Executive Summary

The basic benefit of tax deferral on investment growth is relatively straightforward: by not paying taxes, money that would have otherwise gone to the government instead can remain invested for future growth. To the extent the money will ever be spent, the taxes must eventually be paid, but as long as additional growth can be generated in the meantime, that is a value for the investor. As a result, investors often focus on deferring capital gains, and reducing the rate of portfolio turnover.

Yet a deeper look at the actual economic value of tax deferral reveals that most of the benefit is actually lost with even low levels of turnover. An investment that changes just once a decade actually forfeits more than half of the tax deferral benefits over the span of 30 years, and for a portfolio with dividends as well, a mere 10% turnover forfeits more than 2/3rds of the tax deferral value. In a lower return environment, the true tax deferral benefit of extending the average holding period of an investment from 2 years to 5 years - chopping the portfolio turnover rate from 50% down to 20% - is actually less than 5 basis points, which can be made up in the blink of an eye through a lower cost investment change or a mere day's worth of relative returns (not to mention weeks, months, or years)!

In turn, these results suggest that in the end, investors may be grossly underestimating the damage that's done by having any portfolio turnover, and grossly overestimating the value of trying to add several years to the average holding period of an investment. Of course, high turnover investing has other costs as well, and the results don't necessarily mean that rapid trading will be fruitful. Nonetheless, the limited value of tax deferral even for an investor with a decade-long average holding period suggests that investors should be highly cautious not to sacrifice prudent investment decisions upon the altar of low-turnover tax efficiency, and that it may even be time to reconsider asset location decisions and whether equities should be held in tax-deferred accounts instead.

The Impact Of Turnover On Tax Deferral

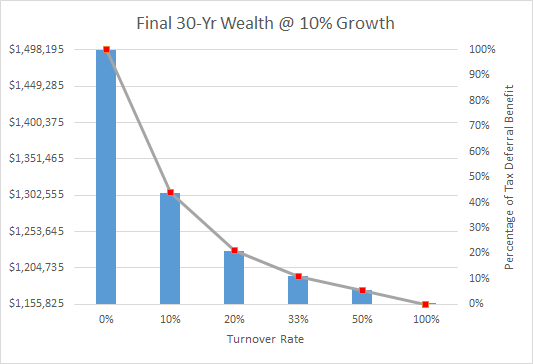

In the ideal world, a portfolio that is being invested for 30 years can actually be bought and held for the entire time horizon (0% turnover). An investor with a $100,000 stock would, assuming a 10% appreciation rate on equities for the long run, see the investment grow to a whopping $1,744,940. Assuming a 15% long-term capital gains rate on the appreciation of $1,644,940, a total of $246,741 of taxes would be due, and the after-tax value at the end of the time horizon would be $1,498,199. By contrast, if the investment's growth was taxed annually - a 100% turnover rate that results in an effective growth rate of only 8.5%/year - the after-tax value in 30 years would be $1,155,825. Thus, in essence, the "value" of tax deferral would be $342,374, which is the difference between the two scenarios. Maximizing tax deferral with 0% turnover results in a whopping 29.6% increase in wealth over the scenario with 100% turnover.

Of course, realistically most investors will likely have some amount of turnover in the range between 0% (never) and 100% (full recognition of gains every year). Accordingly, the chart below graphs the final wealth of not only 0% and 100% turnover, but also a range of other portfolio turnover rates, including 10% (every 10 years), 20% (every 5 years), 33% (every 3 years), and 50% (every other year). As indicated from the examples above, the 0% turnover portfolio results in final wealth of nearly $1.5M, the 100% turnover ends with after-tax wealth of about $1.15M, and the rest of the turnover scenarios fall in between.

Yet notably, the results reveal that the introduction of a mere 10% turnover rate actually accounts for more than half of the decline in final wealth from 0% to 100% turnover! In other words, over 50% of the "benefit" of tax deferral (the difference between the 0% and 100% turnover scenarios) is lost simply as a result of 10% turnover. The difference between 10% and 20% turnover accounts for more than half of the remaining gap as well. If we view the benefits of tax deferral as the difference between no turnover (0%) and full annual turnover (100%), it turns out that the difference between the 20% turnover and 100% turnover portfolios actually accounts for a mere 21% of the tax deferral benefit!

