Executive Summary

The ongoing march of technology and explosion of the internet over the past 20 years is slowly but steadily reshaping the world of investing advice. As more and more tools become accessible directly to consumers, many of the services once provided by financial advisors to analyze, review, and construct client portfolios can now be done at a dramatically lower cost, and without the advisor being involved at all.

In reality, this simply represents the next step in technology continuing to commoditize many of the core services that financial advisors provide their clients, from the days of implementing trades (i.e., actually being a "stockbroker") that's been demolished by online discount brokerage, to helping with the investment search-and-selection process (being replaced by online tools and analytics), to the construction of passive strategic diversified portfolios that can now be accomplished for 25 basis points or less by a number of "robo-advisor" solutions.

Ultimately, this doesn't mean that financial advisors will disappear altogether, as ultimately technology can augment the relationship but not replace it; nonetheless, it will force advisors to continue to evolve their client solutions to stay ahead of the technology commoditization curve, as clients will only pay "so much" for the relationship alone. Some advisors may choose to become more active and (attempt to) deliver a greater value-add with respect to the portfolio itself in the form of alpha, while others may choose to offer financial planning services as a value-add (as many have already begun), and still others may decide to abandon investment management as an offering altogether and focus solely on providing personal financial planning advice itself. Whatever the outcome, though, it seems those advisory firms who hang their hat today on providing little more than the construction of passive strategic diversified investment portfolio for a 1% AUM fee may be in serious trouble, as technology continues to commoditize their core business offering.

Technology Tools For Investment Analysis

Perhaps the most easily evident area where technology has impacted the world of investing is in the capabilities we now have to analyze investments and investment strategies.

Ranging from "the basics" at Yahoo Finance and Google Finance to the more advanced analytics of tools like Morningstar and Bloomberg terminals, to a host of other specialized sites for investment analysis, our capabilities for investment analysis have come a long way from where they were just a few decades ago where we had to leaf through pages and pages of WSJ quotes just to see what price the individual investments in a portfolio closed at the prior day.

On the plus side, these sorts of tools have made it easier to identify and analyze investment opportunities, and also to get better perspective on what to avoid, from investments with poor value to investment managers whose performance doesn't hold up once it can be properly scrutinized - a particularly damaging trend given research suggesting the majority of active managers do not provide sustained (or any) value, and perhaps helping to explain the secular rise of Vanguard and indexing and the hemorraging investment outflows from traditionally actively managed mutual funds in the past 5 years. A more recent crop of tools like SigFig and Jemstep are also making it easier for consumers to analyze an existing portfolio and get immediately actionable advice about what can be improved as well.

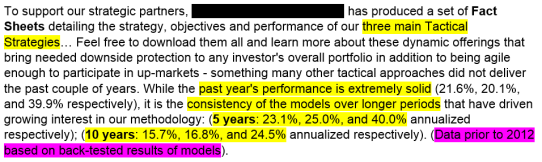

On the other hand, the rise of computing power has also made it easier than ever to analyze historical investments and come up with new strategies, leading to what anecdotally to this blogger seems like a dramatic recent rise in new investment offerings with compelling track records that turn out to be built almost entirely on data-mined history, where "10 year historical returns" turn out to be based on 1 year of an actual track record and 9 years of backtesting, as seen in the real-world example below.

While strategies have to be built on some framework - which means using today's modern computing power to analyze the reams of historical data really could have some value - the extent to which many investment advisors may just be "tricking" consumers (or other advisors?) with dazzling performance numbers accompanied by back-testing disclosures buried on page 5 of the GIPS Supplemental Information is clearly concerning.

Technology Tools For Easier Investment Implementation

Beyond the capabilities of technology to support investment analysis, another way that technology is changing the landscape is how it impacts the implementation of investments and investment strategies.

For instance, it was "just" 20 years ago that the first online brokerage platform came into existence; before that time, buying and selling securities required a phone call to an actual "stockbroker" to facilitate the trade. The rise of online brokerage made it far easier - and far less costly - for investors to implement their investment transactions and strategies, in part by eliminating the need and cost of an actual "stockbroker" to complete the purchase or sale.

Yet while online investing for the past 20 years has primarily been about picking stocks and mutual funds (and more recently, ETFs), the latest technology evolution disrupting the world of investing are the so-called "robo-advisors" - services like Betterment and Wealthfront that will construct the entire asset-allocated passive strategic portfolio for the investor for a mere 0.25% or less. Of course, having a diversified portfolio in a single easy step has long been possible through various multi-asset-class asset allocation mutual funds, but today's technology and offerings allow for similar or better levels of diversification with far more granularity and control.

This depth to the portfolio construction process also makes it feasible to leverage technology tools for additional investment value-adds that were previously done in a more arduous manual processes, from proactive tax loss (or gains?) harvesting, to supporting good asset location decisions. Such services can now be offered effectively directly to consumers and easily implemented via the robo-advisors (or notably, through advisors and their "rebalancing" and trading software tools as well, albeit at a higher cost).

