Executive Summary

Fixed income investments are an important component in a portfolio because of their ability to cushion against equity market losses. However, when it comes to abundant returns, fixed income holdings have not had much luck during the low-interest-rate environment of the past few years. Accordingly, those seeking higher returns from their bond holdings have had to venture into less secure instruments, such as high-yield “junk” bonds and other alternative-fixed income holdings. Making matters worse, the recent spike in inflation means that many fixed income investments are earning a negative real yield. However, this is not bad news for all fixed income instruments, as this increase in inflation has made the rarely used Federal Series I Savings Bond (or, more simply, the “I Bond”) significantly more attractive for investors.

I Bonds are offered via the Treasury Department and are backed by the U.S. government. They can be purchased through the TreasuryDirect website, and such purchases are limited to $10,000 annually per person. What makes I Bonds unique is their interest structure, which consists of a combined “Fixed Rate” and “Inflation Rate” that, together, make a “Composite Rate” – the actual rate of interest that an I Bond will earn over a six-month period.

While the current Fixed Rate for newly purchased I Bonds is 0%, the Inflation Rate for I bonds purchased before May 1, 2022 is an annualized 7.12%, meaning the Composite Rate is also an annualized 7.12% (the highest rate of I Bonds since May 2000!) for the first six months that the I Bond is held (after which a new Composite Rate will be determined by any change to the Inflation rate). While I Bonds have a 30-year maturity, they can be redeemed after being held for at least 12 months. Investors who redeem I Bonds between 12 months and 5 years after issue will forfeit the last 3 months of interest, but I Bonds held for more than 5 years can be redeemed at their current value.

The $10,000 annual limit on I Bond purchases restricts their benefit for those with larger portfolios, but there are several ways investors could increase the amount purchased at the current (very favorable) Composite Rate. For example, because the annual limit is a calendar-year limit, individuals could purchase $10,000 worth of I Bonds before January 1, 2022, and then an additional $10,000 between January 1 and April 30, 2022. Which means a couple could purchase a combined $40,000 worth of I Bonds and receive the annualized 7.12% Composite Rate for the first six months the bond is held. In addition, I Bonds can also be purchased for children or by trusts and estates, which could further increase the amount purchased. Finally, paper I Bonds can be purchased using a tax refund up to a $5,000-per-return limit, which is in addition to the $10,000 annual limit on I Bonds purchased through the TreasuryDirect website.

Ultimately, the key point is that there is a limited amount of time for investors to purchase I Bonds at their very favorable Composite Rate of 7.12%, especially if they want to maximize the amount purchased for the 2021 and 2022 calendar years. In the current environment of low-interest rates and high inflation, I Bonds represent a potential opportunity for investors to increase the yield for a portion of their fixed income portfolio!

Although there has been a significant uptick in inflation recently, interest rates on most fixed income investments remain near historical lows. Despite those low rates, however, fixed income investments remain an important – and often an essential – component of many individuals’ portfolios.

For many investors, fixed income investments are viewed primarily as a safety net – a cushion against market losses. Unfortunately, though, with interest rates remaining so low for so long, many individuals have been forced to make a difficult choice: either continue to hold on to comparatively safe fixed income investments (e.g., CDs, checking accounts, savings accounts, money market funds, Treasury bills) and forgo any type of meaningful return, or venture into the less secure corners of the fixed income world (e.g., high-yield “junk” bonds, peer-to-peer lending, subordinated debt) in search of higher returns, but with greater risk to principal.

As fortune would have it, though, thanks to the recent spike in inflation (the likes of which we have not seen for decades) and a rarely used Federal bond, there may be a way for investors to have their cake and eat it, too… for at least a small portion of their portfolio.

That is to say, there is the potential to earn a relatively strong rate of return (at least when it comes to fixed income investments) while also enjoying a high degree of principal protection.

How? Meet the I Bond.

I Bond Basics

Series I Bonds are bonds offered via the U.S. Treasury Department and are backed by the full faith and credit of the U.S. government, which is essentially the gold standard of guarantees when it comes to fixed income investments. I Bonds are generally purchased through the Federal Government’s TreasuryDirect website (www.TreasuryDirect.gov), and such purchases are limited to $10,000 annually per person.

I Bonds have a 30-year maturity (which technically consists of an original 20-year maturity, plus a 10-year extended maturity), meaning they will earn interest for a period of up to 30 years. The interest can be reported annually, or interest can be deferred until the bond matures, is cashed in, or is reissued to another individual – whichever comes first.

The unique interest rate structure of I Bonds is what makes them so attractive right now. Notably, the interest rate of an I Bond is comprised of two components: the “Fixed Rate” and the “Inflation Rate”. These two components are added together to arrive at the “Composite Rate”, which is the actual rate of interest that an I Bond will earn over a six-month period.

