Executive Summary

In recent years, a new form of retirement income annuity solution has been gaining visibility: the longevity annuity. A "cousin" to the more familiar immediate annuity, the goal of the longevity annuity is similar - to provide income for life - but the payments do not begin until years (or even decades) after the purchase. As such, these "deferred income annuities" can provide significantly larger payments when they do begin - e.g., at age 85 - in light of both the compounded interest and the mortality credits that would accrue over the intervening time period.

However, a fundamental complication of the longevity annuity is that if retirees want to use retirement account dollars but the payments might not begin until as late as age 85, there is a direct conflict with the required minimum distribution rules that compel payments to begin at age 70 1/2. To address this challenge, the Treasury has issued Treasury Regulations under 1.401(a)(9)-6 that resolve this conflict, declaring that as long as a longevity annuity meets certain requirements, it will be deemed a "Qualified Longevity Annuity Contract" (QLAC) and automatically be deemed to satisfy the RMD rules even though payments don't begin until later.

While the new Treasury Regulations may be a boon to annuity companies that wish to sell longevity annuities, though, it's unclear whether the new rules will real impact anytime soon, for the simple reason that longevity annuity purchases have been growing but still represent barely 1% of all annuity purchases; to say the least, consumers have not been banging down the door to buy such contracts, in their IRAs or otherwise. In fact, given that most consumers are reluctant to buy immediate annuities where they surrender their lump sum liquidity to receive payments for life, it's unclear why they would feel better about a similar contract with payments that don't begin for decades! And in the end, the actual internal rate of return on longevity annuity payments - even for those who live to age 100 - is not necessarily very compelling yet compared to available investments or even delayed Social Security alternatives. Nonetheless, when interest rates eventually rise, and as longevity annuity pricing becomes more competitive, the payout rates for longevity annuities will likely rise as well... and the new Treasury Regulations do at least open the door to longevity annuities inside of retirement accounts if they eventually become more compelling!

What Is A (Qualified) Longevity Annuity Contract (QLAC)?

The longevity annuity – also known in some circles as the Deferred Income Annuity (DIA) – is similar in principle to an immediate annuity, where a lump sum is converted into a lifetime stream of payments. The key distinction, however, is that with a longevity annuity, the payments for life don’t begin immediately. Instead, they start at some point in the future.

For instance, a $100,000 contract purchased by a 65-year-old couple might stipulate that payments will not begin until they reach age 85. However, the couple does reach age 85, payments of $2,656.20 will commence and be payable for as long as either remains alive. Notably, the trade-off here is rather “extreme” – if the couple dies anytime between now and age 85 (assuming both pass away), the $100,000 is lost. However, if they merely live half way through age 88, they will have recovered their entire principal, and from there will continue to receive $31,874.40/year thereafter, a significant payoff for “just” $100,000 today.

Of course, the payout rates will vary depending on the starting age. If the 65-year-old couple begins payments at age 75 instead of 85, the monthly payments are only $934.18/month, instead of $2,656.20. The couple could also purchase a single premium immediate annuity at age 65 with payments that start immediately, but the payouts would only be $478.91/month. Thus, in essence, by introducing a 10-year waiting period, the payments more than double; by waiting 20 years, the payments more than quintuple! And if the couple starts even earlier, the payments are greater; a longevity annuity purchased for $100,000 at age 55 with payments that don’t begin until age 85 receive a whopping $4,054.10/month ($48,649.20/year!) if at least one of them remains alive to receive the payments! Alternatively, the couple could include a return-of-premium death benefit (to the extent the original $100,000 is not recovered in annuity payments, it is paid out at the second death to the beneficiary), which would drop the payments to a still-significant $3,690.30/month. (Quotes are from Cannex, as of 7/8/2014)

In essence, the concept of the longevity annuity is to truly hedge against longevity; while the couple may receive limited payments if they don’t survive, the payments are very significant relative to the starting principal if they do live long enough; in fact, the payments can be so “leveraged” against mortality that the couple doesn’t actually need to set aside very much in their 50s and 60s to fully “hedge” against living beyond age 85 (which also makes it easier to invest for retirement when the time horizon is known and fixed to just cover between now and age 85!).

In theory, a longevity annuity could be purchased with after-tax dollars (a non-qualified annuity), or within a retirement account. After all, the reality is that for many people, the bulk of their retirement savings is currently held within retirement accounts, and if there’s a goal to use a longevity annuity to hedge against long life, those are the dollars to use!

