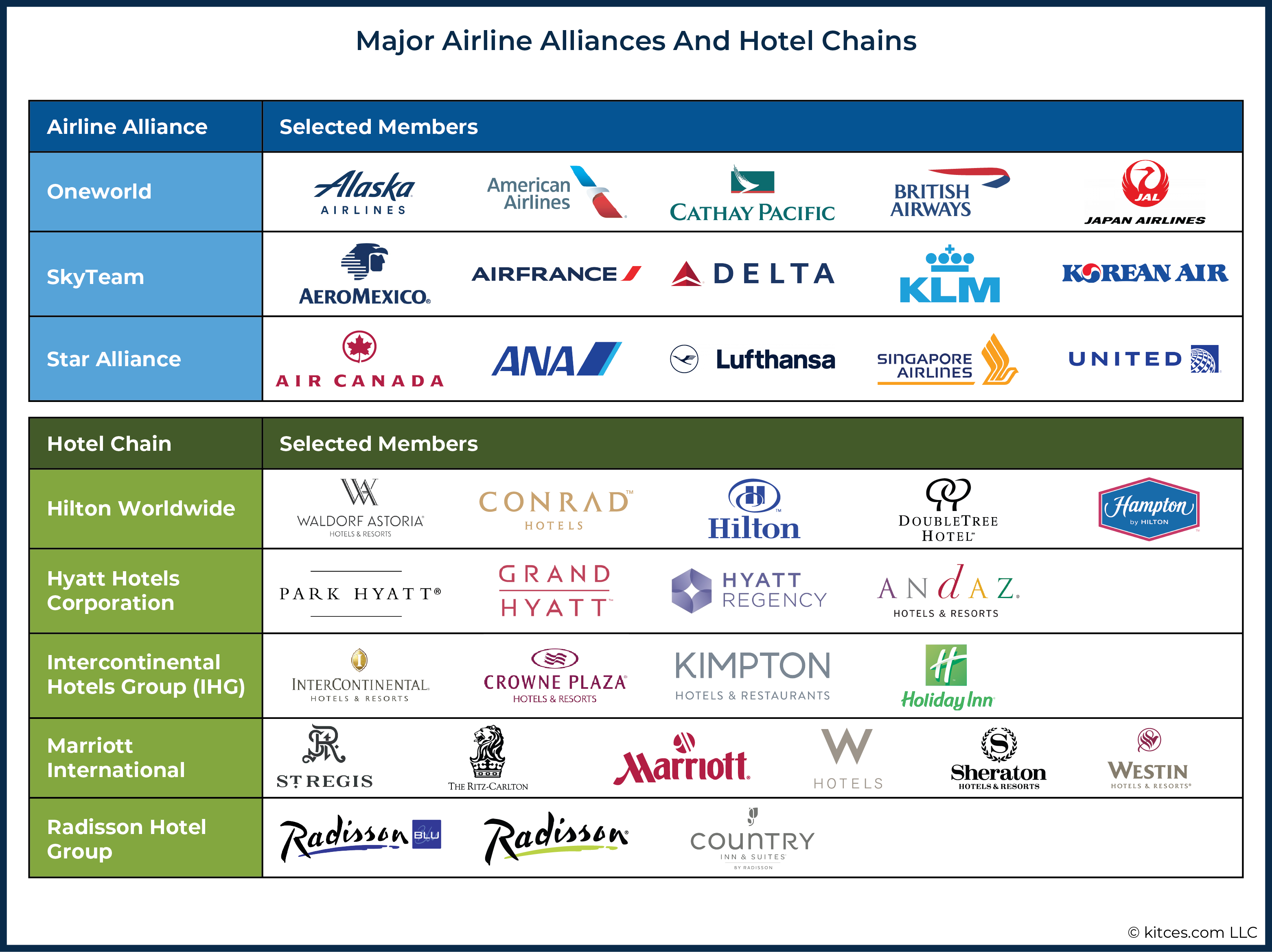

Frequent flyer miles and hotel points are affiliated with loyalty programs belonging to a specific airline or hotel (e.g., American AAdvantage miles or IHG Rewards Club points). And while airline miles and hotel points are less flexible than transferrable points, they do provide some flexibility for redemptions. Most major airlines are part of alliances (e.g., Star Alliance and oneworld Alliance) that allow individuals to earn and redeem miles with airlines across participating companies in the alliance.

