Executive Summary

For more than 20 years, industry benchmarking studies have helped financial advisors understand how to manage the profitability of their businesses, and ensure that the costs to service clients are in line with the fees they’re being charged. However, remarkably little research has been done into the costs that must be incurred to actually obtain those clients in the first place and the cost-effectiveness of various client acquisition strategies that financial advisors use.

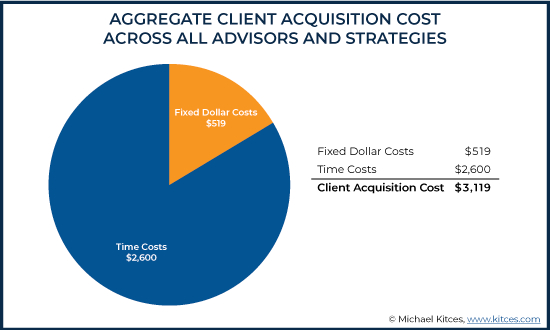

And it turns out those client acquisition costs are substantial! In our recently released Kitces Research report of more than 800 financial advisors who participated in a survey, the average total cost for a financial advisor to acquire a new client is $3,119 per client. Notably, though, a significant portion of that cost is the ‘time cost’ of the financial advisor themselves (an average of $2,600 worth of time spent, or 83% of the total cost of client acquisition), while only $519 is typically spent on hard-dollar marketing costs themselves. Which suggests that while early-on it may be cost-effective for advisory firms often to substitute advisor time for firm dollars when it comes to marketing efforts, especially for those who don’t have a lot of money to invest into growing their business in those initial years, that advisory firms may be overly reliant on an advisor’s (less-and-less-cost-effective) time to grow the business, rather than allocating marketing dollars to grow the business in a more scalable way.

The significant upfront cost to acquire a client is especially salient for financial advisors with recurring revenue models, as the cost to acquire a client may often be equal to or more than the entire revenue generated by the client in the first year – and the equivalent of several years’ worth of profits – which results in a “J-Curve” of client profitability (where aggregate profitability of a new client is negative in the early years and only turns positive over time). Which is important, as overzealous marketing efforts can cause a steep negative J-Curve dip, which in turn can cause the firm to overextend its growth capacity and ‘grow broke’ even if otherwise on a long-term path to profitability. Though on the other hand, the depth of the J-curve of advisor profitability, when coupled with firms that often have 20-30+ year-average client retention (at 95% to 97% annual retention rates), suggests that most advisory firms may be grossly underspending on marketing relative to the astonishing lifetime client value of an individual new client.

To maximize marketing spending – and minimize Client Acquisition Costs (CACs) – our Kitces Research Report identified the most cost-effective (measured by the actual CAC) and cost-efficient (measured by the revenue generated from the client relative to CAC) marketing strategies in use by the financial advisors surveyed, which included both ‘traditional’ methods (e.g., client referrals, networking, and Centers of Influence), but also underappreciated alternatives (albeit with more upfront cost) including SEO, writing a book, webinars, marketing lists, and paid third-party website listings. Interestingly, the most cost-effective strategies differed for firms with the highest marketing efficiency (books, direct mail, paid web listings, marketing lists, and SEO) versus the most efficient strategies for firms not as ‘marketing-inclined’ as others (paid advertising, paid solicitors, seminars, and general networking).

