Executive Summary

Determining a client's risk tolerance is a standard requirement in financial services, both as a matter of best practices, and regulatory minimums. In recent years, though, advisors have increasingly leaned towards doing the minimum required to assess client risk tolerance, due to the frustration that client risk tolerance itself has varied wildly through the bull and bear market cycles of recent years. However, a new study out using FinaMetrica risk tolerance data from before and after the global financial crisis joins a growing body of research suggesting that in reality, client risk tolerance is actually remarkably stable, and that what's changing through market cycles is not the client's risk tolerance, but instead risk perceptions. The significant implications of the research are that planners struggling with unstable client investment behaviors around risk - e.g., buying more in bull markets and selling out in market declines - may actually need to focus more on managing risk perceptions, rather than blaming the instability of client risk tolerance.

The inspiration for today's blog post is a recent new research paper entitled "Individual Financial Risk Tolerance and the Global Financial Crisis" by Australian academics Paul Gerrans, Robert Faff, and Neil Hartnett. The authors looked at the financial risk tolerances of 4,741 investors before and after the global financial crisis in late 2008, using global investor data available from FinaMetrica, arguably the world's leading (and most rigorous and scientifically validated!) risk tolerance assessment tool.

Evaluating Risk Tolerance Over Time

To assess whether risk tolerance changed as a result of the financial crisis, the authors controlled extensively for other demographic details, from gender to wealth to income to education, all of which have been separately shown to have some impact on financial risk tolerance. This narrowed their data set down to 3,368 investors who were tested both before and after the financial crisis with complete (and controlled for) demographic data.

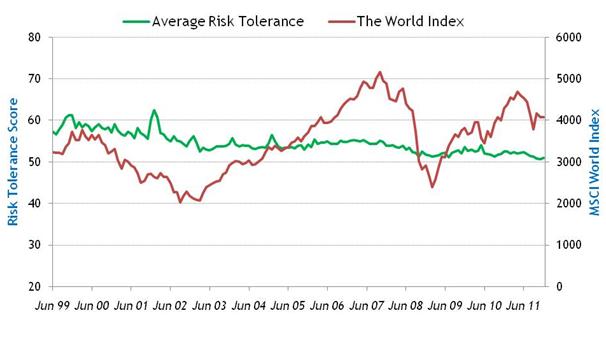

The results of the study found that technically, a miniscule but statistically significant decline in risk tolerance did occur through the financial crisis, but the change was so small that it would not likely lead to any observable difference in behavior and was effectively "stable" over time. This is consistent with other research done using FinaMetrica data, and FinaMetrica's own analysis and review (shown below) that despite volatility of the world markets over the past 12 years, average risk tolerance has remained stable. The very slight downward trend visible in the data is due primarily to the addition of US investors (in 2002) and UK investors (in 2004), who in the aggregate tend to be slightly less risk tolerant than the Australian investors that dominate the early years of data, and consequently bias the average downwards as more of them are included in the total. (Notably, separate research has shown that as investors age, their risk tolerance also declines slightly, and that major life events can affect risk tolerance as well, so an aging sample of investors through the financial crisis would be expected to show a slight downward trend over time.)

To say the least, though, there appears to be no apparent correlation between the trend in risk tolerance and the trend in the world index through the 2002 and 2008 bear markets, or their subsequent recoveries.

Risk Tolerance and Client Behavior

For many planners, the idea that risk tolerance is a stable trait appears to defy the personal experience of working with clients who materially change their portfolios in the face of volatile markets. "If risk tolerance is stable," they argue, "why can't clients stick with their investments?"

The simple answer is that the trait of risk tolerance is not the only factor that affects investor behavior. Instead, investors are ultimately driven by two factors: their risk tolerance, and their risk perception. Risk tolerance determines whether the client is willing to take a specified risk in pursuit of a potential reward. Risk perception is the client's subjective evaluation of whether a particular investment is consistent with that risk tolerance.

For instance, imagine a client whose risk tolerance indicates that it is acceptable to invest in a portfolio that may decline as much as 20%, in order to pursue a long-term return that is 2% higher than a more conservative alternative. In theory, any and every investment that meets this trade-off - can generate a 2% higher return, and is unlikely to decline more than 20% - should be appealing to the investor.

But now let's assume that we're in the middle of a bear market, and the investment in question has just declined 15%. As the behavioral finance research has shown, we have an irrational tendency to overweight what has happened recently, and project it into the indefinite future. As a result, the investor might choose to sell the investment that has declined - not because it violated the client's 20% decline risk tolerance threshold, but because the client's perception is that the current 15% decline might just be the first step of a 25%, 35%, 50%, or 100% loss! In other words, the client perceives the investment to have become intolerable, not because the tolerance changed, but because the perception of risk changed.

In a similar manner, clients in the midst of a bull market tend to be remarkably willing to invest in "riskier" assets. The common assumption is that clients are more tolerant of risk when markets are performing well, but the Gerrans research shown here reveals that is not the case. Instead, the real problem is that when markets are rising and clients provide undue focus to only recent events, clients begin to form the assumption that such investments will always and only go up. Accordingly, even the "riskiest" of investments don't appear to be risky at all, and the investor buys them... again, not because the tolerance for risk increased, but because the perception of risk decreased.

