Executive Summary

While much has been written about the inherent benefits of delaying Social Security benefits to age 70, a fundamental challenge in the real world is that the decision cannot be viewed in the abstract. The decision to delay Social Security isn't just about the value of delaying, but also about the money that must be spent from the portfolio to sustain spending in the meantime, and/or the decision to allocate money towards delaying Social Security and not towards other fixed income investments or a commercially available lifetime immediate annuity.

Yet a deeper look reveals that when viewed from an investment perspective, the decision to delay Social Security actually represents an astonishingly valuable "investment" return, based on the internal rate of return of the cash flows that it provides over time. While it is certainly unlike other more "traditional" investments, in that its return is based not on interest rates or market performance but on the longevity of one's life, for those who do live a long time the decision to delay Social Security can produce real (inflation-adjusted) returns of 4%, 5%, or even 6% for those who live into their 90s and beyond.

Calculated in this manner, the reality is that for those whose greatest retirement "risk" is living far past life expectancy, the decision to delay Social Security can actually be a highly beneficial investment, with a real return that dominates TIPS, is radically superior to commercially available annuities, and even generates a real return comparable to equities but without any market risk! Of course, there is still an aspect of "mortality risk" inherent in the decision to delay, but for those who are most concerned about living a long time and funding a long retirement, the decision to delay Social Security - even if it means partially spending down the portfolio in the meantime - can actually be the best means to securing a successful retirement, by converting the uncertainty of market returns into the certainty of higher Social Security payments!

Adjusting Benefits Based On Social Security Timing Before/After Full Retirement Age

The rules for Social Security allow for a certain benefit at full retirement age, which is then adjusted upwards or downwards by beginning early (as early as age 62) or delaying until later (as late as age 70). For every year benefits begin early, they are reduced by 6.66% per year (up to 3 years, and then reduced by "only" 5% for additional early years), and are increased by 8% per year (until the maximum age 70) for starting late. Because the exact "full retirement age" itself varies between age 65 and 67 depending on year of birth, the exact magnitude of the adjustment will vary. For those born between 1943 and 1954, who will be age 60-71 this year, the full retirement age is 66, which means starting at age 62 will reduce benefits by the maximum 25% (3 years x 6.66% = 20% plus 5% for the 4th year = 25% reduction), and delaying them to 70 will increase by the maximum 32% (4 years x 8% = 32% increase).

In dollar terms, this means an individual who was otherwise eligible for a $1,000/month retirement benefit at full retirement age would have benefits reduced by 6.66% to $933/month by starting a year early, or increased by 8% to $1,080/month by delaying a year. At the extreme, that individual would only get a $750/month benefit by starting as early as possible (at age 62), or could get as much as $1,320/month by waiting as long as possible (to age 70). (Notably, these benefits would also be adjusted annually for cost-of-living adjustments, so these represent real inflation-adjusted benefit amounts at various ages). On a relative basis, this means the decision to delay benefits by the full 8 years from the earliest possible (age 62) to the latest possible (age 70) actually increases the inflation-adjusted benefit by $1,320 / $750 = 76%.

Often the decision to delay benefits is explained as being the equivalent of an 8% annual return (for those delaying past full retirement age), or a 76% cumulative return over 8 years (for delaying all the way from age 62 to 70). However, the caveat to making the decision to delay is that it also has a non-trivial "cost" in the form of benefits that aren't received (and can't be invested or consumed) today. While this certainly doesn't eliminate the value of delaying Social Security benefits, it does make the trade-off more complex and nuanced than just (incorrectly) equating it to an 8%/year (or 76%-per-8-years) returns.