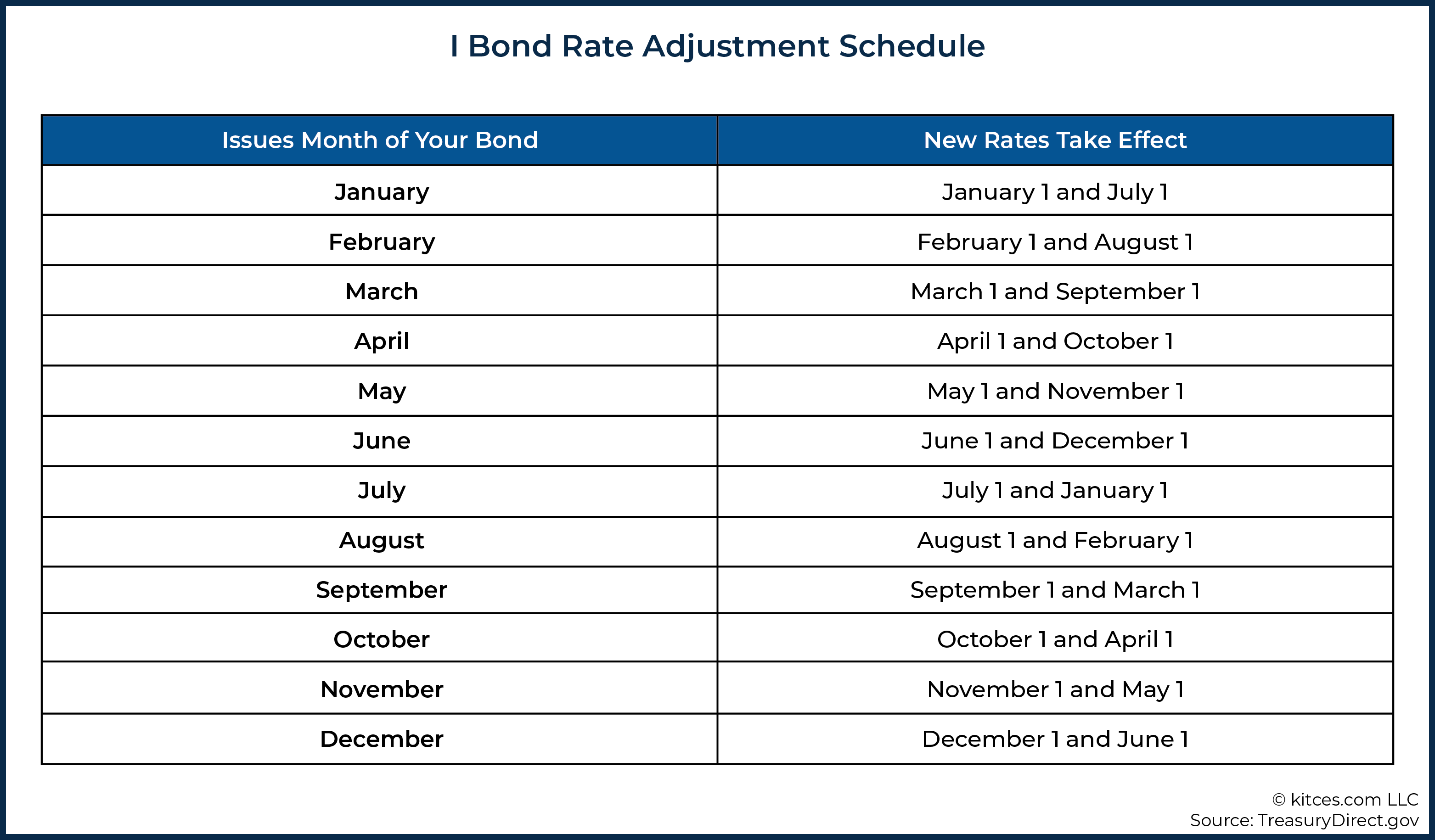

The I Bond Fixed Rate is established by the Treasury every six months (on the first business day of May and November) and applies to all I Bonds purchased during the following six months. And, as the name implies, the Fixed Rate of an I Bond remains constant throughout the life of the Bond.

Currently, the Fixed Rate of newly purchased I Bonds is 0%. While that’s probably not much less than what a lot of individuals are currently earning in their savings accounts, it’s not exactly an enticing proposition either. But remember, the Fixed Rate of an I Bond is only part of the total interest rate.

The second component of an I Bond’s Composite Rate is the Inflation Rate, which, unlike the Fixed Rate, varies throughout the life of an I Bond. It, too, is established by the Treasury Department every six months. The most recently announced Inflation Rate will be applied to an I Bond’s Composite Rate on the I Bond’s next six-month anniversary.

