Executive Summary

For some clients, the focus of financial planning is just about protecting the limited resources they’ve got. For others, it’s about maximizing the potential of what their financial resources and their lives can become. The mindset of clients as they approach the world can have a significant impact their behavior.

Yet this mindset of abundance versus scarcity is not unique to clients; in fact, as financial planners our view about the world also shapes our behaviors. For instance, some become active as volunteers in the industry to get involved, give back, and even network for referrals, while others see little purpose in getting involved in a professional association with “the competition” – even though the reality is there are still more than enough clients out there for everyone.

The challenge is that, just as with clients, an excessive fear of scarcity – whether its assets and financial resources, or potential clients for the advisory firm to grow – can actually lead to outcomes that result in scarcity. Extremely conservative investment clients can actually find that inflation undermines their own financial goals, and advisors who are so fearful that there are too few clients can end out wasting time trying to convince mismatched prospects to work with them (even though it won’t be a good fit in the end). So what’s your mindset, and how does it shape your (business) behavior?

Abundance vs Scarcity Mindset in Financial Planning

The inspiration for today’s blog post was a concept once posed to me many years ago by financial planner Jon Guyton, who pointed out that in doing financial planning with clients, some people seem to have an overall mindset of scarcity in how they approach all their (financial) issues, while others have more of an abundance mindset. And the differences in how they plan and prepare for challenges are profound.

The inspiration for today’s blog post was a concept once posed to me many years ago by financial planner Jon Guyton, who pointed out that in doing financial planning with clients, some people seem to have an overall mindset of scarcity in how they approach all their (financial) issues, while others have more of an abundance mindset. And the differences in how they plan and prepare for challenges are profound.

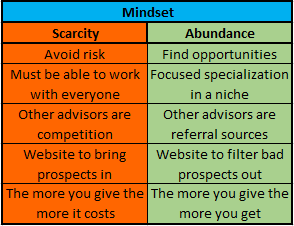

For instance, the scarcity mindset that views money as an extremely limited resource may obsess about hoarding and protecting it, to the extent that the client may be altogether fearful of spending and enjoying it at all. How many of us have seen clients who are genuinely wealthy yet terrified of running out of money, and afraid to use any of their money for their own enjoyment?

An extreme scarcity mindset can lead to severe risk-averse behaviors, often to the point of long-term self harm. For instance, a scarcity view around money might lead a younger person to just save cash flow instead of investing it into themselves and their career, ultimately hindering income growth and making future money more scarce (despite the savings itself). Similarly, a “Money is so scarce I can’t risk much/any of it in the markets and have to keep most/all of it in cash” attitude may drive portfolios to be so conservative that the long-term damaging effects of inflation really do make money more scarce in the future! Sadly, most of us have seen these kinds of problematic and even self-destructive scarcity-minded issues arise with clients.

By contrast, the clients with an abundance mindset are remarkably different. They may be more inclined towards taking risks – recognizing that money lost is something that can be made back again in a world of abundance – but the distinction is more than just about risk tolerance. The abundance mindset doesn’t necessarily ignore risks, it’s simply about seeing the opportunities that lie beyond them, and perhaps a recognition that the world is a dynamic place that will always be changing and presenting new opportunities along the way.

Notably, the abundance versus scarcity mindset isn’t just about clients, though. It’s an issue for all of us – including as advisors – and in practice, I find it affects many of us in how we run our own advisory businesses and conduct our affairs, as much as in how we actually craft advice to clients.

Abundance vs Scarcity in Industry Volunteerism

An excellent example of abundance versus scarcity mind amongst advisors is in our behaviors in getting involved with and volunteering for membership associations like FPA and NAPFA. For some, it’s an opportunity to get involved, to give back, or to network and build connections. For others, they ask “why would I want to do volunteer work with my competition?”

While I have written in the past that financial planners are experiencing a crisis of differentiation – we say we’re experienced credentialed advisors who provide customized individualized financial plans for our clients and deliver great service, but it’s not a differentiator when we all say it – the problem exists only because we have brought it upon ourselves by remaining an emerging profession of generalists and not moving towards specializations and niches (yet).