Calculating The Benefit Of Delaying Social Security

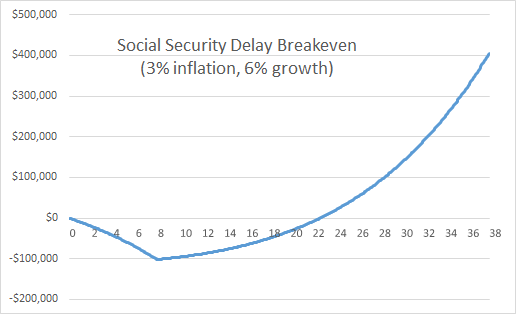

To value the trade-off of delaying Social Security - no benefits paid now, in exchange for incrementally higher benefits in the future - we must calculate the economic value of the exchange. Accordingly, the chart below shows the impact over time of not receiving $750/month (increasing annually for inflation) from age 62 to 70, which then begins to be offset by the higher (inflation-adjusted) payment stream that begins at age 70 itself. Since benefits not paid from age 62 to 70 represents a foregone investment opportunity (either the money could have been invested if it wasn't needed, or it could have been consumed and thereby allowed other assets to remain invested), we must account for not only the $750/month (at age 62) versus $1,320/month (at age 70) benefits, but also for inflation itself (assumed here to be 3%) and this time-value-of-money factor (projected at 6%, a "balanced" portfolio rate of return that could have been earned on the money invested or not-consumed).

As the results reveal, it can take a long time to “recover” from not receiving $750/month (and having the opportunity to invest it, or keep an equivalent amount invested by having the Social Security dollars available to spend). The “breakeven” period with these assumptions is just over 22 years; or stated another way, for the individual who chooses to delay from age 62 until age 70, it takes until beyond age 84 just to recover the economic value of having waited. Notably, though, beyond that point the benefit in favor of delaying Social Security continues to accrue, exponentially, as the compounding time value of money now works in favor of the delay decision, in addition to the fact that the higher delayed benefit is also enjoying ongoing cost-of-living adjustments.

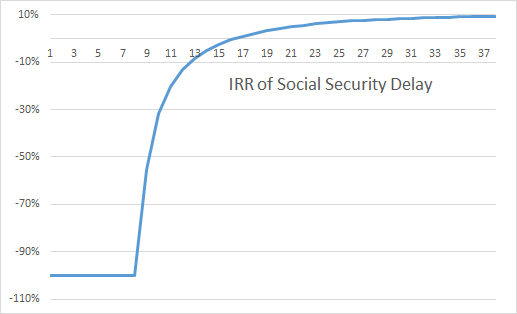

Of course, the point to breakeven is sensitive to the return assumption used. At a greater rate of return, the breakeven takes longer; with more conservative return assumptions, the breakeven is reached more quickly (as there’s less impact to delaying Social Security if the foregone dollars are assumed to not have been able to earn much anyway). In fact, another way to look at the situation is to determine what breakeven rate of return would have been necessary at various points along the time horizon to have achieved a comparable result; in essence, this is simply an analysis of the internal rate of return on the decision to delay (and foregone payments) compared to the higher dollars ultimately received.

As these “Internal Rate of Return” (IRR) results show, delaying Social Security is a “risky” proposition, in that passing away shortly after the delay results in a total loss of foregone payments. Once benefits begin after year 8, it still takes another 8 years for the “excess” payments to make up for the years that early benefits weren’t received (i.e., the IRR crosses 0%), and then another 6 years until the IRR actually equals a 6% growth rate (8 years + 8 years + 6 years = the 22 year breakeven shown earlier at a 6% growth rate).

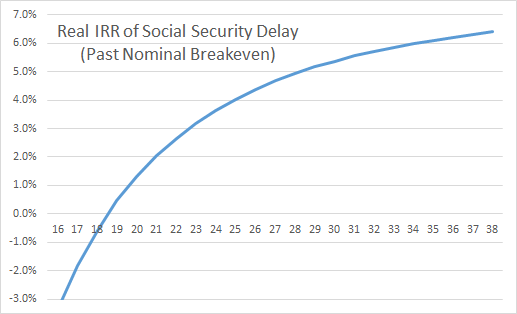

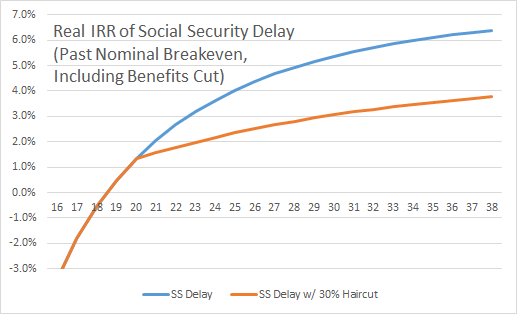

However, beyond that point the IRR continues to increase… on what, in the end, is a “guaranteed” rate of return backed by the Federal government. In fact, the implicit “return” of delaying Social Security is not just a nominal return, it is also a real return, since benefits are adjusted annually for inflation (which was assumed above to be 3%). Accordingly, the chart below shows how the real (inflation-adjusted) IRR trends in the later years, starting in year 17 (when it turns positive) until year 38 (when the individual would be reaching age 100).

