Executive Summary

Government bonds that pay a rate of return that adjusts with inflation to ensure investors receive a fixed, real return have been around since the late 1990s. The most popular form are Treasury Inflation Protected Securities (TIPS), which can be purchased in brokerage accounts or directly from the Treasury, are actively traded in the secondary market, and are often pooled together into increasingly popular mutual funds and ETFs as investors worry about the risk of future inflation. Yet shortly after the arrival of TIPS, the U.S. Treasury also began to issue "Series I Bonds" directly to investors; these government savings bonds were an alternative to the historical Series E/EE and H/HH bonds, but like TIPS offered a rate of return that would float with inflation and ensure a specific fixed, real rate of return.

As real interest rates declined over the past decade, and the U.S. government experienced a sharp increase in debt issuance, TIPS have become increasingly popular as a way to hedge against the risk and fear of future inflation. Given the nature of their return, arguably I bonds can do so as well, but with one notable feature that makes them quite unique: the U.S. Treasury is always available to redeem Series I bonds at their full value, which eliminates any risk that their prices could decline if/when/as interest rates rise. In addition, unlike TIPS bonds, that have some very unfavorable tax treatment (which is why they're often held within IRAs), the I bond actually accrues and compounds its interest without paying it out, which allows the investor to both avoid reinvestment risk and enjoy automatic tax deferral as long as the savings bond is held!

Given these unique features and benefits of Series I bonds, arguably financial planners and their clients should be looking more closely at I bonds (or "Ibonds"!) as a potential way to hedge inflation and rising interest rates in client portfolios, or simply to use as an alternative to cash or ultra-short-term fixed income at a more appealing yield. Unfortunately, dollar amount limitations on the purchase of I bonds restricts the extent to which they can be used, and the requirement that I bonds be held in a TreasuryDirect account (and not a standard brokerage/investment account) further limits the practicality of their use. Nonetheless, for clients who are looking to manage their exposure to inflation and rising rates, or would simply like a better return on emergency funds or short-term funds they don't plan to use for a few years anyway, perhaps it's time to give Series I bonds a closer look.

Understanding Series I Savings Bonds

Series I Bonds are a form of government (savings) bond issued by the US Treasury. Similar to TIPS (Treasury Inflation Protected Securities), they pay a rate of rate of return that is a combination of a fixed interest rate and a floating rate based on inflation (as measured by the non-seasonally-adjusted CPI-U). The effective result is that Series I Savings Bonds pay a guaranteed "real" rate of return at or above inflation (the fixed rate in excess of the floating inflation rate). However, unlike TIPS - which technically pay their stated rate of interest as interest and apply their inflation adjustments to the bond principal (which provides the inflation component of the return by lifting the price of the bond itself and also therefore the base on which interest payments are calculated) - the I Bond actually accrues and compounds both its fixed and inflation returns on the bond itself. The fixed return is set at the time the Series I Bond is issued (updated by the Treasury twice per year, in May and November), and the inflation component of the return is changed every 6 months (which month is based on when the I Bond is issued).

Unlike TIPS (which are bought and sold in the open marketplace), Series I Bonds are not marketable and instead are issued directly from, and redeemed directly to, the US Treasury, through the online TreasuryDirect website. The Treasury will only redeem I Bonds after a 1-year holding period, and apply a penalty of 3 months' worth of interest if they are redeemed within the first 5 years. Because of the fact that the US Treasury is obligated to redeem I Bonds at any time (at least after the first year), the government does place a limit on how much an individual can purchase in I Bonds: up to $10,000 per calendar year for an individual (based on his/her Social Security number, so a couple can acquire $20,000 worth). Individuals are also allowed to purchase up to $5,000 worth of paper I Bonds in a calendar year, but such purchases of paper bonds can be done only via a tax refund; for those who don't want to purchase with a tax refund, and/or don't wish to buy I Bonds in paper form and wish to keep it all on TreasuryDirect, the limit remains at $10,000/year/person. Notably, the limits apply only to the purchase of I Bonds; there is no limit on I Bond redemptions (beyond the 1-year holding requirement and the 3-month interest penalty from 1-5 years).

For tax purposes, Series I Savings Bonds are tax-deferred, and the interest is only reported when the bond is redeemed (unless an election is made to report the interest annually) or when it matures (I bonds can be held for up to 30 years). When the liquidation occurs, the interest is subject to Federal income taxes (reported by the Treasury on a Form 1099-INT), but as with all Federal government bonds, is exempt from state and local taxation.