In truth, we are not literally in direct competition with each other much at all, for the simple reason that there are about 316 million people in the US, comprising about 115 million households, of which nearly 1/3rd have more than $100,000 in net worth (not including their primary residence), over 15 million have at least $500k, and almost 10 million of them are millionaires. Which means in a world where there are “only” about 70,000 CFP certificants to do financial planning, there are 142 millionaires and over 500 mass affluent households per advisors, while most of us make our living with no more than about 75-125 active client households (and it’s not clear our brains can even handle more than about 150 total relationships).

In other words, clients may feel “scarce” because so many of us are going after the same “target market” (if we want to call “people who can afford my services” a target market, which it’s really not!) with the same undifferentiated solution, but the scarcity is caused by how we have narrowed our target clientele and the way (or lack thereof) we differentiate what we do! In reality, the number of potential clients is still quite abundant, and for those who have a clearly defined niche – and work and volunteer with other advisors who have different niches – the opportunity of networking with advisors is that it is not a competitive environment but actually an opportunity to generate cross-referrals! For example, planners with Garrett Planning Network (hourly planning) and XY Planning Network (planning for Gen X and Gen Y clients) often gather referrals by establishing relationships with other advisors who have a different target clientele!

Simply put, while the scarcity mindset would imply there’s no reason for industry volunteerism with “the competition”, an abundance mindset reveals that in the end there are still more than enough prospective clients to go around for all of us… at least once we focus our businesses and choose a (more) clearly defined target clientele!

Abundance vs Scarcity in Marketing

The abundance versus scarcity mindset is also clearly illustrated in the way that most financial advisors market themselves.

For example, I find that it’s still incredibly rare for advisors to share the most basic of consumer information on their websites and marketing materials, like how much their services cost and what their minimums are. The reasoning usually goes something like this: “I prefer to have a conversation with prospective clients about the value that I provide and the associated cost, to be certain they evaluate my services appropriately. In addition, this allows me the opportunity to evaluate whether the prospective client might be a good long-term fit, even though he/she doesn’t meet my official minimums [e.g., someone with less in assets but a high income making large annual contributions to savings]”. The underlying message of the approach: potential clients are so scarce, I believe it’s a productive use of my time to meet with every single person who could possibly be interested in talking to me, just to have the opportunity to hopefully convince one or two to become clients.

By contrast, marketing with an abundance mindset is about putting as much information on your website as possible, including your pricing/fee schedule and also your asset/client minimums, and letting the website be the screening process that ensures the only prospective clients you sit down are those who have already qualified themselves as people who are willing to pay your fees and meet your minimums (as if all that is clearly stated on your website, the only people who should contact you and those who are already comfortable with those amounts/limits/thresholds!).

Accordingly, with an abundance mindset, the goal of marketing as an advisor is to get your valuable information out to as many people as possible, recognizing that if even just a few need some additional help to implement the advice you will have as many clients as you can handle. At that point, your website is not a marketing brochure to tell people what you do, it’s actually a filter to limit who contacts you to only those who really want to do business with you (saving you time from go-nowhere prospect meetings along the way!).

In the end, our view about the world and its opportunities – or perceived lack thereof – can significantly and dramatically shape our actions. And as you might have guessed from the tone of this article, my own view is certainly one of abundance over scarcity; it shapes everything from the amount of time I put into this blog and sharing content with all of you my readers, to the time I volunteer with the membership associations, to how the websites of my various businesses are structured in a world where my own personal greatest challenge has been learning how to filter and say “no” to the sheer number of opportunities that arise.

So whether it’s going through the planning process with clients who are limiting their own success with a scarcity mindset, or taking a fresh look at your business and evaluating whether a scarcity mindset has become your own self-limiting factor, hopefully the idea of an abundance mindset may help to look at the world and what you do in it a little differently!

So what do you think? Do you approach your advisory firm with a mindset of abundance, or a mindset of scarcity? Has it impacted the decisions that you make in how you operate and try to grow your business? Does it impact the advice you give to your clients? Do you see this mindset distinction present in the decisions that your clients make for themselves?