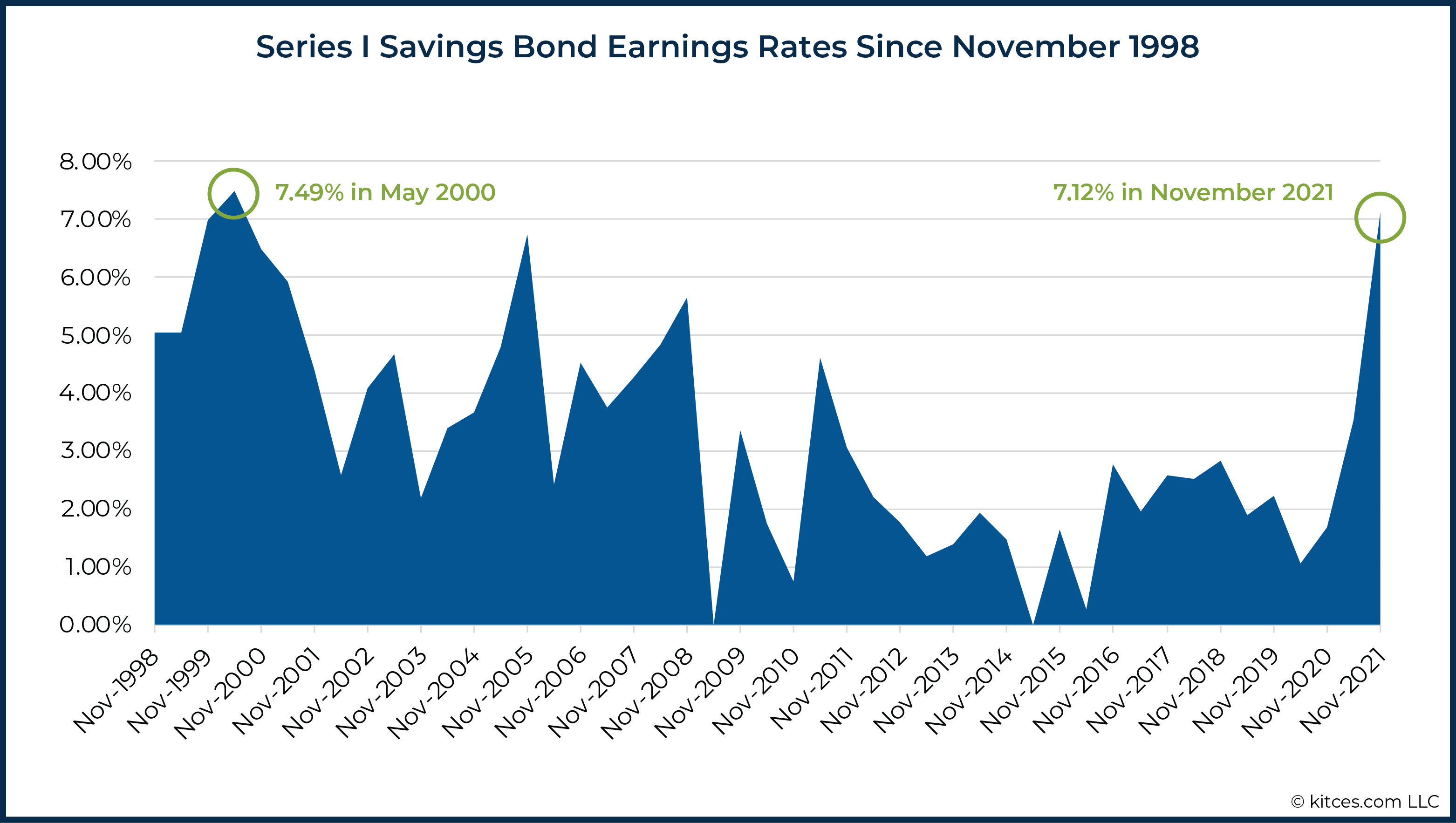

On November 1, 2021, the U.S. Treasury Department announced that the I Bond Inflation Rate for the next six months would be an annualized 7.12% (based on the change in the non-seasonally adjusted Consumer Price Index for all Urban Consumers (CPI-U) for all items). Thus, despite the fact that the Fixed Rate of a newly purchased I Bond is 0%, the Composite Rate of 7.12% is still extremely attractive in today’s environment. In fact, 7.12% rate is the highest rate at issue for I Bonds since May 2000!

The 7.12% (annualized) Composite Rate will apply for the first six months of all I Bonds purchased from November 2021 through April 2022. Upon the I Bond’s six-month anniversary, the new Composite Rate will be applied.

Example 1: Barry buys $10,000 of I Bonds on December 1, 2021. The Composite Rate for his bond is based on the current Fixed Rate of 0% and the adjustable Inflation Rate of 7.12% announced on November 1, 2021.

Thus, from December 1, 2021, through May 31, 2022, Barry’s I Bond will earn an annualized Composite Rate of 7.12%.