For example, Delta SkyMiles can be redeemed not only for flights on Delta, but also on other SkyTeam alliance partners, such as Air France and Korean Air. The ability to use miles for flights on other airlines provides more options when booking flights using award points, particularly for international flights.

While there are no similar alliances for using hotel points, these points still offer flexibility in redemptions across a hotel chain’s portfolio of brands. For example, Marriott Bonvoy points can be earned and used at Marriott hotels, but also Ritz-Carlton, W Hotels, Westin, and Courtyard hotels, among others.

Other Factors To Consider When Evaluating Credit Card Offers

While the most valuable component of credit card offers is typically the sign-up bonus (which can consist of points, miles, or cash), many cards also come with additional perks (and expenses) that can also be evaluated when making comparisons.

Some cards affiliated with airlines or hotels offer perks related to that company. For example, airline-affiliated credit cards often offer a free checked bag or priority boarding benefits to their credit cardholders, while hotels might offer access to room upgrades. These perks can vary widely, but they still can be valuable for those who are able to take advantage of them.

Another consideration when evaluating a credit card offer is the annual fee that is associated with the card. Some cards with large bonuses and travel-related perks have large annual fees, so it is important to consider these in the calculation as well. For example, a card with a $95 annual fee offering a 50,000-point bonus is likely to be more valuable than a card with a $495 annual fee and a 60,000-point bonus for the same airline or hotel. At the same time, cards with higher annual fees often come with credits that can defray the cost of the annual fee. For example, while the American Express Platinum Card has a $695 annual fee, it comes with a $200 airline fee credit, $200 in Uber cash, a $200 credit for certain hotels, and a $240 credit for specified digital entertainment providers, among other credits and rebates. For cardholders who are frequent travelers, these perks can more than make up for the annual credit card fee!

Cards with annual fees may not be worth keeping after the first year, but some credit card companies may offer retention bonuses for those who ask to close their account, so it can be worthwhile to call the card company each year to see what might be available.

However, closing a credit card can potentially impact an individual’s credit score by reducing their total amount of credit available or the average age of credit accounts (depending on how old the account is). Therefore, it might not be prudent to close credit cards immediately before applying for a loan.

Finally, those applying for cards should also consider whether a sign-up bonus will be subject to taxation. While the IRS has not provided definitive guidance on the matter, points received for spending money on a credit card (including those received through sign-up bonuses and as rewards for regular spending) are typically treated as a non-taxable ‘rebate’ for purchases made, while sign-up bonuses that do not require spending on the card can be treated as taxable income. Credit card companies will typically issue the cardholder a 1099-MISC form for any taxable bonuses.

Implementing Credit Card Strategies For Financial Planning Clients

Individuals can get significant value from credit card rewards, but creating a realistic strategy for maximizing rewards can take time. Financial advisors who are familiar with the rewards landscape are well-positioned to support clients in deciding whether to apply for new credit cards and which ones to use for ongoing spending.

With the potential for clients to get thousands of dollars of value annually, crafting a credit card reward strategy can be a helpful way for advisors to demonstrate ongoing value to their clients.

Analyzing Client Credit Card Spending Patterns

Cash flow discussions can be a good opportunity to broach suitable credit card reward programs. Advisors can discuss not only what clients are purchasing with their money, but also how they are doing so. This can uncover important information to help craft a sensible rewards strategy, including how much the client spends with credit cards in total, which categories of expenses (e.g., groceries, gas) they spend the most money on, and whether they are planning any large one-time expenses that can be incorporated into the client’s strategy.

