Executive Summary

Historically, the active vs passive divide has been primarily a question of how to invest within an asset class. Is it better to utilize an active manager who will try to outperform an index (at the risk of underperforming it), or simply buy the index itself in the form of a fund that at worst should simply “underperform” by the margin of a very small fee. Either way, most investment managers will still implement a remarkably similar asset allocation – regardless of the active vs passive divide – based on the principles of Modern Portfolio Theory.

Yet a deeper look at MPT reveals that in reality, it may have never been intended as a model for strategic asset allocation in the first place. Markowitz himself advocated in his original research that MPT should not be implemented simply by looking at long-term historical averages, but instead by adjusting the statistical analysis of risk and return based on nuances not taken into account by formal computations alone.

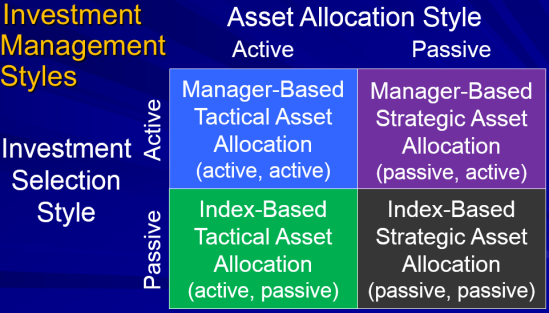

The end point of this dynamic is that the active vs passive divide of investment management is actually split on two different dimensions: to be active or passive within asset classes, and whether to be strategic or tactical amongst them, leading to four quadrants of investment management styles depending on which combination(s) the advisor chooses.

Ultimately, this means that going forward investment managers must be more cognizant to frame their approach based on both dimensions, and recognize clearly where they can – or cannot – add value for clients. So what’s your investment management style? Tactical active, Strategic active, Tactical passive, or Strategic passive?

Classic Portfolio Construction - The Active Vs Passive Divide

The standard approach to portfolio construction starts with determining a client’s goals and risk tolerance, and then finds a diversified asset allocation with an expected return and acceptable risk commensurate with the goals and tolerance. The end point is typically an Investment Policy Statement (IPS) that stipulates how much will be invested in each asset class, and then it’s left up to the advisor to determine how to actually implement each asset class – some may choose to fill in the asset class buckets with index funds, while others may prefer to choose active managers, but clients with similar goals and risk all end out with a similar baseline asset allocation.

So how is the asset allocation itself determined? In practice, most advisors use Modern Portfolio Theory – if not literally with portfolio optimizers, at least conceptually, with a goal of holding various asset classes that have appealing returns, reasonable risk, and low correlations to each other. These three factors – expected return, volatility, and correlations (or a full covariance matrix) are the building blocks of MPT.

Yet while the purpose of MPT is to determine what an optimal “efficient” allocation should be based on the various return/volatility/correlation inputs, as a model it simply shows the investor what to do once the inputs are provided. Coming up with those inputs in the first place is in the hands of the user.

While the typical approach used by advisors today is to rely on long-term historical returns, in his original paper on “Portfolio Selection” where the MPT framework was first published, Harry Markowitz provided his own guidance about how he thought his model (which he called the Expected Return-Volatility Rule or “E-V rule” for short) should be used:

To use the E-V rule in the selection of securities we must have procedures for finding reasonable [estimates of expected return and volatility]. These procedures, I believe, should combine statistical techniques and the judgment of practical men. My feeling is that the statistical computations should be used to arrive at a tentative set of [mean and volatility]. Judgment should then be used in increasing or decreasing some of these [mean and volatility inputs] on the basis of factors or nuances not taken into account by the formal computations…”

“…One suggestion as to tentative [mean and volatility] is to use the observed [mean and volatility] for some period of the past. I believe that better methods, which take into account more information, can be found.”

In other words, in his own paper, Markowitz’s own guidance was that MPT should not be implemented used historical returns and standard deviation (“the observed [mean and volatility] for some period of the past”). Instead, Markowitz envisioned that MPT would be implemented with a combination of statistical techniques and judgment to taken into account nuances of the market not conveyed by statistics alone!

The New Dimension Of Active: Tactical Amongst Asset Classes

The idea of using inputs to MPT beyond just long-term historical averages leads to a more forward-looking approach that takes into account changing market dynamics over time.

