Executive Summary

Most planners are familiar with the 4% safe withdrawal rate research, first established by Bill Bengen in 1994 and based upon a 30-year time horizon. However, a common criticism of the research is that many clients don't necessarily have a 30-year time horizon - it may be longer or shorter, depending on the client's individual planning needs and circumstances. Yet in reality, there is nothing about safe withdrawal rates that must apply only to a 30-year time horizon. In fact, research exists to demonstrate the safe withdrawal rate over a range of time horizons as short as 20 years (where the safe withdrawal rate rises as high as 5% - 5.5%) or even less, to as long as 40 years (where the safe withdrawal rate falls to 3.5%). And in turn, changing the time horizon and the withdrawal rate also affects the optimal asset allocation, making it slightly more equity-centric for longer time horizons, and far less equity-centric for shorter time horizons. In the end, this means that there is no one safe withdrawal rate; instead, there is a safe withdrawal rate matched to the time horizon of the client, whatever that may be!

The inspiration for today's blog post was a recent question that came up during my presentation "The Impact of Market Valuation on Safe Withdrawal Rates" for the NAPFA DC Study Group - where an audience member asked "All of this research seems to be based on 30 year time horizons; what happens if my client is retiring for longer than 30 years?"

While it's certainly true that the "baseline" safe withdrawal rate research is built on a 30-year time horizon - going all the way back to Bill Bengen's first article in 1994, "Determining Withdrawal Rates Using Historical Data" - the reality is that a great deal of research has actually been done on how the safe withdrawal rate changes over varying time horizons.

The Impact of Longer Time Horizons

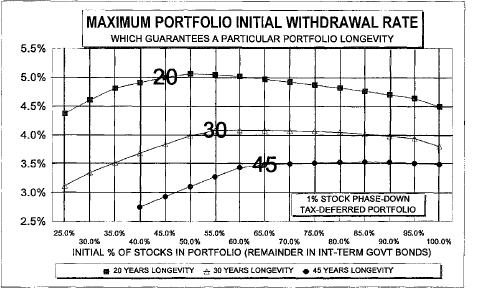

The first article to really look at the impact of changing time horizons on safe withdrawal rates was Bengen's "Asset Allocation for a Lifetime", published in the Journal of Financial Planning in August 1996 as a follow-up to his original seminal paper. In this article, Bengen showed that increasing a time horizon from 30 years out to 45 years reduced the safe withdrawal rate from 4.1% down to 3.5%, as shown below.

These results were similarly supported by David Blanchett, whose 2007 paper "Dynamic Allocation Strategies for Distribution Portfolios" also showed a safe withdrawal rate of 3.5% for a 40-year time horizon (although the primary focus of the article was on setting asset allocation glide paths through retirement). More recently, Wade Pfau's research "Capital Market Expectations, Asset Allocation, and Safe Withdrawal Rates" in the January 2012 issue of the Journal of Financial Planning similarly found a 3.3% withdrawal rate (at a 95% confidence level) for a 40-year time horizon.

Notably, it appears that the safe withdrawal rate does not decline further as the time horizon extends beyond 40-45 years (given the limited research available); the 3.5% effectively forms a safe withdrawal rate floor, at least given the (US) data we have available. The reason for this is relatively straightforward: over long time horizons, even balanced portfolios generate returns significantly higher than 3.5%, and consequently the primary constraint of safe withdrawal rates is just having a withdrawal rate low enough to survive an early 1-2 decade stretch of poor returns. If the withdrawal rate is low enough to survive the first two decades of bad returns, then eventually the good returns arrive, the client recovers and gets ahead, and adding more years to the time horizon is no longer a risk.

The Impact of Shorter Time Horizons

Not surprisingly, if the time horizon is shorter than 30 years, the client can spend more, as the money simply doesn't need to last as long. Accordingly, Bengen's 1996 research showed that for a 20-year time horizon, the safe withdrawal rate rises to 5.1%. Blanchett's 2007 research suggests the 20-year safe withdrawal rate may be as high as 5.5%. Pfau's 2012 research finished in between, at 5.3%.

Little research has examined time horizons materially shorter than 20 years (although Pfau's 2012 research did some analysis in this area), in part because a 15 year time horizon (or shorter) would likely be funded almost entirely using a laddered fixed income portfolio, as the time horizon is too short for any material equity exposure (the upside over the short time period isn't worth the risk). As a result, the "safe" withdrawal rate in such scenarios would be dictated almost entirely by the available fixed income investments and what spending can be supported as each bond matures and the principal is liquidated (with perhaps some safety margin established for the possibility of unexpected inflation, unless TIPS are used to both create the cash flows and hedge the inflation risk).