Or viewed another way, the 100% turnover portfolio grows at an annual rate of 8.5% (the gross of 10% minus a 15% tax drag), while the final wealth of the 0% turnover portfolio (with tax deferral benefits) is equal to 9.4%; the benefit of tax deferral was 0.9%/year of annualized return for 30 years. However, this 0.9%/year benefit of tax deferral drops to 0.44% with the introduction of "just" 10% turnover, and drops to 0.22% with 20% annual turnover. By contrast, a concerted effort to reduce portfolio turnover from 100% to 33% would result in a tax-deferral benefit of only 0.11% of annualized growth!

How Dividends Further Reduce Tax Deferral

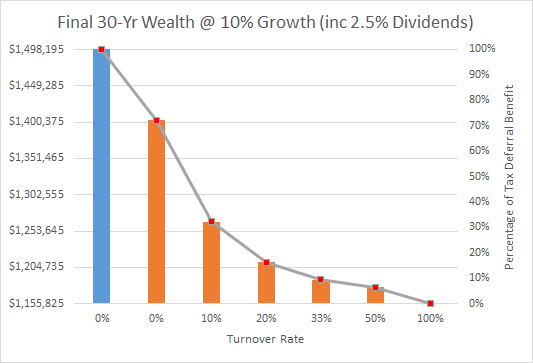

Of course, a major caveat to the scenario above is that it assumes the stock that is held pays no dividends whatsoever. While this may conceivably be true for certain high-growth stocks, ostensibly most investors will hold a more broadly diversified portfolio (or an index fund outright), which means a portion of ongoing growth will be attributable to dividends, not just capital gains. While dividends can be reinvested over the long run, the caveat to the payment of dividends is that they are taxable immediately. Thus, in essence, an investment that pays ongoing dividends in lieu of simply appreciating grows somewhat more slowly, as the dividends that are paid are taxed before they can be reinvested, not unlike turning over capital gains (and given current qualified dividend treatment, taxed similar to long-term capital gains as well).

Yet as noted in the chart above, any level of portfolio turnover that triggers taxation of ongoing growth - including in the form of stocks that pay ongoing dividends - reduces the pace of tax-deferred growth. Even with a portfolio that will otherwise be held without any sale for 30 years, the mere fact that growth is a combination of a 2.5% dividend and 7.5% annual appreciation (where dividends are taxed annually by growth is not taxed until the end) reduces the final after-tax account value to only $1,402,622. By contrast, the fully tax-deferred account was worth $1,498,199, a difference of $95,577.

Accordingly, the chart below shows again the results of a 0% turnover (and 0% dividend) portfolio (worth $1,498,199 at the end), and a 100% turnover portfolio (worth $1,155,825 at the end) as blue bars (same as above), along with a range of portfolios in orange that include a 2.5% annual dividend and the remainder taxed at the indicated turnover rate.

As the results show in this case, the impact of even a modest rate of ongoing dividends is significant. More than 25% of the loss in the value of tax deferral benefits (the difference between the 0% no dividend and 100% turnover portfolios) is attributable to the mere presence of the 2.5% dividend. When including a 10% turnover rate, more than 2/3rds of the "damage" has already been done. A portfolio with a 2.5% dividend and 20% turnover has already foregone almost 85% of the entire benefit of tax deferral! Or stated in the context of the 0.9%/year of annualized growth benefit of tax deferral over the 30 year time horizon, the benefit drops to only 0.7%/year due to the presence of dividends, and a mere 0.33% with dividends and a 10% turnover rate. Or viewed another way, reducing turnover from 100% (annual) to 10% (once a decade) still only accrues a benefit of 0.33%/year of additional growth even after 30 years!

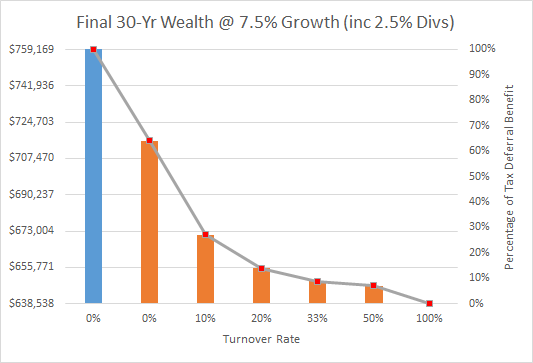

And of course, part of the benefit attributable to the tax deferral shown above is a result of what some consider to be a "generous" historical market return. If the dividend rate remains 2.5% but the appreciation rate is trimmed to only 5% (implying an expected equity total return of 7.5%/year in the future), the chart below is the result.

