Executive Summary

As the retirement income research evolves, an increasingly common question is whether the popular safe withdrawal rate approach is better or worse than an annuity-based strategy that provides a guaranteed income floor, with the remaining funds invested for future upside.

Yet the reality is that as it's commonly applied, the safe withdrawal rate strategy is a floor-with-upside approach, too. Unlike the annuity, it doesn't guarantee success with the backing of an insurance company; yet at the same time, the annuity is assured to provide no remaining legacy value at death, while the safe withdrawal rate approach actually has a whopping 96% probability of leaving 100% of the client's principal behind after 30 years!

Which means an annuity is really an alternative floor approach to safe withdrawal rates - one that provides a stronger guarantee while producing a similar amount of income, but results in a dramatic loss of liquidity, upside, and legacy. Does the common client preference towards safe withdrawal rates and away from annuities indicate that in the end, most clients just don't find the guarantee trade-off worthwhile for the certainty it provides?

The inspiration for today's blog post is a recent email correspondence I had with retirement researcher Wade Pfau, discussing the traditional life-cycle finance economist approach to retirement planning that typically focuses on first securing a guaranteed income floor to cover essentials, and then providing for additional discretionary expenses with a more growth-oriented investment option (since discretionary expenses by definition can be flexible and adjust if/when/as good returns occur). The floor/upside approach is often contrasted with the safe withdrawal rate approach, where the portfolio is managed for total return and ongoing distributions come out of the portfolio as necessary to cover retirement expenses each year, but there isn't a split with a guaranteed floor and a discretionary upside portfolio.

Yet the reality seems to be that as it is designed and commonly applied, the safe withdrawal rate approach is a floor-with-upside approach.

Setting the Retirement Income Floor

In the traditional floor-with-upside approach, the floor might be invested using either TIPS or an inflation-adjusted annuity, providing the retiree certainty that essential expenses can be covered - notwithstanding the uncertainty of inflation - for the desired retirement time horizon (using TIPS) or for life however long than may be (using an inflation-adjusted annuity).

Thus, for example, if a retiring 65-year-old couple has a $1,000,000 portfolio, and decides that they need $25,000/year in addition to Social Security benefits to meet their essential spending needs, the couple might purchase a single premium inflation-adjusted immediate annuity for their joint life expectancy, with an approximate payout rate of 3.88% - this would require $644,330 to purchase the annuity, and leave $355,670 available to invest for growth, to provide upside to future discretionary spending, and to serve as a reserve for emergencies.

Notably, though, with a safe withdrawal rate approach, a remarkably similar result occurs. Assuming a 4% safe withdrawal rate, the couple would need to set aside $625,000 in order to establish the require funds to sustain a $25,000/year inflation-adjusted stream of income reasonably expected to last for 30 years - leaving $375,000 left over to invest for growth, to provide upside for future discretionary spending, and to serve as a reserve for emergencies.

This parity occurs because of the simple fact that at the end of the day, both the retiree and the insurance company are investing pooled funds to pay out an inflation-adjusted stream of income... and they're both subject to the same capital markets, likely use similar investment assumptions, and may even use substantively similar investment selections! Which means in environments where the safe withdrawal rate is low, because rates are low and/or valuations are high, both the payout rate on SPIAs and the sustainable safe withdrawal rate spending from a portfolio suffer similarly, and both end out with a floor remarkably close to 4%! If rates were higher, the annuity payout rates would likely rise; however, if rates were higher, it would also be more likely the retiree could sustain a withdrawal rate higher than 4% as well.

Not All "Guaranteed" Income Floors Are The Same

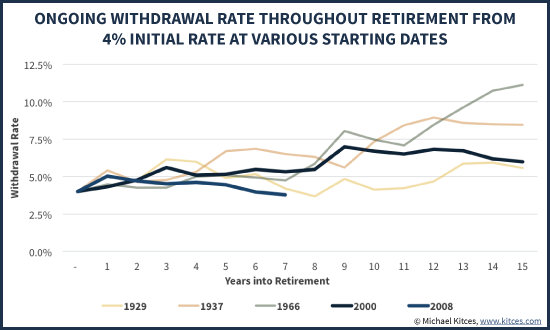

Of course, it's important to note that not all guaranteed (or "guaranteed") floors are the same. While the safe withdrawal rate spending level is set, by definition, at a level that hasn't failed at any point in the past century (at least with respect to the US markets), that doesn't mean some future scenario couldn't unfold that would be worse than anything witnessed historically (although notably, safe withdrawal rate creator Bill Bengen recently showed, and this blog subsequently supported, that even for a year 2000 retiree, the outlook after 15 years still looks far better than any of the historical scenarios that might have stressed a 4% withdrawal rate!).

On the other hand, the inflation-adjusted immediate annuity is backed by a genuine guarantee from an insurance company. Which means even in a scenario worse than any in history, the annuity company guarantee may potentially kee

In addition to the distinction between "never failed in history" and "actually backed by an insurance company guarantee" it is also notable that a safe withdrawal rate floor is fixed for a target time horizon (30 years in the case of a 4% withdrawal rate), while the inflation-adjusted joint survivorship immediate annuity is guaranteed (again, backed by an insurance company) for the lifetime of the couple, regardless of how many years that turns out to be.

The Cost/Benefit Tradeoffs For True Retirement Income Guarantees

All else being equal, any rational retiree would choose an insurance-backed guarantee to "just" the assuredness that the plan has never failed in any historical scenario, and similarly would choose payments that are guaranteed for life instead of just an arbitrary time horizon that could be outlived. However, not all else is not equal.