Implications for Clients

In a world where risk tolerance is stable but risk perception varies, the real challenge of difficult clients is in managing their fluctuating risk (mis-)perceptions. If views of risk and expectations are not anchored properly, the client's potential misperceptions of risk - especially because of the prevalence of the recency bias - can lead to wildly inappropriate investment decisions and a greed-fear buy-sell cycle.

Notably, the difficulty in separating risk tolerance from risk perception also suggests that objective and rigorous measures of risk tolerance, such as FinaMetrica's assessment tool, are crucial. Otherwise, in practice, it may be almost impossible to determine from a subjective conversation alone whether the client is truly risk tolerant, or is risk adverse but misperceiving the actual risks involved. The research on the stability of risk tolerance also suggests that questionnaires showing client risk tolerance was rising and falling through market cycles may have been a reflection of the poor quality of the questionnaire, rather than actual risk tolerance changes of the client.

The bottom line is that this latest research puts another nail into the coffin burying the idea that risk tolerance fluctuates up and down with the vicissitudes of the market (adding to the body of research on the topic that FinaMetrica summarizes here). The research reveals that instead, client risk tolerance is actually stable - and can be measured effectively with the right tools - and that what advisors and their clients must focus on the most is risk perception. Accordingly, best practices should include evaluating risk tolerance, designing a portfolio consistent with that risk tolerance, and then providing the ongoing communication necessary to ensure the client continues to correctly perceive the risk of that portfolio, fighting the natural tendencies to over- and under-estimate the risk over time.

So what do you think? If risk tolerance is stable but risk perception varies, would that change how you communicate with clients? Do you try to assess risk tolerance and risk perception separately? How do you communicate regarding risk perception?

Great piece of writing. Where this takes me, in addition to focusing on client communication to impact their risk perception of particular portfolios, is whether there might be an assessment of how variable perceptions might be. Are some clients more prone to perceptual shifts than others? If so, are there tools that help us identify those variables?

Interesting questions. At FinaMetrica we have given some thought to measuring risk perception, how it changes and how to identify those most likely to change their perceptions. It is the first of these that is the stumbling block in terms of trying to develop a tool. The primary difficulty is in finding questions that will be understandable and answerable by clients. Such questions need to be in plain, high-school English but because the topic is so technical this is nigh on impossible.

To help advisers establish realistic client expectations regarding investment performance we prepare a Risk and Return guide which can be downloaded at http://www.riskprofiling.com/systemresources

Our subscribers tell us that, while clients were not happy with what happened to their portfolios in 2008/9, it was within their range of expectations and so they did not experience panicked sales or lose clients.

We believe that it is critically important for clients that their investments are consistent with the risk tolerance and that they understand the risks they are taking, and we provide tools to help advisers on both counts.

What is financial risk? “Risk perception”?. What risk is it that clients are misperceiving? Risk of what is never defined and no question is ever going to capture my tolerance of something I have no idea of. There is no such thing as “risk tolerance” nor “risk perception”. Fear tolerance is what it really is and your opinion of what you might do someday is not valuable. Its interesting to try and and find the answer to how much asset fluctuation a client will allow when they open their mail before they are ispired to self immolate all prospects of success and instead demand a re-allocation to failure. Who is going to know the answer to that in advance? Not me and not you. It is volatility or fluctuation tolerance you seem to be discussing. The fear of failure is the risk we are trying to measure in advance and it cannot be done. The solution is to do the proper job of determinng the reason for and the amount of any inserting any form of volatility onto a clients balance sheet. Thats called determining a volatility/fluctuation budget. It cannot be done properly without a careful study of the clients current or future defined consumption process. Then assets are arranged in a priority of consumption with highly volatile assets arranged far from the part of the portfolio defined as necessary for the defined lifestyle sustenance. Finally, I just read your questionaire. You seem to be trying to determine the profile of which table game in the casino seems most suitable to send the client to. Good luck indeed chaps.

My problem with most any risk-tolerance questionnaires is that advisers get the answers, but then there is no system put into place to make them reality.

If a client says the most they’re willing to lose in a 12-month period is 15%, most advisers do NOTHING to ensure that the max loss is 15%. They may say “Well, this allocation would have gotten you there in the past.”

But literally every piece of investment related literature states “Past performance is no guarantee of future results.” We found this out the hard way in 2000-2002 and again in 2007-2009. How can you tell the client “This should work!” when you know for a fact that it won’t work at some point in the future.

If the portfolio declines 15%, the ONLY way to ensure that the clients wishes are fulfilled is to go 100% to cash.

Yet very few advisers that I know, and no mutual fund managers, use an actual risk budget and position sizes with stops to make it a reality.

I’d also argue that any risk appetite derived from a questionnaire needs to be cut in half. When a client says they can handle 20% loss, they’ll quickly scream “But I didn’t think it would actually happen!”

Finally, I’d love to hear feedback on risk-tolerance vs. “best interests” for the client. If a client says their risk tolerance is a max loss of 10%, but to reach their financial goals it needs to be 20%, doing what they want is not necessarily in their best interests. Do you do what they need despite their desires? Do you fire this client to avoid fiduciary liability?

Just a little more food for thought…

Inspired by your article here.Perception of the risk is really important here whether its a bear market or a bull market.Great post