Asset Allocation Implications

Beyond the changing withdrawal rates themselves, it's notable that altering the time horizon also affects the optimal asset allocation associated with the safe withdrawal rate. For instance, while both Bengen and Blanchett's research suggests the optimal equity exposure for a 30-year time horizon is approximately 50%-60%, a time horizon stretched to 40+ years merits a slightly more aggressive 60%-65% equity exposure (although Pfau's work suggests more conservative allocations).

On the other hand, a shorter time horizon, where there are fewer years for equities to compound favorably but plenty of years for an adverse bear market to impact the client's sustainable spending, merits a lower equity exposure. While Bengen's research suggested 50% in equities was still appropriate, Blanchett's research suggested that 50% equity exposure was at the high end, and that amounts as low as 30% may be appropriate. Similarly, Pfau's 2012 research indicated an optimal equity exposure of only 25% for clients with a 20-year time horizon.

Matching The Time Horizon To The Client

The bottom line is that while the safe withdrawal rate approach has focused on 30-year time horizons, the methodology to evaluate sustainable spending can be applied to any particular time horizon, and will impact both the safe withdrawal rate itself, as well as the optimal asset allocation to achieve it.

The key, of course, is to match the time horizon of the safe withdrawal rate to the client's own retirement time horizon - which in turn may involve some planning discussion itself. Some planners prefer to assume a 30-year time horizon for a 65-year-old couple, while others use 30 years for a 60-year-old couple and some shorter horizon for 65-year-olds. In addition, different clients retire at different ages depending upon their personal circumstances, and of course some clients are planning not for a joint life expectancy but an single one.

Nonetheless, the fundamental point remains - a safe withdrawal rate can be applied to a client's individual plan and retirement time horizon, but it is important to match the right spending and asset allocation amounts to the appropriate time horizon for that particular client.

So what do you think? Do you incorporate safe withdrawal rates into your spending discussions with clients? Do you modify the safe withdrawal rate based on the client's time horizon? Would your planning shift if you discussed 5%+ safe withdrawal rates with 20-year time horizons, versus 3.5% safe withdrawal rates for 40+ year time horizons? What numbers do you use?

Michael,

Thanks for the very good overview of the relationship between time horizon and safe withdrawal rates.

Regarding asset allocation, I think the reality is that for a wide range of stock allocations, the impact on withdrawal rates is very minimal. The optimal asset allocation is only slightly better than many nearly optimal asset allocations.

If I may direct you here:

http://wpfau.blogspot.jp/2011/11/length-of-retirement-and-safe.html

The second figure, labeled Figure 7, was an extra figure that didn’t make the final cut in the paper of mine you mentioned above. I had too many figures. But it shows how the range of nearly optimal stock allocations is quite wide for many time horizons, and that 35% stocks actually falls into the range of nearly optimal stock allocations for time horizons between 10 and 40 years.

I’ll stop adding links, but just this past Saturday I posted about the different approaches of planning for fixed time horizons and incorporating mortality data to account for the specific probabilities for living to each subsequent age, and some of the impacts that has. That would be another good topic for a blog post by you, as I’d be interested to hear your thoughts.

Best wishes, Wade

I have an issue with the following inconsistency.

Let’s assume we have a 65 year old and are using a 30 year time horizon and we are using a 60% equity allocation. The safemax calculations assume that the 60% equity allocation is maintained for the duration.

But now let’s advance this person 20 years to age 85. They clearly no longer have a 30 year time horizon. Instead it is probably more like 15 years at this point.

From your article you mentioned that a 15 year horizon is probably too short for equity exposure (i.e., should just use bond ladder).

So this raises two questions.

1. How do we migrate the portfolio from a 60% equity exposure to a 0% equity exposure over those 20 years?

2. Do safemax calculations have to be redone to incorporate changing allocations?

David

FYI, my answer to #1 is that the allocation level in any given year is dependent on both the time horizon and market valuation. And my answer to #2 is yes.

David,

You are bringing up a good point.

One variable withdrawal strategy I’ve seen describes using the SAFEMAX over time for increasingly shorter retirement horizons. But this implies that valuations will keep rising higher and higher for the SAFEMAX to continue being necessary.

At the same time, I think the optimal withdrawal strategy for someone who doesn’t worry much about bequests is to annuitize a minimum floor if desired and otherwise withdraw something along the lines of 1 / remaining life-expectancy for the rest of retirement.

Best wishes, Wade

I have two SWRs in my own planning – pre-Social Security (~10 years), then post-Social Security which drops the rate significantly.

At my age (early 50s) I’m pretty confident some semblance of Social Security will exist for at least the first few years of my retirement.

I’ve also noticed that making it through the first decade is critical – once you are through 10 years, you should be set for the long term.