Beginning June 1, 2022, and through November 30, 2022, though, Barry’s I Bond will earn interest based on the Composite Rate that is announced on May 1, 2022.

Given the fact that the Fixed Rate for newly purchased I Bonds is 0%, the Composite Rate of I Bonds purchased today will generally equal the Inflation Rate. Why “generally” and not “always”?

Simple. The value of an I Bond – its principal plus any interest accrued to date – cannot go down. More specifically, while the Inflation Rate component of an I Bond can be negative (indicating a deflationary environment), the Composite Rate cannot be below 0%.

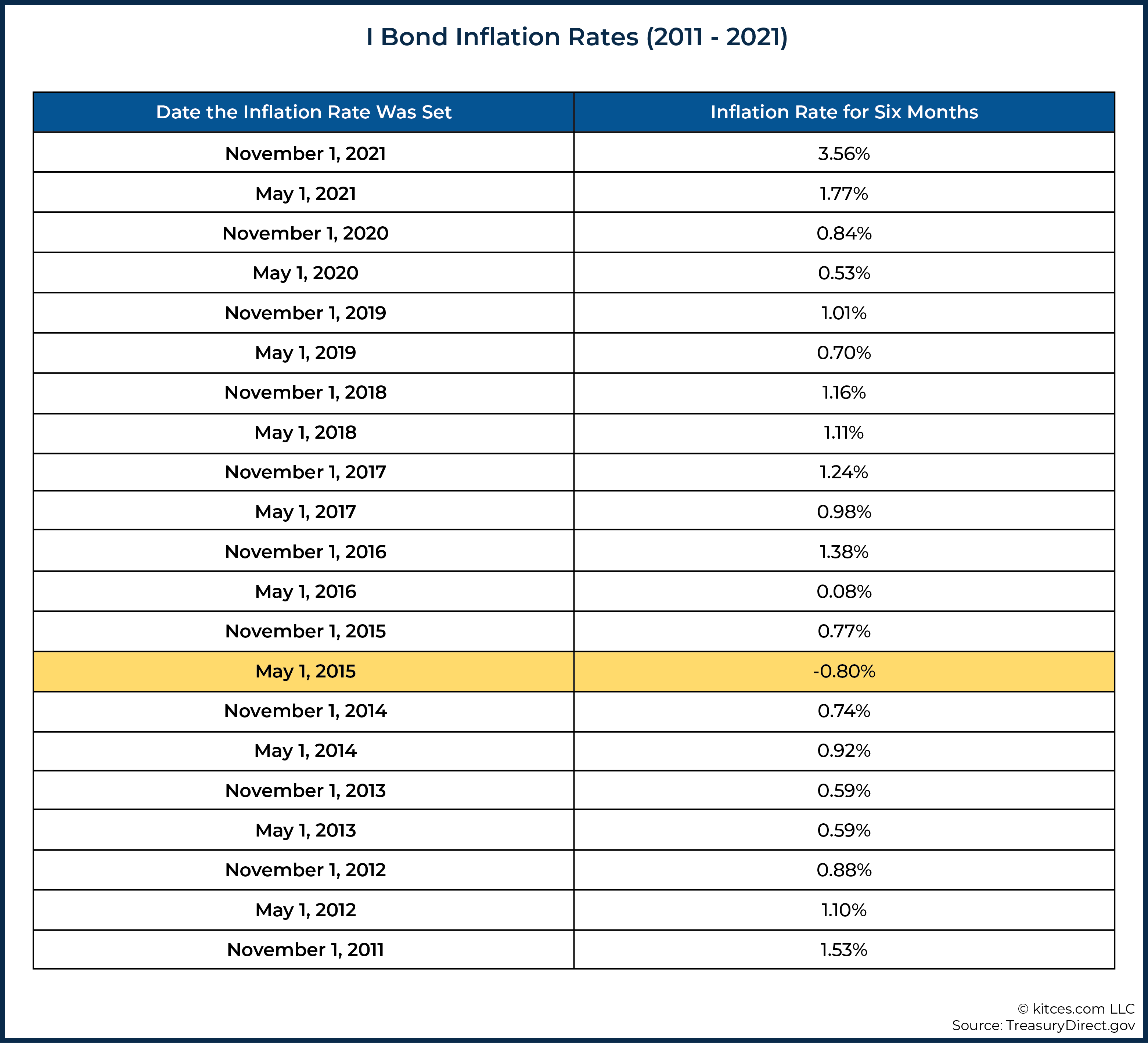

So, as long as the Inflation Rate of an I Bond purchased today is 0% or higher, the Inflation Rate and the Composite Rate will equal one another. However, in the event that the Inflation Rate dips into negative territory during the I Bond’s life (as would have been for an I Bond resetting its rate per the May 1, 2015 Inflation Rate, as indicated on the chart below), the Composite rate for the next six-month interest segment would equal 0%.

