Executive Summary

If there's one thing that has remained certain in this decade of difficulty, it's the gold standard advice for retirement planning: save a healthy amount of your income, start young, invest steadily, and you'll be able to retire when you want to and enjoy the standard of living you hoped and dreamed for.

Yet the reality is that this model of retirement planning advice excellence is actually far more speculative than we have ever acknowledged, and might be better summed up as: "Save for decades, build a base, and then in the last few years, quickly double up your wealth with investment growth and retire happily." We'd never say that to our clients... yet in truth, that's exactly what we have been recommending all along!

It's one of the easiest and most basic questions in financial planning. A 20-something year old client comes in and says that she'd like to retire in 40 years with a million dollars, and wants to know how to save and invest. The advice is simple; we pull out the financial calculator, enter a "modest" growth rate of 8% for a balanced portfolio, an assumption of 40 years, a future value of $1,000,000, and press the "payment" button to solve for the amount of annual savings. The screen tells us the solution is to save about $3,600 per year, or $300 per month. Armed with this guidance, the young client goes on her merry way to a safe and successful path to retirement, comfortable in the knowledge that 40 years of diligent saving and investing will get her to her goal.

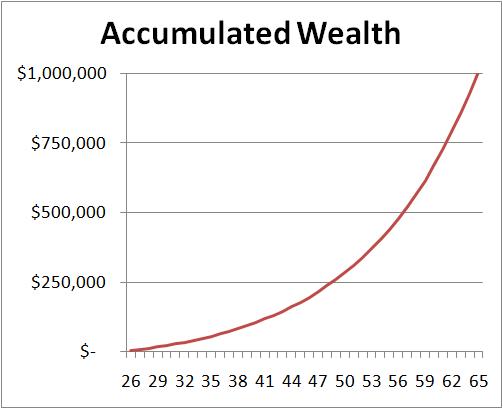

Yet in reality, what we've actually done is guide the client towards a slow steady accumulation path for the first few decades of her working career, that she must quickly double-up in the last few years to have any hope of achieving her $1,000,000 retirement savings goal on time. To understand why this is the case, here is a simple chart showing the client's accumulation over the 40 year time horizon using the basic assumptions mentioned earlier.

Yet in reality, what we've actually done is guide the client towards a slow steady accumulation path for the first few decades of her working career, that she must quickly double-up in the last few years to have any hope of achieving her $1,000,000 retirement savings goal on time. To understand why this is the case, here is a simple chart showing the client's accumulation over the 40 year time horizon using the basic assumptions mentioned earlier.

Compounding growth is a pretty amazing thing, and as financial planners we often extol the power of compounding over long periods of time. Yet we also forget just how powerful compounding is over short periods of time as well!

As the chart reveals, while it is true that the client has accumulated $1,000,000 by the end of the 40-year time horizon, it's notable that after 30 years, the client still has less than $450,000! And of course, at that point the impact of a marginal $300/month of savings is fairly negligible; the client will succeed because of the investment returns. With an assumption of "just" 8% in growth, the classic rule of 72 means the client will double her wealth in 9 years.

Accordingly, by this savings approach, the best way to have $1,000,000 in 40 years, is to have $500,000 in 31 years, and then quickly double your money in the last decade and retire!

No wonder many retirees are looking at their portfolios today and wondering how they'll ever be able to retire! Our advice to a client who planned to retire sometime this year was to accumulate $400,000 - $500,000 over the first 30 years of their lives, and then spend the 2000-2010 decade quickly doubling that wealth to their $1,000,000 retirement goal. Yet what happened instead? The markets delivered virtually flat returns over the decade, and dutiful ongoing savings in the final decade... of $300/month... did little to make up that half million dollar shortfall!

Where does this leave us? It means that we are probably far too reliant on compounding to work not just the way that it does, and we rely on the biggest part of the compounding curve to hit exactly when we need it - if we don't actually get that last doubling of 8% for the final 9 years, the retirement plan can be dramatically off track. In response, that means some clients might wish to save more, while others more realistically at least need to acknowledge how remarkably uncertain the actual retirement date will be when committing to a saving/accumulation plan of this nature.

So what do you think? Should we be communicating accumulation planning differently to clients, given how much our projections actually rely on tremendous accumulations from compounding in a very limited number of years at the end of a projection? Have you been unintentionally communicating "the best way to your retirement is to spend a few decades getting halfway there, then double up your money right at the end" to your clients?

What a fantastic post!

One of the biggest issue facing the the advice industry is that we have been far too reliant on a false sense of precision and have failed to objectively consider just how fragile many of our assumptions have been.

I am excited so see what kind of response you get from this.

Keep it my Michael!

well stated, you point out the great risk in planning for the “way out” future. this plus the risk of emotional reactions is why I think people need either a guaranteed investment OR a more consistent set of returns than offered by traditional investing.

I think this comes down in part to the fallacy of trying to predict anything too far out in time (like 40 years). It is the same with the other side of the coin and predicting income need for the rest of one’s retirement at the beginning of retirement. We’re talking about fluid situations that need constant attention and potentially constant adjustment.

I think it best to be upfront with a client and explain the realities that there is no silver bullet other than staying vigilant to one’s goals.

Great post, Michael. You are raising an extremely important topic.

I don’t think that the problem is trying to predict something too far out in time. To give effective retirement planning guidance, planners MUST do this. It’s just a reality that a retirement is something that takes a long time to plan.

The problem (in my view!) is that most of today’s retirement planning tools do not include valuation adjustments. The Lost Decade was no surprise to those who understand that valuations affect long-term returns. In fact, the return sequence we saw was a bit on the lucky side given the insane valuation levels that applied in January 2000. But most of today’s financial planners failed to warn their clients that the sorts of returns possible starting from fair valuation levels are extremely unlikely starting from insanely high valuation levels.

