Executive Summary

The growth of financial planning has been an incredible success story of the past 40 years, as the broader financial services industry slowly but steadily continues its shift away from the pure sale of products and towards the direction of personalized financial advice. Over the 25 years since the first CFP certificant was minted in 1973, nearly 10% of financial advisors obtained the designation, and the pace has accelerated as the CFP certification has continued to grow while the total number of advisors has been stagnant, now reaching what may be the “tipping point” of nearly 25% of all financial advisors.

Yet at the same time, the growth of CFP certificants – especially in the past decade – has not only outstripped the growth of all financial advisors; it has also dramatically outpaced the growth in the number of affluent households that financial planners typically serve. The end result: we are rapidly approaching the point where there are so many CFP certificants that there aren’t enough available half-million, millionaire, or wealthier clients available for them to serve.

As a result, financial planning may soon undergo a shift towards serving a wider base of clientele. The change will be driven not merely out of a desire to become a recognized profession that serves a wider base of the public, but instead out of sheer business necessity as financial planning firms of the future find they must lower their minimums and seek out a new “blue ocean” of prospective clients rather than continue to fight in a highly competitive space where just being a comprehensive financial planner is no longer the differentiator it once was!

Growth Of Financial Planning

Although the first CFP certificant was minted in 1973, for much of the early years financial planners were at the fringe of the broader world of financial advisors, and formed a fairly insignificant percentage of those who delivered insurance, investments, and advice. It took nearly 25 years to mint the first 34,000 financial planners (from 1973 to 1998), and by that time they still compromised barely 10% of all those who might have called themselves “financial advisors.”

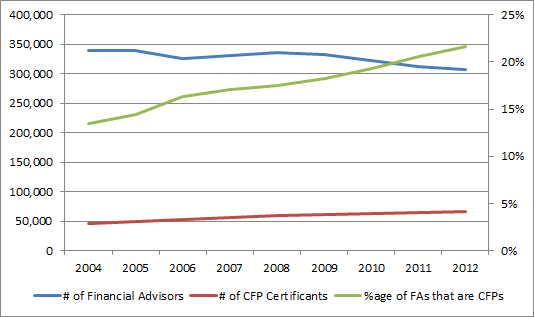

Over the past 15 years, however, the landscape has begun to shift dramatically. The number of financial advisors has been stagnant and is now in outright decline, while the number of CFP certificants has more-than-doubled to 69,000. The end result: while in the late 1990s barely 1-in-10 financial advisors were CFP certificants, it’s now rapidly approaching 1-in-4! The chart below, based on the CFP Board’s reported certificants, and the number of financial advisors based on Cerulli research back to 2004, shows how this trend has played out in recent years.

While the percentage of CFP certificants is still limited, “just” approaching 25%, it’s notable that with many types of innovation (across various industries), reaching 20%+ market penetration often represents the “tipping point” where adoption accelerates (his concept was the basis of Malcolm Gladwell’s popular “Tipping Point” book). Already, the pace has been accelerating - there were as many CFPs added in the past 15 years as there were in the prior 25 – which means financial planning may just be approaching the crossover point where it becomes even more widely adopted as a core of delivering personalized financial advice.

How Many Affluent Households Are Available To Consume Financial Planning?

While from the perspective of the public, the explosion of available financial planners has been and should continue to be a tremendous positive, when viewed from the competitive perspective it paints a very different picture, especially given the trend in recent years towards larger financial planning firms that have tended to lift their minimums to target more affluent clientele.

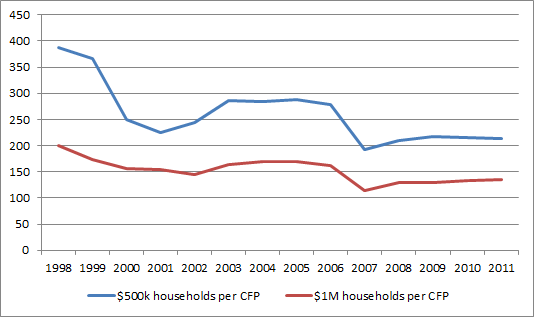

For instance, the chart below graphs the number of households with either $500k or $1M of net worth (not including their personal residence, based on available data from Spectrem Group) relative to the number of CFP certificants (as reported by CFP Board).

