Executive Summary

One of the foundational principles of retirement success is to start saving early. After all, the longer that money can stay invested, the more compounding growth can work in your favor; all the better if your savings grow inside a Roth IRA and avoid the grinding impact of taxation.

Yet the reality is that clients really have two major assets: their financial assets, and their human capital asset. And when the client is young, the human capital asset is actually the bigger of the two by far. As a result, allocating savings towards human capital in ways that increase its value or growth rate can actually have far more impact than investments in financial assets; spending $2,000 on classes that produce a $1,000 raise in base salary can, over the next 40 years, generate nearly 20 times the wealth of merely saving the $2,000 in a Roth IRA and growing it for decades.

Does that mean that clients who allocate savings to retirement accounts when they're young are actually making an inferior long-term investment?

The inspiration for today's blog post was a recent conversation I had with another planner who is starting a firm intended to serve Gen X and Gen Y clients. As the planner noted, an assets-under-management business model would be difficult to run profitably, given that younger people often don't have an asset base to invest yet. "Indeed," I replied, "And you might find that the best way to maximize the young client's long-term wealth is to keep them from investing in financial assets at all!"

Human And Financial Capital

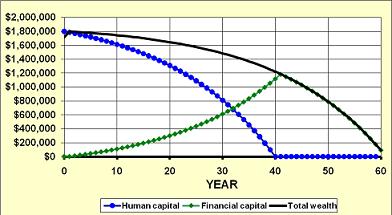

As I have written in the past, the reality is that young clients actually have two major categories of assets to manage on their balance sheet: financial capital, and human capital. The financial capital includes investments of various sorts, from stocks and bonds to bank accounts to real estate. The human capital represents the client's income earning power over time. Early in life, the human capital is high and the financial capital is low. As the client works and ages, human capital is converted into cash flows that are either spent, or saved as some form of financial capital. Ultimately, when the human capital runs out - at retirement - the financial capital is spent down for the individual's remaining years.

As I have written in the past, the reality is that young clients actually have two major categories of assets to manage on their balance sheet: financial capital, and human capital. The financial capital includes investments of various sorts, from stocks and bonds to bank accounts to real estate. The human capital represents the client's income earning power over time. Early in life, the human capital is high and the financial capital is low. As the client works and ages, human capital is converted into cash flows that are either spent, or saved as some form of financial capital. Ultimately, when the human capital runs out - at retirement - the financial capital is spent down for the individual's remaining years.

As a result of this dynamic, the reality is that clients actually have the potential to increase their total wealth by either increasing financial capital - saving more and/or generating higher returns - or by increasing their human capital - working more hours, more years, or growing income more rapidly.

Changes To Human Capital

As the chart above illustrates, the reality is that in a client's early years, the human capital - often simply quantified as the present value of future earnings - dominates the balance sheet, while financial capital is low. This is due primarily to the simple fact that there is an entire career's worth of earning years ahead.

Because of this, though, the reality is that making investments that alter the trajectory of an individual's future earnings can have a dramatic impact on the value of human capital and therefore on lifetime wealth. Whether it's a slight increase in earnings (that becomes the new base for future raises and income growth) or merely an increase in the growth rate of future earnings in the years to come, small changes have a big effect.

For instance, imagine a 25-year-old client who is looking ahead at a 40-year working life. Current earnings a few years out of college are $40,000. Assuming earnings increase at 3%/year for inflation, the client is anticipated to earn just over $3 million of cumulative earnings over the working years; at a discount rate of 8%, the client's human capital is effectively an $808,424 "asset" on the balance sheet.

So what happens if the client gets a $1,000 raise, pushing up base salary to $41,000 (upon which all future inflation adjustments are applied). Over the 40-year working career, a $1,000 raise isn't just a $1,000 increase in income, but a $20,210 increase in the total (net present) value of the human capital asset.

On the other hand, improving the client's career trajectory has an even greater impact - if the client can generate a 1% real growth rate in income (i.e., grow income at 4%/year where inflation is only 3%), the human capital asset jumps in value (on a present value basis) by a whopping $112,374! Small changes have a significant impact over extended periods of time.

Choosing Where To Invest

The distinction between financial and human capital is important because the reality is that when clients have excess cash flow available to invest, there is a choice about where to invest it. Allocating the savings to a bank account or a Roth IRA represents a decision to invest in financial capital. Allocating the savings to take a class to advance education or improve job skills would be a decision to invest in human capital.