Understanding a client’s spending habits can help the advisor create a range of options for credit card bonuses and ongoing spending. For example, a client who spends $10,000 per month with credit cards will have greater capacity to meet any spending requirements for sign-up bonuses than one that only spends $1,000 per month.

Understanding the categories on which the client spends the most money can also help the advisor to recommend appropriate credit cards that maximize the spending in those areas. For example, a client that spends $20,000 per year on travel could be well-suited for a card that offers multiple points per dollar spent on travel expenses, while a client with a large family that spends $15,000 per year on groceries can consider a card with a points bonus for spending at grocery stores.

Example 4: Tim’s client Susan spends $40,000 per year on her credit cards, including $15,000 on travel and $12,000 at restaurants.

Based on this spending pattern, Tim recommends that Susan use a Chase Sapphire Preferred card, which earns 3 points per dollar spent at restaurants, 2 points per dollar spent on travel, and 1 point per dollar on other spending.

Thus, Susan will earn 12,000 (her annual dining expense) × 3 (reward points for each restaurant dollar spent) + 15,000 (annual travel expense) × 2 (reward points for each travel dollar spent) +13,000 (annual spending in other categories) x 1 (reward points for other spending) = 79,000 points for the year.

Finding out whether a client is expecting to have large one-time expenses can also be useful because a single expense could potentially cover the full amount of required spending for a credit card sign-up bonus.

For example, a client paying expenses for a child’s wedding could leverage sign-up bonuses to give themselves a vacation afterward!

Example 5: Sue Ellen’s clients Morty and Helen are planning to spend $12,000 for their son’s wedding and are interested in using points earned from credit card sign-up bonuses to go to Europe. Based on the amount they plan to spend and their travel goal, Sue Ellen recommends that they each apply for the Citi/AAdvantage Platinum Select card and the Marriott Bonvoy Boundless card.

The Citi/AAdvantage card offers 60,000 American AAdvantage miles after spending $3,000, and the Marriott Bonvoy card offers 3 free nights at any Marriott property up to 50,000 points after spending $3,000.

By using their four respective cards each to cover $3,000 of wedding expenses, not only are Morty and Helen able to help their son by covering $12,000 of his wedding expenses, but they are also able to enjoy a relaxing European vacation for themselves, with enough credit card reward points to cover round-trip airline tickets and six hotel nights!