Comparing I Bond Yield To Other ‘Safe’ Fixed Income Investments

Just how good is a 7.12% interest rate? Ultimately, that depends on the relative safety of the investment, as well as what comparable investment options may be yielding at the same time.

In addition to I Bonds, investments such as savings accounts, money markets, CDs, and other U.S. government bonds are generally considered to be among the safest options for individuals looking to protect their principal. But while the safety of these investments is comparatively similar, the difference in the current yield of I Bonds compared to the rest of the options is night and day.

A cursory search on Bankrate.com, for instance, reveals that, as of December 2021, top money market rates are hovering around 0.6%, while the rate for a 5-year CD averages around a paltry 1%. And other U.S. Government bonds aren’t any better. For example, as of December 1, 2021, the yield on a 52-week Treasury Bill was 0.25%, while the Real Yield Curve for Treasury Inflation-Protected Securities (TIPS) with a maturity of 5 years was negative 1.55%!

When the I Bond’s current 7.12% yield is compared to these other, comparably ‘safe’ options, it becomes easy to see just how good of a deal I Bonds are in the current environment.

I Bond Redemption

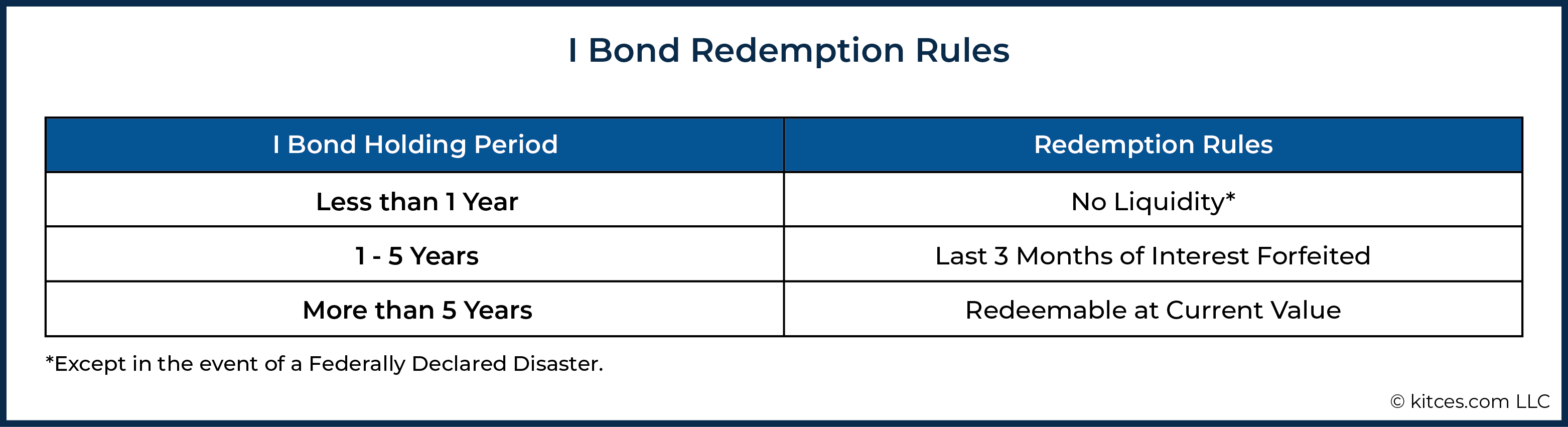

There’s always a catch, though, right? For I Bonds, the ‘catch’ for many people could be the limited liquidity and/or potential to forfeit up to three months of interest in the event that an I Bond is not held long enough.

More specifically, the ability to redeem an I Bond, and its impact on the bond’s value, can be summed up as illustrated in the following chart:

Given the fact that I Bonds are completely illiquid for the one-year period following their purchase (other than in the event of a Federally declared disaster), they would clearly not be an appropriate investment option for anyone who may need access to such funds during that time. For those who can afford to part with the money for at least one year, however, the liquidity restrictions should be of minimal concern.

In fact, even if an individual were certain that they would redeem a newly purchased I Bond right after the one-year mark, such a purchase may still be an attractive option. Notably, with the current Composite Rate at 7.12% (dramatically higher than comparably ‘safe’ alternatives), an I Bond purchased today would offer a pretty compelling rate of return, even in a worst-case scenario.

Example 2: Bobby is getting married in 12 months and will need $10,000 to pay for the wedding. He currently has the cash sitting in a ‘high-yield’ savings account, earning 1%. At the end of 12 months, when Bobby needs to withdraw his funds, the future value of his savings account would be $10,109.

Now, suppose that Bobby, with complete knowledge of the fact that he will not need the funds until 12 months from now, uses the $10,000 to purchase an equivalent amount of I Bonds with a current annual Composite Rate of 7.12%. Because this rate is locked in until the next rate adjustment in six months, Bobby can assume that his I Bonds will be worth $10,361 at that time.