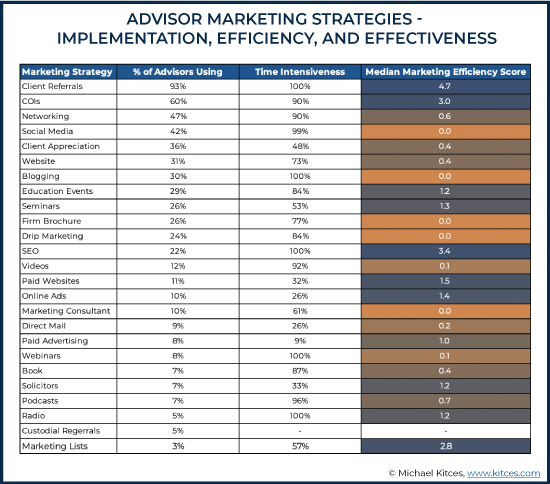

Examining marketing strategy efficiency relative to advisor adoption rate also reveals that some of the most commonly used strategies are actually among the least efficient (e.g., social media, blogging, and client appreciation events), whereas some of the lesser-used are still very efficient (e.g., marketing lists, radio, solicitors, online ads, and paid websites). This suggests an inherent inefficiency when it comes to marketing strategies chosen by financial advisors. The biggest driver behind this inefficiency appears to be the strong advisor preference for strategies that rely on the advisor’s time (versus hard dollars invested in the strategy), and an overweighting on strategies that produce a high quality of leads over those that produce a scalable quantity of leads or are actually the most cost-effective (which may help to explain why larger firms are outgrowing smaller ones, as they are able to accommodate scalable hard-dollar marketing strategies that smaller advisors might not otherwise be able to afford or be willing to invest into).

Ultimately, though, the key point is that while there is a wide range of marketing options available for advisors, effectiveness and efficiency are important criteria that need to be considered to ensure that resulting growth is sustainable, as initial costs may be recouped only after a client has generated revenue for the firm over several years. In fact, with an average CAC of $3,119, this Kitces Research Report suggests that perhaps the primary reason that advisory firms struggle to serve mass affluent clientele and the broader population is not because it is cost-ineffective to service them, but that it’s too cost-ineffective to market and gain a scalable number of them as clients in the first place! Though on the other hand, with recent reports suggesting robo-advisors have ‘just’ an average acquisition cost of $500 - $1,000, it seems clear that an opportunity exists for advisors to reduce the overall cost of their marketing efforts (and/or for third-party providers to scale their own lead generation services for advisors)… which may both improve the profitability of advisory firms, and allow them to grow more scalably and reach a wider range of clientele.

The Importance Of Client Acquisition Costs And The J-Curve Of Lifetime Client Value

For any business to be profitable, it must generate more profit from selling a product to or servicing a customer (after appropriate operational and service expenses) than it takes in marketing and sales efforts to get the customer in the first place.

For instance, if a business wants to be profitable selling a widget for $100 and it takes $70 to make the widget… it better cost the business less than $30 to market and sell the widget, or there won’t be any money left for profits!

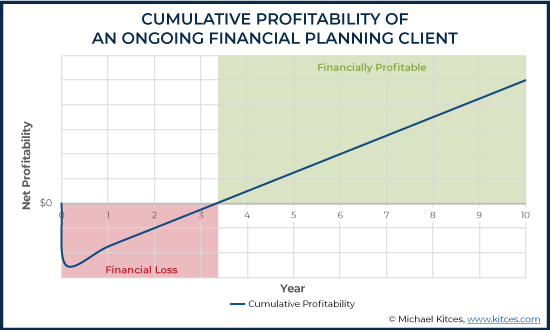

Of course, in businesses that have recurring revenue in an ongoing relationship, it’s entirely possible that clients won’t be profitable initially – particularly given the potential upfront costs to get the client – but can become profitable over time as ongoing profits recover the initial acquisition costs and then generate positive cash flow thereafter.

In the context of financial advisors, particularly those on the AUM model, this produces a “J-curve” of client profitability, where moderate ongoing fees with high upfront costs (given the difficulty of getting a client in the first place) results in an initial upfront loss that becomes a more profitable client relationship over time.

For instance, imagine an advisory firm that spends $5,000 on a marketing event and gets one new $500,000 AUM client who will generate $5,000/year in ongoing revenue thereafter. Offhand, it appears that the firm will ‘recover’ its marketing cost in the first year, but the truth is that it takes money to service the client and deliver the financial plan and ongoing advice. If the firm has a 30% profit margin, then in practice it only ‘recovers’ $1,500/year in profits, which means it will take more than 3 years to recover the original cost… even though the firm will ultimately generate $10,000 of cumulative profit over the next decade (assuming an average retention rate of 90%, which means the firm would have an average client tenure of 10 years).