For older clients who are nearing or at retirement, the decision about where to allocate capital is clear - it should be directed to financial assets, which have to carry the full load of financial support when the human capital runs out at retirement. For younger clients, though, the decision is not nearly so straightforward.

For instance, imagine a client has $2,000 available to invest. The money can either be directed to a Roth IRA to generate tax-free retirement income in the future, or it can be used to take a series of classes at the local college on Microsoft Office that could potentially lead to a small promotion at work with a $1,000 increase in base salary.

Offhand, this seems like a losing proposition - spending $2,000 on classes leads to only a $1,000 increase in current income? Yet when viewed over the entire career, the outcome is quite different - as noted earlier, the net present value of the investment over the entire career is actually more than $20,000, representing a 1,000% return! Viewed on a future value basis, the extra earnings invested each year for the next 40 years would produce nearly $400,000 of future financial assets; by comparison, the $2,000 IRA would grow to "only" a little over $20,000 over the span of four decades. Thanks to the benefits of compounding, the human capital investment actually outperforms the IRA savings by a whopping 2,000%!

Risk And Uncertainty Of Human Capital

It's certainly true that investments in human capital are not always the "sure thing" projected here. Not every investment in a class that improves productivity or job skills delivers a clear corresponding increase in income. Nonetheless, the "investment opportunity" is often still underrated; as the numbers here show, even spending $10,000 on education for a $1,000 lifetime increase in income is still an incredibly positive financial result (and superior to the Roth IRA investment, even if we tax some of the earnings along the way).

And of course, the example shown here merely projects the impact of a $1,000 raise; not the benefit of increasing job skills enough to generate a material promotion (e.g., a 10% raise!), or to set an individual's career trajectory on a higher overall growth rate (although as the numbers showed earlier, a 1%/year increase in income growth rate actually produces an ever greater impact than the $1,000 raise on a $40,000 base income!). Similarly, as noted in the past on this blog, more education and job skills are also associated with lower unemployment - if that $2,000 investment means you keep your $40,000 job and your neighbor is laid off, the benefit of the investment relative to your neighbor is even more dramatic than any of the projections shown here!

The point here is not to justify the high cost of a college education in particular - if the outflow is not $2,000, but $100,000 or $200,000 or more, the burden is really on the student to generate a higher income to come out favorably in the end. The point is simply that, even on a smaller scale basis, the principle still holds: even though there are many years to invest and grow money in a Roth IRA as a young person, the compounding benefits of investing in human capital can still be exponentially greater. Or viewed another way, investing in human capital in the early years can allow for even more savings towards financial capital in the later years after the income has grown... even when accounting for benefits like four decades of tax-free Roth IRA compounding growth.

So what do you think? Have you ever counseled a client to invest in their career and income growth instead of a retirement account? Or is it risky because the career payoff is still so uncertain? Is investing in human capital a rational and effective approach despite the uncertainty? Are young clients under-investing in career and over-investing in financial accounts?

(Editor's Note: This article was featured in the 15th Edition of Financial Carnival for Young Adults on Young Family Finance.)

Michael, this is an intriguing notion, but I think it’s very difficult to apply it outside of a few well-defined areas where there is a clear link between a specific educational or training outcome and increased salary.

Other than an old-fashioned college or professional degree, the example I’m most familiar with is credit hours for public school teachers, where frequently a teacher could increase her salary by a known amount, permanently, by earning a certain amount of continuing education credits related to her job. That’s a pretty straightforward IRR calculation.

Can you think of other examples that are similarly straightforward? Because as you point out, the unclear (I was going to say “speculative,” but that’s perhaps too harsh) relationship between marginal investment in education and increased salary makes it very hard to do more than a gut-level analysis in most cases. And that, to my mind, makes the kind of investment you’re talking about, much of the time, riskier than simply investing the money in equities.

Matthew,

Indeed, I’ll grant there is some uncertainty here. Depending on the individual’s profession/vocation, I’ll even grant ‘borderline speculative – although I think targeted focus on what’s most productive could reduce that uncertainty to some extent.

But we’re not talking small rewards either. My simple example is 2,000%(!) better than the Roth, and I don’t think it’s a stretch at all to get a 5% raise (on a $40k salary) for improving job skills.