While by definition these real returns are only available to those who live to later years at or beyond life expectancy, the results are quite significant. Those who reach age 90 (which would be the 28th year after delaying) have generated the equivalent of a 5% real rate of return in what is essentially a government-backed bond!

Comparing Social Security Delay To Alternatives

Delaying Social Security Versus Bonds

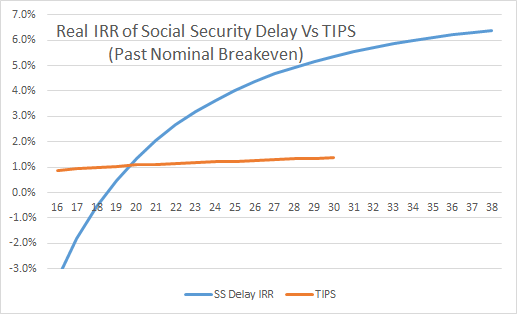

Given the charts above showing the implicit return generated by delaying Social Security, we can compare the value to other investment alternatives. For instance, the chart below shows the real IRR on delaying Social Security versus a comparable TIPS yield along the current yield curve.

As the results show, it does take until nearly year 20 before the real return of delaying Social Security is superior to the results from a TIPS yield. However, beyond that point, the economic value of delaying Social Security continues to rise dramatically, producing a real return that is multiples of a comparable risk government bond! And notably, the available return from TIPS ends beyond the 30-year market (there are no longer-dated government TIPS available today), while the value of delaying Social Security just continues to compound higher for those fortunate enough to live long enough!

Delaying Social Security Versus Immediate Annuities

Another way to compare the value of Social Security – which is ultimately a lifetime stream of payments – is to compare it to other commercially available annuities.

Accordingly, we can compare the higher payments received by delaying Social Security benefits from age 62 to 70, to the payments that would be received by accumulating those early payments and simply buying a commercially available immediate annuity at age 70. For these purposes, we assume that the inflation-adjusting Social Security payments from age 62 to 70 are accumulated in a conservative government bond fund (since the time horizon is fairly short) with a 2% growth rate. With a $750/month payment (which was $1,000 at full retirement age, reduced by 25% for starting early) the cumulative value of the benefits would be $86,587 by the start of age 70.

To compare, the chart below shows what can be purchased from a commercially available annuity for males and females at age 70 with $86,587, either on a nominal or CPI-adjusted basis. By comparison, the decision to delay Social Security over those years produces an excess payment of $722/month at age 70 (which is $1,320 with delayed retirement credits, plus 8 years of 3%-assumed cost-of-living adjustments to produce a $1,672/month nominal payment, reduced by the $950/month inflation-adjusted payment that would have been available by having started benefits immediately at age 62).

| Monthly Annuitization Income of $86,587 For 70-Year-Old | |||

|---|---|---|---|

| Fixed Annuitization | CPI-Adjusted Annuitization | Social Security | |

| Male | $572.20 | $425.61 | $722.00 |

| Female | $537.11 | $399.76 | $722.00 |

(Thanks to John Olsen and Cannex for providing immediate annuitization quotes for this research!)

As the results reveal, the payments produced by Social Security dominate the nominal or real payments available from a comparable commercially available annuity. This appears to be due primarily to the assumptions that are embedded in the Social Security formulas and benefits, many of which were built when longevity was shorter and interest rates were higher; compared to annuities available today (which use current longevity and rate assumptions), the Social Security delay decision is far superior. Which means, in essence, if a retiree has any plans annuitize assets at all, the “best” annuity to be had is actually to delay Social Security benefits (where the “purchase price” are personal assets spend from age 62 to 70 while waiting for the higher Social Security payments to begin).

One important distinction, though, is that Social Security – as it is essentially a “straight life” annuity – does represent a “riskier” form of annuity, in that any death that occurs during the 8-year delay time window results in a total loss, and also that there is not a “period certain” option to ensure payments will continue for a specified number of years as is the case with commercially available annuities. On the other hand, the annuity quotes above also assume no period certain payment, and the inclusion of such a payment would just make the commercial annuity quotes even lower and the Social Security delay look even more appealing. Ultimately, there is a legitimate risk trade-off here for retirees to consider, though arguably the “cost” of getting a floor for those payments is quite significant. In addition, it’s notable that for couples where the higher payment for the individual is also a higher survivor payment for the couple, these delayed Social Security benefits are essentially joint survivorship payments, which makes them even more appealing (as the commercial annuity rates above would be significantly lower if priced for joint survivorship rather than a single life male or female!).