More generally, though, the fundamental point is that particularly in recurring-revenue businesses, clients don’t necessarily need to be profitable upfront from day 1… but they do need to cumulatively become profitable over time. In essence, then, the lifetime value of the client must exceed the acquisition cost to acquire that client.

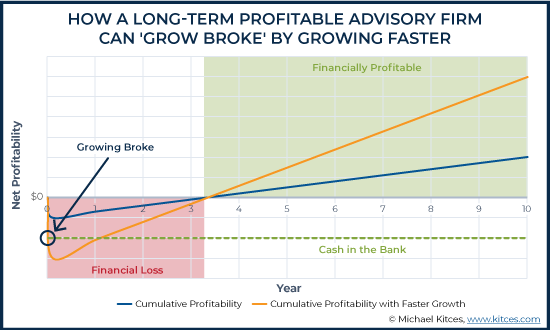

The important caveat in businesses like recurring-revenue advisory firms that have a J-curve of profitability, though, is that it’s actually possible to ‘grow broke’.

Because even as long-term profitable clients are producing negative cash flow in the initial year or few (due either to upfront marketing and sales costs to get the client, or sometimes simply due to the additional financial planning service work that tends to occur earlier in the relationship), there is a very real risk that advisory firms can both become long-term profitable and still end out being short-term bankrupt!

For instance, if the advisory firm with the earlier J-curve of growth was to get 3 new clients at the same time – a series of 3 events that cost $5,000 each ($15,000 total) and generate 3 new $500,000 AUM clients (paying $5,000 each at 30% profit margins) , the firm’s long-term profits may be even greater, but their short-term financial costs are amplified as well! If the firm only had $10,000 of cash in the bank in the first place, it is growing profitably with slow growth… and ‘growing broke’ with fast growth!

Of course, the fundamental risk to all such growth strategies is that clients must be retained in the long run to be long-term profitable (and recover the upfront costs to acquire and service them). Fortunately, though, industry benchmarking studies show that advisory firms typically have 90%+ retention rates in the recurring-revenue AUM model, and ‘top’ firms have 97% to 98% retention rates, providing more than enough time horizon to recover those marketing costs.

Still, though, the key point is that even if clients will be profitable in the long run (or very profitable with 30+ year retention for top firms!) and receive services that will keep them on board, there is still a fundamental risk that an advisory firm can ‘grow broke’ along the way.

Which in turn makes it especially important to understand, and then try to manage, the firm’s upfront client acquisition costs to get those clients in the first place. As the shallower the J-curve dips, the less risk there is of growing broke!

What Is The Client Acquisition Cost For A Financial Planning Client

Despite the overwhelming importance of Client Acquisition Costs relative to lifetime client value and profitability – especially in advisory firms that tend to have a J-curve for client profitability – in practice, there has been substantial industry benchmarking and research into client profitability… and virtually none into client acquisition costs to get those clients.

Accordingly, last year our Kitces Research team launched a study to measure what advisory firms really are spending to acquire their financial planning clients – the true Client Acquisition Cost for a financial advisor.

Notably, though, Client Acquisition Costs are challenging to measure in advisory firms, as historically financial advisors haven’t spent much money to acquire clients. Instead, the cost of the financial advisor themselves was the client acquisition cost… for the insurance or investment product manufacturer that was trying to sell its products to consumers.

As from the perspective of an insurance company or mutual fund manager, paying a financial advisor a commission to sell the company’s products literally was the sales/marketing “client acquisition cost” for that insurance company or mutual fund manager to get the next new client! And insurance companies and asset managers managed their client acquisition costs by using a commission-based system, ensuring that advisors were only compensated when clients actually came in to the firm that could be profitable in the long run (with surrender charges that would allow the product company to recover the company’s client acquisition cost – the commission – if the client didn’t actually stay long enough to reach the crossover point of J-curve profitability).