The key distinction is the liquidity and flexibility that the safe withdrawal rate approach provides, relative to the immediate annuity - including the fact that any excess returns accrue to the benefit of the investor (not the insurance company), and that a premature death leaves any remaining investments to family, charity, or anyone else the decedent designates (not the other annuitants doing business with the insurance company).

Which means in practice, retirees have to weigh the benefit of a not-quite-fully-guaranteed safe withdrawal rate floor with the fully guaranteed annuity, against the cost of liquidity, upside, and legacy assets. And the differences may not be trivial.

After all, as previously discussed in this blog, while the safe withdrawal rate approach is one that self-liquidates the portfolio over 30 years in the worst case (historical) scenario, the reality is that 96% of the time, the retiree still has 100% of his/her principal remaining. In fact, in over 50% of the scenarios, the retiree more-than-quadruples the starting principal value, in addition to sustaining 30 years of retirement spending.

Of course, this fails to address the second guarantee provided by the insurance annuity - that payments will last for life, however long that may be, while in the worst case scenario the safe withdrawal rate approach is expected to deplete the portfolio at the end of 30 years. Yet the reality is that a 65-year-old couple has only a 17.6% probability of actually living for 30 years (the life expectancy for a 65-year-old couple is just under 24 years), and as noted above the retiree also has a 96% chance of having 100% of principal left over to fund unexpected longevity years as well. Which means to truly fail, the couple needs to be unlucky enough to live through an investment environment worse than any found in history (so there's no principal left at the end), and be the approximately one-out-of-six couples that is actually still alive at/beyond the 30-year time horizon. As discussed previously in this blog, when you combine low-probability investment disasters and low-probability longevity scenarios, you can end out with some astonishingly low probability scenarios... many of which could be further "saved" by small mid-course corrections, anyway.

Is Any Retirement Income Floor Guarantee Truly Guaranteed?

Of course, it's also important to note that even insurance company guarantees are only as good as the insurance company backing the guarantee. This is important because, in the context of discussing investment scenarios that cause safe withdrawal rates to fail, which by definition must be worse than anything witnessed in history, extraordinary investment shocks that destroy a 30-year safe withdrawal rate could potentially threaten an insurance company, too.

Similarly, a dramatic shift in population longevity - where a large number of clients all begin to live materially longer and threaten the conservatism of a 30-year time horizon for a 65-year-old couple - could also threaten the health of the insurance company. Granted, these are extremely low probability scenarios - thus why good insurance companies maintain strong financial ratings despite the conceivable possibility this could occur - but again, that's the point. For the retiree who is deeply concerned about such remote possibilities, questioning the safety of safe withdrawal rates inevitably raises questions about the security of the insurance company's guarantee as well - especially for affluent clients whose immediate annuity payments may exceed any state guaranty protections.

This, unfortunately, is the problem with anchoring decisions to remote catastrophic events; it becomes difficult to know which investment strategies - or entire insurance companies - will survive intact.

Choosing A Retirement Income Floor Approach

The bottom line is that choosing between immediate annuities and safe withdrawal rates is not a decision about whether to use a floor/upside approach or not; it's about choosing which floor is preferable, in light of the trade-offs the decision entails.

In the context of the earlier example, the client who annuitizes for $25,000/year of income is guaranteed with inflation-adjusted income for life, but is guaranteed at best to have only whatever the remaining $355,670 portfolio grows to. On the other hand, the client who uses the safe withdrawal rate approach grows that $625,000 allocation to $2.5 million over half the time (even after withdrawals!), in addition to whatever the $375,000 portfolio also grows to as well! Which means the effort to turn "never failed in history" to "guaranteed by an insurance company" (and hoping the insurance company won't also fail in such a catastrophic scenario) can cost the client's heirs a whopping $2.5 million more than half the time, to protect against a scenario that has an incredibly remote joint probability (of worse-than-history bad returns and the insurance company surviving and unusually extended longevity to be around to witness the problem in the first place).

Notably, this trade-off becomes even more problematic as the income need rises relative to the portfolio. If the client's goal was $40,000/year from the portfolio instead of $25,000/year, the client would either allocate all of the $1,000,000 portfolio to the safe withdrawal rate approach, or annuitize the entire $1,000,000 portfolio, which still wouldn't quite produce all of the desired $40,000/year real income stream (given the 3.88% payout rate, and not to mention potentially creating further liquidity issues).

In point of fact, I suspect this is one of the primary reasons why the safe withdrawal rate approach is so radically more common than annuitization strategies in the first place - both produce roughly comparable floor amounts, but the safe withdrawal rate approach doesn't surrender liquidity and control, and retains what in reality is a high probability of something between a substantial and very substantial upside (compared to an annuity approach that guarantees nothing of the annuity's value will be left and no upside can be enjoyed). And for the retiree who wants the annuity guarantee, and a reserve for liquidity and emergencies, the annuity retiree actually has to save significantly more than the safe withdrawal rate retiree - which may be especially problematic when most retirees already fail to save enough.

But the bottom line is that when a retirement spending goal is tied to a 4% safe withdrawal rate, the strategy effectively is a floor-with-upside approach - and one where the odds are overwhelming that the client will preserve all of the original principal, and potentially several multiples thereof, which will be available to either safely raise retirement income further some number of years down the road, serve as a contingency against unexpected longevity, or leave a substantial legacy. The client does have the potential to convert "highly probable" scenarios into something more certain, but the transaction does entail significant trade-offs.

So what do you think? Would you consider safe withdrawal rates to be a floor-with-upside approach? How important is the upside to clients if the floor is reasonably secure? How secure do you consider the safe withdrawal rate floor compared to an annuity guarantee? Is it worth the upside cost? Does the annuity guarantee still feel secure in light of the scenarios it would take to cause a safe withdrawal rate failure in the first place?