As the data reveals, back in the late 1990s, there were almost 200 millionaires for every CFP certificant; since then, the number of millionaires is up almost 30%, but the number of CFP certificants are up 100%. As a result, the number of millionaires per CFP has fallen to only about 130. In the case of a more “mass affluent” clientele – those with at least 500k of net worth (not including the personal residence), the results are even more extreme, as the number of mass affluent per CFP certificant has fallen from about 385 down to just over 200.

And of course, as noted earlier, CFP certificants make up barely 25% of all financial advisors. In the aggregate, the number of $1M households is currently no more than 30 per financial advisor in the aggregate, and the number of 500k households per financial advisor is only about 46.

In other words, just serving clients at these levels, there aren’t even enough clients to go around for the number of financial advisors, and there are barely enough to go around even if every half-million and millionaire household worked with a CFP certificant (given that research suggests at best an individual can only maintain about 150 {financial planning and other} relationships). And if/when/as the share of financial advisors that are CFP certificants continues to increase, there simply will not be enough clients for the number of financial planners.

And of course, the caveat to the numbers above is that some large number of households are self-directed regarding their financial matters; only a subset of these prospective clients will ever actually become financial planning clients. Which means in truth, the problem of the availability of affluent clients – or a lack thereof – may already be far more severe than the charts suggest!

Finding The Blue Ocean In Financial Planning

All of this discussion is not to imply that there’s no opportunity for success and growth as a financial planner. Instead, the simple point is that financial planning is rapidly approaching the crossover point, not only where it needs to serve a wider base of households simply to grow beyond being “something for wealthy people” into a recognized and bona fide profession, but also simply because we’re “running out” of more affluent clientele! And to say the least, we’re also reaching a crossover point where being a CFP certificant and providing comprehensive financial planning as an experienced practitioner is no longer a differentiator but now more of a minimum standard just to be competitive, especially as financial planning remains one of the few clear value propositions in a world where much of what advisors traditionally did in the past – from implementing insurance and investment products, to building basic asset-allocated diversified portfolios – is becoming commoditized by technology.

On the other hand, adjusted for the number of households with $100,000 or more in net worth (excluding the personal residence), the number of potential clients per CFP certificant is (still) a far more manageable 542 (and even a respectable 122 households per total financial advisors). Going further “downstream” yields even more available clientele, not only because there are more of them, but also because only a limited number of financial planners are currently serving the space. In other words, figuring out how to work with a wider range of households is essentially an entirely new “blue ocean” – similar to the environment of the more affluent from 10-15 years, it’s a space where just being an educated, experienced comprehensive financial planner is a differentiator.

On the other hand, adjusted for the number of households with $100,000 or more in net worth (excluding the personal residence), the number of potential clients per CFP certificant is (still) a far more manageable 542 (and even a respectable 122 households per total financial advisors). Going further “downstream” yields even more available clientele, not only because there are more of them, but also because only a limited number of financial planners are currently serving the space. In other words, figuring out how to work with a wider range of households is essentially an entirely new “blue ocean” – similar to the environment of the more affluent from 10-15 years, it’s a space where just being an educated, experienced comprehensive financial planner is a differentiator.

Notably, though, succeeding with this kind of target clientele will require the delivery and business models for financial planners to evolve further from where they are today. On the one hand, many of the problems of these clients may be “simpler” (in that they don’t involve the kinds of esoteric tax rules and strategies applicable to wealthier clients), but may also have a heavier educational and behavioral component. Early results from some planners serving this space suggests that financial planning may need to be more “modular” (analyzing one section of the plan at a time, as wanted/needed) rather than always delivering the fully comprehensive (written) financial plan up front. And whether the business model of the future to serve this space is a form of the existing commission-based models, the Garrett Planning Network’s hourly model, a new form of monthly retainer model, or something else altogether, remains to be seen as well.