In turn, because financial advisors (and salespeople in general) didn’t typically have a lot of ‘marketing capital’ themselves to invest in order to sell their company’s products, the primary marketing cost for most financial advisors was the time of the financial advisor, engaging in activities like cold-calling and networking (and eventually, spending time with existing clients to get referrals from them). A tendency that still holds today, with industry benchmarking studies showing that most financial advisory firms spend only about 2% of their revenue on marketing… even as a recent Kitces Research study showing that financial advisors spend almost 20% of their time on business development activities.

Which means in practice, advisory firms likely do allocate a more-business-to-consumer-typical 10% of their expenses to marketing and sales. It’s simply done as 2% in ‘hard-dollar’ costs, and an implicit allocation of 8% in advisor time costs (where advisor “direct costs” are typically 40% of an advisory firm’s expenses, and if 20% of the advisor’s time is on business development, 40% x 20% = 8%).

Accordingly, our recent Kitces Research study on “How Financial Planners Actually Market Their Services” evaluated the true Client Acquisition Cost, as an assessment of cost-effectiveness, for advisory firms by measuring not only the financial hard-costs that advisors expend on marketing but also the imputed cost of the financial advisor’s own time as well.

And on that basis, across a sample size of nearly 1,000 advisors, the average Client Acquisition Cost of a financial advisor is $3,119 per client… of which $519 are hard-dollar costs, and $2,600 (or 83% of the total cost to acquire a client) is the “time cost” of the financial advisor themselves.

What Are The Most Cost-Effective Marketing Strategies For Financial Advisors?

Of course, the reality is that financial advisors engage in a very wide range of marketing strategies, not all of which have the same $3,119 Client Acquisition Cost. Instead, some marketing strategies will be more cost-effective than others – which, in fact, is the whole point of analyzing and benchmarking client acquisition costs in the first place.

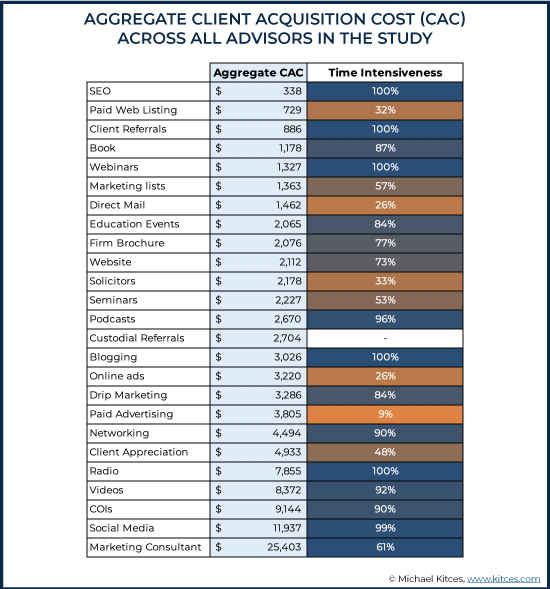

In our Kitces Research study, we found that in practice there was a remarkably wide range of Client Acquisition Costs for various financial advisor marketing strategies, from as little as $338 per client to as much as $25,000+!