For instance, in an environment where intermediate bonds yield 2% instead of 8%, it’s not difficult to see that their expected return will likely differ as well (both due to the difference in yields themselves, and the impact on bond prices if those yields begin to revert towards the long-term average around 5%). Yet using an MPT framework, “optimizing” for low-yield bonds with high downside risk, or higher-return bonds with upside opportunity, will lead to significantly different optimal portfolios.

Similarly, stocks with high P/E ratios (and a low earnings yield) also have very different risk/return characteristics than “cheap” low P/E stocks with strong earnings (at least for the market in the aggregate; individual stocks may vary). This, again, leads to a similar result: favorably valued stocks with a good “margin of safety” will end out with a different allocation on the efficient frontier than buying markets at nosebleed valuations and an elevated risk they will revert to the long-term average.

Which means ultimately, as the risk/return characteristics of all the asset classes change, so too do the inputs to MPT, which impacts the efficient frontier, and leads to a startling conclusion: proper implementation of MPT actually means the optimal asset allocation itself should change over time! Portfolio managers monitoring dynamic markets may actually be compelled to make tactical shifts amongst asset classes just to maintain a constant risk/return exposure in the first place! By contrast, choosing a static, “strategic” asset allocation is akin to saying “perhaps the best estimate of future risk/return/correlations really is the long-term historical averages for those parameters” (Markowitz’ admonition notwithstanding).

Active vs Passive Investment Selection and Strategic vs Tactical Asset Allocation

The impact of dynamic inputs to MPT leads to what are ultimately two different levels at which a portfolio can be managed actively: changes amongst the asset classes, and changes within the asset classes.

Changes within asset classes represents the classic “passive vs active” divide: once there is a set asset allocation, do you want to implement those asset classes using active managers who try to beat the asset class benchmark, or is it preferable to simply own index funds that may not beat the asset class benchmark but at least will do a good job representing its place in the portfolio and “underperform” by no more than a modest indexing fee?

By contrast, changes amongst asset classes represent a new “to be active or not” decision –whether to make active changes to the asset allocation itself based on changing inputs to MPT (a tactical approach), or rely on a static asset allocation (a strategic asset allocation). The difference is whether or not the asset allocation itself it changes over time.

At the intersection of these two dimensions, then, is a combination of four possible “investment management” styles, depending on whether the manager is tactical or strategic in selecting asset classes, and passive or active in implementing those asset classes.

In the “traditional” world of portfolio construction, all investment management decisions remained on the right side of the chart. Asset allocation was presumed to be strategic for all, and the only decision was whether to implement that asset allocation with index funds (the passive approach) or to try to identify stock-pickers/mutual funds capable of outperforming those indices (the active approach).

On the left side of the chart, though, is the new rise of “tactical” asset allocation. In the lower left is the index-based tactical approach. If you took a snapshot of the portfolio, you would see a long list of index funds; but if you took another look at the portfolio in a year, you would different allocations to those index funds. The active implementation is not in the use of active managers in lieu of index funds, but the active management of the index fund allocations themselves! Notably, this form of “active implementation of index funds” may go a long way to explaining the meteoric rise of ETF funds, which may have less to do with financial advisors becoming more passive, than simply shifting to try to provide active management value in the lower left rather than the upper right! (For instance, Morningstar estimates ETF-managed portfolio strategies now have over $100B of AUM and grew 40% in 2013!)

In the upper left are the “double active” portfolio managers – those who actively shift amongst the asset classes, and also seek out active managers within them. Thus, for instance, an actively managed mutual fund might be sold either because the manager themselves is no longer providing value, or because the manager is doing a great job but in an asset class overall that has a poor outlook (e.g., you could have picked a brilliant tech fund manager in 2000, but the real opportunity was not picking the right tech manager but knowing when not to own tech in the first place!).

Where Do You Add Value?

The four quadrant “portfolio manager style” boxes lead to a number of different ways that advisors may choose to add value.

The “anchor” is the lower right: the low-cost passive, strategic portfolio. Arguably, this portfolio is now becoming so “easy” to implement that it is being commoditized altogether; any number of robo-advisors are now available to fill this box at a cost around 25bps.

From there, advisors who choose to add value around the investment portfolio have two choices: go left, or go up translates to either adding value by providing advice about how to allocate tactically amongst the asset classes, or provide value in the selection of active managers who can excel within those asset classes (or do that level of active management hands-on themselves).