Challenging Implications For Financial Advisors

These technology-driven developments and changes to the landscape are ultimately positive, as they drive down investment costs for consumers and promote better access to investing, but can be very disruptive. On the one hand, the rise of better technology tools for analysis and implementation have the potential to make investment advice more efficient and effective. On the other hand, it also threatens to disintermediate advisors out of the process altogether.

In fact, it is arguably the rise of online investing that spelled the demise of the traditional stockbroker. While the trend began in 1975 when deregulation abolished the (high) fixed fees for trading stocks and instead allowed the marketplace to dictate transaction commission costs, creating the so-called "discount broker", it was the rise of online discount brokerage firms that allowed consumers to disintermediate "stockbrokers" altogether and force them to find a new/different way to add value.

Initially, stockbrokers shifted from being in the brokerage-transaction-implementation business to the "manager search and selection" business of seeking out high quality (mutual fund) managers, aided by technology tools like Morningstar to do the heavy lifting. As mutual funds struggled to succeed in the decade of the 2000s, though, and investment analysis tools increasingly found their way directly to consumers (via direct-to-consumer sites and also the supporting tools from the online brokers themselves), the world of financial advisors shifted again, to a focus on building diversified asset allocation portfolios, and the AUM model rose in popularity.

Now the robo-advisors are threatening to do to passive, strategic diversified portfolio construction what the online discount brokers did to implementing stock trades: commoditize the implementation down to the point of razor-thin margins that disintermediates advisors from the process altogether, including the supporting value-adds like tax harvesting and asset location that can be accomplished by technology.

In turn, these trends of technology providers away from raw transaction implementation (online discount brokerage, technology 1.0) and towards more technology-driven comprehensive portfolio implementation (online robo-advisor portfolio construction, technology 2.0) will force advisors who support investments to once again find a new way to add value. Just as manager search-and-selection became popular after stockbrokering was commoditized, and comprehensive asset allocation and portfolio construction has become popular after manager search-and-selection was commoditized, next financial advisors will likely be forced in one of three directions:

1) Get more active (and really provide value). While there is less and less value in "just" providing a basic passive strategic diversified portfolio, advisors who can really add value with active management strategies will continue to command a premium price. The caveat, of course, is that good active management itself is at best very difficult to do, may not be feasible for many advisors, and requires additional resources to implement effectively (from research tools to support staff). And of course, with all those enhanced analytics tools, advisors should be prepared for their results to be more scrutinized than ever going forward (notwithstanding the significant challenges in effectively measuring and benchmarking active unconstrained multi-asset-class investment strategies).

2) Amp up financial planning (and split pricing accordingly?). For those facing the commoditization of investment management, offering comprehensive financial planning advice is arguably the "anti-commoditizer" because of its complexity and highly personalized nature. For many firms, this trend is already playing out, given the number that provide financial planning in addition to investment management as a form of "comprehensive wealth management" that supports their pricing and value proposition. Ultimately, though, some firms may decide to separate these pricing structures altogether, as the commoditizing force of technology leads to an "unbundling" where firms offer a low-cost "base" price for portfolio management and a separate retainer price structure for financial planning (notwithstanding the problems that can arise when pricing investment management and financial planning separately). In turn, advisors will likely increasingly decide to outsource the investment management process altogether, as there is little value to dedicating internal resources to a commoditized service instead of other more lucrative value-add areas.

3) Ditch investment management altogether and focus solely on financial planning. The last option some advisors may consider is eschewing investment management altogether, and simply focusing on financial planning and/or other services instead. In reality, some parts of the financial planning world - like the Garrett Planning Network - have been moving in this direction already, simply because the investment-management-centric AUM model is not accessible to a wide swath of Americans who need financial advice but don't have assets available to invest. But as passive strategic portfolio construction is increasingly commoditized, more and more advisors may ultimately decide that it's just not profitable enough to stay attached to the AUM model, if they don't have a lot of value to add to the portfolio construction process itself. And of course, as financial planning increasingly shifts to younger generations that don't have assets, alternative models like monthly retainers are more likely to become popular anyway, as indicated by the recent rapid growth of organizations like XY Planning Network.

Ultimately, the sweeping impact of technology on the world of investments is not going to be the end of financial advisors, though it will be a significant threat for those who ignore the trends and continue to charge 1% to offer an increasingly commoditized passive strategic portfolio construction solution at "premium" pricing that isn't justified in the marketplace (in fact, regulators are now starting to scrutinize "reverse churning" where advisors place clients in ongoing-AUM-fee accounts but "do nothing" to provide value for the "high" costs they're charging!). In addition, even the early online discount brokers are evolving themselves in this direction; while trading compromised 60% of Charles Schwab revenue in the 1990s, it's down to only 17% today as the firm shifts itself towards more holistic-portfolio-centric AUM-style models, as online discount brokers have actually commoditized the value out of the very business they disrupted in the first place!