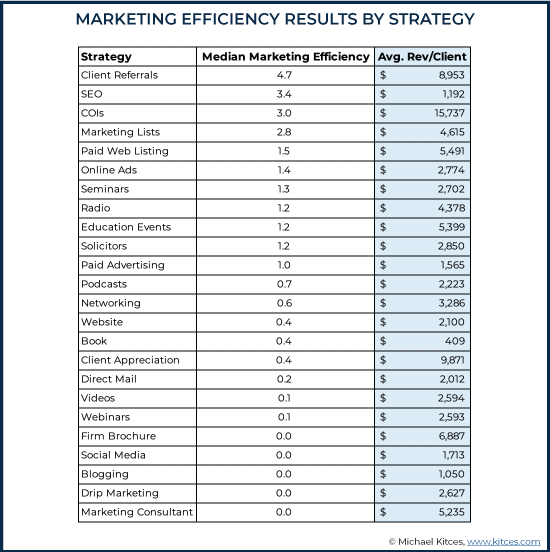

Notably, as the results reveal, “Client Referrals” (which routinely show up as the #1 strategy for financial advisors to grow) really are a very cost-effective marketing strategy for financial advisors, due in no small part to the fact that most of the time it takes to cultivate the referral relationship is already subsumed in cultivating the client relationship in the first place. Which means that while client referrals themselves are ‘time-intensive’ (in that they’re generated almost entirely by the advisor’s time, and not outright marketing dollars), referrals are a very time- (and therefore cost-) effective growth strategy, at least at the margin (for clients with whom the advisor has already established a deep relationship, with little additional time to ask for the referral or meet an introduction over lunch).

However, a number of more-commonly-hard-dollar marketing strategies also proved to be remarkably cost-effective, including Search Engine Optimization (SEO) to drive more local clients (especially given that “financial advisor near me” is still one of the most popular financial-advisor-related Google searches), Paid Web Listings (e.g., FeeOnlyNetwork, SmartAsset’s SmartAdvisor, Zoe Financial, etc.), writing a book, delivering webinars (notably more cost-effective than seminars for generating prospects!), and paying for marketing lists.

However, other upfront-financial-cost strategies were remarkably less cost-effective, including paid advertising (average Client Acquisition Cost of $3,805), radio (CAC of $7,855), and paying for third-party marketing consultants at a whopping $25,403 of spending per new client (though to be fair, in at least some cases, the marketing consultant likely generated an ROI for the firm by improving the cost efficiency of other strategies, which is not reflected in this result).

On the other hand, the results reveal that a number of low-dollar-cost-but-time-intensive marketing strategies for financial advisors are also remarkably ineffective, once considering the advisor’s time in the actual cost to acquire the client.

Accordingly, networking had an average Client Acquisition Cost of $4,494 (more than 10X the cost of improving the advisor’s website SEO!), client appreciation events had a CAC of $4,933, networking with Centers Of Influence (COIs, where advisors try to get referrals from key attorneys, accountants, or other ‘influencers’ in their community/target market) had an average Client Acquisition Cost of $9,144 (due to the extensive time it takes to cultivate the relationship), and social media (at least just for social media’s sake alone and not part of a broader integrated marketing strategy) had one of the worst Client Acquisition Costs at a whopping $11,937. (Suggesting that either social media itself is a very poor marketing channel, or that if it can be cost-effective, most advisors are executing it very poorly!)

Instead, the most cost-effective strategies for an advisor’s time, beyond generating referrals from existing clients, were all related to educating prospects, including writing a book, conducting webinars or a podcast, launching a blog, or staging education events.

Which Marketing Strategies Are The Most Cost-Efficient For The Clients They Get?

While our Kitces Research study shows that some financial advisor marketing strategies are far more cost-effective than others in generating new clients, not all strategies generate the same kind of client, in terms of the client’s affluence, needs, and ability to pay for financial advice.

Accordingly, another way to evaluate the effectiveness of financial advisor marketing strategies is to more directly relate the cost of acquiring the client to the average revenue the client generates (as a proxy for the client’s long-term Lifetime Client Value). As if a strategy that costs $10,000 to acquire a client generates a client who pays $10,000/year, it’s actually just as efficient (from a marketing Return On Investment perspective) as one that costs $1,000 but only generates an average client revenue of $1,000/year.

When viewed in this context, a somewhat different perspective on the relative efficiency of various financial advisor marketing strategies emerges.

In our study, we assessed marketing efficiency as new revenue generated in the preceding year for every $1 spent on marketing efforts, which include both advisor time and hard dollars used. Perhaps not surprisingly, client referrals gravitate all the way to the top when viewed from an efficiency perspective, as not only are client referrals relatively time- and cost-efficient (at least at the margin, given the time already invested into the client relationship), but they also tend to produce a high quality of leads (as in general, clients tend to refer others who are ‘like them’ in their peer network, so a referral from a good client on average turns out to be a good prospect as well).