Delaying Social Security Versus Growing Investment Assets

For many, the decision about whether to delay Social Security benefits is not merely a choice about when benefits begin, but a choice about whether portfolio assets will be spent while waiting for the higher payments to start. Which means, ultimately, that the decision to delay Social Security benefits must be discounted by the opportunity cost of not being invested in the portfolio. Or viewed another way, delaying Social Security will only be appealing if the IRR of the Social Security delay produces a superior risk-adjusted return to the return that could have been obtained via the portfolio itself.

In this context, we can refer back again to the implicit real return over time generated by the decision to delay Social Security benefits. As the chart revealed, while it takes many years for the real rate of return to merely turn positive after delaying benefits, in the later years the real returns become very large, crossing about 1.3% after 20 years, 4% after 25 years, 5% after 30 years, and 6% after 34 years.

By contrast, the long-term real return on equities has been “only” about 7%, which represents a 7% equity risk premium over an alternative risk-free rate. Which means for equities to generate a comparable risk premium over the value of delaying Social Security, equity real returns would need to be 8.3% after 20 years, 11% after 25 years, 12% after 30 years, and 13% after 34 years. Arguably, these are questionable real returns to expect in any environment, and even more questionable in the context of today’s above-average valuations.

It’s also notable that these results hold true even if we do nothing to fix the current Social Security shortfall, where the trust fund is projected to run out in roughly 20 years and benefits could only be paid from current Social Security taxes – which would not actually "end" Social Security payments at all, but merely would result in a 30% haircut in benefits starting in 20 years. Yet as the chart below shows, even if the shortfall occurs – i.e., we do nothing to fix the system with adjusted benefits, or higher taxes, at any point in the next several decades – the internal real rate of return over the long run is still compelling. And to the extent we make adjustments sooner rather than later, either through more modest changes to benefits, or an increase in Social Security taxes, the orange line will simply move even closer to the original blue line.

Which means that ultimately, delaying Social Security benefits provides superior risk-adjusted returns to equities and portfolio investing in the long run, both with the current system and even if it’s not otherwise “fixed” as well. Obviously, this is not true in the short run – as noted earlier, it takes more than 15 years to breakeven at all. Yet if the retiree’s time horizon was that short, the proper investment would not likely be equities anyway. In scenarios where there is a long time horizon, and the retiree wishes to hedge longevity by owning a portfolio with long-term growth assets, the reality is that delaying Social Security becomes the superior “long-term growth asset” for the retiree. In other words, spending portfolio assets to delay Social Security becomes the equivalent of liquidating a “low” return asset to buy a “higher” return one instead!

Delaying Social Security As The Best Long-Term Return Money Can Buy

Social Security, and the decision to delay benefits represents a unique form of “investment” – a return that is contingent not upon interest rates or market performance, but survival and longevity. Of course, it’s worth noting that because the value of the Social Security delay decision is contingent on how long someone lives, it is clearly not beneficial for those who are in poor health or are otherwise not optimistic about living a long time (though be certain to look at joint health and longevity in the case of couples planning for survivor benefits, not to mention other couples-specific strategies like File-and-Suspend that may further impact timing decisions).

Nonetheless, the decision to delay Social Security can be evaluated based on the implicit rate of return it creates by choosing to delay, and over longer time horizons – when clients may “need the money most” as they have more years of retirement expenses to cover in the first place – the return of the Social Security delay becomes quite compelling. In fact, the return is generally far superior to any risk-adjusted returns that can be achieved over comparable time periods by the available alternatives, whether investing in risk-free bonds, growth equities, or buying a commercially available annuity. And because the system is indexed to inflation, its real returns will be maintained even if inflation rises, and will only become better if longevity continues to increase as well. In fact, ultimately the decision to delay Social Security delivers the best results when there is either unexpected inflation, unusually long longevity, or especially bad market returns, which are the exact three scenarios that traditional portfolios are the least effective at managing, making the decision to delay Social Security the ultimate form of “anti-fragile” triple hedge!