Making tactical decisions amongst asset classes may be driven by absolute or relative valuation measures, top-down macroeconomics, or outright forecasting of exogenous events. Making active decisions within asset classes entails a skillset in security analysis and bottom-up analysis, considering costs and fees, liquidity and trading capabilities, etc.

Investment managers may ultimately choose a blend of how they wish to provide blend, and how they wish to do it. They might make tactical decisions internally, but implement with actively managed funds for the security selection. They might be a firm of bottom-up stock-pickers, but draw on outside research for macroeconomic input amongst the asset classes. They might focus on being in the “manager search and selection” business and identify managers capable of making the amongst or within asset class decisions.

Notably, all of this is still separate from the raw benefits of effective implementation, which (in the case of individuals at least) may still include components of tax-loss harvesting, rebalancing, and asset location, which can be applied across any of the four portfolio manager style boxes.

But the bottom line is simply this: as investment management continues to evolve (perhaps back to how Markowitz first envisioned it!), the decision about “active vs passive” is no longer just about index vs actively-managed mutual funds to invest within each asset class, but also about the decisions amongst the asset classes as well. Investment managers would be well served to consider which aspects of active – within and/or amongst – they wish to pursue (or not!), and ensure they know whether/where they intend to add value (and whether they have the resources to do so). This challenge – to clearly show where value is added – will only become increasingly pressured in the future, as the robo-advisors increasingly commoditize the lower right corner of the portfolio manager style boxes, forcing investment managers into one active dimension or the other, or in another direction altogether (such as financial planning and wealth management!) to increase their value-add.

This is a great start towards more clarity and texture for this concept. It’s not simply a “passive – good, active – bad” discussion. I tend to look for active managers for certain asset classes who help to manage downside risk; I do NOT expect index-beating performance. My value to clients consists of good financial planning FIRST (so the portfolio can be designed in context) and then, helping them to avoid negative investor alpha (by sticking to their investment policy and updating their plan every year).

Great article, Michael! Markowitz’s admonition for implementing MPT has been broadly missed; or maybe conveniently overlooked as the lower-right is easy to do and then move on to the next new account.

Very good framework, and thanks for the reminder that Markowitz’s theory is based on future expectations, not blindly crunching past results.

However, predicting the future is a bit of a problem — even P/E ratios have no predictive value. Dimson, Marsh and Staunton of the London Business School (see Credit Suisse Global Investment Returns Yearbook 2013) simulated timing entries and exits from the market based on CAPE, and found that this method resulted in worse performance than staying in the market at all times (the robo-advisor bottom-right corner passive-passive technique). Their conclusion is poignant: “sadly, we learn far less from valuation ratios about how to make profits in the future than about how we might have profited in the past.”

As one of my favorite reads each year, I found that piece by Dimson et al problematic.

1. We don’t really know how they constructed their out of sample model. I suspect I would find it wanting if for no other reason that an out of sample model constructed in 1920 would have lacked a lot of information from market history that allows us to make informed choices today (even if the advantages of knowing history are ignored by most.)

2. Their data is more kind to using valuation in the US. International comparisons are useful, but the underlying fundamentals upon which investors make their models in their experiment are far more stable in the US relative to many of the countries that the strategy seemed to not work in, and especially when you factor in how small many of those markets were in the past and how dominated by just a handful of companies (often only one or two companies might account for over 50% of the market cap in some markets.) I don’t think it is an accident that countries with a more stable history show valuation as more useful in general. I suspect as more countries “develop” that we see using valuation become more useful in more and more countries.

3. On the surface it contradicts their encouraging us to buy out of favor assets and move away from expensive assets in the same article! However, I don’t think it really does contradict it even if we take on faith their results because…

4. The results assume 100% t-bills or 100% stocks as the choice. Obviously not an ideal choice. How about moving from expensive US Large Cap Growth in the run up to 2000 to less expensive high return options in international markets, Emerging markets, REIT’s, TIPS, other fixed income, and in the US small cap value and Value stocks in general. That worked great, whereas just going to T-Bills in 97 or 98 even in that extreme case left you a lot of catching up to do even with the crash. Of course now REIT’s are expensive and small and value in the US is startlingly more expensive than in the years around 2000, so where you go now as opposed to then is a huge question.