This doesn't mean that all advisors are doomed to be replaced by technology; in the end, technology can augment (advisor) relationships but it doesn't replace a real relationship. Nonetheless, these trends will put continued pressure on investment advisors in particular, to either add more value to their investment offering, better utilize technology to make themselves more efficient, enhance their financial planning and wealth management solutions to justify their total value to clients, or consider stepping away from the increasingly technology-commoditized world of investments altogether and focus on personalized financial planning instead.

So what do you think? Is technology impacting the advisor value proposition? Are "robo-advisors" a competitive threat, or simply pushing advisors to evolve their business models and value? Will technology do more to augment advisors than challenge them, or is it the other way around?

Spot on post. I am giving a presentation on this topic at our annual forum in February. I have talked to a number of top executives at independent firms and wirehouses who are still unaware of these pending threats. There is no doubt that advisors have to get really focused on what value they are bringing to the table or/(and) face meaningful fee compression.

What amazes me is the number of institutions that are multiple steps behind the current state of portfolio management and advice and the massive amounts of assets they have. I believe it is proof that the sensitivity around personal finances remains high and people need a human to understand them. The relationship that a trusted advisor has with their client provides far more than a financial plan. It provides an empathetic foundation to achieve financial aspirations and equally important, comfort from anxiety during turbulent times.

The robo-advisors are currently subsidized by their venture capital investors. The barriers to entry seem low and pent up money is looking for outlets. The competition will spur many technological advancements and possibly regulatory simplification for the benefit of us

all. People aren’t replacing their doctors with WebMD, but doctors now have access to more information than ever before: net positive for everyone. As the robo-advisors push to make it as a business, more and more will look to partner with advisors as opposed to disintermediate them. The smart advisors will be open to learning from the conversation.

Indeed Jamie, my expectation is that ultimately many robo-advisors will find they function better to augment advisors and partner with them, rather than succeed in competing with and replacing them.

However, those still running an ‘old’ business model that don’t acknowledge these commoditization forces will find themselves pressured from all directions!

– Michael

All very good points. That is why the companies who focus on augmenting humans with robo-advisor technology at their core are the most interesting to me. Although they don’t seem to get quite as much press as the two main robo-advisors, I think companies like Learnvest and Personal Capital are in the best position of any of these new entrants to have long term success in the market. It might serve advisors well to focus on learning what they can from their approach in addition to keeping an eye on robo-advisors.

Excellent advice. Been reading and posting a few articles on the topic of technology to my Twitter account lately. More than usual about “robo” stuff.

I think there might be a 4th solution — Develop a financial business firm that is based on the Family Office model — but geared more towards a firms ideal clients.

Many FAs already have strategic alliances with other trusted advisors. Also, where I live, there are “financial buildings” where everyone in the building handles a different piece of finance.

My thoughts are more in alignment of having all that under one firm’s umbrella.

And it’s good that there will always be people around who 1) don’t do their own investing — for whatever reasons. 2) Want and are willing to pay for someone’s advise or help.

Many years ago, when technology hit the trading desk there was talk about not needing traders. Think what people want about people in my previously profession, but there are still traders and a different set of skills/employees needed today by firms. Things are different today, for sure. Technology has added to the field and ease of individuals doing their own trading (something few did or would even think about 30-40 years ago.).

Michael,

How do you think this compares to the field of tax preperation? While H&R Block and TurboTax have used technology to take all the simple situations, I still pay my CPA top dollar for comprehensive tax advice. One would think the financial planning field would be similar. “Advisors” who are selling portfolio management are going away, while advisors doing portfolio management as part of comprehensive financial planning are more valuable than ever. Your thoughts?

Matthew,

There are some parallels to the field of tax preparation, but not as much as many suggest. Tax preparation is a REQUIRED service – to comply with the law – which means it’s something that people “must” buy (or do themselves).

Financial planning and advice, on the other hand, is generally something that has to be SOLD – someone has to be convinced voluntarily that it’s worth paying for. That’s a very different dynamic, and one that is much more human.

It’s very notable that Personal Capital – a company often classified as a “robo-advisor” but actually uses real human beings as advisors, just engaged in a virtual relationship – is being built by Bill Harris, who previously led Intuit. In other words, the guy who RAN TurboTax decided to NOT run the analogous purely-technology solution when coming into the advisor space, but instead the advisor-augmented-by-technology model.

But yes, at the core your comparison around high-end accounting is certainly accurate – inasmuch as TurboTax commoditized basic tax compliance but not value-add accounting and tax advice. The same will be true in the financial advisor world; core components like portfolio construction can/will be commoditized, but personalized advice, not so much.

– Michael