While he cannot predict what the new adjusted Composite Rate will be when it is announced in 6 months, even in a worst-case scenario, where (some very unexpected) deflation would occur and the Composite Rate for the second six-month term of the bond would be adjusted from 7.12% to 0%, Bobby’s I Bonds would still have earned a rate of 3.56% over the year from the first six-month period, higher than the 1% rate of his “high-yield” savings account!

And if Bobby were to cash in his I Bonds right after the one-year mark as planned (in the worst-case scenario), he’d walk away with $10,356 – $10,109 = $247 more than if he had kept the cash in his high-yield savings account, as ‘losing’ the last three months of 0% interest (the penalty for selling his I Bonds before the five-year minimum holding period) would be a wash.

It’s hard to imagine that Bobby would be able to earn anywhere near a 3.56% rate of return on anything else over the coming year that would give him the same peace of mind, knowing the principal of his investment is protected to pay for his wedding.

Limits On I Bond Purchases

For individuals with significant wealth, one of the biggest problems with I Bonds is the limit on the total amount of such bonds that can be purchased during the year. More specifically, individuals can buy no more than $10,000 of I Bonds purchased in electronic form through the Federal Government’s TreasuryDirect website each year.

Further limiting such purchases is the fact that, unlike FDIC protection (which can be ‘expanded’ through the use of different registrations), the $10,000 limit per person on such I Bond purchases is a ‘hard’ limit. If the same people use different registrations (e.g., joint accounts, individual accounts), it does not increase the amount of I Bonds that they can collectively purchase.

Notably, when there is only one owner named on an I Bond, the bond is applied towards their $10,000 annual purchase limit. For I Bonds with two named owners, the purchase will be applied only towards the primary owner’s $10,000 annual purchase limit and will not be prorated between the two co-owners.

Example 3: Ian and Ida Ives are a married couple exploring fixed income investments. They have recently discovered I Bonds and, given their current interest rate and strong principal protection, they would like to invest as much as possible.

Ida creates a TreasuryDirect account and purchases $10,000 of I Bonds, naming Ian as her co-owner.

Ian, meanwhile, opens up his own TreasuryDirect account and purchases $10,000 of I Bonds in his name only.

Collectively, the Ives have purchased $20,000 of I Bonds in electronic form, which is the maximum amount that they can purchase for the year. Despite the fact that Ida did not purchase any I Bonds for herself alone, her $10,000 annual limit was used up via her purchase of the I Bonds on which she named Ian as the co-owner.

Additionally, because Ian was not the primary owner named on Ida’s purchase, the purchase of I Bonds he made in his name only does not result in exceeding his own $10,000 limit.

Strategies To Increase Total I Bond Purchases

For investors in a similar position to the Ives in the example above, one common question that arises is, “Well, is there anything that I can do to buy more of these I Bonds?” The answer, in many situations, is “Yes.” And while the expanded amount of I Bonds that can be purchased may still not be as much as an individual wants, in the ‘right’ situation, it can still meaningfully increase the total.

The $10,000 Limit Is A Calendar Year Limit

The $10,000 annual limit on I Bond purchases applies to calendar years, not fiscal years. Accordingly, individuals who have not purchased any I Bonds for 2021 can purchase $10,000 (per person) of I Bonds now and another $10,000 of I Bonds in January 2022 (or any other time during 2022).

With that in mind, it’s worth recalling that the current Composite Rate of 7.12% applies to the first six months of all I Bonds purchased before May 1, 2022.

Example 4: Recall Barry, from Example 1, who purchased $10,000 of I Bonds on December 1, 2021, with a Composite Interest Rate of 7.12% for the first six months.

Beginning January 1, 2022, Barry’s $10,000 annual limit is ‘re-filled,’ allowing him to purchase another $10,000 of I Bonds with the same 7.12% Composite Rate applicable to that tranche’s first six months.

The ability to ‘double up’ on a late-year/early-year purchase of I Bonds is nothing new, but as shown in the earlier graphic, the benefits of doing so haven’t been this significant for a long time.

Buy I Bonds For Other Family Members

As noted above, the annual $10,000 limit on I Bonds purchased via the TreasuryDirect website applies to each individual separately. That goes for adults, as well as for children, grandparents, and other relatives.

So, for instance, while a married couple with 3 young children can purchase ‘only’ (a total of) $20,000 of I Bonds for themselves each year, they could also purchase an additional $10,000 × 3 = $30,000 of I Bonds for their children.

Buy I Bonds For Other Entities

Although it may seem a bit odd to some, entities such as trusts and estates (as well as corporations and partnerships) can purchase I Bonds as well. The $10,000 limit on purchasing electronic I Bonds via the TreasuryDirect website applies to each entity separately, even if the beneficial owner is the same.