Unique Features & Benefits Of Series I Bonds

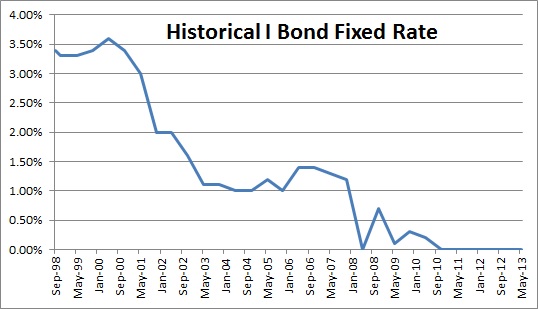

Over the past 15 years that Series I Bonds have been issued, their real (fixed) rate of return has declined significantly, along with the overall environment for real returns on bonds. While in the early years (the late 1990s) I Bonds had a fixed rate as high as 3.6% (and the total return of the I bonds included the CPI-U on top of that amount!), because the bonds are always redeemed at their current value, I bonds have not enjoyed any price appreciation through the declining rate environment as TIPS and other bonds have. On the other hand, the fact that I bonds continue to accrue interest under the terms of the bond means those early I bond investors are enjoying not only a fixed rate of 3.6% (plus inflation!) on their principal, but their interest payments are automatically reinvesting at those rates, too! (Unlike TIPS bonds, where the fixed rate of interest is paid out and must be separately reinvested, subjecting the owner to both reinvestment risk and also potential additional transaction costs.)

On the other hand, Series I bonds cannot have a negative fixed rate, which means that in today's environment - where TIPS as long as 5 years still have a negative real return - the fixed rate on the I bond is "only" 0%. In addition, if/when/as interest rates ultimately rise from here - which can cause a decline in the price of a market-traded bond - the fact that I bonds can always be redeemed with the Treasury at their accrued value means that I bond owners effectively have a guaranteed put option on the value of the bond to ensure it won't experience a price decline in a rising rate environment.

Overall, returns on Series I Savings Bonds have grown more and more mediocre over the past 15 years, as inflation has generally been low, and the fixed rate on I bonds has declined as well. Given a 0% fixed rate, an I bond buyer who purchased 1 year ago would have generated a total return of only about 1.96% (which would be 0% fixed + 1.96% as the change in CPI-U {NSA} over that time period).

US Inflation Rate data by YCharts

On the other hand, given what most investors anticipate (or at least hope!) is a trough in interest rates, I bonds function as a form of "floating rate" bond investment. If interest rates begin to rise due to rising inflation, the bonds will outright generate a higher nominal return as their interest rate rises to match a higher CPI-U. If real rates rise - such that the Treasury begins to issue future I bonds with higher fixed rates - the owner can simply redeem the bond and reinvest into a new one (albeit limit to the $10,000/person/year limitation on those new purchases). Conversely, if deflation actually sets in, the I bond is also protected; not only can the fixed rate never be negative, but if the CPI-U is negative it can never do more than offset the fixed rate (which would reduce the bond's total return to zero), which means unlike TIPS the I bond can only go up with higher inflation and cannot decline with deflation (while TIPS do have a guarantee that their principal value at maturity cannot be less than the original value of the bond, if deflation occurs for a TIPS bond that's already had positive inflation adjustments, deflation can result in a loss of those prior principal increases).

Integrating Series I Bonds Into Client Portfolios

The dollar amount restrictions on the purchase of Series I Savings Bonds will likely limit their appeal for many advisors and clients, especially higher net worth individuals for whom a $10,000 allocation (or $20,000 for a married couple) is a fairly limited slice of their overall net worth (or even "just" their bond allocation). On the other hand, given that the dollar amount limitation is annual (based on the calendar year), a married couple could purchase as much as $40,000 of Series I bonds over the next few months (using both their 2013 and soon-to-be-2014 funding options) which suddenly makes the potential allocation enough to be relevant for at least many clients. Of course, those who wish to purchase so much in I bonds must also have liquid funds available to do the purchase in the first place, and the funds must be held in a taxable account, as I bonds cannot be purchased inside of an IRA or other retirement account (nor would there be any reason to do so, since the bonds are tax-deferred anyway).

Obviously, many clients (and advisors) will not likely be "excited" to purchase bonds with a stated real return of 0% (plus the rate of CPI-U), but on the other hand for those who might be keeping a material amount of money in cash or ultra-short-term bonds anyway - perhaps fearing the risk of rising rates - the reality is that even "just" CPI is trending significantly higher than the yield on short-term fixed income. In other words, being assured of a 0% real return on a portion of the fixed income allocation might actually be better than the current alternative! And if/when rates rise and the funds can be reallocating into higher yielding options, the I bonds can be liquidated and reinvested accordingly; in essence, clients get a higher yield than short-term bonds, while still not facing any risk of price declines if rates rise (beyond the tiny 3 months of forfeited interest, which still only amounts to a fraction of 1% at today's rates).

Another way to consider fitting Series I Savings Bonds onto a client's balance sheet is to view them as an emergency fund alternative, given that I bonds maintain the principal stability of cash or a money market fund, but at a materially higher rate of return. Of course, clients considering a TreasuryDirect I bond holding as an emergency fund must remember that the funds will be illiquid for the first 12 months - so be certain there's an alternative to access needed funds in the meantime! - and also that checks cannot be written directly against a TreasuryDirect account (so realize that in a true emergency, it may still take a few days to liquidate and transfer money to another bank account to fund an emergency expense). Nonetheless, for those that can navigate these kinds of short-term cash flow timing concerns, I bonds arguably just represent a higher return money market alternative.