Nonetheless, the bottom line is simply this: over the past decade, as financial planning has continued its evolution towards being a recognized profession, there has been a growing professional angst over figuring out how to expand financial planning to serve more. But the successful growth of financial planning may soon turn this from a wistful desire into a sheer business necessity, as the pace of growth for CFP certificants has so outpaced the growth of the affluent households they serve that expanding to a wider market may soon shift to being a professional desire to a sheer business necessity!

Share your own thoughts in the comments below. Have you felt pressure to lower your minimums (or not raise or put them in place to begin with?)? Do you think the competition for clients as a financial planner is more difficult than it used to be?

The lowering of account minimums reflects several market realities, (1) less complicated accounts are more profitable, far more numerous and far less complicated than large accounts, (2) building a practice around expert prudent process translates into an extremely high level of threshold counsel which is scalable without regard to a minimum level of assets, (3) advanced technology and more modern approaches to portfolio construction facilitate a far higher level of portfolio detail being managed in real time as required for fiduciary standing than is presently possible in a commissioned sales format without regard to account minimums, (4) scale and the streamlining of cost is achieved through a functional division of labor and work flow management not allowed or possible in a brokerage format again not dependent on account minimums, (5) Client satisfaction and advisor accountability and ongoing responsibility for recommendations in the client’s best interest all require conflict of interests to be eliminate without regard to account minimums. Thus, there is not rationale that suggests account minimums are determinative of the level of counsel provided or the cost entailed. innovation exponentially increases the level of counsel provided and greatly streamlines cost.

SCW

Our firm has tried to enforce an AUM minimum with little success. Deciding a clients value based on the single AUM metric may very well work fine for Separate Account Managers or Investment Only shops. But our ideal clients are ones that understand and utilize our resources, participate in firm events, stay engaged with us and their financial situation, and understand our wealth management philosophy. While some practical and deminimus limits are necessary, I find it hard to fathom how ignoring such a large segment of the population is a worthwhile long-term strategy regardless of the advisor to HNW metrics.

While I appreciate the healthy philosophy you have postured you make clear that some “practical” limits (minimums) are necessary and that directly speaks to the AUM minimum debate here. Seems the economy of scale seen typically requires AUM in some stated range if only to overcome the other threat to the AUM model…fee compression. AUM for 25 basis points at lower than industry average account values becomes an asset gathering operation and not a planning practice – yet that does compete with the planner trying to make it on the mass affluent or at least that segment of the market willing to write a check for planning services. Try paying yourself a professional salary on a pure hourly model in a solo practice. I did for several years as a member of a network of planners. There are only so many billable hours in a work-week and when you wear all the hats…marketing guy, bookkeeper, planner and office manager pity the soul who also has a family to attend to and eats and sleeps occasionally. The starving idealist is often exactly what one runs the risk of becoming in that scenario (credit Bob Veres for label I believe).

It’s worth noting that I agree with the concept of ‘practical’ limits and minimums as well. The article wasn’t titled “Why Minimums Will Soon Be Abolished” but just why they will be LOWERED. There are real overhead constraints in executing an advisory firm, and SOME minimum revenue/client is still a business reality…

Michael: I enjoy reading your perspectives. However, on this one, I’m not too concerned as an “under age 40 CFP”. I think the fact that so many Boomers are turning 65 each day (more millionaires are being “minted” each day and the aging demographic of the advisor community will translate to plenty of work to do in the future in the HNW space.

Scott,

The number of millionaire households being minted isn’t much. I wrote about this on the blog in late 2012 as well (see http://www.kitces.com/blog/6-ways-the-new-normal-is-re-shaping-the-growth-of-financial-planning-firms/ ) – at that time, we were JUST getting back to the number of millionaires who had existed in 2007 (5 years earlier). As of now, we’re just barely making new highs on the number of millionaires from where we were 7 years ago.

And although I haven’t seen any good statistics for it, given that advisors in the aggregate seem to be attracting clients, and few are losing clients, the number of “unattached” millionaires (or ‘pre-‘millionaires) who don’t already have an advisor has likely diminished greatly as well over the past decade.