Example 5: Recall Barry, from Examples 1 and 4 above, who purchased $10,000 of I Bonds on December 1, 2021, and plans to purchase another $10,000 of electronic I Bonds on January 1, 2022. However, he is looking for a way to invest even more in I Bonds.

Barry happens to be the 100% owner of an S corporation. Additionally, he has established a trust of which he is the sole beneficiary.

While the $10,000 annual limit on electronic I Bonds purchases would prevent him from exceeding that amount as an individual, he could purchase an additional $10,000 of I Bonds in the name of his S corporation, as well as an additional $10,000 of I Bonds via his trust before the end of the year.

And, of course, in 2022, he’d be able to purchase another $10,000 of I Bonds in each of those entities.

Furthermore, while corporations, partnerships, and other business entities can only purchase I Bonds in electronic form, (many) trusts and estates entitled to a Federal income tax refund can use the refund to purchase an additional $5,000 in paper I Bonds annually.

Use Tax Refunds To Purchase Additional Paper I Bonds

The $10,000 limit on annual I Bond purchases per person, as described above, only applies to I Bonds purchased in electronic form. But there’s another way to purchase I Bonds!

More specifically, individuals can direct up to $5,000 of their income tax refund towards the purchase of paper (yes… paper) I Bonds. To do so, individuals must file Form 8888, Allocation of Refund (Including Savings Bond Purchases), and complete Part II of the form, U.S. Series I Savings Bond Purchases.

Notably, the $5,000 limit is a per-return limit. Most married couples file jointly, and so combined with the 2 x $10,000 = $20,000 of electronic I Bonds that they can purchase directly via the TreasuryDirect website, their combined maximum annual I Bond purchase limit would be increased by $5,000.

In the event, however, that a married couple files separate returns, they can each file Form 8888 with their respective return and request that (up to) $5,000 of their refunds be allocated towards the purchase of paper I Bonds.

For such married couples filing separately, then, the maximum amount of I Bonds that could be purchased during the year increases to $10,000 × 2 (purchased electronically through TreasuryDirect) + $5,000 × 2 (purchased through separate income tax returns via Form 8888) = $30,000.

Of course, in order for a taxpayer to use Form 8888 to direct some or all of their refund towards the purchase of I Bonds, they must be entitled to a refund to begin with! Accordingly, to the extent that an individual would like to take advantage of the ability to purchase an additional $5,000 of I Bonds with their Federal income tax refund, it’s important to review their withholdings and/or estimated tax payments to make sure that they are on track to have a refund sufficient to support their desired purchase.

Convert Paper I Bonds To Electronic I Bonds Using SmartExchange

While the ability to purchase an additional $5,000 of I Bonds (with income tax refunds, through filing Form 8888) may make the paper bond option attractive (as it increases the maximum annual purchase limit), ultimately, most individuals are best served by holding as many of their Federal bonds in electronic form as possible.

Thus, to the extent that an individual purchases paper I Bonds, it is generally best to convert those paper bonds to electronic bonds at the earliest possible opportunity.

Notably, paper bonds are at greater risk of loss due to theft, fire, flood, or other natural disasters. In addition, converting paper I Bonds to electronic I Bonds makes them easier to keep track of (both for investment purposes as well as simply knowing where the bonds are) and are easier to redeem for cash at the appropriate time.

Thankfully, the TreasuryDirect website offers an easy way for individuals to make the paper-to-electronic conversion via what the Treasury refers to as SmartExchange.

Individuals simply need to log in to their TreasuryDirect account and select the “Establish a Conversion Linked Account” option. Once the Conversion Account is established (effectively an account within an account), individuals need only to follow the online instructions to facilitate their conversions.

In a perfect world, an investment would have a high degree of principal protection, provide a strong return, and would always be fully liquid. Of course, we don’t live in that perfect world, and all investments offer some sort of trade-off.

That said, for some investors, the current rate on I Bonds may make them about as close to a perfect-world investment as they can get. Notably, I Bonds offer 100% principal protection backed by the full faith and credit of the United States, an interest rate that is currently an annualized 7.12%, and full liquidity after just one year (albeit with the loss of three months of interest through the end of the bond’s fifth year of ‘life’).

With such attractive qualities, many investors would happily invest large portions of their wealth into such vehicles… if they could. Unfortunately, that’s generally not possible, thanks to the $10,000 maximum amount of I Bonds that can be purchased for any individual during any year.

That said, for those who do wish to invest more than $10,000 in I Bonds at the current 7.12% Composite Rate, a variety of options may be available. One option is to simply purchase one tranche of I Bonds before the end of 2021 and a second tranche in early 2022 (before May 1), while the 7.12% annualized rate will still be guaranteed to apply to the first six months. Others may wish to expand their purchase of I Bonds by purchasing some for other family members, such as children or grandchildren, or using their businesses or trusts to purchase additional $10,000 ‘slabs’ of I Bonds each year. Finally, individuals (along with certain trusts and estates) can use a Federal income tax refund to purchase up to an additional $5,000 of I Bonds annually.