In this scenario, the total wealth is reduced (lower growth rate), as is the benefit of tax deferral is reduced in the first place (with less growth, there's less value to deferred taxation); the difference in wealth between 100% and 0% turnover is only 0.6%/year of annualized growth after 30 years. In addition, the consequences of even just a modest dividend and a small amount of turnover are even more severe. The presence of the dividend alone results in a loss of more than 1/3rd of the entire value of tax deferral, and the inclusion of a mere 10% turnover rate results in a loss of almost 3/4th of the entire tax deferral benefit; or viewed from the opposite end, once we include a mere 10% turnover and a 2.5% dividend, the entire value of tax deferral (over just having 100% turnover) is no more than 0.18% of annualized growth after 30 years, and only accounts for about 1/4th of the tax deferral benefits in the first place!

The table below provides a full summary of the results.

| Turnover | ||||||||

|---|---|---|---|---|---|---|---|---|

| No Dividend | With Dividends | |||||||

| 0% | 0% | 10% | 20% | 33% | 50% | 100% | ||

| 10% Growth Rate | ||||||||

| Final Wealth | $1,498,199 | $1,402,622 | $1,266,457 | $1,211,735 | $1,188,338 | $1,177,833 | $1,155,825 | |

| Annualized Return | 9.4% | 9.2% | 8.8% | 8.7% | 8.6% | 8.6% | 8.5% | |

| Tax Deferral Value | 0.94% | 0.70% | 0.33% | 0.17% | 0.10% | 0.07% | N/A | |

| Benefit Reduction | N/A | 25.5% | 64.9% | 81.9% | 89.3% | 92.8% | 100.0% | |

| 7.5% Growth Rate | ||||||||

| Final Wealth | $759,171 | $715,902 | $671,267 | $655,398 | $649,256 | $647,082 | $638,539 | |

| Annualized Return | 7.0% | 6.8% | 6.6% | 6.5% | 6.4% | 6.4% | 6.4% | |

| Tax Deferral Value | 0.62% | 0.41% | 0.18% | 0.09% | 0.06% | 0.05% | N/A | |

| Benefit Reduction | N/A | 34.0% | 71.2% | 85.0% | 90.4% | 92.3% | 100.0% | |

Practical Implications For Investors: Low Turnover Is Overrated?

The practical implications of these results are significant: notwithstanding common wisdom, there is remarkably little value to reducing portfolio turnover, unless it can be reduced all the way to zero. The presence of even the most modest of turnover - a portfolio that is changed but once a decade - forfeits over half the benefit of tax deferral, reduced even further by the presence of dividends, and further still in an environment with lower returns. Similarly, the benefit of shifting from 50% turnover to 20% turnover - normally considered quite significant, as that would increase the average holding period of an investment from 2 years to 5 years(!) - is no more than 10 basis points of annualized growth over a multi-decade time horizon. By contrast, a 10bps difference could be made up by one day's worth of relative return improvement by making an investment change, and even just switching to a similar investment with a lower expense ratio every few years can more than recover the entire benefit of tax deferral in the first place!

The significance of the tax drag of any level of turnover also potentially impacts decisions like asset location as well. Given how limited the value of tax-deferral actually is for a relatively low turnover dividend-paying portfolio, the results suggest that equities perhaps deserve a greater weighting towards tax-deferred retirement accounts than is commonly acknowledged, as the real benefits of tax deferral in a brokerage account are limited. If the tax deferral period is long enough - and returns are high enough - the benefits of equity tax deferral can even overwhelm the fact that the gains are "converted" to ordinary income, especially given that the benefits of asset locating bonds in a tax-deferred account are even more limited given today's low bond yields.

The bottom line, though, is simply this: unless equity investments will truly be held indefinitely with 0% turnover... and have little or no ongoing dividends... the true economic value of tax deferral for a low-but-not-zero turnover portfolio is quite limited. In turn, this suggests that investors should be highly cautious not to sacrifice prudent investment decisions upon the altar of low-turnover tax efficiency, as even the slightest differences in cost or relative return can easily trump the tax deferral benefit itself (though obviously, racking up transaction costs is still a return drag, and converting long-term capital gains into short-term gains has additional adverse effects. Nonetheless, the next time you're weighing the benefits of tax deferral against a prospective investment change, think twice about whether it's really worthwhile to try to defer those capital gains out to the future if there's a legitimate investment reason to make a change now. In this situation, the tax tail wagging the investment dog is unlikely to be worth it, as the real value of deferring capital gains is actually far less than most people think.