Granted, one of the reasons I’m upbeat on financial planning for the CFPs-under-40 crowd is that eventually, when the bulk of the baby boomer advisors have retired, there will be a dearth of planners for the number of affluent households. But that’s the outlook in ~10-15 years from now. Between now and then, it looks like there’s more of a squeeze before we younger advisors can see the light at the end of the tunnel…

– Michael

Mostly what I read about are that the numbers of FAs are on the decline (which I think is actually a good thing). So Michael, I’m missing something regarding your point of view on why FAs will have to lower their minimums.

As it is, not all FAs work with ultra-affluent ideal clients. However, they (if they are my clients) have AUM minimum to guide them and an ideal client profile that’s used to market their services.

My thoughts about the “business” I’d watched grow and change is that FAs will be relied on much more as the center of a person’s financial needs. Think Family Offices… but on a smaller scale. And that there will be lots of strategic alliances and partnerships between FAs and whomever and whatever services their ideal clients need on a usual basis.

Maria,

The TOTAL number of “FAs” are on the decline. But the number of CFPs are on a dramatic rise. In other words, I suspect a large portion of the “FAs on the decline” include old-school stockbrokers and insurance agents who had long been edged out of the high-net-worth space anyway by more comprehensive advisors.

If we believe ANYTHING to the viewpoint that the high net worth are interested in the more comprehensive wealth management services, it would seem the number of wealth managers is still on the rise (as the non-wealth-manager FAs are the ones declining in head count).

Does that help to clarify?

– Michael

Understand your points now. Thank you for the clarification.

One of the things I’m seeing regarding the CFP is that many are entering the industry as CFPs. They want to have their own solo practices 🙁 They tell me that when they looked around it seemed like they “had” to have the CFP in order to get started.

Could be that in 10 years, the “new normal” for the industry will be the CFP and some other new designations will come about.

On the other hand, this is not the only country making millionaires. Foreign investors are continually coming into this county will need advice and planning from the American side. Call me an optimist, but I’d like to think that the number of millionaire will grow again.

And I already know that the industry grows into what is needed at the time.

Michael, I don’t have minimums. I’ve come up with my own formula for those I feel have a good return on human capital potential. I consider human capital growth, center of influence potential, savings and credit habits, a willingness to learn, good communicators. It allows me to capture young professionals who I feel are on their way to be leaders in their business. I work with young television anchors in several cities, those who have started their own businesses, people who have wonderful connections in the community, good core financial habits and are just starting out on careers in industries I feel are prospering. I have a grasp on how many I can handle. I call this group my “inner potential circle.” So far it’s provided me self satisfaction. I love being the go-to financial person for these younger people; it’s exciting to watch them develop. For me, a great long-term investment in my business.

Too many advisors with CFPs may drive down minimum asset requirements and minimum fees. A second, equally ominous trend, is the rise of the electronic advisor. In the future, investors may be able to choose between electronic advisors at 25 bps (Wealthfront, Betterment), the online advisor at 50 bps, and the face-face advisor at 100 bps. The online advisor communicates by telephone, email, text messages, and video. Investors can choose the level of service they are willing to pay for. And, investors who do not believe they are getting adequate value at 100 bps may downgrade their level of service to save money.

Add this trend to the one in Michael’s article and advisors will be facing some serious strategic issues that will impact their income and the future value of their businesses.

As the Paladin Registry mentioned (electronic advisors) Here is one way I think the industry will make up for the loss of advisors. http://www.financial-planning.com/fp_issues/44_01/high-tech-invader-to-compete-with-advisors-2687607-1.html

With the supposed estimate of 10,000 baby boomers retiring each day,there is neccesity for cfp’s

to add an additional title or even titles to their resumes.Retirement specialists,retirement

analyst.

Clients in retirement require a complicated mix of specialities that I think the industry is

behind the curve on.

Those agents who are wise,have gotten those designations to assist retirees.

Those others who have taken a 10 hour course,and expect to fool themselves and they’re clients will do nothing for themselves nor the

industry they’re in,other than be catastrophic for retirees long term financial health.