Even after considering the ways in which the standard $10,000 I Bond limit can be expanded, the total amount that can be invested in such bonds in a limited period may never be enough to fully satisfy an individual’s desire. The bottom line, though, is that given the investment’s rather favorable attributes – especially in today’s environment – when it comes to I Bonds, many clients will be happy to take whatever they can get.

Hello – great article. I have been inviting in I bonds for a year or so. My wife and I have a revocable grantor trust with all of our assets in it. Our TreasuryDirect account is in the trust’s name. The trust has both of our social security numbers associated with it. With that, I thought I could buy $20,000 of I bonds per year. I tried that this year, and while the purchase went through, TreasuryDirect sent me a letter saying I was abusing the system and could have my account closed and bonds redeemed. Any thoughts on how to buy our full allocation of $20,000 each year?

The problem is that the $10K limit is per account, regardless of how many people are listed on the account. I am surprised that a $20K purchase for one account would even be accepted by the TreasuryDirect website. You should contact them to find out what has to be done to fix this. Since this occurred in a trust account, you and your wife can still each open your own separate personal account and buy $10K per calendar year. That would enable you to buy a total of $30K of electronic I Bonds per calendar year for the three accounts.

Thanks for this. I was a not quite accurate in my description of what I did. Rather than 1 purchase of $20K, I did 2 separate purchases of $10k each about a month apart. The second one went through, but with that second one I got the note from TreasuryDirect saying this was not OK and they reserve the right to redeem and close my account, which they have not done and enough time has passed that I don’t think they will.

So one thing I want to make sure I have right – the tax ID on the trust is both my and my wife’s SSN. Despite that you are thinking that I can buy $10k for the trust, $10k for me and $10k for my wife in a calendar year?

Thanks

Yes, that is correct. Even though your SSNs are on the trust, your personal TreasuryDirect accounts are still counted as separate from the trust. A married couple with a trust is a common way for a household to buy up to $30K of I Bonds within a calendar year, as long as each account only buys $10K within that year. If you complete the purchases this year, then in January you can buy up to a total of another $30K of I Bonds using those three accounts. I Bonds are great deal at the moment.

Nevermind

There’s a lot of interest in this. I really appreciate the deep dive.

At my firm, we’re fee-only and work on retainer, so we’ve been talking with some clients about I Bonds. Another advisor and I have a YouTube channel. The videos on I Bonds (one on generalities, one with a third advisor who has been using them since 2005 and a third about giving them as gifts) are popular!

I don’t want to be overly-promotional, and I don’t even know if this will work, but here’s the link to the discussion with the advisor who has been using them for over a decade:

https://youtu.be/AYr_7L6OaCs

If the bonds are sold before the 5 year mark and you lose 3 months of interest. Is the 3 month loss of interest on the base rate, the inflation rate or, both?

I’m guessing the current rate for the 6-month period during which the bond is sold. From my understanding, the rate is adjusted to the rate of inflation every 6 months.

Can you purchase these I Bonds within a ROTH IRA account? So that the 7.12% interest is not taxed?

No. They can only be purchased by individuals directly from Treasury using after tax dollars.

The Treasury Direct site is so clunky and the customer service is so horrible if something goes wrong or you simply need to change the registered bank account (just do a web search to see what I’m talking about) that I’d prefer to hold paper bonds and cash them at my local bank, as previously with EE bonds. In light of this I don’t think it’s good advice to encourage anyone to “convert those paper bonds to electronic bonds at the earliest possible opportunity.”

This procedure may be changing. In spite of being a depositor in the bank I recently cashed some savings bonds, I was told bank would now be cashing bonds up to $1,000. and was encouraged to either come back for additional redemptions or send bonds to Treasury Direct. I can see a change coming to the day Treasury will be the only option for redemption, although if you are a person who keeps good records and tracks your bonds, keeping them in paper form is the better way, in my opinion, and I would keep them in a safety deposit box.

Is it possible to roll an H bond coming up to maturity into an I bond?

Thanks Jeffrey- I did this in size.

Just wanting to clarify, if you are wanting to redeem right after the 12 months of non-liquidity, because it was not held for more than 5 years, you would lose the last 3 months of interest on that I Bond? In this scenario, you would only earn the interest for 9 months, unless you held it for 1 year and 3 months to get that “ideal” annual return. Is that correct?

Can one person buy $10k for their own account, and also listed be as second owner on more than one other account?

For instance, in Example 3 above, could Ian have his mother open another account with her as the first owner and himself as the second owner? That would mean he is listed as sole owner on one account, second owner on the account with his wife, and second owner on the account with his mother.

Thanks.

Is an IRA LLC allowed to invest in I-Bonds?

what happens if you purchase through an LLC and then that LLC is closed at a later date, say 2 years? Does the bond have to be redeemed?