Working with Centers of Influence, on the other hand, looks substantially better when viewed from a marketing efficiency perspective (ranked the 3rd most efficient strategy) than on the basis of Client Acquisition Costs (ranked the 3rd most costly) alone, as while cultivating such relationships is time-intensive and therefore cost-intensive (as measured by Client Acquisition Costs that include the value of the advisor’s time), it also generates on average a more affluent new client (higher revenue/client) than any other advisor marketing strategy measured.

Still, though, it’s also notable that rounding out the top 5 most-efficient strategies, when considering the revenue generated by the client, include investing into better website SEO, marketing lists, and paid web listing services (e.g., FeeOnlyNetwork, SmartAsset’s SmartAdvisor, Zoe Financial, etc.), which are all strategies that involve spending ‘hard dollars’ to improve the advisor’s client acquisition.

In this context, investing in SEO is likely more cost-effective than the others because much value can be generated from a one-time SEO investment that generates ongoing leads for months or years thereafter (whereas paying for marketing lists and web listings requires the advisor to continue to pay on an ongoing basis to continue to generate more leads). Which presumably means that the cost-efficiency of SEO would be expected to increase quickly over time (as fixed costs are recovered), whereas marketing lists and web listings may increase more gradually (or stay the same) over time (as more new clients requires more ongoing marketing investment).

At the other end of the spectrum are the least efficient strategies, which include generic drip marketing (e.g., with canned newsletter content), blogging, social media, creating a firm brochure (which does little if the advisor doesn’t do something with it to market), and the unfortunately-dubious ROI of investing into a marketing consultant (though, again, the results/value of the marketing consultant may be expressed in improvements in marketing efficiency of other strategies mentioned here).

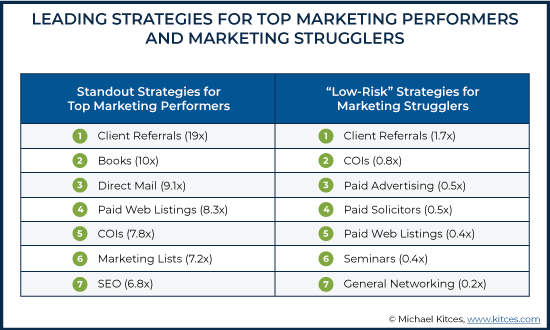

It’s also notable, though, that some strategies were especially effective amongst top-performing firms (i.e., the top 25% in terms of marketing efficiency). In other words, not only are different advisors more or less effective with some marketing strategies over others, but certain marketing strategies appear to be more conducive to ‘exponential’ growth amongst those top-marketing advisors than others.

These most-scalable ‘standout’ strategies included client referrals (which amongst top advisors generated an average of almost 19X the new revenue as the cost to acquire the referral), books (an average 10X multiplier of revenue/cost for top marketing firms), direct mail (a 9.1X multiplier), paid web listings (8.3X multiplier), COIs (7.8X multiplier), marketing lists (7.2X multiplier), and SEO (6.8X multiplier).

On the other hand, a different subset of strategies was more efficient amongst the ‘worst’ performers in advisor marketing. As in practice, some advisors are just not as marketing-inclined as others, and a material number of advisors reported generating “0 clients” as a result of their marketing efforts in various strategies (with certain strategies having materially higher failure rates than others).

Still, though, even amongst advisors that struggled with marketing (and generally implemented marketing strategies with efficiency scores of <1, which means the client generated less revenue in the first year than the cost in time or hard dollars to get them), there were a number of strategies that still had positive non-zero values (i.e., even the 25% poorest-performer advisor marketers were still getting at least some clients). These relatively ‘low risk’ (prone to at least some success in procuring clients, even amongst those who struggle with marketing) included client referrals (1.7X), COIs (0.8X), using paid advertising (0.5X), paid solicitors (0.5X), paid web listings (0.4X), seminars (0.4X), and general networking (0.2X).