Unfortunately, though, there’s a major problem with holding a longevity annuity inside of a retirement account: how do you have a contract that doesn’t begin payments until age 85 held within an account that has required minimum distributions (RMDs) beginning at age 70 ½!?

Final Treasury Regulations Provide Rules To Coordinate An RMD And A QLAC

To address the fundamental conflict between the structure of a longevity annuity and the RMD rules, the Treasury issued Proposed Regulations 1.401(a)(9)-6 in 2012, and the Regulations were finalized last week. The basic approach of the Regulations is to define a “Qualified” Longevity Annuity Contract (QLAC), and then declare that any longevity annuity that meets the QLAC requirements will not be in conflict with the RMD rules.

To be eligible as a QLAC, a longevity annuity must meet the following requirements:

- Only 25% of any employment retirement plan (or 25% across all pre-tax IRAs aggregated together) can be invested into a QLAC.

- The cumulative dollar amount invested into ALL QLACs across all retirement accounts may NOT exceed the LESSER of $125,000 (original regulations were only $100,000), or the aforementioned 25% threshold. The $125,000 dollar amount will be indexed for inflation, adjusted in $10,000 increments.

- The limitations will apply separately for each spouse with their own retirement accounts.

- The QLAC must begin its payouts by age 85 (or earlier)

- The QLAC must provide fixed payouts (not variable or equity-indexed), though it may have a cost-of-living adjustment (COLA)

- The QLAC cannot have a cash surrender value once purchased (i.e., it must be irrevocable and illiquid), but it can have a return-of-premium death benefit payable to heirs as a lump sum or a stream of income

If the longevity annuity meets the above requirements to be deemed a QLAC, then the value of the QLAC is excluded when calculating RMDs (for other retirement assets), and the payments from the QLAC (whenever they begin) are implicitly assumed to satisfy their RMD obligation (though the QLAC payments will not satisfy RMDs for any other retirement accounts).

Example. Jeremy purchased a $50,000 QLAC at age 65 that will begin payments of $15,937/year at age 85. In addition, he has $400,000 of other IRA assets. By age 70 ½, his IRA has grown to $600,000, and he must begin to take RMDs from the account. His RMDs will be calculated only on the $600,000 account balance, and not include any implied value from the QLAC. Moreover, when Jeremy turns 85 (and we’ll assume his IRA is up to $900,000), he will begin to receive his $15,937/year payments from the QLAC begin, he will still have to take RMDs from his $900,000 IRA (and cannot count any of the $15,937/year QLAC payments towards his IRA’s RMD). The $15,937/year payments from the QLAC itself will automatically (because the QLAC was qualified in the first place) be deemed to meet the RMD rules for that portion of Jeremy’s assets.

Notably, longevity annuities purchased in Roth accounts are not considered QLACs, for the simple reason that Roth IRAs do not have RMDs to comply with in the first place; as a result, an unlimited amount of longevity annuities could be purchased within a Roth IRA (if desired), and the account balances and longevity annuities inside Roth IRAs are not counted towards the $125,000 and 25% limits.

For contracts purchased in traditional retirement accounts (IRAs or employer retirement plans), the dollar and percentage limits do apply. In practice, most investors will be limited to 25% of retirement accounts, as until they have at least $500,000 of retirement accounts the 25% limit will hold (only with accounts greater than $500,000 would the $125,000 dollar limit be the lesser of $125,000-or-25%). On the other hand, each spouse could invest this much into a QLAC, effectively doubling the longevity annuity amount for a couple (if desired).

New Rules Allow You To Buy A QLAC Longevity Annuity In An IRA, But Should You?

While the Qualified Longevity Annuity Contract (QLAC) rules allowing a longevity annuity to be owned inside of a retirement account were essential to avoid running afoul of the RMD rules, the question still arises: a (qualified) longevity annuity can be now purchased inside of a retirement account… but will anyone actually want to?

Thus far, the industry statistics suggest that demand for the products is still weak. In 2012, longevity annuity purchases topped $1B for the first time (averaging $250M per quarter), and in the first quarter of 2014 they’re up to $620M (an annual pace of almost $2.5B). However, the first quarter of 2014 also saw $57.7B of total annuity sales, which means longevity annuities only make up barely more than 1% of all new annuity transactions. By contrast, even single premium immediate annuity purchases were $2.5B in Q1 of 2014, nearly quadruple the pace of longevity annuities. Nonetheless, interest in longevity annuities does seem to be growing, and more companies are throwing their hats into the ring with new products.