I’ll grant that most writers don’t get a raise in $$$/word for taking a writing class. But at the same time, most of the best paid writers didn’t just luck into the job. They studied and learned (and practiced). Whether you’re an engineer or a financial planner or a computer programmer, there are educational programs that can materially improve job prospects.

Argusbly, the resurgence of vocational schools and very applied programs like what University of Phoenix and similar schools offer suggest that many are already realizinf the payoff. It doesn’t take much of a raise, reduction in unemployment, or improvement in job trajectory to obliterate the return of ‘just investing in a retirement account’.

-Michael

Good points all. I’d love to see some more specific cases. I suspect that most people given $2000 and told to spend it on improving their human capital wouldn’t know where to start, but you’re right that as I start to think about it, more and more ideas for a variety of different types of workers come to mind.

I feel investing in one’s career is almost always a great decision and is preferred to investing in markets if resources limit one over the other.

We all have clients who made loads of money in their 40’s and 50’s (an overnight success!), even if their earlier years were low earning. It’s most certain that these folks invested in themselves over time.

If a young person has poor prospects due to a certain occupation, all the more reason to invest in new skills (new field or a business).

Good article.

Ramit of “I Will Teach You to be Rich” fame has also come to this conclusion and since his constituency is mostly 20 and 30 somethings, he has created two course for people to improve their career asset.

His earn 1K is about how to create extra side self-employment income (http://earn1k.com/) and his dream job program is about how to land a better job (http://www.iwillteachyoutoberich.com/insiders-kit/dreamjob/). Both courses cost a few thousand, but for those who follow through can give a much higher return than you would expect from traditional investments.

David

And you’ve just explained why I’m back in school! Great article Michael. I’ll keep you posted on how the human capital part pays off!! LOL!

This doesn’t just apply to those with traditional careers, but to clients who have their own businesses — and in spades.

It takes capital to grow a business. There are enormous decisions to be made by business owners, especially in the early years, as to whether to use earnings to fund growth or to fund retirement plans.

I have never seen this question arise in an “either/or” format in real life where the person in question had a decent job. You make a great point about the need to invest in one’s career, Michael. But with careful budgeting and frugal living, nearly everyone who is gainfully employed can invest in both career and retirement. The far bigger problem in my experience is an unwillingness to live frugally and save. Among our besetting sins is our unrelenting opposition to delayed gratification.

I think this is a great article and definitely gives young people something to think about. Done correctly, it’s absolutely true that an investment in your career can pay huge dividends, often as you say much greater than simply saving.

But as another commenter has pointed out, I would be careful about painting this as an either/or proposition. In addition to the possibility of accomplishing both types of investing, it worries my to think that people might read this and conclude that they don’t need to start saving. If anything, starting the saving process at a young age makes for a strong habit. If you ignore that habit when you’re young, what are the chances that you’ll pick it up “later” instead of waiting until it’s too late?

I do not think your point here was to persuade young people that they don’t need to save. I think your argument is a good one, and should be made complementary to advice to start saving early.

Matt,

I don’t think this is necessarily a prescription to “not save” by investing in your human/career capital instead of a retirement account.

Whether you redirect $3,000/year to your retirement account, or training classes, it’s still $3,000/year you’re NOT using to maintain your ongoing lifestyle and spend on consumption – and as you note, THAT is the real key here.

In other words, if someone makes $30,000/year and allocates $3,000 to saving OR classes, the end result is still that they’re getting into the habit of living on only $27,000/year and NOT the last 10%. And I fully agree with you that that is a crucial habit. But it’s actually still being achieved whether “savings” goes to a retirement account or a class.

You can see some of my further comments about the importance of setting good spending habits elsewhere on this blog too; for instance, http://www.kitces.com/blog/archives/336-Is-A-Goal-To-Save-A-Percentage-Of-Income-Every-Year-Bad-Retirement-Advice.html

Respectfully,

– Michael

All true, Michael. However, investments in human capital are subject to much steeper diminishing returns. Whereas, financial profits, although eventually subject to DMU, have a much flatter trajectory.

I’m not sure why you have made a connection with all young people and a lack of human capital. I am 23 years old with a college degree in a field where a masters and doctorate degree mean very little. At some point with every career, you reach a diminishing return on investment in your human capital. The best investment, in my case, for human capital is to go to work everyday and learn. Not continuing education. So in my case it is probably better to go with an IRA.

However, there are plenty of fields that would benefit from a masters or doctorate degree. To say that one is more valuable than the other for young people is a generalization at best.