Right you are Mr Kitces. AS an investor I acknowledge that I have a scarcity mindset which I have to consciously fight. Very well stated. I also call the scarcity mindset the Tom Joad wagon.

It’s an ironic challenge in many ways. I regularly see situations where the scarcity mindset that helped a client to accumulate their assets via aggressive saving now also makes it very difficult for them to enjoy it… because unfortunately if the mindset is focused around scarcity, there’s always ‘something’ to fear even when resources have built significantly. Sometimes we are our own worst enemies?

I’m continually amazed how often I run into advisors who are afraid the share their “secret” formula for success. The pie is so large, and information so readily available that constant collaboration is going to make us all better. I regularly meet with adivsors I respect in the area to share ideas, best practices, what’s working, and what’s not. The chance of running into the same clients, even for those who are geographically close (which is becoming less and less important), is small.

So true, Dan. I have helped out several local advisors with advice and referrals and they always seem amazed that another advisor is willing to help them.

Love this post, Michael! I would say that the idea of the abundance mentality also increases the value of mastermind and study groups as well. Sharing ideas and being a referral source for each other can be extremely powerful in my experience. Advisors continue to be surprised by how much I will tell them about my business.

I never thought about the scarcity mentality or abundance mentality in terms of clients. Great point!

100% agree with you, Sophia! Michael does a great job in this post and as I read it I immediately though of you, Alan, and Mary Beth (along with many others and the XY Planning Network members) as those who are perfect examples of working with an abundance mentality and how doing so can be rewarding and fulfilling.

The generous sharing of more experienced advisors (who also referred business to me if it didn’t fit their practice) was a HUGE part of my early positive experience in building my practice. Generosity may require some courage, but it’s worth it!

When I started my practice 10 years ago I used 60million/50 (ratio of baby boomers to clients needed) Now that’s a business plan. As Nick Murray says ” For planners who are really good at what they do- measured by the only people who count; their clients – all times and all market conditions are perfect for their business. There are at all times plenty of people who have needs that have to be addressed, without depending on external conditions to bring them to your door.

Very well put and quite timely, as I just received a referral today from a CFP. They felt I was a better fit given my niche. I have also referred several prospects to other advisors, and never felt doing so would compromise my existing and/or growing business. I find that by approaching the world and business with an abundance mentality, it manifests and will eventually find its way back to you. The same is true for volunteering and pro bono work. As Sophia stated, you also create a lot of great contacts and mastermind opportunities.

So true, Michael! Thanks for sharing these thoughts.

So true. I was just talking with someone who gave me a list of reasons why they weren’t able to grow their client base over the last few years. Robos, not enough people in their area who have saved money, people doing their own investing, not enough money to pay for a high-end website, etc. Scarcity mode at it’s core. In that mode we’re all apt to attract clients in that mode, too.

What if we all came from a point where there is more than enough business for everyone to be had? And that finding the type of clients we were passionate about working with would bring in the money, too?

Right on with the transparency in prices. I’ve been told so many times to take my fees off my site. “It’s just not done”, “you’ll lose business before you find it”, “people need to understand the value you provide before talking with you”. All can be true and I’m sure they are at times. But heck, I get fewer looky-lou’s now than when I didn’t have prices.

If people are asking for your fees, they belong on your website. I recommend that my clients consider doing it, too. Not one is willing to take the risk (although they have created pricing sheets to provide people they’ve spoken to). Little steps to bigger steps.

When if find that scarcity mindset sets in with my clients, I have to go back and look at my mindset. I did that five years ago when I realized that I should be paid (handsomely) for my workshops and I stopped working for free. I value practice management and see many who don’t, not getting where they want to go. That value is translated into a price.

Barbara Stanny, T. Harv Ecker as well as others have written very good books on Money Mindsets. In fact, The Millionaire Mind (affiliate link: http://www.ElevatingYourBusiness.com/b/peak.html ) is an excellent program I attended (and recommend clients and friends attend) to see where scarcity mode (and other negative money mindsets) that may still creep in from time to time.