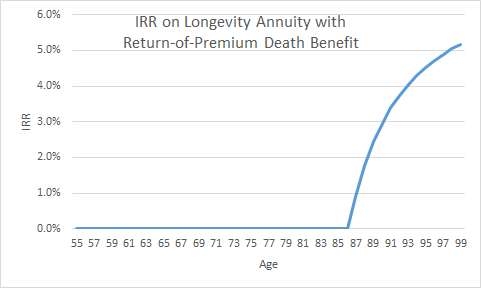

At a more basic level, though, the fundamental challenge is that in a world where consumers are often loath to purchase an immediate annuity – ostensibly out of concern for losing their liquidity and their upside potential – it seems even more of a stretch for a longevity annuity to be compelling, with the same problems but no payments until what may be decades from now. Fortunately, the common “what if I get hit by a bus” fear can be mitigated at least, with the purchase of a return-of-premium death benefit, though such guarantees just lower the payments even further. For instance, the 55-year-old who purchases a longevity annuity for $100,000 will get guaranteed payments of $3,690.30/month starting at age 85 with a return-of-premium death benefit along the way. However, if we calculate the actual internal rate of return being generated on the longevity annuity over the time period, the results turn out to be less compelling, as shown below.

As the results reveal, it still takes until age 87 before the couple actually receive back their original principal and begin to generate any actual “return” on their dollars. Even by age 90, the internal rate of return is only 3%, and by age 100 it’s still only 5.3%. While 5.3% certainly isn’t a “bad” return from an annuity company, over a 45-year time horizon it’s still not a very compelling return either, as a combination of both interest rates and mortality credits. Even in today’s low-return environment, long-term corporate bonds pay close to those yields, and the long-term return on equities is highly likely to beat 5.3% over 45 years as well (especially given that no cash flows are assumed for 30 years, which provides a significant barrier to fend off market volatility along the way).

In other words, while it might be nice that a longevity annuity can give a significant payment that's "guaranteed for life" beyond age 85, if its internal rate of return is low enough, the truth is that a simple conservative investment over the same time horizon might have generated even more cash flow over any foreseeable age of death (even with very long life). Similarly, because the internal rates of return are modest, using a QLAC in a retirement account to defer the onset of required minimum distribution (RMD) obligations isn't very effective either. And the reality is that delaying Social Security – which itself is implicitly a longevity annuity – still has a far better implicit payout rate as well compared to today’s commercial longevity annuities, especially given that Social Security is inflation-adjusted while a longevity annuity also runs the risk that unexpected inflation will significantly degrade the purchasing power of its guaranteed income. (Some contracts do provide inflation-adjusted payments starting after age 85, but still require the retiree to "guess" - and risk being wrong - at what inflation will be between today and when payments begin.)

Notwithstanding the not-terribly-compelling implied returns that longevity annuities provide in today's marketplace, the potential remains for longevity annuities to become an increasingly significant part of the retirement income puzzle, especially if/when/as interest rates rise (boosting future payouts), and/or more companies enter the marketplace (potentially making longevity annuity pricing more competitive – i.e., with higher payouts). And for those who do find a longevity annuity compelling, for at least a portion of retirement income… the new QLAC regulations do at least permit investors to own such contracts inside their retirement accounts. And while the dollar amount contributions remain limited, from a practical perspective a retiree would likely only put a portion of funds into a longevity annuity anyway (as they still need to fend for themselves between now and when payouts begin!).

In the end, though, whether prospective retirees will pursue such trade-offs or not remains to be seen, and thus far it appears the "breakthrough" of the Qualified Longevity Annuity Contract (QLAC) regulations is more about permitting insurance companies to sell longevity annuities inside of retirement accounts than consumers demanding to do so, especially once guaranteed payouts are converted into the equivalent not-terribly-high return they're providing over the ultra-long time horizon. Nonetheless, if guaranteed future payouts get higher in the coming years as rates rise and the marketplace heats up, longevity annuities might get a whole lot more interesting.