For other clients, the best fit for Series I bonds may be not as an emergency fund alternative, but as a TIPS alternative for those who are concerned about rising rates. Given today's real yield curve for Treasuries, I bonds offer a better fixed rate than 5-year TIPS, have more favorable tax treatment (tax-deferral of all growth, which helps shelter both interest payments and the "phantom income" for TIPS principal adjustments), are less sensitive to rising rates (as I bonds effectively have a duration of 0, while 5-year TIPS have at least some exposure to rising rates), and can be cheaper to acquire and invest in (I bonds are purchased with no expenses or transaction charges, while TIPS not purchased at auction face potential bond trading costs, bid/ask spreads, and/or mutual fund or ETF expense ratios). On the other hand, for the true hold-to-maturity 30-year investor, it's notable that TIPS provide a far more appealing real yield of almost 1.5% (compared to the 0% on I bonds), and don't have the dollar amount purchase limitations.

For clients who are especially interested in buying more I bonds, it's notable that the $10,000 limit is effectively increased to $15,000 given the rule allowing up to $5,000 of paper I bonds to be purchased with a tax refund. Clients who are especially eager to purchase Ibonds may even wish to "overpay' on 4th quarter estimated taxes, just to get a tax refund to purchase TIPS (and may wish to file quickly if they do so, as this strategy also means clients will be without the use of their money or any interest it may generate during the intervening time period).

Ultimately, it's important to remember that I bonds are not true floating rate funds, as while the interest rate can rise with inflation, the fixed rate remains locked in (for 30 years!) at the time of purchase, unless redeemed and reinvested (which subjects the buyer to the dollar amount limitations again). Nonetheless, for those who fear the potential that inflation itself may drive interest rates higher, the I bond provides a unique alternative way to hedge the risk and allow the investor's rate of return to rise, and without the bond price risk of rising rates. Similarly, in the event that real yields rise, I bond buyers again are hedged against the risk of price declines thanks to the implied put option of being able to redeem the bond with the U.S. Treasury at any time for full value and reinvest in the future into new I bonds at higher rates (or simply other then-higher-yielding fixed income alternatives).

Given that Series I Savings Bonds must be held in a client's own TreasuryDirect account - and not via a traditional brokerage/investment account - the option may be somewhat less appealing than just buying TIPS, as that impacts the advisor's ability to easily buy/sell investments on behalf of clients and to rebalance portfolios, not to mention charging fees on assets under management itself. Nonetheless, in today's environment there are unique benefits that Ibonds can provide, which TIPS do not, and given that for some clients the dollar amounts may simply be carved out of funds they already hold in cash and liquid alternatives anyway, perhaps Series I bonds deserve a closer look for many clients and their portfolios.

I do think it’s a reasonable suggestion, but it’s more for do it yourselfers than it is for clients who want someone else to take care of their money. I have a treasury direct account myself and converted all my paper EE bonds and my experience is that it’s not the easiest way to invest.

I have heard that starting in January, the Treasury will be offering actual Floating Rate Notes.

http://www.treasurydirect.gov/instit/statreg/auctreg/FRNTermSheet.pdf

Michael..very interesting and timely piece..As a matter of fact, yesterday I had conversatons with a friend on scenarios of raising inflation in US snd he mentioned about David Rosenberg’s recent interview on inflation in US and he expects to raise higher by as early as 2014. I have few clients for whom we have allocated TIPS in their portfolios. One of them is a Dubai Non Resident Indian and as you know the cuurency is pegged to the dollar. He is going to be working in Dubai for next 15-18 years and was wondering whether will he be eligible to buy I bonds, since he needs to purchase from Treasury Directly as a retail foreign investor. It will be great, if youcould

Another benefit of I Bonds: One can exclude the interest earned on the redemption of I Bonds from Federal income tax when the funds are used for college tuition and educational expenses (provided the bond holder’s income didn’t exceed certain thresholds).

It’s interesting that Dr William Bernstein placed I-bonds and TIPS behind equities as inflation fighters:

“The best insurance against inflation, he says, is a globally diversified stock portfolio with an extra pinch of gold-mining and natural-resource companies. Treasury inflation-protected securities, U.S. bonds whose value rises with the cost of living, also can help.”

Source:

‘Shallow Risk’ and ‘Deep Risk’ Are No Walk in the Woods

http://blogs.wsj.com/moneybeat/2013/07/26/shallow-risk-and-deep-risk-are-no-walk-in-the-woods/

Avi Oren, retired CFP, MBA, M. Sc (Biomedical engineering)

Great post. I suggested Ibonds as gift on my blog about a year ago http://www.pdxfis.com/i-bonds-a-great-gift-to-children-and-grandchildren/. Great for paying future college expenses.