Advisor Satisfaction Of Marketing Strategies: Quality Introductions Over Actual Results?

Ultimately, one of the key findings of our Kitces Research study on “How Financial Planners Actually Market Their Services” is that the financial advisor community is remarkably inefficient when it comes to marketing. As a list of the most popular marketing strategies reveals little correlation between what advisors are commonly doing, and what actually works (efficiently), beyond the fallback of relying on client referrals (which, while efficient, appears to also simply be popular because it’s all that advisors have left in the absence of any other marketing strategy).

Instead, it appears that the biggest driver of financial advisor marketing is an undue reliance on time-based strategies of the advisor (client referrals, COIs, networking, social media, client appreciation events, etc.), and an avoidance of strategies that rely on hard-dollar costs but may actually be far more efficient (e.g., marketing lists and paid web listings). Which may make sense early on in an advisor’s career – when there’s a lot of time and not a lot of dollars – but can become increasingly efficient as the firm (and the value of the advisor’s time) grows.

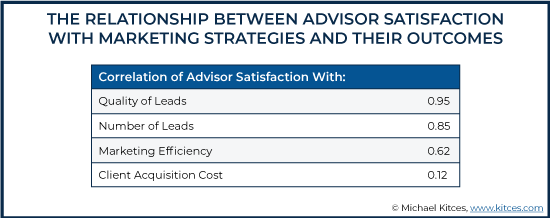

In part, though, this may also be a result of the fact that advisory firms are not only limited in the amount of money they are willing to spend on marketing (or can spend, given the J-curve of profitability), but that advisors also place a(n irrationally) high emphasis on the quality of leads from their marketing strategies over the quantity of leads or their actual marketing efficiency. As in practice, advisor satisfaction ratings of their own marketing strategies were most correlated to the quality of leads, and then the quantity (number) of leads, while the efficiency of the marketing strategy was a distant third (though notably, as long as the strategy was effective, advisors were more focused on the marketing efficiency of the strategy than just its client acquisition costs).

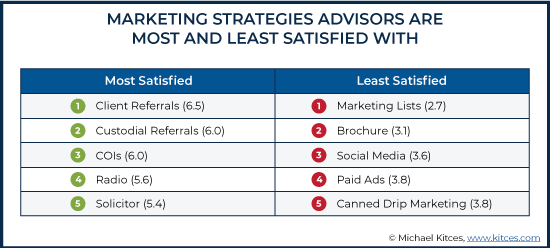

In other words, advisors tend to eschew strategies that generate a high volume of cost-effective leads where they still have to filter through the bad fits to find the good ones (which may help to explain why paid web listings and paid marketing lists score poorly in satisfaction despite being so high in marketing efficiency – because advisors don’t like needing to spend their time filtering out and rejecting the low-quality leads that may result), and prefer strategies that have a greater reliability of producing a high-quality lead, most typically through an introduction (where client referrals and COIs are among the most satisfying, along with RIA custodial referrals, radio, and paid solicitors).

Or stated more simply: financial advisor marketing strategies appear to be inefficient because advisors are putting too much emphasis on having high-quality leads (ostensibly with a high close rate), and not enough emphasis on strategies that can be even more cost effective but may require filtering through some bad fits to find the good ones.

The Limitations Of Inefficient Financial Advisor Marketing Strategies

Ultimately, the key point of analyzing the Client Acquisition Costs and efficiency of various financial advisor marketing strategies isn’t just to address the notion that advisory firms may need more perspective on what are really the most efficient marketing strategies (or not)… as the results show in particular that advisors may be grossly overweighting the importance of social media (which shows remarkably poor results) and underweighting the importance of SEO (which shows incredibly positive results).