If you count the total return obtained over the 40-year time-period from 1970 through 2010, it was what should have been expected or better. The reason why retirement plans are not working out is that clients accepted the insane gains of the late 1990s as real. The reality, of course, is that those gains were being borrowed from investors of the 2000s. Clients are now surprised to be paying back those borrowings because the need to do so was never impressed on them (for marketing reasons).

Had those close to retirement been told in 2000 that the odds were that stocks would be paying a negative return for the next 10 years, they could have moved their money into TIPS paying 4 percent real and their retirements would be in great shape today. We need to put Buy-and-Hold behind us and start explaining to middle-class investors the many important implications of Shiller’s 1981 finding that valuations affect long-term returns.

Rob

I think we’re all finding out how difficult it is to achieve a future dollar outcome. Luck has a huge part to play.

I have a client in the last 5 years of their retirement who is very disappointed that he is now unlikely to achieve his (self chosen) future dollar target. Yet, he still has 5 years of savings to add at much lower prices. It would have been much worse for him to have been 5 years younger and actually achieved his retirement dollar target, only to then enter the Global Financial Crisis.

Despite the fact that we’d love it to be so, financial planning is not about hitting pre-determined dollar targets in the future. We are just unable to control the world that way.

It is far less precise than this. It’s part relative – where we aim to improve our clients prospects relative to all other investors, and part absolute, where we make decisions based on their personal goals and objectives. And, there’s no absolute end date (that we can confidently predict anyway).

It makes it a tough, but valuable, game that is ever evolving. I think we’ll look back in horror in 20-30 years time at the overly simplistic approaches we took to providing personal wealth management advice.

Dear Michael,

I read the NYT article about this blog post. It’s great. I thought I might point you toward two papers that consider this issue you bring up in your blog.

In a Spring 2009 article in Journal of Portfolio Management, Basu and Drew label the phenomena described in this NYT article as the ‘Portfolio Size Effect’. They actually argue because so much of the absolute returns come in the final decade, target date funds that reduce stock allocations as one approached retirement are counterproductive. A working paper of their article is at:

http://www98.griffith.edu.au/d….5971_3.pdf

I wrote a rebuttal to this, justifying target date funds (reducing stock allocation as one ages). It is scheduled for the Fall 2011 Journal of Portfolio Management, and a working paper is at:

http://ideas.repec.org/p/ngi/dpaper/10-11.html

Anyone who is using one of those simple calculators with a fixed rate of return could be in for a big shock, as accumulated wealth will not grow as neatly as your figure. You are addressing a very important issue.

Michael, remarkably revealing analysis – had not seen the physics of financial compounding “deconstructed” before and in fact I have often referenced the virtues of Rule of 72 compounding when talking to young investors….But doesn’t a robust Monte Carlo simulation model at least frame the sequence/late-state compounding risk?

Moreover, at least one variable annuity company (Allianz) that offers an accumulation rider that guarantees the highest contract value during the accumulation period (no guaranteed annual increases but a nice no-surrender walk-away feature after 10 years). I have not used it (or many VAs for that matter), but it may be a product/rider to take a hard second look at for a portion of a client’s (50ish) retirement capital based on your analysis.

Michael – This is incredibly profound. I’ve always advised younger clients to save as much as they possibly can now to potentially be able to reduce the amount they may have to save later when they have more financial obligations. Using your example, if $300 a month using a linear assumption as you’ve illustrated will give them a chance of hitting their goal, then investing $1500 a month for the first decade of their plan aggressively will allow them to potentially be able to back down their savings rate later in life once they have a few kids, etc. and the increased expenses that accompany middle-adulthood. Saving the maximum amount as early as possible is the best prescription, and can reduce the reliance on the somewhat subjective variance of future investment performance in the decade pre-retirement.

I’ll be the only one to disagree, I guess. Given that the market has never failed to return at least 7.3% annualized over *any* 40 year period, no matter how you slice it (and that includes the Great Depression!), this point, while interesting, does not really invalidate the standard investment advice. On average, even if the last 10 years are bad, those people would likely have made enough in the first 30 years to more than make up for it. We also have to keep in mind that most companies still keep paying dividends in down markets, and if these dividends are reinvested, you are effectively buying future dividends for a discount, so it’s crucial to consider total returns rather than just nominal returns. Where people run into trouble is when they deviate from the standard investment advice in response to market events, either getting greedy or panicking. But if people really did robotically invest the indicated amount every month according to the formula, they would almost certainly meet or exceed their stated goal. 40 years is an exceedingly long time in terms of the stock market. Even if we are entering a period of lower growth rates, it’s still hard to coiceive of the market underperforming over a 40 year period.

Sam,

Your comments would be correct for an investor who places a single lump sum into the market on the first day and doesn’t touch it for 40 years.

For systematic savers over that time horizon, the DOLLAR-WEIGHTED returns can be DRASTICALLY different than the TIME-WEIGHTED returns you are citing here. That’s the whole point.

If just getting an average return of 7.3% over 40 years always worked, every retiree who spends “just” a 6% withdrawal rate would finish with a giant pile of money left over, too. But that’s not the either – in fact, a 6% withdrawal rate fails almost 50% of the time.

The moment you introduce ongoing cash flows, the sequence of returns becomes extremely important. Over very long time periods with a very long series of cash flows, it can become dominating.

Simpy put, the fact that the market “averages out” over 40 years has very little impact on whether the ongoing-cash-flows result in the desired wealth. It’s a huge problem for retirees taking withdrawals, and it’s the exact same problem in reverse for savers going in.

– Michael