Michael, when I made the shift from a scarcity mindset to an abundant mindset is when I became successful as an entrepreneur. It’s ‘cosmic’ you should mention this topic as I just spoke on it at the Garrett Planning Retreat. I talked about when I used to let my anxiety drive my day when I first started my planning practice. The phone didn’t always ring or the prospect I was sure would sign on, did not. Viewed through the scarcity glasses, I’d feel limited, fearful, suffocated. The day I decided that I’d approach my work (and my life) with abundance, I tapped into all my strength and skill and stand in confidence as a result. It is an amazing shift — one that takes courage for many because scarcity can seem much easier. Scarcity is reinforced by the media and the messages we hear each day and in the fears of clients. Expanding your mind to possibility open up many options, which can quickly revert to “overwhelming” without practice.

The shift to abundance thinking made all the difference in how I approach each day. “What can I create today” and “What’s possible today” not only guide my own actions for the day, week, and year, and how I develop my marketing training, but also how I interact with my team members, contractors, clients, and partners. Collaboration & new approaches take all to the next level!

Abundance is a fundamental tenet of content marketing today — give give give and give some more. You will receive in return. And it will be abundant in more ways than just revenue. The fulfillment that comes from saying “how can we work together” with a competitor or “what do you want to make possible?” with a client makes a shift so impactful that when you practice and exercise these muscles each day, you’ll be amazed what shows up for you in your work.

And, yes, on a bad day I fall back into scarcity thinking. And I hate it. It sucks the life out of you. When I get stuck, I call a fellow entrepreneur — I make sure it’s one who ‘gets’ the abundance vs. scarcity distinction. I blame my “scarcity scars” and, after a quick dialogue, shift back to the abundant mindset. I am thankful each and every time.

I could go on and on on this topic…thanks for opening up this door!! I cannot stress enough what a difference the shift makes on your ability to run a successful business and enjoy it much much more!

(plus, the good news is it spills over into your Life too!)

~Kristin

Another “home run” Michael. This article is so relevant to my clients and me (especially me). Thanks!

Great article Michael. I think the journey from scarcity — or at least lack of abundance —

to abundance is one that many of us have traveled somewhat in parallel as our professional

success climbs. I had a business coach early on that told me, “Fake it

til’ you make it.” I wasn’t a good actor then or now, but somewhat quickly my confidence and abundance mindset increased.

An interesting question to me as a young parent like yourself is how to instill that abundance

mindset without crossing over into the overconfidence zone.

Micheal – you killed it with this one. Succinctly breaking down what I have been trying to get my head around for the last several years. Has broad applications in our daily lives and the lives of our clients as well. Love the mindset chart…thanks!

Also, my apologies for my “scarcity” of spelling skills and the auto-correct – thank goodness for math!

Yikes, this thread struck a nerve! Totally agree. I volunteer and give back thru ACPlanners on a few committees and mentorning/coaching some newer members. I joined an accountability/pracitice management group a year ago. Monthly group call and twice monthly buddy calls. I have learned so much about this business by gleaning knowledge and experiences from colleagues about their practices thru these relationships.

Michael, interesting piece. There is an obvious issue when there is a difference between the mindset of the advisor and the mindset of the client – it does not matter which way around it is. If there is a difference there will be conflict. It comes back to client selection. Client selection is not just about identifying your target market.

For example, if an advisor determined that medical consultants were to be their target market, they would then need to dig deeper and understand what are the characteristics of those consultants that will make them their ideal clients. Then they must decide if their ideal client has an abundant or scarcity mindset – that forms part of the criteria for determining the fit between the two.

The essence of “investing” in the capital markets in a capitalist system is abundance over scarcity. That there will be growth (of course unbridled and unregulated growth have their own problems) and on account of that growth there will be a positive return to capital over time. Nick Murray points this out in a rather “schmaltzy” way. Bill Bernstein has written about this in a historical and mathematical way. And John Bogle has written about this in a folksy way. I don’t see how one can be an “investment” advisor without being optimistic about the future.