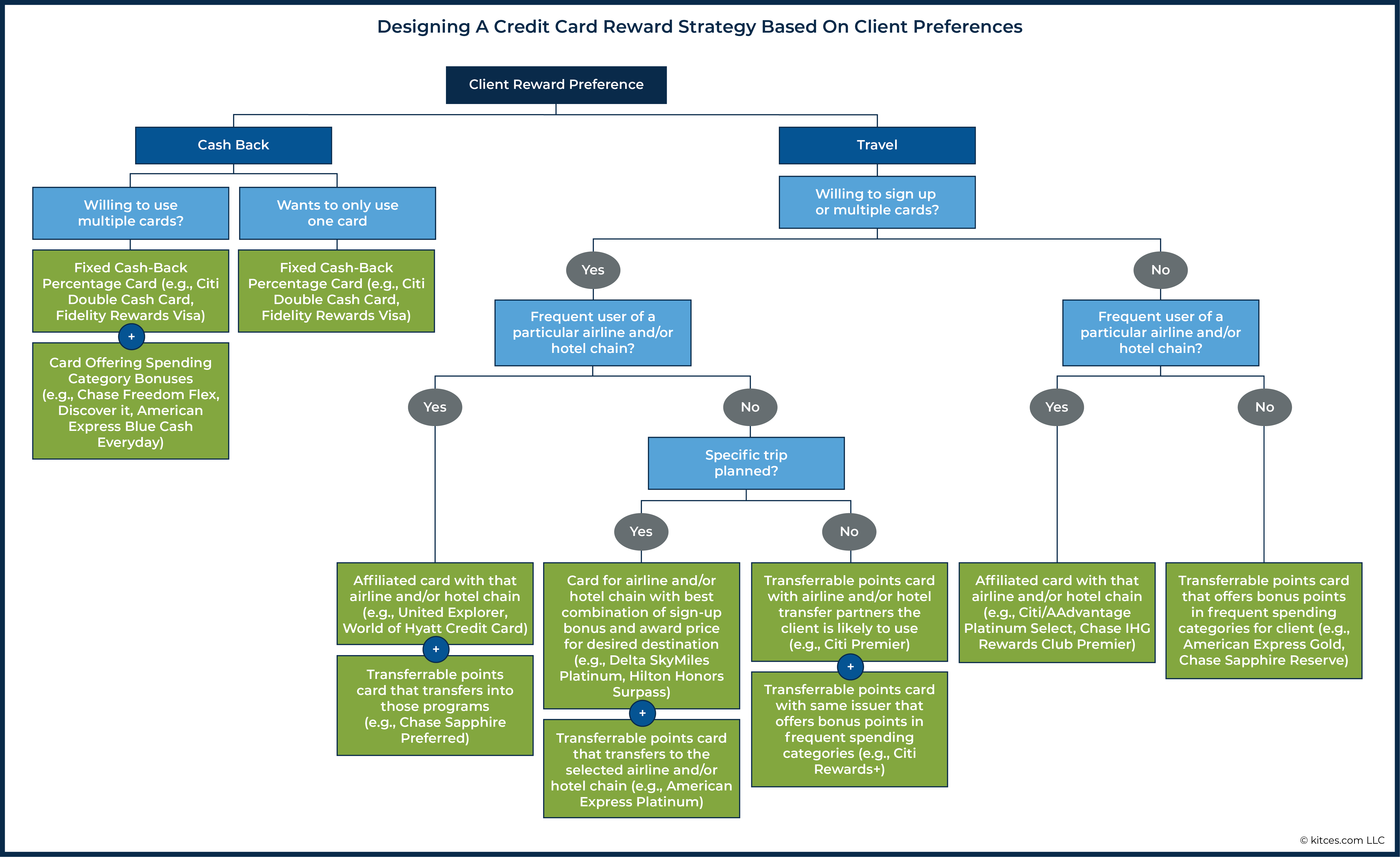

Understanding Client Preferences

In addition to understanding a client’s spending patterns, it is also important to gauge their interest in certain credit card rewards and their preferences for using them. While some clients might be interested in applying for multiple new cards each year to build up points and miles through sign-up bonuses, others might be less interested in applying for cards and would prefer earning rewards on a single card. Either option can be profitable for the client, but it is important that they are comfortable with the process.

‘Simple Cash’ Clients

Clients who don’t travel much and who don’t want to manage multiple credit cards would benefit more from the flexibility and convenience of cash back rewards as opposed to point-based reward programs.

Example 6: Kramer spends $50,000 per year on his current credit card, which earns 1% cash back on all purchases.

He likes the simplicity of cash back and wants to use the same card for all of his purchases, so his advisor recommends the Citi Double Cash card that offers 2% cash back.

Kramer can now earn $50,000 (credit card spending) × 2% cash back = $1,000 in cash rewards each year from his regular spending, in comparison to the $50,000 × 1% = $500 he was earning before.

‘Travel Maximizer’ Clients

Clients who travel and who are willing to sign up for multiple credit cards in a given year can earn significant value from credit cards that offer transferrable points as well as those affiliated with the airlines and hotels they regularly use for travel.

Example 7: Mickey’s client Newman loves to travel and is willing to sign up for multiple cards. He often travels for business, typically flying on United Airlines and staying in Hyatt hotels.

Mickey recommends that Newman apply for the following cards over the course of the year:

- The Chase Sapphire Preferred card, which offers a 60,000 Ultimate Reward Point sign-up bonus (after spending $4,000). The Ultimate Rewards points can be transferred to both United and Hyatt’s loyalty programs.