I agree with you that there are better hedges for old age than longevity annuities. In a Roth IRA or non-retirement account, one option is to purchase U.S. Treasury STRIPS that mature at perhaps 80 or 85 years of age and at maturity time, buy an immediate life annuity with the proceeds. This has several advantages over a longevity annuity purchased years or even decades in advance: (1) the bonds can be cashed out prior to maturity and may be worth considerably more than their cost if held for many years, (2) the counterparty risk (i.e., of an insurance company going insolvent) is eliminated, (3) not all — or any — of the maturing bond proceeds have to be committed to the immediate annuity, and (4) if one spouse dies — or has significantly impaired health — prior to purchase of the immediate annuity, the immediate annuity can be written for larger annual payouts than would be possible with a longevity annuity (e.g., written as a single life annuity or an impaired life annuity). By my calculations, if I purchase the STRIPS around age 60, then after about age 80-85, the IRR with this method is about 50 bp less than with a longevity annuity. However, this seems like a small price to pay for the advantages and flexibility outlined above.

You might want to fix the title-seems to be missing a word or two.

Similarly, 2nd sentence shouldn’t end with “the year”; maybe

“retirement”.

Anyway, good article, putting the “landmark” ruling

into proper perspective. Let’s wait for the interest rates to perk up a

bit before rushing out to buy a QLAC.

Patrick,

Ack, thanks for catching these. Fixed now. That’s what I get for doing late-night writing after our power outage earlier this week! 🙂

Michael, did your comparison of longevity annuities versus long-term bonds take into account the tax advantage of reducing the RMD by purchasing the annuity within an IRA? That’s a big deal, no?

Buchro,

No, I haven’t specifically tried to measure the implicit value of the additional deferral period within the IRA by using a QLAC. I suspect the ultimate value will be modest, due primarily to the fact that the underlying growth rate of the investment is modest (and that’s what we’d use to calculate the increased future value of the tax deferral).

There’s clearly SOME value, and it’s SOME benefit… just not sure how huge it will really be in the end and if that would be enough to drive a decision to use the QLAC. Stay tuned for further analysis though…

– Michael

Comparison to Social Security is not apples-to-apples. The Longevity annuity is a Cash Refund – show the IRR of a Life Only QLAC (SSI is life only) and then tell us which has better implied returns 🙂

Joe,

Fair point. I’m working on some follow-up material on this for my newsletter that does look at this on a life-only QLAC basis (or just life-only longevity annuity in general). Not surprisingly, the life-only QLACs are better, though the IRRs still noticeable lag Social Security. (They become somewhat more compelling relative to other investments, though.)

– Michael

While I agree with the conclusion (not yet an attractive product) the analysis is far from complete.

With the exception of specific tax benefits granted to certain insurance products an insurance carrier is always standing between an investor and the capital markets looking to obtain a portion of funds. That is why they’re insurance companies. **For that reason the goal is to use the least of it to handle whatever risk you’re trying to cover, and that means analyzing ROP longevity annuities doesn’t make any sense at all.** The only ones worth analyzing are the non ROP longevity annuities at 85 (which I don’t get why the treasury regulated age for QLAC because conceivably you would want to move that out to as far of an age you felt the rest of the portfolio could comfortably handle to get the most mortality leverage out of each $1 used).

How do you analyze an age 85 longevity annuity with no ROP.

Step 1 compute the actual implied leverage without mortality

–Let’s assume that SPIA payout rates actually represent fairly efficient pricing relative to capital markets given the level of competition in that space (I don’t really agree with that, but it’s a fair assumption). So let’s use 8.75% payouts at age 85 as a future SPIA assumption.

–Let’s use your example of $2656 per month at 85 from $100k at 65. $2656*12/.0875 = ~$365k. IRR on $100k to $365k in 20 years is 6.7%. That is without any adjustments for mortality. Quite literally junk pricing before considering mortality issues.

Step 2: Adjust the return by mortality risk

–Same SPIA assumption

–From some readily available data the odds or passing away between the ages of 65 and 85 are roughly about ~45% to someone 65 today.

–(1-.45)*$365,000 = ~$200,000

–Time value $100,000 to $200,000 over 20 years and you get 3.53%. Not particularly attractive.

This is why the treasury should have not established an age limitation. In theory as this industry is just taking hold insurance companies would want to sell and consumers would want to buy the farthest out policies first to procure the most financial leverage for the least amount of funds.

I.e. it would appear to be actuarially sound to offer up approximately $4,000 a month starting at age 95 with $10,000 invested today at 65. Only 1 in 8 people would actually live long enough to receive it, but everybody retiring at age 65 (for example) could plan on 30 exact years for retirement needs. Now the fact that the actuarial return the insurance carrier is offering is sub 3% on a statistical basis doesn’t matter because the leverage the insurance has makes the statistical yield immaterial by comparison.

Then again I’ve never seen an annuity payout rate for someone over the age of 85 that actually seemed to make all that much sense though either. Life expectancy of only ~3-5 years? Okay here’s 10% a year.