5. Finally, they ignore telling us about how it deals with risk. Even if returns were on average about the same (putting aside my suspicions that their test may have some issues, especially given other research I have seen) what about risk? Especially for those in or near retirement reducing sequence of returns risk could be extremely important. I suspect that the skew of the returns in their test was huge!

Excellent post! A tactical asset allocation (whether indexed-based or manager-based) is essential to improve risk adjusted rates of return. Just the fact bond rates are at historical lows makes historical averages moot! Adjustments must be made to asset allocation or investors will be taking unnecessary risk.

Exactly!

No small surprise that Markowitz does so much work with Research Affiliates which specializes in Tactical Asset Allocation.

Which brings up a host of questions for an efficient management of a planning firm and the industry that supports it. Most of the tools that are readily available for implementing financial and investment advice are wedded to the strategic asset class model of investing. While tactical decisions based on macroeconomic factors writ large are quite difficult to model in a way that can be easily packaged for the typical planner, it would seem to me that it would be very beneficial to many if tools such as Money Guide Pro and commonly available optimizers were able to handle and even provide projections based at least on valuation for those who wish to do so.

It would also be nice if they had an easy way to model in the fact that the allocation will change over time (and thus current projections would not determine long term returns!) While there are workarounds for such issues, it is not easy.

This issue was dealt with brilliantly by Ben Inker of GMO recently when it comes to retirement and I was curious if you had read it, “Investing for Retirement: The Defined Contribution Challenge.”

My first question when I read it was “Who is going to help the typical practitioner implement such an approach?” There are no tools which tackle the problem in the way they look at it. In my own practice I try (it is always nice to see a problem approached in a way that you see it) but it is hardly an easy process which typical planners can implement who do not see themselves as first and foremost investment experts.

Whatever the merits of some amount of dynamism in a portfolio, it is a problem to implement that it would be nice for some group to discuss and help planners put together a reasonable approach to doing it without straining their resources. “Outsource it” then some might say. Certainly in estimating returns that could be done easily (Heck, for many asset classes GMO provides them for free.) How about a TAMP? Putting aside the extra layer of expense in TAMPing it out as opposed to implementing such an approach in house with some simple modeling tools, can we find one that implements the philosophy we are comfortable with? I find it hard.

Ultimately no forecasts we model will be right, but it would be nice if we had readily available models and tools with at least reasonable forward looking returns either built in or easily entered both for investment purposes and planning purposes.

I get the logic behind tactical allocation, particularly your point here about the actual risk/return characteristics of a static allocation changing over time. But is there any evidence that advisors can successfully and consistently get the tactical changes right? If there is, I’d love to hear more about that research. But otherwise, it’s hard for me to get past the fact that this feels like just another name for market timing, which always sounds great in theory but is incredibly difficult to do with any consistency.

You are asking the right question about whether it can be executed, and given the tools most advisors have at their disposal I would say it is problematic at best.

On whether advisors can consistently get the tactical changes right, of course not. If you mean consistently aligning themselves in the most profitable way relative to the markets, that is an impossible task. However, one could turn that question around about not doing it. If we maintain a static asset allocation can we consistently produce the expected returns that our present tools imply? Of course not. Markets are not consistent.

The real question is, will an intelligent approach to changing the asset allocation improve results in terms of risk and return? I think it can, but as stated, we don’t have tools readily available to do so easily ourselves for the most part and the costs of doing so if fully outsourced are not all that attractive right now.

Finally, some tactical asset allocation strategies are about market timing, or some form of trend following. However, weighting assets away from expensive assets and toward cheaper assets is not market timing. It does not assume we know when things will happen, only that in general over time cheaper assets outperform more expensive assets.

There is much to be learned from the institutional market /Sovereign wealth funds when icome to portfolio construction, where more informed opinions are required. None of this is so complex it is beyond retail advisor, it just requires skill, experience and an understanding of the determinative value of tools and resources. It is never a check the box of things to do, it requires judgment.. The biggest institutional vendors of asset allocation resources have perpetuated the myth of plug and play with out crediting the skill required to actually add value. For example here in the US the major wirehouses only do capital market assumptions once a year which may result in precisely wrong strategies based on outdated information. That should not be the state of the industry–advisors should demand better and be prepared to manage complexity and pay for it.

SCW