- The Chase United Explorer card, which offers a 60,000 United MileagePlus mile sign-up bonus (after spending $3,000), plus a free checked bag and priority boarding on United flights.

- The Chase World Of Hyatt card, which offers a 30,000 Hyatt point sign-up bonus (after spending $3,000), plus Hyatt Discoverist status, which gets him premium internet and preferred rooms, among other benefits when he stays at Hyatt hotels.

This strategy not only gives Newman more United miles and Hyatt points that he can redeem for flights and hotel stays, but also upgrades his experience when using the two companies for both his business and personal travel.

Of course, clients are likely to have a wide range of preferences when it comes to earning and redeeming credit card rewards. The flow chart below shows how an advisor can work through the various credit card reward styles given client preferences to determine the best strategy and to recommend useful credit cards for the client.

Keeping Track Of Client Recommendations

To make better credit card recommendations over time, advisors can create a system to track their recommendations and how they are implemented. For example, including a client’s reward preferences (e.g., cash back or travel) and approximate credit card spending in their CRM file would allow the advisor to quickly come up to speed if the client asked for a credit card recommendation outside of the annual meeting.

Further, advisors can create a file to track the cards that clients apply for to ensure that they do not make duplicate recommendations and that their clients do not run afoul of the application limits imposed by the credit card companies.

Combining these steps with quarterly reviews of the Frequent Miler’s Best Offers page would give an advisor an understanding of both client preferences and available credit card options.

Supporting The Award Redemption Process

In addition to helping clients earn credit card rewards, advisors can also support the overall goal of redeeming points and miles for cash and travel. Cash back rewards are the easiest to redeem and are typically applied as statement credits (which are generally simpler than redeeming via direct deposit or physical check, which are sometimes also available options).

It is important to note that, depending on the card, cash back awards are not always automatically applied to each statement. Sometimes, cardholders may need to request the reward to be issued as a statement credit. Advisors can support this process by confirming with clients not only how much cash back they earned in a given year (which allows them to determine if clients have the best card(s) to maximize their rewards), but also that they actually redeem their rewards!

Redeeming credit card rewards for travel is a trickier process than getting cash back, but advisors can play an important role in helping clients get the travel awards they want if they understand how travel rewards work and the flexibility offered by transferrable points.

For example, some transferrable points can be redeemed for travel booked directly through the credit card issuer’s site at a fixed rate, such as with the Chase Sapphire Reserve card. Cardholders can redeem their Ultimate Rewards points at a rate of 1.5 cents per point for any travel booked through the Ultimate Rewards portal. For example, a cardholder would be able to redeem 20,000 points (earned through a signup bonus or through regular spending) × 0.015 cents per point = $300 toward flight expenses. This shows how transferable points can provide excellent flexibility, as clients can use them to book available flights with any airline, or lodging at any hotel, rather than be limited to flights offered by a certain airline alliance or hotel chain, as is the case with frequent flier miles or hotel loyalty programs.

On the other hand, airline flight rewards are determined either through award charts that set a fixed mile cost for travel between two regions or, increasingly, dynamically based on demand. This means that since a particular company’s miles or points can decline in value if the airline or hotel changes its award chart or pricing (e.g., to require more miles for a given flight or hotel stay), it is typically recommended to earn these travel rewards with a specific use in mind rather than building up a stash for an unspecified trip in the future (that could end up costing more points than it does now).

Example 8: Marla’s client Jackie wants to take his girlfriend Sidra to Hawaii and needs to know how many reward miles he will need to do so.

Using American Airlines' award chart, Marla sees that a one-way economy class MileSAAver ticket between the Continental U.S. and Hawaii costs 22,500 miles (or 45,000 miles round-trip), so Jackie will need 90,000 miles (45,000 miles x 2 tickets) to pay for both tickets.

Marla recommends that Jackie get these miles by signing up for the AAdvantage Aviator Red card (60,000 AAdvantage miles after the first purchase) and the AAdvantage Platinum Select card (50,000 AAdvantage miles after spending $2,500).