You need to track your networth on a 10yrs basis excluding the annuity. There you will find the answer the income is there but your dead.

The benefit on the longevity annuity, assuming the buyer thinks logically, is that they will take more risk with other assets. If you know that you have a known and guaranteed source of income in the future, logically, one would be more apt to invest in equities. So the annuity may indirectly push many retirees to have 50%+ of their portfolio invested in equities–a percentage that studies prove they “should” have but most shy away form.

It is possible to buy longevity insurance inside a Roth IRA. The payments and accumulation are both tax free. This makes the tax equivalent yield perhaps 20% higher. True?

Midhenry,

Yes, it’s possible to buy longevity insurance inside of a Roth IRA. The distributions will be tax-free, as is the case for any Roth IRA.

I wouldn’t really say that makes the tax-equivalent yield 20% higher though. The yield is the yield. The nature of the Roth doesn’t change the yield of the investment, because the tax treatment is dependent on the Roth itself, not the investment. WHATEVER you own inside the Roth is going to be tax-free.

– Michael

It seems to me it might be a good idea to push out the decision to purchase the longevity annuity as long as possible till age 80 plus to and the client has a good chance of needing to hedge the tail risk of a long life.

Jason,

Waiting until age 80 to purchase a longevity annuity is really just “waiting to buy an immediate annuity” in the first place.

You can do that, but the problem is that waiting to purchase eliminates any opportunity to generate mortality credits during the waiting period. Which means, all else being equal, you’d have to invest for aggressively from now until 80 than your money would have otherwise been invested within the longevity annuity, to make up for the fact you’re not participating in the mortality pool and mortality credits as a survivor.

Or viewed another way, having your money at mortality risk between now and then makes it cheaper to buy the future income than just waiting and buying it later. That’s inherent to the pricing of lifetime annuitized income.

Not to say that’s necessarily a “bad” trade-off, but it IS a trade-off that you’d give up by waiting.

– Michael

Michael- I agree, waiting till age 80 would not be best. What risks do you see in delaying buying a longevity annuity like 6 months while the clients wait to see what happens with interest rates? What impact would this have on mortality credits? Thank you for your help.

Greg,

Every little bit of waiting is giving up a little bit of mortality credits. Will waiting 6 months be disastrous if rates DON’T increase? No. But if you wait 6 months and they don’t increase, and then you wait 6 more and they still don’t increase, and they you wait 6 more because “now it must be happening soon”… you risk the frog-boiling-in-a-pot-of-water phenomenon.

Certainly waiting and having rates materially rise will be good news, but it still comes back to how long you’re going to wait for it to happen. And remember it has to be LONG-TERM rates that rise. If the Fed raises short-term rates and the market predicts a recession and the long-term rates fall further, it just gets worse. That’s the risk of trying to time interest rates. :/

– Michael

You missed the big selling point, its deferring RMDS.

I’d be curious to see if Bill Reichenstein has done any research with the QLAC as it relates to finding a segment of the population where the benefit is less tax on Social Security Income. It would seem to me that possibly tabling a portion of qualified assets into QLACs for the lower middle class may help optimize taxation of SS Benefits. Just a thought.

If you are not paying any tax on ss you dont have any extra money to invest. Get Real!

A risk of waiting is that interest rates don’t rise fast (six years and counting) but longevity rises making annuities more expensive http://goo.gl/ZcjwYX

One reason longevity annuities have not gained in popularity is because sales commissions are very low for this type of annuity. Insurance agents and “financial planners” will always tout the products that give them the highest payout. I had never heard of this product until I happened across it in a book. As you can tell, I am skeptical of those selling annuity products. Even is this is a good product for me it is doubtful that anyone would recommend it to me. Caveat Emptor.

Financial planners are planning for their future by planning for yours!

Minor nit: It is Qualifying Longevity Annuity Contract not Qualified

Regards

Brian

Brian,

I don’t see “Qualifying” used anywhere in the article?

– Michael

Right. I am saying that the proper name is “Qualifying LAC” and not “Qualified LAC”

Regards

Brian

You dont take RMDs from non qualified money.

You really need to do the numbers, because you can easily over insure yourself . You need to keep track of your net worth excluding annuity on a 10 yr basis. You will find if you live past about 115 it might be a good deal. So maybe its not such a good idea.

Does you rate of return account for income tax saved by lowered RMDs? Thanks

Time to Update the article with Secure act 2.0