The significance is that when the top-line average Client Acquisition Cost is $3,119, financial advisors are very constrained in who they can serve in the first place. As if the baseline cost to acquire a client is over $3,000, then even in the long run, an advisory firm may need to generate revenue of close to $3,000/year (which typically means working with a client who has at least $250,000 of assets under management) just to be able to achieve a 3-5 year breakeven on their marketing investment at a typical advisory firm profit margin.

In other words, the implication of a $3,119 Client Acquisition Cost is that the real reason that financial advisors struggle to serve the mass of middle-market consumers isn’t merely because of the cost to service those clients, but specifically the cost to market to get those clients in the first place, such that there’s no way to generate a positive return on the advisory firm’s marketing and sales efforts unless the firm can get a client that generates $3,000+/year of annually recurring revenue.

Similarly, these results help to explain why financial advisor business models like those that are based on hourly or standalone financial planning fees have struggled to take off. As in theory, ‘at scale’, an hourly advisory firm could work with 500 clients each, at $200/hour, for 3 hours per client each year, and generate $300,000 of revenue, while still paying an advisor a healthy $120,000/year (given typical direct costs of 40% of total revenue) just to ‘sit there’ and give advice to those clients.

However, with an average Client Acquisition Cost of over $3,000 per client, it would cost a typical advisory firm $1.5 million in marketing and sales efforts just to get 500 hourly clients that generate $300,000 of revenue. Which means until there is far more demand for financial planning services directly from consumers themselves, and/or a platform that generates hourly and project planning fee leads far more cost-effectively, advisors will never be able to scale such models.

Not because the clients can’t be served profitably, but because getting enough clients to make it work would either require the advisor to spend so much time marketing that they wouldn’t have any hours left to do the work and bill the clients, and/or would require so much in hard-dollar marketing costs that the advisor simply wouldn’t be able to generate enough revenue to make it back.

Thus, instead, advisors tend only to take hourly or project planner fees when the leads come in passively (as at that point, the prospect is already there, and thus is still profitable to service at the margin). Or the firms remain ‘stuck’ operating on such hourly or project fee models, with average revenue per client that is smaller than the AUM or recurring-retainer/subscription models with higher lifetime client value (and that therefore can generate a positive return on their marketing efforts).

Still, though, the other implication of this research is that there’s still substantial room for financial advisors to reduce their marketing costs and grow more effectively. As ironically, “robo-advisors” have been lambasted in recent years for having ‘just’ an average client acquisition cost of $500 to $1,000 per client – which is actually 1/3 to 1/6 of the typical human financial advisor’s client acquisition cost!

On the other hand, the relative inefficiency of financial advisor marketing and client acquisition costs suggests there is significant room for third-party lead generation solutions (e.g., the emerging class of advisor directories and paid web listing services), if they can develop processes that generate leads on their platforms at scale (i.e., with lower client acquisition costs), and then pass through (i.e., ‘re-sell’) the leads to advisors in a manner that both profits the marketing platform and reduces the client acquisition costs of the financial advisor. (Though it may require a shift in advisory firms to adopt “business development associates” that can help screen and filter such calls, so the advisor’s marketing efficiency isn’t lost filtering out the inevitable quantity of low-quality leads that come alongside the high-quality ones.)

From a broader industry perspective, the implication of this analysis of Client Acquisition Costs for financial advisors is that in the end, most advisory firms may actually be “marketing constrained”… where client acquisition costs in the aggregate are so high that it takes years to recover the cost of the advisor’s time and/or hard-dollar marketing costs in ongoing profits, which in turn limits how much advisors can actually spend on marketing in the first place. And that the largest advisory firms are outgrowing the smaller ones in part because they have the positive cash flow to be able to afford to invest into the scalable hard-dollar marketing strategies, while individual advisors are primarily constrained to time-based strategies.

Still, though, when considering the true cost of a financial advisor’s own time in business development, it appears that while advisory firms may be constrained by the J-curve of profitability, that there is still an undue emphasis on marketing strategies that substitute the advisor’s limited dollars for the advisor’s limited time, which in the long run can cost the firm even more than just investing more of their revenue directly into marketing and growth!