Hotel chains also publish reward charts that put their hotels in different reward redemption categories. For example, Hyatt’s chart has eight categories for its hotels, ranging from 5,000 points for a standard night at a Category 1 hotel (that typically includes Hyatt’s least expensive hotels in dollar terms) to 40,000 points per night at a Category 8 hotel (that includes some of Hyatt’s most expensive properties). While some clients might prefer to redeem their points for several nights at a lower-cost hotel, others might want to splurge on the luxury redemption.

Advisors can support clients in booking travel using miles and points by first understanding the client’s travel plans, researching approximately how many miles and/or points it will cost (using the companies’ award charts or pricing out the trip on the airline or hotel website), and then suggesting a credit card strategy that can earn them enough rewards to book the trip.

It is important to note that award availability can change, so it helps if clients plan well in advance and if they can be flexible with the dates of their trip. For clients who do not want to go through the process of searching for and booking the award travel on the airline’s or hotel’s website, many award-booking services are available; these can be particularly useful for booking premium-class flights where availability can sometimes be hard to find.

Ultimately, the key point is that clients can be leaving money (or travel opportunities) on the table by not maximizing their credit card rewards, and advisors who help them take advantage of their rewards can demonstrate ongoing value to clients.

Cash flow discussions during client meetings can serve as a starting point for gauging a client’s potential credit card spending and rewards preferences. Advisors can also recommend suitable credit cards for sign-up bonuses and ongoing spending based on a client’s interest, as well as supporting the award redemption process.

With the potential to earn thousands of dollars’ worth of cash or travel rewards annually, incorporating credit card rewards into financial planning discussions can be a major driver of client loyalty!

Thanks, Adam!! I am a “travel maximizer” who uses these techniques (and more) to save thouisands of dollars per year on travel. This is by far the most accurate and thorough article I have seen written by a non-travel professional.

Two thoughts:

1. To re-emphasize one of your points – travel rewards cards should only be used by those who are disciplined enough (and have the cash flow) to pay off their balances in full every month, and to avoid incurring extra expenses just to earn more travel rewards. Those who are less disciplined will find that extra expenses far outweigh the travel benefits.

2. There is a downside to purchasing airline tickets through third party portals such as the Chase Ultimate Rewards portal, instead of directly from airlines – in case of flight irregulities, it can be much more difficult to get refunds or other satisfactory resolutions. Portal customer service is generally poor or nonexistant. For example, just before the onset of Covid, I purchased a $750 international air ticket through the Ultimate Reward portal. When covid struck, the airline offered me a useless credit for future travel; I was unable to get the portal to refund my points.

Thanks for reading and for the comments UAPhil! I definitely agree on discipline being important when using rewards cards–it’s tempting to go all-in right away but starting slow can be more sustainable.

Great article, Adam. Like Phil, this is a big hobby of mine as well–for the past nine years. While I have mentioned this “game” to clients in the past, I don’t have the bandwidth to add it formally to my offered services.

Award Wallet is a great app for viewing travel award accounts in one place and tracking point expiration dates.

I also extensively use Excel to track account opening dates, progress towards bonuses, benefits of each card, closing date of account, etc….

Married couples initially don’t realize that each person can apply for the same cards and earn the same bonuses. And if they have a business, that’s a third way. Then if you are a real enthusiast, like me, you also include your mother and adult children!

Free travel is the best! Happy New Year!

Thanks for the comments Tim. Definitely agree on Award Wallet and the potential benefits for married couples. Hope your 2022 is off to a good start!

Thanks for this article! I’m a cash-back guy myself. It’s not worth the time and mental bandwidth to me to chase the rewards points and then book using them. But I can see how it might be worthwhile for some of my clients who don’t mind spending the time.

Thanks for reading Rob! Cash back is a great option for ease of earning and using rewards. I actually do a combination of travel points and cash back myself.